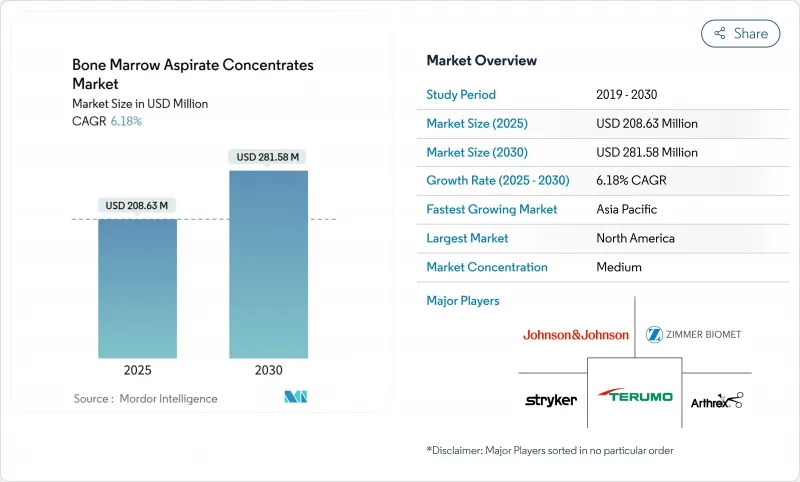

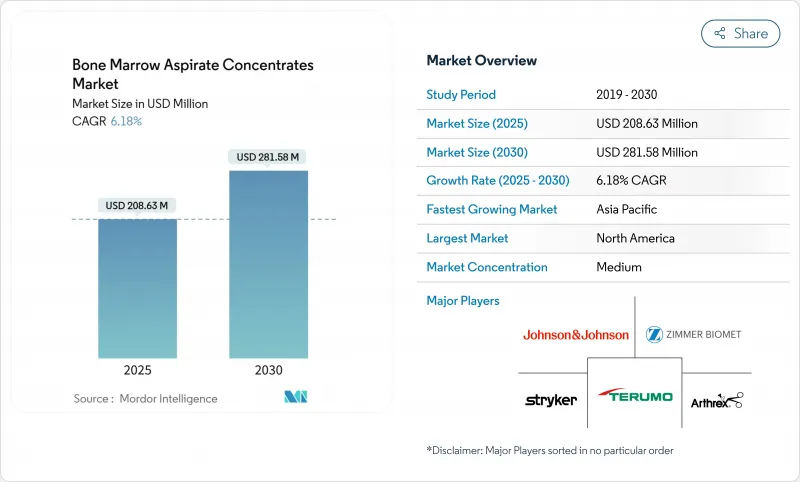

골수 흡인 농축물 시장은 2025년에 2억 863만 달러가 되고, 2030년에는 2억 8,158만 달러에 이를 것으로 예측되며, CAGR은 6.18%를 나타낼 전망입니다.

현재의 골수 흡인 농축물 시장 규모는 낮은 침습 재생 절차의 급속한 보급, 정형외과 용도의 임상 검증 확대, POC(Point-of-Care) 원심 분리의 꾸준한 기술 업그레이드를 뒷받침하고 있습니다. 스포츠 부상 증가, 소액 지급자의 유리한 보험 적용 결정, 자동화된 단일 사용 키트는 오염 위험을 줄이면서 환자 접근을 넓히고 있습니다. 주요 제조업체들은 세포 생존율을 유지하는 폐쇄 루프 시스템을 지속적으로 개선하고 있으며, 공급자는 치료 비용을 줄이고 환자 처리량을 가속화하기 위해 외래 수술 센터(ASC)를 위해 양을 이동하고 있습니다. 골수 은행과 생존 가능한 골 매트릭스를 번들링하는 전략적 파트너십은 골수 흡인 농축물 시장에서 경쟁을 더욱 강화하고 있습니다.

근골격계 장애의 유병률 증가는 개복 수술을 피하는 재생 옵션에 대한 수요를 촉진하고 있습니다. 장기 코호트에서는 BMAC 주사 후 골관절염의 지속적인 기능 개선이 기록되었으며 IKDC 점수는 4년 동안 56에서 73으로 개선되었습니다. 전문 선수와 활동적인 노인들은 현재 재활을 단축하고 관절의 완전성을 보호하는 치료를 선호합니다. 동시에 보험사는 인공관절 치환술에 비해 BMAC에 의한 비용 절감을 평가하여 조기 연골 병변에 대한 보험 적용을 촉진하고 있습니다. 정형외과 전문의는 BMAC를 힘줄, 반월판, 골절 프로토콜에 통합하는 것이 늘어나고 있으며, 골수 흡인 농축물 시장 전체에서 농축 골수 시스템에 대한 하류 수요를 강화하고 있습니다.

새로운 자동화 플랫폼은 무균성을 지키면서 재현 가능한 세포 수를 제공하여 과거의 편차 우려를 해결합니다. BioCUE를 이용한 I상골 괴사 연구에서는 외래 환자에서 안전성과 안정한 전구 세포 수율이 확인되었습니다. 폐쇄 루프 카트리지는 워크플로우를 간소화하여 지역 병원과 ASC가 완전한 클린룸 실험실 없이 BMAC 프로그램을 시작할 수 있도록 합니다. 통합된 광학 센서는 실시간으로 세포의 생존율을 검증하고 임상가가 환자 프로파일마다 농축량을 조정할 수 있게 되었습니다. 공급업체는 단일 사용 카세트를 컴팩트한 탁상형 원심분리기와 결합하여 이 모델은 시설의 자본 장벽을 크게 줄이고 골수 흡인 농축물 시장 전체에 광범위한 도입을 촉진합니다.

기증자의 나이, 흡입 기술 및 장비 선택에 따라 결과가 크게 다르기 때문에 표준화된 지침을 얻을 수 없습니다. 비교 시험에 의하면, 전구 세포의 회수율은 시판되는 플랫폼간에 최대 5배의 개방이 있습니다. 일관성이 없는 엔드포인트는 메타분석을 방해하여 가이드라인의 승인이나 지불자의 신뢰성을 저하시킵니다. 노인 기증자는 식민지 형성 단위가 낮고 정형외과의 중심층에서 치료를 복잡하게합니다. 그러므로 규제 당국의 심사관은 엄격한 출시 기준을 요구하며, 골수 흡인 농축물 시장의 혁신자에게 승인 스케줄의 연장과 비용 부담을 부과하고 있습니다.

이 시스템은 2024년 골수 흡인 농축물 시장 규모의 68.12%를 차지하며, 수술실 전체에서 BMAC 능력을 구축하는 자본적 성질을 강조했습니다. Harvest SmartPrep과 같은 주요 플랫폼은 항상 경쟁자보다 높은 결합 조직 전구 세포 수를 제공하며 골수 흡인 농축물 시장 전체의 프리미엄 가격을 지원합니다. 병원에서는 설치 시간을 단축하고 기술자 실수를 줄이는 통합 터치 스크린 인터페이스와 자동 밸런스 로터가 선호됩니다. 흡입 바늘과 일회용 카세트를 포함한 액세서리는 설치 기반의 지속적인 수요를 반영하여 CAGR 6.84%와 가장 날카로운 궤도를 기록했습니다. SurGenTec의 FDA 인증 B-MAN 키트는 안전성을 높이고 워크플로우를 간소화하는 소모품 파이프라인을 보여줍니다.

액세서리의 급증은 자본 지출을 변동하는 사례 기반 비용으로 전환하는 병원 공급망 전략에 의해 강화되었습니다. 공급업체는 다년간의 헌신과 함께 서비스 계약과 일회용 거래를 번들로 제공하여 예측 가능한 수익을 확보하는 경향이 커지고 있습니다. 북미의 성숙한 시설에서는 의사가 BMAC를 관절경, 척추 고정술, 골절 치료에 도입하기 때문에 수술실 당 소비량이 증가하고 있습니다. 아시아 신흥센터에서는 반자동 원심분리기로 전환하기 전에 수동 흡입 키트로 시작하는 경우가 많으며, 골수 흡인 농축물 시장을 확대하는 계단형 채용 경로가 형성되어 있습니다.

북미는 2024년에 41.64%의 골수 흡인 농축물 시장 점유율로 선두를 유지했고 2030년까지의 CAGR은 5.37%를 나타낼 것으로 예측됩니다. 이 지역은 세포 기반 장치의 안전성 시험에 대한 FDA의 명확한 지침, 합리화된 510(k) 패스웨이, 일부 정형외과 용도에 대한 메디케어의 적용 등의 혜택을 받고 있습니다. 미국 병원은 현재 표준을 지원하는 대량의 골수 채취 기술의 선구자이며, ASC 네트워크는 교외에서의 접근을 계속 확대하고 있습니다. 캐나다와 멕시코의 확대는 더욱 완만하지만, 미국 시설로의 국경을 넘어서는 의료 관광은 여전히 중요하며, 골수 흡인 농축물 시장 전반에 걸친 기술의 성장과 보조 액세서리 수요를 지원하고 있습니다.

유럽은 CAGR 5.89%를 나타내며 2024년 EU의 인간 유래 물질 규제에 의해 회원국간에 품질 기준이 조화되는 것이 활력이 되었습니다. 독일, 프랑스, 영국은 확립된 정형외과 프랜차이즈와 까다로운 공공 보험을 활용하여 압도적인 점유율을 차지하고 있습니다. 남부 및 동부 시장은 재생 의료를 추구하는 의료 관광객을 위한 민간 병원 체인을 통해 점차 추진하고 있습니다. 유럽 의약품청(EEA)의 선진 치료 룰북은 제조업체에게 명확한 신청 서류를 기대시켜 시장 투입까지의 시간을 단축하고 경쟁력을 높이고 있습니다.

아시아태평양은 일본, 중국, 인도, 호주가 재생 의료 인프라에 상당한 투자를 하고 있기 때문에 CAGR 6.97%를 나타내 가장 빠른 속도로 추이하고 있습니다. 일본의 의약품 의료기기 종합기구(PMDA)는 스테미락의 상업화에 의해 명시된 명확한 승인 경로를 관리하고, 지역의 규제 당국의 벤치마크가 되고 있습니다. 중국에서는 간엽계 줄기세포 치료의 시험 패스웨이가 가속되는 한편, 지방의 보험 파일럿은 체중이 걸리지 않는 연골 병변에 대해 BMAC를 상환하고 있습니다. 인도의 사립 정형외과 병원은 중동 및 아프리카의 의료 관광을 활용하여 최첨단 원심분리기를 도입하고 액세서리 수입을 촉진합니다. 그 밖에 GCC 국가, 브라질, 남아프리카는 국경을 넘는 환자를 유치하기 위해 지출을 할당하고 골수 흡인 농축물 시장의 세계 수요를 형성하고 있습니다.

The bone marrow aspirate concentrates market stood at USD 208.63 million in 2025 and is forecast to reach USD 281.58 million by 2030, registering a 6.18% CAGR.

The current bone marrow aspirate concentrates market size underscores rapid uptake of minimally invasive regenerative procedures, expanding clinical validation for orthopedic use, and steady technology upgrades in point-of-care centrifugation. Growing sports injuries, favorable micro-payer coverage decisions, and automated single-use kits are widening patient access while lowering contamination risk. Key producers continue to refine closed-loop systems that maintain cell viability, and providers are shifting volumes toward ambulatory surgical centers in pursuit of lower procedure costs and faster patient throughput. Strategic partnerships that bundle bone marrow banking with viable bone matrices further amplify competitive intensity in the bone marrow aspirate concentrates market.

Escalating musculoskeletal disorder prevalence is propelling demand for regenerative options that avert open surgery. Long-term cohorts document sustained functional improvement in knee osteoarthritis after BMAC injections, with IKDC scores improving from 56 to 73 over four years. Professional athletes and highly active seniors now prefer treatments that shorten rehabilitation and protect joint integrity. Concurrently, insurers evaluate BMAC cost savings against arthroplasty, promoting coverage for early-stage cartilage lesions. Orthopedic specialists increasingly integrate BMAC into rotator cuff, meniscal, and fracture protocols, reinforcing downstream demand for concentrated marrow systems across the bone marrow aspirate concentrates market.

Novel automated platforms deliver reproducible cell counts while guarding sterility, addressing historical variability concerns. Phase I osteonecrosis studies using BioCUE confirmed safety and consistent progenitor yields in outpatient settings. Closed-loop cartridges streamline workflow, enabling community hospitals and ASCs to launch BMAC programs without full clean-room laboratories. Integrated optical sensors now validate cell viability in real time, letting clinicians tailor concentrate volumes per patient profile. Vendors pair single-use cassettes with compact tabletop centrifuges, a model that sharply reduces facility capital barriers and drives wider installation across the bone marrow aspirate concentrates market.

Outcomes differ materially by donor age, aspiration technique, and device choice, making standardized guidance elusive. Comparative trials show progenitor recovery swings of up to fivefold between commercial platforms. Inconsistent study endpoints hamper meta-analysis, slowing guideline endorsement and payer confidence. Elderly donors exhibit lower colony-forming units, complicating treatment in the core orthopedic demographic. Regulatory reviewers therefore request stringent release criteria, extending approval timelines and imposing cost burdens on innovators within the bone marrow aspirate concentrates market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Systems generated 68.12% of the 2024 bone marrow aspirate concentrates market size, underscoring the capital nature of building BMAC capacity across surgical suites. Leading platforms such as Harvest SmartPrep consistently deliver higher connective tissue progenitor counts than rivals, supporting premium pricing across the bone marrow aspirate concentrates market. Hospitals favor integrated touch-screen interfaces and auto-balance rotors that cut set-up time and reduce technician error. Accessories, encompassing aspiration needles and disposable cassettes, recorded the sharpest trajectory at a 6.84% CAGR, reflecting recurring demand from the installed base. SurGenTec's FDA-cleared B-MAN kit illustrates the pipeline of consumables that boost safety and streamline workflow.

The accessories surge is reinforced by hospital supply chain strategies that shift capital outlays toward variable, case-based costs. Vendors increasingly bundle service contracts with discounted disposables in exchange for multi-year commitments, locking in predictable revenues. In mature North American accounts, consumption intensity per operating room is climbing as physicians integrate BMAC into arthroscopy, spine fusion, and fracture management. Emerging Asian centers often start with manual aspiration kits before migrating to semi-automated centrifuges, creating a stair-step adoption path that broadens the bone marrow aspirate concentrates market.

The Bone Marrow Aspirate Concentrates Market Report is Segmented by Product (BMAC Systems and BMAC Accessories), Application (Orthopedic Surgery, Wound Healing & Chronic Ulcers, and More), End-User (Hospitals, Ambulatory Surgical Centres, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained leadership with 41.64% bone marrow aspirate concentrates market share in 2024 and is projected to post a 5.37% CAGR through 2030. The region benefits from clear FDA guidance on safety testing for cell-based devices, streamlined 510(k) pathways, and Medicare coverage for select orthopedic uses. United States hospitals pioneered large-volume marrow harvesting techniques that underpin current standards, and ASC networks continue to broaden access in suburban locales. Canada and Mexico expand more slowly, yet cross-border medical tourism into U.S. centers remains material, sustaining procedure growth and ancillary accessory demand across the bone marrow aspirate concentrates market.

Europe follows with a 5.89% CAGR, energized by the 2024 EU regulation on substances of human origin that harmonizes quality norms across member states. Germany, France, and the United Kingdom dominate installations, leveraging established orthopedic franchises and generous public insurance. Southern and Eastern markets are gradually catching up through private hospital chains that cater to inbound medical tourists seeking regenerative options. The European Medicines Agency's advanced therapy rulebook gives manufacturers clearer dossier expectations, shortening time to market and fostering competitive parity.

Asia-Pacific delivers the fastest trajectory at 6.97% CAGR as Japan, China, India, and Australia invest heavily in regenerative infrastructure. Japan's PMDA governs a well-defined approval route illustrated by Stemirac's commercialization, setting a benchmark for regional regulators. China accelerates investigational pathways for mesenchymal stem treatments while provincial insurance pilots reimburse BMAC for non-weight-bearing cartilage lesions. India's private orthopedic hospitals capitalize on medical tourism from the Middle East and Africa, installing state-of-the-art centrifuges and driving accessory imports. Elsewhere, GCC nations, Brazil, and South Africa allocate spending to attract cross-border patients, rounding out global demand for the bone marrow aspirate concentrates market.