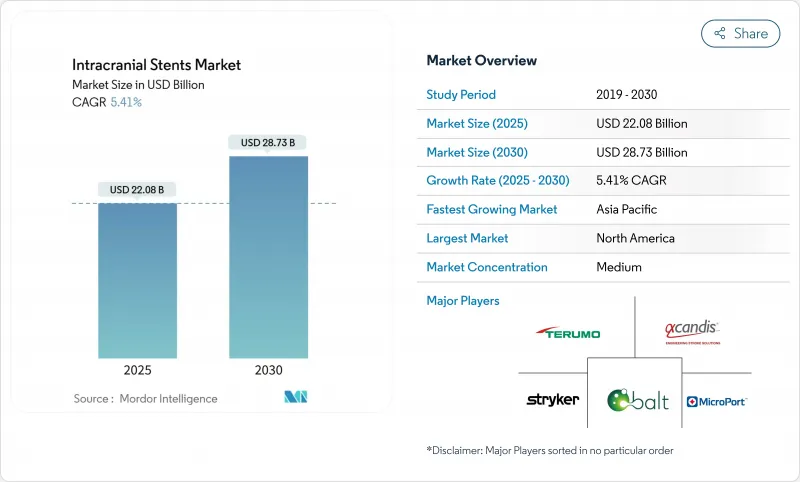

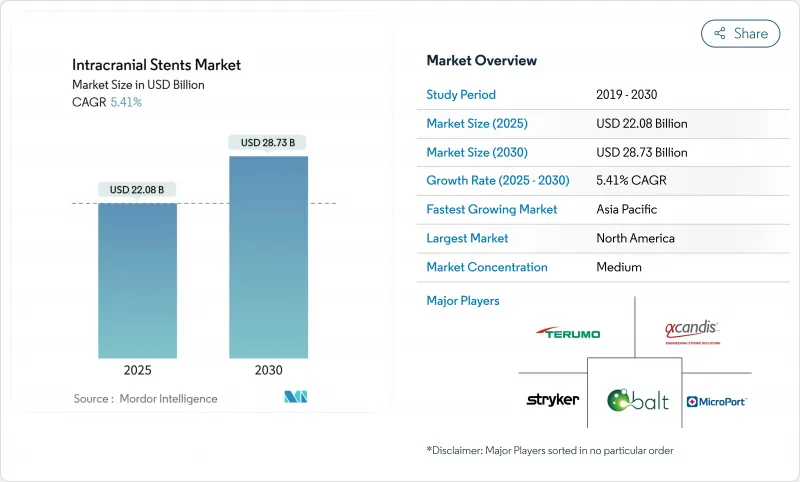

두개내 스텐트 시장은 2025년에 220억 8,000만 달러, 2030년에는 287억 3,000만 달러에 이를 전망으로, CAGR 5.41%로 성장할 것으로 예측됩니다.

보급을 뒷받침하는 것은 인구 고령화, 플로우 다이버터 기술의 꾸준한 진보, 저침습 신경혈관 치료 적응을 확대하는 환급 제도의 확대입니다. 인공지능에 의한 지침, 자가확장형 스텐트의 보급, 코팅의 기술 혁신에 의해 성공률은 더욱 높아지고, 합병증 프로파일도 저하하고 있습니다. 동시에 뇌졸중 센터 인증과 외래 환자로의 전환은 특히 인프라 프로젝트가 가속화된 아시아태평양에서 능력을 최적화하고 기술을 가능하게 하는 성장으로 시장을 전환하고 있습니다.

방사형 접근 방식은 절차의 안전성을 손상시키지 않으면서 혈관 합병증의 발생률을 낮추고 회복 시간을 단축할 수 있기 때문에 현재 교육 모듈의 주류가 되었습니다. 플로우 다이버터 스텐트는 다단 코일 색전술을 단일 장치 전개로 대체하여 카테터 시간과 방사선 노출을 줄임으로써 이러한 변화를 보여줍니다. 미국에서는 혈전제거술이 가능한 뇌졸중센터가 인정되어 표준 사용이 정착화되고 있으며, 외래수술센터의 당일 퇴원모델은 가치에 근거한 지불 이니셔티브와 완벽하게 일치하고 있습니다.

인구의 노화는 동맥류와 두개내 협착의 기준선 발생률을 증가시키고 스텐트 유치술의 세계 후보자 풀을 확대합니다. AI 이미징 툴은 조기에 침묵 동맥류를 감지하고, 플로우 다이버터의 5년 후 폐색률은 96%로 내구성 있는 성능이 확인되었고, 가이드라인이 보다 광범위하게 보강되고 있습니다. 중국에서는 2만 5,438명의 비파열 동맥류 환자가 등록되었으며 73.6%가 혈관내 치료를 받고 있습니다.

25명의 스텐트 유치를 포함한 누적 250명의 교육 수요는 노동력 확대를 늦추고 많은 2차 병원을 인력 부족에 빠뜨리고 있습니다. 펜 메디신과 같은 증례 수가 많은 거점 병원에서는 연간 2,000건 이상의 인터벤션에 성공하고 있지만, 인재는 여전히 도시에 집중되어 있어 지방이나 변두리 시장에서는 접근에 격차가 발생하고 있습니다. AI 지침은 기술 격차를 완화시킬 수 있지만, 대규모의 무작위화 시험 및 규제 검토는 아직 보류 중입니다.

플로우 다이버터의 두개내 스텐트 시장 규모는 단일 장치에 의한 동맥류 폐색 및 재치료 부담 감소에 대한 의사의 강한 선호도를 반영하여 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 9.12%로 확대될 것으로 예측됩니다. 그럼에도 불구하고 자체 확장 장치는 광범위한 적응증과 운영자의 익숙성으로 인해 2024년 판매량의 45.25%를 차지하였습니다.

Pipeline Vantage와 같은 4세대 플로우 다이버터는 현재 6개월 후의 폐색률이 81.7%에 달하고 있으며, 친수성 코팅으로 혈전색전 합병증은 4.7%로 떨어지고 코일과의 안전성 차이는 줄어들고 있습니다. 풍선 확장형은 정확한 유치가 중요한 구부러진 소아 증례에서 틈새 역할을 유지하고, 스텐트 어시스트 코일은 완전한 분류를 목표로 하는 수술자의 진료를 지원하고 있습니다.

2024년 두개내 스텐트 시장 점유율의 59.15%를 니티놀 기반 디바이스가 차지하였으며, 형상 기억의 신뢰성과 긴 임상 실적의 혜택을 받고 있습니다. 그러나 고분자 및 생체 흡수성 대안은 외과의사가 젊은 환자나 위험이 낮은 환자에게 평생 금속을 사용하지 않기 때문에 CAGR 8.56%에서 성장하고 있습니다.

철 기반 재흡수성은 부식 속도 최적화가 진행 중이지만, 심장혈관 검사에서 얻은 폴리디옥사논의 스캐폴드는 안전하게 용해되기까지 2개월간의 지지성을 입증합니다. 코발트-크롬은 복잡한 재건에서 시각화를 위해 여전히 선호되고 있습니다. 이러한 재료 이동은 의료 제공업체에게 초기 비용과 평생 위험 감소를 비교 검토하기 위해 새로운 조달 상의 의문점이 되었습니다.

2024년 두개내 스텐트 시장은 종합적인 뇌졸중 센터 네트워크, 유리한 보험 환급, 숙련된 운영자를 공급하는 견고한 펠로우십 파이프라인을 배경으로 북미가 36.34%의 매출을 이끌었습니다. 장비 제조업체는 차세대 코팅 및 AI 소프트웨어를 미국 및 캐나다 센터에서 시험적으로 적용한 후 세계 전개하는 경우가 많아 국내에서의 채용 사이클을 가속화하고 있습니다.

유럽에서는 규제의 조화와 폴리머 코팅을 한 플로우 다이버터를 여러 국가에서 평가하는 COATING 시험과 같은 국경을 넘은 임상시험에 의해 꾸준한 성장을 유지하고 있습니다. 독일, 프랑스, 북유럽의 의료제도도 복잡동맥류에 대한 유로 전환술을 포함하도록 뇌졸중 가이드라인을 업그레이드하고 있으며, 과거의 기기 클래스보다 빨리 보험 환급이 확보되고 있습니다.

아시아태평양은 뇌졸중 센터에 대한 공공 투자와 치료되지 않은 다수의 동맥류 인구에 힘입어 CAGR 8.01%로 가장 빠르게 성장하는 지역입니다. 중국의 비파열 두개내 동맥류 치료 시험은 2만 5,000명 이상의 환자 등록과 혈관내 치료율이 70% 이상인 점 등 수요 규모의 크기를 나타냅니다. 인도와 인도네시아는 새로운 신경 카테터 실험실의 증설을 보장하고 일본과 한국은 각국의 환급이 명확하기 때문에 폴리머 코트 스텐트의 조기 도입국이 되고 있습니다.

중동 및 아프리카는 도입 곡선이 가파르며 사우디아라비아와 아랍에미리트(UAE)의 의료 도시 개념의 혜택을 누리고 있습니다. 남미는 두 가지 속도로 움직이고 있습니다. 브라질과 콜롬비아는 민간 부담 하에서 급성장하고 있지만, 경제 규모가 작은 국가는 예산 제약에 뒤처져 있습니다.

The intracranial stents market stands at USD 22.08 billion in 2025 and is forecast to reach USD 28.73 billion by 2030, advancing at a 5.41% CAGR.

Uptake is propelled by an aging population, steady gains in flow-diversion technology, and wider reimbursement that collectively expand candidacy for minimally invasive neurovascular care.Flow-diverter breakthroughs now let physicians treat aneurysms once deemed inoperable while shortening procedural steps, a change that is reshaping everyday practice. Artificial-intelligence guidance, growing self-expanding stent familiarity, and coating innovations further raise success rates and lower complication profiles. At the same time, stroke-center accreditations and outpatient migration are leaning the market toward capacity-optimized, technology-enabled growth, especially in Asia-Pacific where infrastructure projects are accelerating.

Radial-access approaches now dominate current training modules because they lower vascular complication rates and trim recovery times without undermining procedural safety. Flow-diverting stents exemplify this change by replacing multi-stage coil embolization with single-device deployment, reducing catheter time and radiation exposure. Certification of thrombectomy-capable stroke centers in the United States is cementing standardized use, and the same-day-discharge model inside ambulatory surgery centers aligns perfectly with value-based payment initiatives.

Population aging raises the baseline incidence of aneurysms and intracranial stenosis, expanding the global candidate pool for stenting frontiersin.org. AI-imaging tools now detect silent aneurysms earlier, while five-year occlusion rates of 96% for flow-diverters confirm durable performance and reinforce broader guidelines jnis.bmj.com. In China, 25,438 patients were enrolled for unruptured aneurysm care, with 73.6% managed endovascularly, illustrating huge latent demand.

Training demands of 250 cumulative cases, including 25 stent placements, slow workforce expansion and leave many secondary hospitals understaffed. High-volume hubs such as Penn Medicine handle over 2,000 interventions annually, but talent remains clustered in urban centers, leading to access disparities for rural or frontier markets. AI guidance may ease skill gaps, yet large randomized trials and regulatory review are still pending.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The intracranial stents market size for flow-diverters is projected to expand at 9.12% CAGR between 2025-2030, reflecting strong physician preference for single-device aneurysm occlusion and reduced retreatment burden. Self-expanding devices nevertheless control 45.25% 2024 volume thanks to their broad indication list and operator familiarity.

Fourth-generation flow-diverters such as Pipeline Vantage now achieve 81.7% six-month occlusion, while hydrophilic coatings have lowered thromboembolic complications to 4.7%, narrowing the safety gap with coils. Balloon-expandable models retain niche roles in tortuous pediatric cases where exact placement is critical, and stent-assisted coils continue to bridge practice for operators transitioning toward full flow diversion.

Nitinol-based devices accounted for 59.15% of the intracranial stents market share in 2024, benefiting from shape-memory reliability and long clinical track records. Yet polymer and bioresorbable alternatives are growing at 8.56% CAGR as surgeons aim to avoid lifelong metal in young or low-risk patients.

Iron-based resorbables are undergoing corrosion-rate optimization, while polydioxanone scaffolds from cardiovascular trials provide proof of two-month support before safe dissolution. Cobalt-chromium remains favored for visualization in complex reconstructions. This material shift adds new procurement questions for providers weighing up-front cost versus lifetime risk mitigation.

The Intracranial Stents Market Report is Segmented by Type (Self-Expanding Stents, Balloon Expanding Stents, and More), Material (Nitinol, Cobalt-Chromium and More), Application (Intracranial Stenosis, Brain Aneurysm and More), End-User (Hospitals, Ambulatory Surgery Centers and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led the intracranial stents market in 2024 with 36.34% revenue, anchored by comprehensive stroke-center networks, favorable reimbursement, and a robust fellowship pipeline that supplies skilled operators. Device manufacturers often pilot next-generation coatings and AI software in United States or Canadian centers before global roll-out, accelerating domestic adoption cycles.

Europe maintains steady growth through regulatory harmonization and cross-border clinical trials such as the COATING study, which evaluates polymer-coated flow-diverters across multiple countries. National health systems in Germany, France, and the Nordic region have also upgraded stroke guidelines to include flow-diversion for complex aneurysms, securing reimbursement faster than past device classes.

Asia-Pacific is the fastest-growing region at 8.01% CAGR, propelled by public investment in stroke centers and a large untreated aneurysm population. The China Treatment Trial for Unruptured Intracranial Aneurysm highlights demand scale, enrolling over 25,000 patients with an endovascular treatment rate above 70%. India and Indonesia follow with capacity pledges for new neuro-cath labs, while Japan and South Korea serve as early adopters of polymer-coated stents due to national reimbursement clarity.

The Middle East and Africa are at an earlier adoption curve but benefit from medical-city initiatives in Saudi Arabia and United Arab Emirates that import high-end imaging suites and training partnerships. South America shows dual-speed dynamics: Brazil and Colombia grow quickly under private-payer segments, while smaller economies lag amid budget constraints.