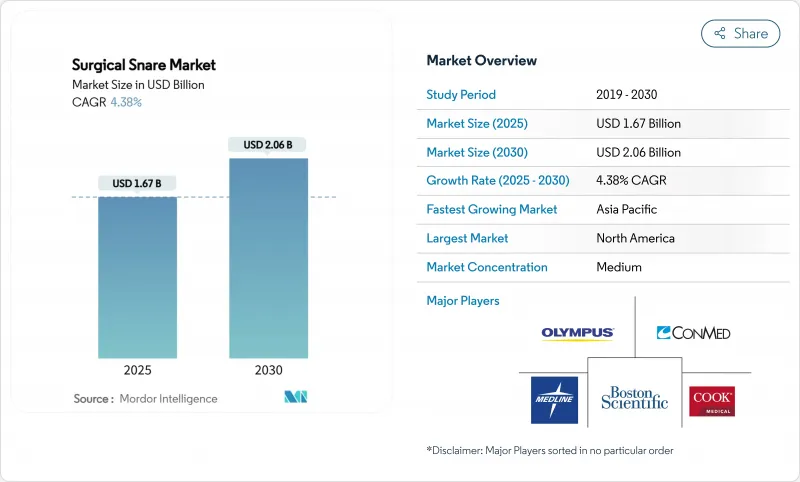

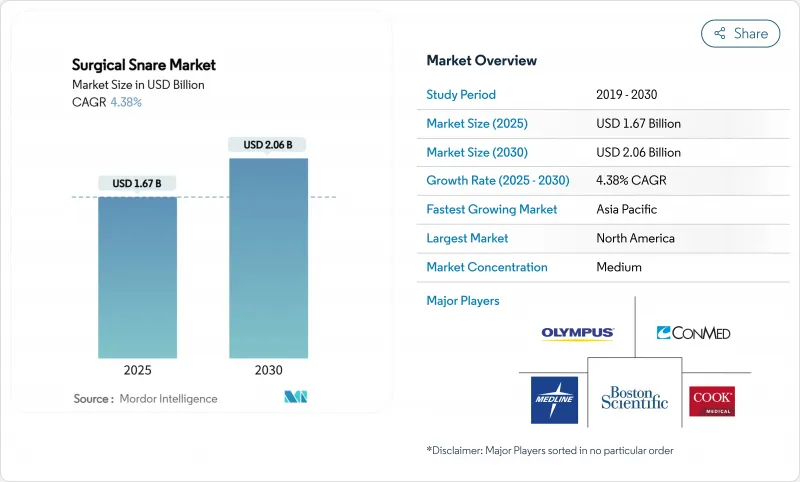

외과용 스네어 시장은 2025년에 16억 7,000만 달러에 이르고, 2030년에는 20억 6,000만 달러에 달할 것으로 예측됩니다.

성장은 대장암 검진 증가, AI 지원 검출 시스템의 광범위한 채용, 안전성 프로파일을 향상시키는 콜드 스네어 폴리펙토미로의 전환과 일치합니다. 외래 수술 센터(ASC)는 현재 미국 수술의 72%를 병원보다 45-60% 낮은 비용으로 실시하고 있으며, 일회용 스네어에 대한 수요가 급증하고 있습니다. 고령화에 의한 인구동태의 추풍이 수술건수를 한층 더 유지하는 한편, 기술 리더는 가격경쟁보다 형상의 최적화나 인공지능에 의해 차별화를 도모하고 있습니다. 최근의 일회용 가이드 시스킷의 리콜을 포함한 품질 보증의 과제는 채용 궤도를 지키기 위한 견고한 임상 근거와 시판 후 감시의 필요성을 강조하고 있습니다.

회복 속도와 합병증 발생률이 낮은 환자의 요구에 따라 수술 건수는 내시경 기술로 이동하고 있습니다. 현재 장치의 요구 사항은 작은 루멘을 통해 조직을 정확하게 캡처하는 데 중점을두고 있으며 로봇 지원 플랫폼과 호환되는 콜드 스네어 디자인이 선호되고 있습니다. 현재 17개 로봇 내시경 시스템이 개발 중이며 9개 시스템이 승인 신청 중입니다. ASC는 이 동향을 활용하여 증례를 유치하고 있으며, 향후 10년간 25%의 증례 수 증가를 예측했습니다. 임상의는 무균성을 보장하기 위해 단일 청소년 스네어를 표준화하기 때문에 이러한 경향은 외과용 스네어 시장을 밀어 올립니다. 스네어에 AI 대응의 시각화를 번들하는 벤더는 가치 중시의 의료 시스템으로 한층 더 견인력을 획득합니다.

2023년에 새로운 30건의 소화기 ASC가 개설되어 입원 환자 환경으로부터의 구조적 변화를 나타냈습니다. CMS는 부위 중립 상환을 지지해 2025년에 2.6%의 ASC율 갱신을 계획, 지불 총액은 74억 달러로 증가할 것으로 예상됩니다. 민간 자본을 통한 자금 조달은 대도시 지역의 네트워크 구축을 가속화하고 일회용 스네어의 표준 구매를 증가시킵니다. ASC는 신속한 회전과 감염 대책을 중시하기 때문에 외과용 스네어 시장의 일회용 분야는 재사용 가능 영역보다 빠르게 확장됩니다. 관리자가 재고의 단순화를 요구하기 때문에 기술에 특화된 키트를 설계하는 제조업체가 구입을 선호하고 있습니다.

콜드 스네어법에서는 즉시 출혈이 10.8%인 반면, 핫 스네어법에서는 3.2%를 나타낼 전망입니다. 따라서 책임 추구는 기구의 선택과 훈련의 필요성에 영향을 미칩니다. 규제 당국은 특히 유럽 의료기기 규정(European Medical Device Regulation) 하에서 안전성 데이터의 충실을 의무화하는 등 임상 증거에 대한 요구를 강화하고 있습니다. 확립된 감시 시스템과 엄격한 시판 후 후속업체를 갖춘 제조업체는 이 장애물에도 불구하고 자본을 획득했습니다. 신흥 시장은 긴급시의 용량이 제한되어 있어 위험을 더욱 날카롭게 느끼고 있으며 대량생산센터에서의 단기적인 섭취를 억제하고 있습니다.

2024년 외과용 스네어 시장 점유율의 68.36%를 일회용 기기가 획득했습니다. 2030년까지 연평균 복합 성장률(CAGR)은 4.89%를 나타내 감염 관리의 의무화가 치료당 비용 우려를 상회할 것으로 예측됩니다. 재사용 가능한 내시경으로 인한 최근의 오염 사고는 구매자를 일회용 옵션으로 향하게 합니다. 그러나 폐기물 관리 비용이 증가하고 2026년 8월에 발효된 유럽의 새로운 포장 규칙은 일회용 모델에 대한 지속가능성의 압력을 낳고 있습니다. 카디널 헬스사는 2024년에 1,830만개의 일회용 제품을 리사이클용으로 회수하여 새로운 순환형 경제에 대한 대응을 나타냈습니다.

재사용 가능한 스네어는 유효한 멸균 워크플로우를 운영하는 대량 처리 센터에서 여전히 중요합니다. 이러한 시설에서는 일회용 십이지장 내시경의 수술당 비용 797-4,400달러에 비해 평생 비용이 낮다고 강조하고 있습니다. 그러나 EU의 의료기기 규정 준수에 따라 재사용할 수 있는 비용은 지속적인 검사 비용이 들고 절약 격차가 줄어듭니다. 현재의 보급 곡선을 감안하면, 일회용 기기의 외과용 스네어 시장 규모는 2030년까지 13억 달러를 넘어 증수분의 대부분을 차지하게 됩니다. 의료 제공업체는 매립지에 미치는 영향을 줄이기 위해 환경 친화적 인 재료를 추구하고 있으며 공급업체는 생분해 성 고분자를 탐구하고 있습니다.

타원형 디자인은 2024년에 41.28% 시장 점유율을 차지했으며, 의사가 익숙해지고 병변에 대한 적용 범위가 넓다는 것을 뒷받침했습니다. 그러나 편평한 병변에서의 탁월한 캡처 효율과 오른쪽 결장에서의 우수한 인체공학은 크레센트 디자인이 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 4.73%를 나타낼 전망입니다. 초기 임상 증거에 따르면 크레센트 스네어는 측면으로 퍼지는 종양의 완전 절제율을 향상시키고 있습니다. 벤더는 조직 그립을 강화하기 위해 마이크로 톱니 모양의 와이어 에지를 통합하여 대응합니다.

특수 쉴드 및 육각형은 틈새 해부학 시나리오에 해당하지만 외과용 스네어 시장에서 차지하는 비율은 작습니다. Exacto Cold Snare의 쉴드 형상은 기존의 타원형이 79%인 반면 91%의 완전 절제를 가져오고 형상 최적화로 인한 성능 향상을 강조합니다. AI 유도 네비게이션 시스템 수요는 알고리즘이 예측 가능한 곡률 프로파일을 가진 장치를 선호하기 때문에 모양 특이적 스네어의 채택을 가속화할 수 있습니다. 이러한 혁신이 성숙함에 따라 초승달 디자인의 외과용 스네어 시장 규모는 2030년까지 5억 9,000만 달러에 달할 가능성이 있습니다.

외과용 스네어 시장은 용도별(재이용 가능 외과용 스네어, 단회 사용 외과용 스네어), 형상별(타원형, 초승달형, 기타), 최종 용도별(소화기 내시경, 복강경, 기타), 최종 사용자별(병원, 외래 수술 센터(ASC), 전문 클리닉), 지역별(북미, 유럽)

북미는 성숙한 스크리닝 프로그램, 견고한 ASC 인프라, AI 의사결정 지원의 조기 도입에 힘입어 2024년 매출의 43.26%를 차지하며 선두에 올랐습니다. 2030년까지의 성장률은 4.2%에 그치지만, 이는 가치관에 근거한 의료가 높은 절제 완전성과 낮은 합병증 발생률에 보상하기 때문입니다. 안전 리콜과 관련된 FDA 모니터링을 통해 공급업체는 투명성이 뛰어난 실제 세계 증거가 있는 제조업체를 지지하게 됩니다. 북미의 외과용 스네어 시장 규모는 2030년까지 8억 3,000만 달러 이상에 달할 것으로 예상되며, 단일 청소년 보급률은 75%를 초과합니다.

유럽은 EU 의료기기 규제를 중심으로 한 고급 규제 환경에 있습니다. 승인 비용의 상승은 적합 공급업체에 경쟁력을 가져오는 반면, 환경 정책에 의해 2026년부터는 재활용 가능한 포장이 의무화됩니다. 독일, 프랑스, 북유럽 국가들은 AI CAGe 시스템에 대한 투자를 계속하고 있으며, 상환의 역풍에도 불구하고 외과용 스네어 시장의 CAGR은 4.1%를 나타낼 전망입니다. 병원은 증거에 뒷받침된 스네어 디자인과 트레이닝 서비스를 확보하기 위해 다년간의 전략적 계약을 맺는 경우가 늘고 있습니다.

아시아태평양은 인프라 확장 및 스크리닝 가이드라인 채택으로 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 5.76%를 나타낼 전망입니다. 중국은 계속 커뮤니티 검진 프로그램을 시험적으로 실시하고, 일본은 2024년에 AI 대장 내시경 검사 도구를 상환하기로 결정하고 기술 수요를 밀어 올렸습니다. 태국과 인도네시아에서는 비용에 대한 민감성이 지속되고, 구매자는 가치 엔지니어링 장치로 방향타를 끊습니다. 현지 제조 파트너십은 수입 관세를 줄이고 지역 경쟁력을 강화합니다. 2030년까지 아시아태평양은 세계의 외과용 스네어 시장 수익의 30%에 기여하여 북미와의 차이를 줄일 수 있습니다.

The surgical snare market stands at USD 1.67 billion in 2025 and is projected to reach USD 2.06 billion by 2030, reflecting a steady 4.38% CAGR.

Growth aligns with rising colorectal-cancer screening volumes, broader adoption of AI-assisted detection systems, and the transition toward cold-snare polypectomy that improves safety profiles. Ambulatory surgery centers (ASCs) now perform 72% of United States procedures at 45-60% lower costs than hospital settings, sharply increasing demand for single-use snares. Demographic tailwinds from aging populations further sustain procedure volumes, while technology leaders differentiate through shape optimization and artificial intelligence rather than price competition. Quality-assurance challenges, including recent recalls of single-use guide sheath kits, underscore the need for robust clinical evidence and post-market surveillance to protect adoption trajectories.

Patient demand for faster recovery and lower complication rates is shifting procedural volumes toward endoscopic techniques. Device requirements now emphasize precise tissue capture through small lumens, favoring cold-snare designs compatible with robotic-assisted platforms. Seventeen robotic endoscopy systems remain under development, while nine hold regulatory approval. ASCs leverage this trend to attract cases, forecasting 25% volume growth over the next decade. The preference boosts the surgical snares market as clinicians standardize on single-use snares to secure sterility. Vendors that bundle AI-enabled visualization with snares gain additional traction in value-focused health systems.

Thirty new gastrointestinal ASCs opened in 2023, illustrating a structural shift away from inpatient settings. CMS supports site-neutral reimbursement and plans a 2.6% ASC rate update for 2025, raising total payments to USD 7.4 billion. Private-equity funding accelerates network build-out in metropolitan areas, increasing standardized purchasing of disposable snares. Since ASCs emphasize quick turnover and infection control, the single-use segment of the surgical snares market expands faster than the reusable segment. Manufacturers that design procedure-specific kits gain purchasing preference as administrators seek inventory simplification.

Cold snare techniques record 10.8% immediate bleeding compared with 3.2% for hot snare use, though delayed bleeding rates favor cold techniques. Liability exposure therefore influences device selection and training requirements. Regulators intensify clinical-evidence demands, particularly under the European Medical Device Regulation that mandates enhanced safety data. Manufacturers with established surveillance systems and rigorous post-market follow-up capitalize despite the hurdle. Emerging markets feel the risk more acutely due to limited emergency capacity, which moderates short-term uptake in high-volume centers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Single-use devices captured 68.36% of the surgical snares market share in 2024. The segment should advance at 4.89% CAGR to 2030 as infection-control mandates override per-procedure cost concerns. Recent contamination incidents involving reusable endoscopes push purchasers toward disposable options. However, rising waste management costs and new European packaging rules effective August 2026 create sustainability pressures on single-use models. Cardinal Health collected 18.3 million single-use items for recycling in 2024, showcasing emerging circular-economy responses.

Reusable snares remain relevant in high-volume centers that operate validated sterilization workflows. These facilities highlight lower lifetime costs compared with the USD 797-USD 4,400 per procedure expense for single-use duodenoscopes. Yet EU Medical Device Regulation compliance raises ongoing testing costs for reusables, narrowing the savings gap. Given the current adoption curve, the surgical snares market size for single-use devices will surpass USD 1.3 billion by 2030, representing a majority of incremental revenue. Providers increasingly demand eco-friendly materials to mitigate landfill impact, prompting vendors to explore biodegradable polymers.

Oval designs held 41.28% market share in 2024, underscoring physician familiarity and broad lesion applicability. Crescent designs, however, post the fastest 4.73% CAGR to 2030 due to superior capture efficiency in flat lesions and favorable ergonomics in the right colon. Early clinical evidence shows crescent snares improving complete resection rates for lateral spreading tumors. Vendors respond by integrating micro-serrated wire edges to enhance tissue grip.

Specialized shield and hexagonal shapes address niche anatomical scenarios but account for a smaller slice of the surgical snares market. The Exacto Cold Snare's shield shape yielded 91% complete resection versus 79% for traditional ovals, highlighting the performance boost that shape optimization can deliver. Demand for AI-guided navigation systems could accelerate adoption of shape-specific snares because algorithms prefer devices with predictable curvature profiles. As these innovations mature, the surgical snares market size for crescent designs could reach USD 590 million by 2030.

The Surgical Snare Market is Segmented by Usability (Reusable Surgical Snares, Single-Use Surgical Snares), by Shape (Oval, Crescent, and More), by Application (Gastrointestinal Endoscopy, Laparoscopy, and More), by End-User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), by Geography (North America, Europe, Asia-Pacific, and More).

North America led with 43.26% of 2024 revenue, underpinned by mature screening programs, robust ASC infrastructure, and early adoption of AI decision support. Growth through 2030 sits at 4.2% as value-based care rewards high resection completeness and low complication rates. FDA scrutiny following safety recalls prompts providers to favor manufacturers with transparent real-world evidence. The surgical snare market size in North America is expected to exceed USD 830 million by 2030, with single-use penetration topping 75%.

Europe presents a sophisticated regulatory environment anchored by the EU Medical Device Regulation. Higher approval costs create competitive moats for compliant suppliers, while environmental policy drives recyclable packaging mandates starting 2026. Germany, France, and the Nordic region continue to invest in AI CADe systems, positioning the surgical snare market for steady 4.1% CAGR despite reimbursement headwinds. Hospitals increasingly sign multiyear strategic agreements to secure evidence-backed snare designs and training services.

Asia-Pacific posts the fastest 5.76% CAGR through 2030 due to infrastructure expansion and screening guideline adoption. China continues to pilot community screening programs, and Japan's decision to reimburse AI colonoscopy tools in 2024 boosts technology demand. Cost sensitivity persists in Thailand and Indonesia, steering buyers toward value-engineered devices. Local manufacturing partnerships reduce import duties and strengthen regional competitiveness. By 2030, Asia-Pacific could contribute 30% of global surgical snare market revenue, narrowing the gap with North America.