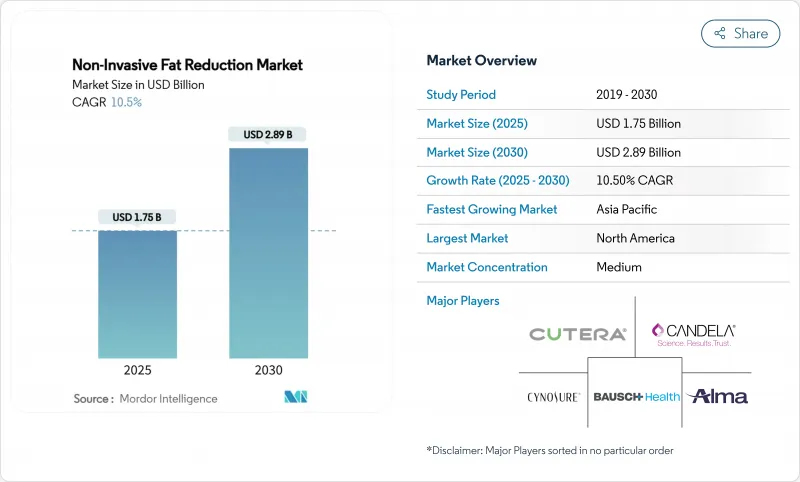

비침습적 지방 감소 시장은 2025년 17억 5,000만 달러에 달하고, 2030년에는 28억 9,000만 달러에 이를 것으로 예측되며, CAGR은 10.50%를 나타낼 전망입니다.

GLP-1 체중 감량 약물은 피부 느슨함을 드러내고 환자가 장비 기반 조각 솔루션을 통해 수정을 원하기 때문에 수요가 가속화됩니다. Cryolipolysis(Cryolipolysis)의 채용이 정착되어 있지만, 고강도 집속 전자파(HIFEM) 시스템은 지방의 아폽토시스와 보이는 근육의 긴축을 결합하여 점유율을 획득하고 있습니다. 특히 메도스파 체인을 통한 Tier2 도시에의 프로바이더 진출은 액세스와 가격의 투명성을 향상시킵니다. AI 가이드를 통한 바디 스캔은 치료 계획의 정확성을 높이고 남성 고객 기반 증가는 비침습적 지방 감소 시장 전체를 확대합니다.

GLP-1 처방의 광범위한 증가는 급속한 지방 감소가 윤곽 수정을 필요로 하는 잔류 이완을 드러내기 때문에 보조 수요를 증가시킵니다. 무작위화 시험은 이러한 작용제가 근육보다 지방량을 감소시키는 것으로 확인되었으며, 장비 플랫폼이 대응하는 특이적인 스컬프팅 요구를 생성합니다. 제공업체는 약물 요법, 영양 요법, 크리오리포라이시스 또는 HIFEM 세션을 동기화하는 조합 프로그램을 판매하여 약물 요법 환자를 효과적으로 미용 고객으로 바꿉니다. 신체의 윤곽 형성은 단계적인 사이클에서 이루어지기 때문에 이 접근법은 경상적인 수익을 유지합니다. 그러나 보험사가 GLP-1 치료제의 보험 적용에 소극적이기 때문에 하류 기기 도입이 억제될 수 있어 일괄 치료를 위한 유연한 자금 조달 모델의 중요성이 부각되고 있습니다.

규모를 확장하는 체인은 브랜드화되고 표준화된 치료 메뉴를 지금까지 충분한 서비스가 제공되지 않았던 2차 도시와 교외 회랑에 가져옵니다. 부동산 경비 절감과 민첩한 인력 배치 구조는 품질을 떨어뜨리지 않고 경쟁력 있는 가격 설정을 가능하게 하는 유닛 이코노믹스를 지원합니다. 프랜차이즈 플랫폼은 스킨 케어, 레이저, 웰니스 멤버십을 교차 셀링하고 비침습적 지방 감소 시장을보다 광범위한 라이프 스타일 제안에 통합합니다. 컨솔리데이터는 집중 교육과 공유 서비스 조달을 채택하여 마진을 보호하면서 지리적 침투를 가속화하고 있습니다. 이 모델은 보다 광범위한 인구층과 가격대에 수익원을 분산시킴으로써 불황 위험을 헤지합니다.

평균 가격은 바디 존당 750달러에서 4,000달러로, 여러 주기와 영역을 치료하는 경우 풀코스는 1만 달러를 넘는 경우가 많습니다. 주요 보험 회사는 장비에 의한 지방 감소를 선택적 치료로 분류하고 있으며 환자는 자기 자금으로 이루어집니다. 따라서 가처분 소득의 변동은 예약 의도에 영향을 미칩니다. 공급자의 데이터에 따르면 거시 경제가 불안정한 시기에 예약 취소가 급증합니다. 클리닉은 현재 핀텍 기업과 제휴하여 0%의 할부 플랜을 제공하고 있지만, 젊은 소비자에게는 신용 승인이 여전히 장벽이 되고 있으며, 비침습적 지방 감소 시장의 보다 넓은 중간층으로의 침투를 늦추고 있습니다.

크리올리포라이시스는 2024년 장비 수익의 42.35%를 유지해 10년 동안 안전하고 이해하기 쉬운 워크플로우가 신규 및 베테랑 의료 제공업체 모두에게 호소했습니다. 그럼에도 불구하고 HIFEM 시스템의 CAGR은 18.25%를 나타낼 전망입니다. HIFEM 시스템은 세포 사멸 지방 세포와 비대근 섬유라는 두 가지 생물학적 표적을 동시에 다루기 때문입니다. 시술 후 초음파 영상에서는 4회 시술로 근육이 16% 증가하고 국소지방이 19% 감소했습니다. 이 전반적인 결과는 소셜 미디어 피트니스 인플루언서에 의해 형성된 환자의 기대와 일치합니다. 전자기 플랫폼에 의한 비침습적 지방 감소 시장 규모는 재활 통증의 적응이 보험 코드를 획득하면 더욱 확대될 것으로 예측됩니다. 고밀도 초점 초음파(HIFU)는 피부 탄력 틈새 시장에서 경쟁하고 낮은 수준의 레이저 빛은 실질적으로 가동 중지 시간이없는보다 부드러운 대사 조절을 원하는 고객에게 호소합니다. 이러한 방식으로 각 모달리티는 성능 대 편안함이라는 명확한 위치를 차지하며 클리닉이 맞춤형 계획을 위해 여러 시스템을 재고하도록 권장합니다.

바이 모달 콤비네이션은 견인력을 증가시키고 있습니다. 지방 용해 냉각 전에 지방 세포의 감수성을 높이기 위해 고주파열을 거듭하거나 지방 용해 후 피부의 탄력을 높이기 위해 HIFEM과 RF-마이크로니들을 연속적으로 실시합니다. 조기의 채용 예에서는 2개의 기기를 큐레이션된 "트랜스포메이션 저니"에 패키지화하면, 고객 1인당의 평균 매출이 30% 높아진다고 보고하고 있습니다. 한편, 주사 가능한 아이스 슬러리는 여전히 인체 실험 중이지만 시술 당 소모품 비용을 낮추면 자본 집약적 인 플랫폼을 파괴 할 수 있습니다. 따라서 제조업체는 미래의 상품화를 피하기 위해 파이프라인의 연구 개발을 가속화하고 있습니다. 기술의 다양화로 인해 비침습적 지방 감소 시장은 반복적 업그레이드가 자본지출주기의 반복에 박차를 가하는 역동적인 시장으로 확고해지고 있습니다.

피부과와 미용 클리닉은 의사의 신뢰와 임상 감독으로 2024년 매출의 54.53%를 달성했습니다. 그러나 접객 디자인, 웰니스 소매, 회원제 과금을 통합한 메드스파는 CAGR 17.85%를 나타낼 전망입니다. 대부분의 의료기기는 법적으로 인증 외과 의사의 감독을 필요로 하지 않기 때문에 기업이는 원격 감독 계약에 따라 운영되는 의사 조수와 간호사를 직원으로 여러 단위의 발자국을 확대할 수 있습니다. Tier-2 도시에서는 임금 격차가 작고 디지털 마케팅도 일원화되어 고객 획득 비용이 절감되고 EBITDA 마진은 20%를 넘습니다.

병원은 마취와 집학적 애프터 케어가 필요한 복잡한 지방 부종과 비만 후 윤곽의 경우에 전문화하는 경향이 있습니다. 피트니스 센터는 대조적으로 즉각적인 시각 피드백을 추구하는 충동적인 구매자를 캡처하는 근력 훈련 지역 근처에서 추가 cryolipolysis 포드를 테스트합니다. 비침습적 지방 감소 업계는 또한 성형외과의사가 수술실과 장비 스위트를 병설하고 환자 파이프라인을 상호 수분시키는 하이브리드 '외과 스파'의 증축을 볼 수 있습니다. 프라이빗 에퀴티로부터의 자금 유입은 2020년부터 2024년 사이에 400건의 메디스파 거래로 31억 달러를 넘어 확장 가능한 미용 의료에 대한 기관 투자자의 확신을 뒷받침했습니다. 이 유동성은 평생 가치 추적, 예약 알림 자동화, 보조 스킨 케어 라인의 업셀을 수행하는 CRM 플랫폼에 자금을 공급하여 수십 년에 걸친 고객과의 끈끈한 관계를 견고하게 만듭니다.

북미는 2024년 수요의 38.63%를 차지했습니다. 이는 확립된 메디컬 스파의 밀도, 높은 재량 소득, FDA의 투명성이 높은 패스웨이가 시장 출시를 가속하고 있기 때문입니다. 미국은 지역 수익의 80% 이상을 차지하고 있으며 캐나다와 라틴아메리카의 의료 관광을 통해 다른 곳에서는 사용할 수 없는 독자적인 크라이오리포라이시스 어플리케이터가 증폭되고 있습니다. 대사 증후군 사례에서 클라이오리폴라이시스를 커버하는 상환 조종사는 절차의 가치를 더욱 정당화하고 결과가 심혈관계에 대한 이익을 입증하면 보다 광범위한 지불자의 견인력을 풀어낼 수 있습니다. 디지털 헬스 신흥기업은 시술 후 모니터링용 웨어러블을 통합하여 후속 스케줄링을 정교하게 하는 종단적인 데이터를 임상의에게 제공합니다.

유럽은 의료기기 규제 프레임워크에서 고도로 규제된 기기 승인을 특징으로 하는 두 번째로 큰 슬라이스를 차지합니다. 독일, 프랑스, 영국이 중심 소비국이지만, 남유럽 국가들은 관광 중심 경제가 '휴가+치료' 패키지를 판매하기 때문에 평균 이상의 성장을 보이고 있습니다. 엄격한 광고 규제로 인해 과도한 홍보 불만이 제한되기 때문에 브랜드는 검토를 거친 입증 자료를 공개하지 않을 수 없으며 소비자의 신뢰를 부주의하게 높입니다. 클리닉은 에너지 효율적인 발전기와 재활용 가능한 젤 패드를 선호하며 라이프사이클 배출량이 적다는 것을 증명하는 공급업체는 시장에서 차별화됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 12.27%를 나타내 가장 급성장하고 있는 지역으로 중산계급의 인구확대와 도시지역의 외모의식의 고조가 그 원동력이 되고 있습니다. 중국은 조사 대상이 된 미용 소비자의 91%가 거시 경제의 변동에도 불구하고 지출을 유지하거나 증가 할 예정이며 수량으로 선도하고 있습니다. 일본은 세션 설정 시간을 40% 단축하는 로봇 지원 어플리케이터 암으로 대표되는 혁신을 진행하고 있습니다. 한국은 K뷰티 프로토콜을 수출해 동남아 전역에서 채용되고 있는 콤비네이션 테라피의 청사진을 보급시킵니다. 인도의 젊은 인구층은 민간 병원의 급속한 건설과 함께 장비 수입 관세가 완화되면 큰 업사이드를 가져옵니다. 호주는 지리적 거리를 채우기 위해 원격 의료 컨설팅을 활용하여 환자 퍼널 관리를 최적화합니다.

남미와 중동 및 아프리카는 신흥의 핫스팟으로, 브라질과 아랍에미리트(UAE)은 현지 미용 성형 수술을 대체하는 저렴한 시술을 지지하고 있습니다. 환율 변동과 관세가 도입의 장애물이지만, 숙박과 치료를 결합한 의료 투어리즘 번들은 고액의 치료비 부담을 경감합니다. 모든 지역에 걸쳐, 지역별 규제의 명확성과 임상가 교육은 비침습적 지방 감소 시장 확대의 결정적인 결정 요인으로 계속되고 있습니다.

The non-invasive fat reduction market is valued at USD 1.75 billion in 2025 and is forecast to reach USD 2.89 billion by 2030, advancing at a 10.50% CAGR.

Demand accelerates as GLP-1 weight-loss drugs expose skin laxity that patients want corrected by device-based sculpting solutions. Cryolipolysis holds entrenched adoption, yet high-intensity focused electromagnetic (HIFEM) systems capture share by pairing fat apoptosis with visible muscle toning. Provider expansion into tier-2 cities, particularly through medspa chains, improves access and price transparency. AI-guided body scanning tightens treatment planning precision, while a growing male customer base broadens the overall non-invasive fat reduction market universe.

Widespread GLP-1 prescription growth lifts ancillary demand as rapid fat loss reveals residual laxity requiring contour correction. Randomized trials confirm these agonists reduce fat mass more than muscle, creating specific sculpting needs that device platforms address. Providers market combination programs that synchronize medication, nutrition, and cryolipolysis or HIFEM sessions, effectively converting pharmacotherapy patients into aesthetic clients. The approach sustains recurring revenue because body contouring is performed in staged cycles. However, insurer reluctance to cover GLP-1 drugs may temper downstream device uptake, highlighting the importance of flexible financing models for bundled care.

Scaling chains bring branded, standardized treatment menus to previously under-served secondary metros and suburban corridors. Lower real-estate overhead and agile staffing structures underpin unit economics that support competitive pricing without quality compromise. Franchised platforms cross-sell skincare, laser, and wellness memberships, embedding the non-invasive fat reduction market into a broader lifestyle offering. Consolidators employ centralized training and shared-service procurement to protect margins while accelerating geographic penetration. The model hedges recession risk by diversifying revenue streams across a wider demographic and price spectrum.

Average pricing ranges from USD 750 to USD 4,000 per body zone, with full courses often exceeding USD 10,000 when multiple cycles and areas are treated. Major insurers classify device-based fat reduction as elective, leaving patients to self-finance. Disposable income volatility therefore influences booking intent; provider data show appointment cancellations rise sharply during macro-economic uncertainty. Clinics now partner with fintech firms to offer 0% installment plans, yet credit approvals remain a barrier for younger consumers, delaying penetration into the broader middle class of the non-invasive fat reduction market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cryolipolysis retains 42.35% of 2024 device revenues as its decade-long safety dossier and straightforward workflow appeal to both new and veteran providers. Nonetheless, HIFEM systems post an 18.25% CAGR because they tackle two biologic targets simultaneously: apoptotic adipocytes and hypertrophic muscle fibers. Post-procedure ultrasound imaging shows 16% muscle growth and 19% local fat depletion after four sessions. This holistic outcome aligns with patient expectations shaped by social media fitness influencers. The non-invasive fat reduction market size for electromagnetic platforms is projected to widen further once rehabilitative pain indications gain insurance codes. High-intensity focused ultrasound (HIFU) competes in skin tightening niches, while low-level laser light appeals to clients seeking gentler metabolic modulation with virtually no downtime. Each modality thus occupies a distinct performance-versus-comfort position, encouraging clinics to stock multiple systems for tailored plans.

Bi-modal combinations register growing traction. Providers layer radiofrequency heat to increase adipocyte susceptibility before cryolipolysis cooling or coordinate sequential HIFEM plus RF-micro-needling to tighten skin post-lipolysis. Early adopters report 30% higher average revenue per client when two devices are packaged into curated "transformation journeys." Meanwhile, injectable ice slurry, still in in-human feasibility trials, could disrupt capital-intensive platforms by lowering per-procedure consumable costs. Manufacturers therefore accelerate pipeline R&D to hedge against future commoditization. Taken together, technology diversification cements the non-invasive fat reduction market as a dynamic playground where iterative upgrades spur repeat capital expenditure cycles.

Dermatology and cosmetic clinics delivered 54.53% of 2024 revenue owing to physician trust and clinical oversight. Yet medspas outpace them with a 17.85% CAGR by integrating hospitality design, wellness retail, and membership billing. Since most devices do not legally require supervision by board-certified surgeons, entrepreneurs can scale multi-unit footprints staffed by physician assistants and nurses operating under tele-supervision agreements. Lower wage differentials in tier-2 cities combined with centralized digital marketing reduce customer acquisition cost, elevating EBITDA margins above 20%.

Hospitals tend to specialize in complex lipedema or post-bariatric contour cases requiring anesthesia and multidisciplinary aftercare. Fitness centers, in contrast, trial adjunct cryolipolysis pods near strength-training zones, capturing impulse purchasers seeking immediate visual feedback. The non-invasive fat reduction industry also witnesses hybrid "surgical spa" build-outs where plastic surgeons co-locate operating rooms and device suites, cross-pollinating patient pipelines. Capital inflows from private equity exceeded USD 3.1 billion across 400 medspa transactions between 2020-2024, underscoring institutional conviction in scalable aesthetics. This liquidity funds CRM platforms that track lifetime value, automate appointment reminders, and upsell adjunct skincare lines, cementing sticky client relationships across decades.

The Non-Invasive Fat Reduction Market Report is Segmented by Technology (High-Intensity Focused Ultrasound, Radiofrequency Lipolysis, and More), End User (Hospitals, Dermatology and Cosmetic Clinics, and More), Application Area (Abdomen, Thighs, Sub-Mental, and More), Gender (Female and Male), Age Group (18-34 Years and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 38.63% of 2024 demand thanks to established medspa density, high discretionary income, and a transparent FDA pathway that accelerates first-to-market launches. The United States makes up more than 80% of regional revenue, amplified by medical tourism from Canada and Latin America for proprietary cryolipolysis applicators unavailable elsewhere. Reimbursement pilots covering cryolipolysis in metabolic syndrome cases further legitimize procedure value and could unlock broader payer traction if outcomes demonstrate cardiovascular benefit. Digital health start-ups integrate post-procedure monitoring wearables, providing clinicians with longitudinal data that refine follow-up scheduling.

Europe accounts for the second-largest slice, characterized by highly regulated device approval under the Medical Device Regulation framework. Germany, France, and the United Kingdom are core spenders, although southern European nations show above-average growth as tourism-centric economies market "vacation plus treatment" packages. Strict advertising rules limit hyperbolic claims, compelling brands to publish peer-reviewed substantiation that inadvertently boosts consumer trust. Eco-responsibility themes resonate strongly; clinics favor energy-efficient generators and recyclable gel pads, creating a market differentiator for suppliers who verify lower life-cycle emissions.

Asia-Pacific is the fastest-growing territory at a 12.27% CAGR through 2030, driven by expanding middle-class populations and heightened appearance consciousness in urban centers. China leads volume, where 91% of surveyed aesthetic consumers plan to maintain or increase spend despite macro-economic volatility. Japan advances innovation, exemplified by robotics-assisted applicator arms that cut session set-up time by 40%. South Korea exports K-beauty protocols, popularizing combination therapy blueprints adopted across Southeast Asia. India's young demographic, coupled with rapid private-hospital build-outs, presents significant upside once device import duties ease. Australia rounds out regional uptake, leveraging tele-health consults to bridge geographic distance and optimize patient funnel management.

South America and the Middle East & Africa represent emerging hot spots, with Brazil and the United Arab Emirates championing procedure affordability relative to local cosmetic surgery alternatives. Currency fluctuations and customs tariffs pose adoption hurdles, yet medical tourism bundles that combine lodging with treatment mitigate sticker shock. Across all regions, localized regulatory clarity and clinician training remain decisive determinants of non-invasive fat reduction market expansion.