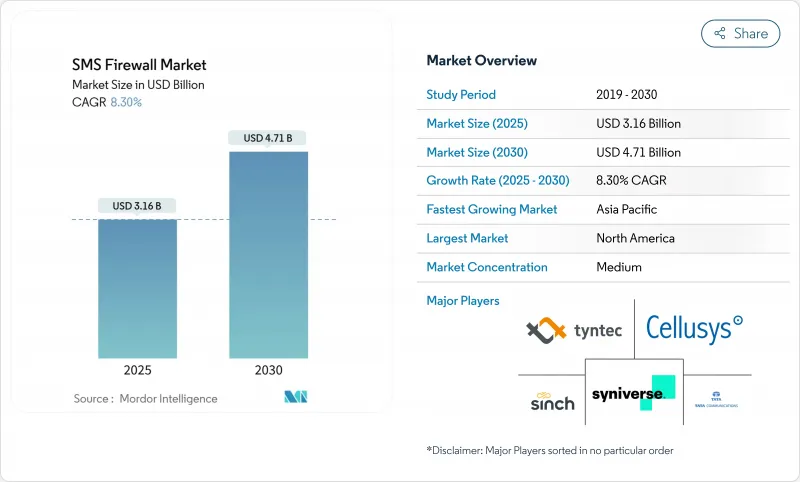

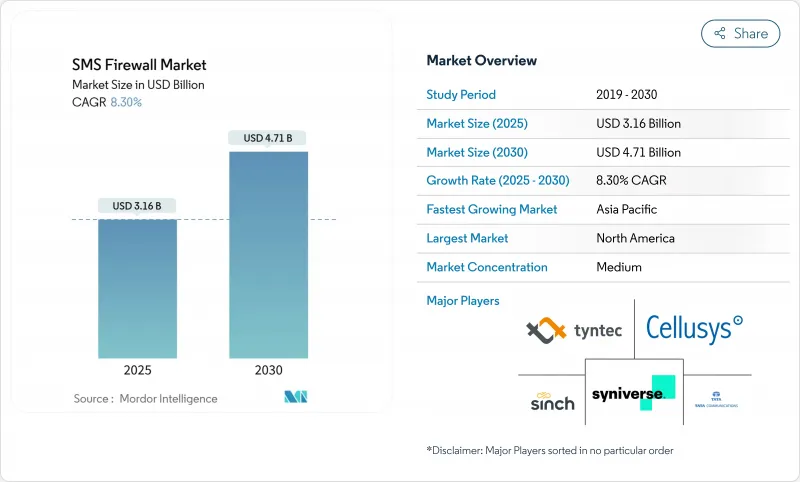

SMS 방화벽 시장 규모는 2025년에 31억 6,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 8.30%로 성장할 전망이며, 2030년에는 47억 1,000만 달러에 달할 것으로 예측됩니다.

통신 사업자는 A2P 수익 확보, 새로운 추적성 의무 대응, 5G 네트워크 슬라이스를 시그널링 위협으로부터 보호하기 위해 차세대 방화벽에 투자하고 있습니다. SS7에서 Diameter 방화벽으로의 전환, 얼리어댑터 국가에서의 5G 전개 가속, 온쇼어 필터링을 강제하는 각국의 데이터 주권 규칙 등에 의해 설비투자는 증가의 길을 따라가고 있습니다. 동시에 CPaaS의 통합은 공급업체의 마진을 압박하고 있으며 공급업체는 AI를 활용한 애널리틱스 및 관리 서비스를 제공함으로써 차별화를 도모하고 있습니다. 공급업체 간의 적당한 단편화는 클라우드 네이티브 구독 도구로 Tier-3 및 Tier-4 모바일 네트워크 사업자를 대상으로 하는 틈새 전문가를 위한 공간을 남깁니다.

사업자는 음성 소득 감소에 직면하고 있기 때문에 인증된 A2P 메시징이 수익 회복을 위해 매우 중요합니다. 인도의 분산형 대장 프레임워크는 Airtel 고객에게 누출을 40% 줄이고 스팸을 98% 줄였습니다. 브라질과 나이지리아의 유사한 수익 창출 프로그램은 합법적인 기업 메시지와 회색 경로를 분리하는 고급 트래픽 분석에 의존합니다. 이 모델에서 통신 사업자는 보안을 통합한 프리미엄 딜리버리 서비스를 재판매할 수도 있습니다. 채산은 취할 수 있는 것, 전개에는 머신러닝에 의한 검사 툴이 필요하고, 소규모 통신 사업자에서는 레거시 인프라스트럭처에서 호스팅할 수 없습니다.

SIM 박스 사기는 연간 31억 1,000만 달러의 손실을 초래하여 통신 사기 전체의 7.8%를 차지하고 있습니다. 인위적으로 트래픽을 늘리고 피싱 캠페인을 음성, SMS, 소셜 앱을 결합하여 규제 당국의 대응이 강요되고 있습니다. 인도의 AI 기반 스푸핑 방지 플랫폼은 3개월 만에 사기 전화를 90% 줄였습니다. 이러한 성공으로 인해 다른 규제 당국은 더 광범위한 사기 방지 스택에 통합된 SMS 방화벽 기능을 요구하게 되고 SMS 방화벽 시장은 확대되고 있습니다.

인도에서 27,000명의 사업자가 컴플라이언스 지원을 요청했듯이 수천 명의 소규모 사업자들이 DLT 등록 및 규칙 최적화를 위해 노력하고 있습니다. 머신러닝 규칙의 지속적인 튜닝과 위협 라이브 피드의 통합은 이러한 사업자를 관리형 서비스로 향하게 하지만, 예산 제한으로 인해 도입이 늦어지고 있습니다.

2024년 SMS 방화벽 시장 점유율의 65.3%는 A2P 메시징이 차지하며 금융, 헬스케어, 공공 서비스에 있어서 인증 규칙의 의무화에 지지되고 있습니다. A2P 부문의 SMS 방화벽 시장 규모는 기업이 배달 보증 및 스팸 방지에 대가를 지불하고 있기 때문에 CAGR 8.3%로 확대될 것으로 예측됩니다. 기업은 안전한 P2P 경보에도 투자하고 있으며 P2P 기업용 카테고리의 CAGR을 10.2%로 밀어 올립니다. Jack Henry는 이미 매월 1,200만에서 1,500만 건의 보안 경보를 Twilio를 통해 전달하고 있으며, 전달량은 50배로 증가할 예정입니다.

A2P의 성장은 회색 경로를 필터링하는 방화벽 업그레이드를 가속화하고 인바운드 고객의 문의와 같은 P2A 이용 사례는 스푸핑 공격으로부터 기업을 보호하는 인증에 달려 있습니다. RCS와 같은 경쟁 채널은 P2A의 기세를 약화하지만 규제 부문은 여전히 SMS에 의존하고 있습니다. 일회용 비밀번호와 서비스 알림이 증가함에 따라 보안이 높은 A2P 트래픽은 운영자의 수익 전략의 중심이 되고 있으며 SMS 방화벽 시장을 강화하고 있습니다.

온프레미스 유형이 2024년에 53.22%의 판매 점유율을 유지하는 이유는 Tier 1 캐리어가 로컬 데이터 제어를 선호하기 때문입니다. 그럼에도 불구하고 클라우드 옵션은 소규모 사업자의 강한 수요를 반영하여 CAGR 13.1%를 보일 것으로 예측됩니다. 클라우드 전개의 SMS 방화벽 시장 규모는 크로스보더 처리를 인정하는 지역의 규제 당국이 위협의 공유 피드를 지지하기 때문에 급증할 것으로 예측됩니다.

하이브리드 아키텍처는 데이터 현지화에 관한 법률이 존재하는 지역에서 지지를 모으고 운영자는 클라우드에서 메타데이터를 분석하면서 메시지 컨텐츠를 육상에서 저장할 수 있습니다. 통신 사업자의 시설 내에 배치된 엣지 노드는 기밀 데이터를 오프사이트로 이동시키지 않고 거의 실시간 분석을 제공합니다. 이러한 유연성이 추가 투자에 박차를 가하고 SMS 방화벽 시장은 기존과 신흥 도입 모델 모두에서 계속 성장하고 있습니다.

북미가 2024년 매출 점유율 37.8%로 선두를 차지했습니다. 이는 엄격한 프라이버시 규칙, 5G 조기 도입, 기업의 통신 스택에 방화벽을 통합하는 대규모 CPaaS 생태계 덕분입니다. 2025년에는 캐나다와 멕시코와의 국경을 넘어서는 메시징이 새로운 감사 추적의 의무화를 유발하기 때문에 통신 사업자의 지출은 계속 견조하게 추진하고 있습니다. 로보콜과 스미싱 사기에 대한 연방 정부의 주목이 수요를 더욱 끌어올려 SMS 방화벽 시장에서 북미의 리더십은 흔들리지 않습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 12.5%로 가장 급성장하고 있는 지역입니다. 인도의 DLT 프레임워크는 엔드 투 엔드 메시지 추적성을 강화하고 지역 청사진 역할을 하는 반면, 중국의 적극적인 5G 슬라이싱 배포가 차세대 방화벽 도입을 가속화하고 있습니다. 동남아시아 사업자들은 인도의 성과 향상을 반영한 스팸 삭감책으로 추종하여 SMS 방화벽 시장을 총체적으로 확대하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정) 준수와 세밀한 동의 로그가 필요한 범 EU 월경 트래픽 규칙 간의 균형을 맞추고 있습니다. 데이터 주권 조항이 운영자를 온쇼어 필터링으로 향하게 하는 반면, 공유 위협 피드는 저위험 범주에서 클라우드 채택을 지원하고 있습니다. 중동 및 아프리카에서는 모바일 퍼스트의 경제권이 자본 비용을 줄이기 위해 클라우드 네이티브 방화벽을 채택하고 있지만, 소규모 이동통신사에서는 의식의 갭이 침투를 늦추고 있습니다. 남미에서는 인도와 마찬가지로 메시지의 KYC 인증이 의무화되어 저비용 규제 대응 솔루션에 대한 수요가 높아지고 있습니다.

The SMS Firewall Market size is estimated at USD 3.16 billion in 2025, and is expected to reach USD 4.71 billion by 2030, at a CAGR of 8.30% during the forecast period (2025-2030).

Operators are investing in next-generation firewalls to secure A2P revenues, comply with new traceability mandates, and guard 5G network slices from signaling threats. Migration from SS7 to Diameter firewalls, accelerated 5G rollouts in early-adopter countries, and national data-sovereignty rules that force on-shore filtering keep capital spending elevated. At the same time, CPaaS consolidation is compressing vendor margins, prompting suppliers to differentiate with AI-driven analytics and managed services offers. Moderate fragmentation among suppliers leaves space for niche specialists that target tier-3 and tier-4 mobile network operators with cloud-native, subscription-based tools.

Operators face declining voice income, so authenticated A2P messaging has become pivotal for revenue recovery. India's distributed ledger framework showed a 40% cut in leakage and a 98% spam drop for Airtel customers. Similar monetisation programs in Brazil and Nigeria rely on advanced traffic analytics that separate legitimate enterprise messages from grey routes. The model also lets carriers resell premium delivery services with embedded security. Although profitable, rollout demands machine-learning inspection tools that smaller carriers cannot host on legacy infrastructure.

SIM-box fraud causes USD 3.11 billion in yearly losses and represents 7.8% of total telecom fraud. Artificially inflated traffic and phishing campaigns now combine voice, SMS, and social apps, pressuring regulators to act. India's AI-based anti-spoofing platform cut fraudulent calls by 90% in three months. Such successes push other regulators to demand integrated SMS firewall capability within wider fraud-prevention stacks, expanding the SMS firewall market.

Thousands of smaller operators grapple with DLT registration and rule optimization, as seen when 27,000 entities in India sought compliance assistance. Continuous tuning of machine-learning rules and integration of live threat feeds push these operators toward managed services, yet budget limits slow adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

A2P messaging held 65.3% of the SMS firewall market share in 2024, underpinned by mandatory authentication rules across finance, healthcare, and public services. The SMS firewall market size for A2P segments is set to expand at an 8.3% CAGR as enterprises pay for guaranteed delivery and spam control. Enterprises also invest in secure P2P alerts, pushing the P2P enterprise category to a 10.2% CAGR. Jack Henry already moves 12-15 million secured alerts each month through Twilio and plans a fifty-fold volume growth.

A2P growth accelerates firewall upgrades that filter grey routes, while P2A use cases such as inbound customer queries hinge on authentication that shields enterprises from impersonation attacks. Competing channels like RCS slow P2A momentum, yet regulated sectors still rely on SMS for universal reach. The rising volume of one-time passwords and service notifications keeps security-rich A2P traffic central to operator revenue strategies, fortifying the SMS firewall market.

On-premise deployments retained 53.22% revenue share in 2024 because tier-1 carriers favor local data control. Even so, cloud options are projected to record a 13.1% CAGR, reflecting strong demand from smaller operators. The SMS firewall market size for cloud deployments is forecast to rise sharply as regulators in regions that allow cross-border processing endorse shared-threat feeds.

Hybrid architectures gain traction where data localization laws exist, letting operators analyze metadata in the cloud while storing message content on shore. Edge nodes positioned inside carrier facilities provide near-real-time analytics without moving sensitive data off-site. This flexibility spurs additional investment, ensuring that the SMS firewall market continues to grow in both traditional and emerging deployment models.

The SMS Firewall Market is Segmented by SMS Type (A2P, P2A, and P2P), Deployment Mode (On-Premise and Cloud), Service Type (Professional Services and Managed Services), End-User Industry (BFSI, Government and Public Safety, and More), Network Generation (2G/3G, 4G/LTE, and 5G), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led with a 37.8% revenue share in 2024, thanks to stringent privacy rules, early 5G adoption, and large CPaaS ecosystems that embed firewalls into enterprise communication stacks. Carrier spending stays strong in 2025 as cross-border messaging with Canada and Mexico triggers new audit trail mandates. Federal attention on robocalls and smishing scams further boosts demand, anchoring North American leadership within the SMS firewall market.

Asia-Pacific is the fastest-growing region at a 12.5% CAGR to 2030. India's DLT framework enforces end-to-end message traceability and functions as a regional blueprint, while China's aggressive 5G slicing deployment accelerates next-generation firewall uptake. Southeast Asian operators follow with spam-reduction drives that mirror India's performance gains, collectively enlarging the SMS firewall market.

Europe balances GDPR compliance with pan-EU cross-border traffic rules that require granular consent logs. Data-sovereignty clauses push operators toward on-shore filtering, yet shared threat feeds encourage cloud adoption in low-risk categories. In the Middle East and Africa, mobile-first economies adopt cloud-native firewalls to reduce capital expenses, though awareness gaps among smaller MNOs slow penetration. South America mirrors India by mandating KYC verification on messages, fueling demand for low-cost, regulation-ready solutions.