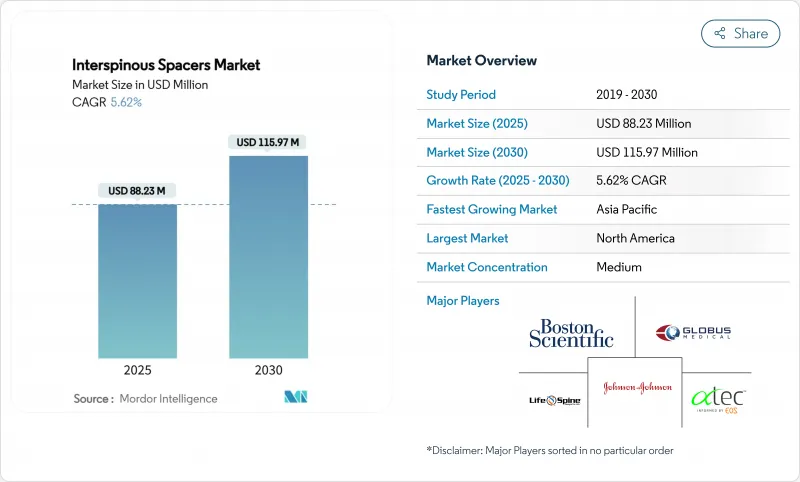

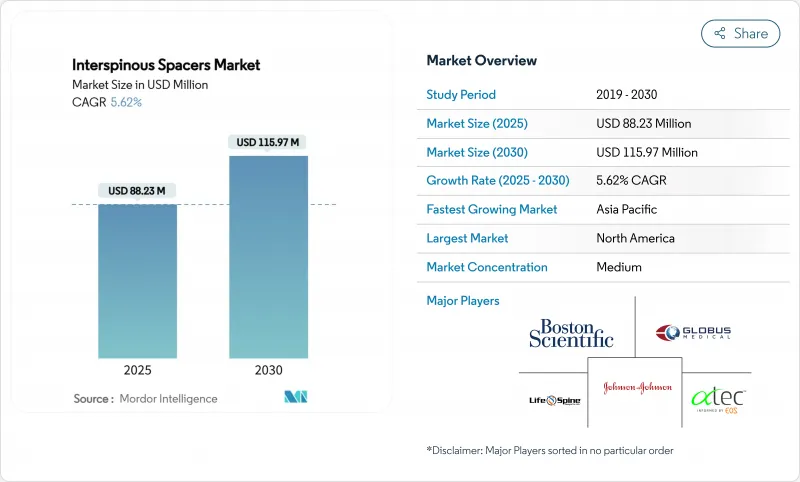

극돌기간 스페이서 시장은 2025년에 8,823만 달러에 이르고, CAGR 5.62%를 나타내 2030년에는 1억 1,597만 달러로 확대될 것으로 예측되고 있습니다.

수요가 계속 증가하고 있는 이유는 외과의사가 기존의 고정술을 대신하여 허리 협착증을 견고하게 고정하지 않고 제압하는 운동 온존 임플란트를 사용하게 되었기 때문입니다. 상업적인 견인력은 고령화, 척추 외래 환자 수 증가, 낮은 침습 치료에 보답하는 꾸준한 상환 제도 개혁에 의해 지원됩니다. 장비 제조업체는 생체 재료의 혁신, 운동과 안정성의 균형을 이루는 하이브리드 설계, 치료 결과를 기록하는 데이터 대응 후속 시스템에 의해 차별화를 도모하고 있습니다. 새로운 수술센터에 대한 아시아태평양의 투자와 같은 날 퇴원에 대한 북미 지급자의 인센티브는 극돌기간 스페이서 시장 전망을 더욱 강화합니다.

극돌기간 스페이서는 극돌기간을 흩어져 움직임을 유지함으로써 간접적인 제압을 가능하게 하여 척추절제술에 비해 수술시간과 출혈량을 줄입니다. AO Spine의 조사에 따르면 아시아태평양의 외과의사는 이러한 낮은 침습 기술을 점점 선호하고 있습니다. 이미지 지침에 대한 액세스가 넓어지면 정확도가 향상되고 학습 곡선이 단축되고 장비 수요가 자극됩니다.

65세 이상의 성인의 최대 47%가 허리 척추관협착증을 앓고 있으며, 관절 보존적 치료의 큰 후보자가 되고 있습니다. 단독 극돌기간 제압술의 5년간의 내구성 데이터는 고정술을 견딜 수 없는 노인 코호트의 적성을 뒷받침합니다. 일본과 한국에서는 급속한 고령화가 진행되고 있어, 지역 전체에서 수술 건수가 가속하고 있습니다.

추적 조사는 5년째 이후의 이동, 극돌기간 골절, 인접부 변성을 강조하여 재치환술의 비용 부담에 대해 지불측의 정사를 촉구하고 있습니다. 하이브리드 시스템은 생체 역학적 모델링에 의해 뼈와 임플란트의 계면에서 피크 응력을 줄이고 수명을 향상시킬 수 있다는 것을 보여줍니다.

정적 비압축성 임플란트는 2024년 매출의 52.35%를 차지하며, 외과의사가 익숙하다는 것을 뒷받침했습니다. 그러나 하이브리드형 임플란트는 제어된 움직임과 필요한 안정성을 양립시키기 위해 CAGR 12.25%를 나타낼 전망입니다. 유한요소법에 의한 연구에서는 하이브리드 설계가 진동시의 패싯 응력을 경감하면서 생리적 범위를 유지하는 것이 확인되었습니다. 임상적 증거가 증가함에 따라, 하이브리드는 예측 기간 동안 극돌기간 스페이서 시장을 재형성할 것으로 보입니다.

극돌기간 스페이서 시장은 확장 가능한 모델과 부문 모델이 외과 의사에게 수술 중 유연성을 가져다 다양화가 계속되고 있습니다. 하이브리드 유닛에 내장된 적응성이 높은 소재는 하중에 자동으로 반응하므로 보다 폭넓은 병태에 대응하여 수술팀 내 임플란트 선택에 관한 논의를 재구성합니다.

티타늄은 입증된 강도와 이미지의 선명도로 2024년에도 42.53%의 점유율을 유지했습니다. 외과의사는 현재 장기적인 이물질 혼입과 이미지 아티팩트를 제거하는 재흡수성 PLGA와 PLA를 추구하고 있으며, CAGR은 9.85%를 나타낼 전망입니다. 환자의 해부학적 구조에 맞춘 커스텀 메이드의 3D 프린팅 생체 흡수성 임플란트가 POC(Point-of-Care)로 출현하고 있으며, 극돌기간 스페이서 시장의 또 다른 기폭제가 되고 있습니다.

선구적인 임상시험은 흡수성 폴리유산 스페이서를 자가 이식과 결합하면 복잡한 뼈 이식의 조달을 피하여 견고한 융합을 얻을 수 있음을 보여줍니다. 개발자는 척추가 재형성된 후에만 구조적 지지가 사라지도록 분해 스케줄을 계속 개선하고 있습니다.

북미는 수술 건수가 많음, 구조화된 상환, 극돌기간 스페이서 기술에 정통한 척추외과의 설치 기반을 배경으로 2024년 41.71%의 점유율을 유지했습니다. 메디케어의 2025년 지불 조정과 번들 케어 파일럿은 외래 환자 경로에 대한 보상을 계속하기 때문에 극돌기간 스페이서 시장에 긍정적인 기세를 유지합니다.

아시아태평양은 CAGR 9.61%를 나타내 가장 빠르게 성장하는 지역입니다. 지역 후생성은 수술용 로봇, 내시경실, 외과의사 휄로우십 프로그램에 자금을 투입하고 있습니다. 일본에서는 PMDA의 패스트트랙이 신형 임플란트의 승인을 촉진하고, 중국에서는 중간 소득층의 확대에 의해 자비 진료에 의한 동작 온존 옵션의 보급이 진행되고 있습니다.

유럽은 MDR 준수의 압력에도 불구하고 안정된 수요를 유지합니다. 2028년까지의 경과조치에 의해 기존의 극돌기간 스페이서의 판매가 인정되고 있지만, 제조업체는 CE마크를 유지하기 위해 시판 후 조사를 강화해야 합니다. 독일과 프랑스에서는 고정술과 관련된 장기 재활을 완화하기 위해 낮은 침습 제압술에 공적 자금이 투입되었습니다. 중동, 아프리카, 남미의 신흥 시장은 민간 병원 네트워크가 주요 브랜드를 수입하고 제휴 훈련이 지역 외과 의사 기반을 확대하고 있기 때문에 추가 상승 요인이 되고 있습니다.

The interspinous spacers market is valued at USD 88.23 million in 2025 and is forecast to advance to USD 115.97 million by 2030, reflecting a 5.62% CAGR.

Demand continues to expand as surgeons replace traditional fusion with motion-preserving implants that decompress lumbar stenosis without rigid fixation. Commercial traction is supported by the ageing demographic, growing outpatient spine volumes and steady reimbursement reforms that reward minimally invasive care. Device makers differentiate through biomaterial innovation, hybrid designs that balance motion with stability and data-enabled follow-up systems that document outcomes. Asia-Pacific investment in new surgical centres and North American payer incentives for same-day discharge further strengthen the interspinous spacers market outlook.

Interspinous spacers enable indirect decompression by distracting spinous processes and preserving motion, which reduces operative time and blood loss compared with laminectomy. Surgeons in Asia-Pacific increasingly prefer these minimally invasive techniques, according to AO Spine surveys. Broader access to imaging guidance enhances accuracy, shrinks the learning curve and stimulates device demand.

Up to 47% of adults aged >= 65 exhibit lumbar stenosis, creating a large candidate pool for motion-preserving treatment. Five-year durability data for stand-alone interspinous decompression supports its suitability in elderly cohorts unable to tolerate fusion. Rapid ageing in Japan and South Korea accelerates procedure volumes across the region.

Follow-up studies highlight migration, spinous fractures and adjacent-segment degeneration after year 5, prompting payer scrutiny of revision cost exposure. Biomechanical modelling shows hybrid systems reduce peak stress at bone-implant interfaces, which may improve longevity.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Static non-compressible implants controlled 52.35% of 2024 revenue, underscoring surgeon familiarity. Yet the hybrid cohort is growing at a 12.25% CAGR as it blends controlled motion with required stability. Finite-element work confirms that hybrid designs maintain physiologic range while reducing facet stress during vibration. Rising clinical evidence positions hybrids to reshape the interspinous spacers market over the forecast period.

The interspinous spacers market continues to diversify as expandable and segmental models give surgeons more intra-operative flexibility. Adaptive materials embedded in hybrid units automatically respond to load, meeting a wider spectrum of pathologies and reframing implant selection discussions inside theatre teams.

Titanium maintained 42.53% share in 2024 owing to proven strength and imaging clarity. Surgeons now pursue resorbable PLGA and PLA formats that eliminate long-term foreign body and imaging artefacts and are climbing at a 9.85% CAGR. Custom 3D-printed bioresorbable implants tailored to patient anatomy are emerging at point of care, signalling another catalyst inside the interspinous spacers market.

Pioneering trials show resorbable polylactic acid spacers achieving solid fusion when combined with autograft, bypassing complex bone-graft procurement. Developers continue to refine degradation timelines so structural support disappears only after the spinal column remodels.

The Interspinous Spacers Market Report is Segmented by Product Type (Static, Expandable, and More), Biomaterial (Titanium & Titanium Alloys, and More), Minimally-Invasive Approach (Open Posterior Approach and Percutaneous), Application (Lumbar Spinal Stenosis, and More), End-User (Hospitals, Orthopedic & Spine Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America sustained 41.71% share in 2024 on the back of high procedure volumes, structured reimbursement and an installed base of spine surgeons experienced in interspinous spacer techniques. Medicare's 2025 payment adjustment and bundled care pilots continue to reward outpatient pathways, thereby preserving positive momentum for the interspinous spacers market.

Asia-Pacific is the fastest growing geography at a 9.61% CAGR. Regional health ministries pour capital into surgical robotics, endoscopic suites and surgeon fellowship programmes. Japan's PMDA fast-track nurtures novel implant approvals while China's expanding middle class drives self-pay uptake for motion preservation options.

Europe maintains steady demand despite MDR compliance pressure. Transitional allowances until 2028 permit legacy interspinous spacer sales, though manufacturers must intensify post-market studies to retain CE marks. Uptake is strongest in Germany and France where public payers fund minimally invasive decompression to reduce lengthy rehab associated with fusion. Emerging markets in the Middle East, Africa and South America contribute additional upside as private hospital networks import leading brands and partnered training expands the regional surgeon base.