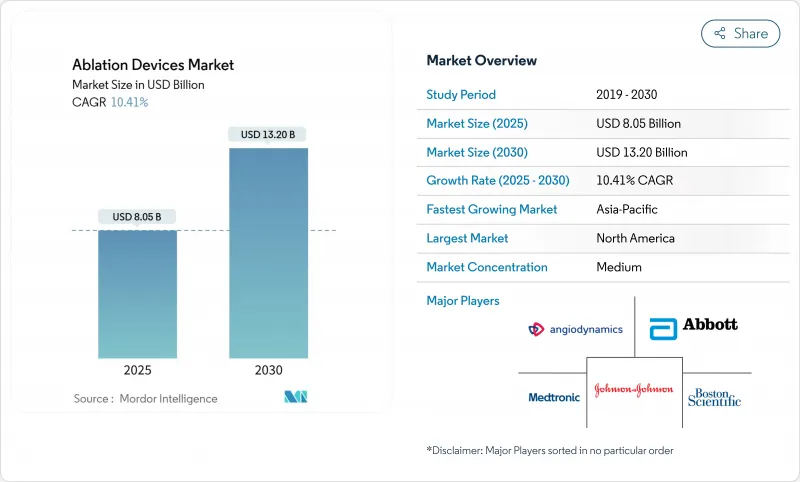

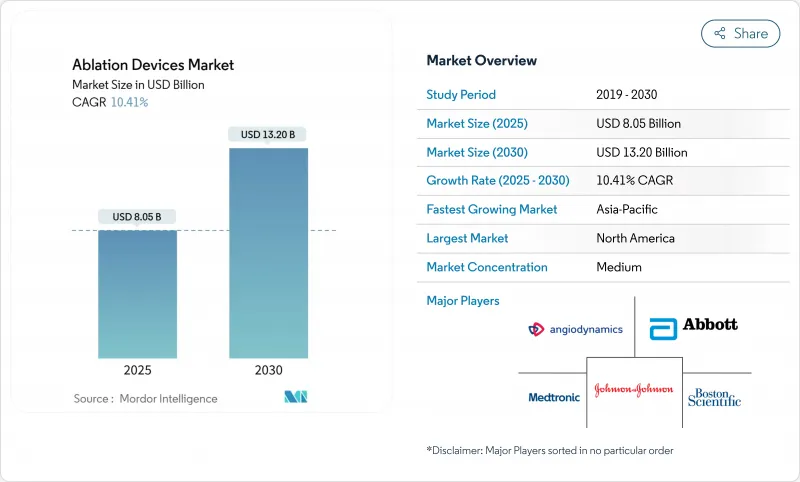

절제 기기 시장은 2025년에 80억 5,000만 달러로 추정되고, 2030년에는 CAGR 10.41%로 성장할 전망이며, 132억 달러로 상승할 것으로 예측됩니다.

저침습 치료에 대한 왕성한 수요, 펄스 필드 절제에 대한 급속한 규제 클리어런스, 만성 질환의 부담 증가가 이 상승 곡선을 지원합니다. 라디오 파 플랫폼은 여전히 수익의 중심이지만 초기 데이터에서 절차의 단축과 합병증 위험의 감소가 확인되었기 때문에 비열식 시스템이 견인 역할을 하고 있습니다. 지역별로는 헬스케어의 근대화에 의해 선진 치료에 대한 접근이 확대되고 있는 아시아태평양이 성장하고 있으며, 북미는 프리미엄 가격과 꾸준한 임베디드 사이클에 의해 수익의 주도권을 유지하고 있습니다. 통합과 적극적인 연구개발 비용으로 경쟁업체 간의 적대관계는 첨예화되고 있지만, 에너지 전달의 혁신과 정밀한 이미징과 매핑 솔루션을 결합할 수 있는 기업에게는 시장이 계속 보상되고 있습니다.

펄스 필드 절제(PFA)는 인접 기관에 열 손상을 피하는 조직 선택 에너지를 제공하여 치료 시간을 거의 절반으로 줄입니다. ADVENT 시험에서 보스턴 과학의 FARAPULSE는 대부분의 사례를 60분 이내에 완료하면서 12개월 후 무부정맥 생존율 81.6%를 달성했습니다. Medtronic의 PulseSelect는 88%의 무재발생률과 비슷한 시간 단축을 보였으며, Abbott의 Volt 플랫폼은 94.5%의 재절연으로부터의 방출을 보고했습니다. 2024-2025년 여러 PFA 시스템이 FDA에 승인되는 것은 규제 당국의 신뢰를 보여주며 전 세계적인 전개를 뒷받침합니다. 고급 매핑과 폐쇄 루프 제어를 통합한 보다 광범위한 포트폴리오는 절제 기기 시장을 더욱 확대할 것으로 예측됩니다.

병원은 측정 가능한 영업 이익을 통해 PFA에 대한 투자를 정당화하고 있습니다. 유럽 센터에서는 합병증 감소 및 치료실 체류 시간 단축으로 자원 사용이 줄어들었기 때문에 클라이오 절제에 비해 환자 1인당 850달러, 라디오파에 비해 1,301달러 비용 절감이 보고되었습니다. 이미 세계 20만 명 이상의 환자가 FARAPULSE로 치료를 받고 있으며, 조기 도입자의 피드백에 따르면 평균 치료 시간은 30분 가까이 있으며, 신규 사용자의 학습 곡선을 가속시키는 효율성을 나타냅니다. 의사가 발작성 심방세동 및 지속성 심방세동에 대한 자신감을 높일수록 PFA는 틈새 기술에서 플랫폼 기술로 전환하여 절제 기기 시장 전체의 성장을 강화하고 있습니다.

500,000달러 이상의 설비 투자와 3,000달러에서 8,000달러 사이의 일회용 카테터 가격은 소규모 시설이 차세대 시스템을 채택할 것을 망설였습니다. 연간 서비스 계약은 소유 비용에 15-20%를 곱합니다. 의료 제공업체는 현재 지불을 임상 성과에 연결하는 가치 기반 가격 설정을 요구하고 있으며 제조업체는 선행 지출을 억제하는 공유 세이빙 및 페이퍼 사용 모델을 만들도록 강요되고 있습니다.

라디오파 소작 요법은 수십년에 걸친 임상적인 익숙함과 효율적인 상환 경로를 통해 2024년 소작 장치 시장 점유율의 43.55%를 유지했습니다. 그러나 펄스 필드 시스템은 의사의 증례 단축과 안전성 향상으로 절제 기기 시장에서 가장 빠른 CAGR 23.25%로 성장할 것으로 예측됩니다. 크라이오 절제는 폐 정맥 격리를 위해 여전히 중요하지만, 마이크로파 시스템은 종양학에서 보다 크고 균일한 절제 구역이 특이한 지보를 확고히 하고 있습니다. 히스토트립시는 최근 간종양에 대해 85-95%의 성공률로 FDA의 인가를 얻었는데, 이는 기계적 에너지 요법이 보다 널리 받아들여지고 있음을 보여주고 있습니다.

기술 구성은 또한 환자의 해부학적 구조에 맞게 출력을 조정하고, 일관된 병변 세트를 만들며, 운영자의 변동을 줄이는 인공지능(AI)의 영향을 받습니다. 레이저와 고밀도 초점 초음파는 피부과뿐만 아니라 페인 클리닉과 부인과에도 퍼지고 있습니다. 자본 예산이 멀티 에너지 콘솔로 전환하는 동안, 모달리티를 하나의 플랫폼으로 통합할 수 있는 공급업체는 절제 기기 시장에서 더 큰 시장 기회를 얻을 수 있는 입장에 있습니다.

간종양, 폐종양, 신종양의 프로토콜이 확립되어 있기 때문에 2024년의 절제 기기 시장의 39.53%는 종양학이 차지했습니다. 심혈관 절제는 CAGR 12.35%로 성장할 것으로 예측되며 심방세동의 조기 절제를 실시하는 EP 실험실 간 절제 기기 시장 규모 점유율 싸움이 격화될 전망입니다. 안과 및 통증 관리의 틈새 용도는 개복 수술없이 섬세한 조직을 대상으로 마이크로카테터에 의해 꾸준히 확장됩니다. 부인과에서는 임신성을 온존하는 선택 수요가 높아짐에 따라 저침습의 자궁근종 치료가 견인력을 증가하고 있습니다.

임상 데이터는 심장 성장을 계속 검증합니다. 고급 3D 매핑이 병변 배치를 안내하는 경우 12개월 후 내구율이 90%를 초과하는 것으로 보고되었습니다. AI 주도 알고리즘은 절제 라인을 더욱 개인화하고 웨어러블 모니터는 치료 후 리듬 메트릭을 획득하여 의사의 신뢰성을 강화하고 절제 기기 시장의 볼륨을 밀어 올리고 있습니다.

북미는 2024년 세계 매출의 38.82%를 차지했습니다. 성숙한 상환 제도, FDA 승인 가속화, 강력한 교체 사이클이 리더십을 유지하고 있습니다. 보스턴 사이언티픽은 출시 첫 해에 40,000명 이상의 환자를 팔라펄스로 치료하고 급속한 보급을 뒷받침하고 있습니다. 또한 이 지역에는 새로운 적응증을 뒷받침하는 중요한 데이터를 낳는 주요 연구센터가 있어 병원과 외래센터에서의 신뢰성을 높이고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 12.52%로 예측되는 가장 빠르게 성장하는 지역입니다. 중국과 인도에서는 국가의 의료 개혁 및 의료기기 제조의 확대로 조달 비용이 낮아 입수성이 향상되고 있습니다. 일본의 규제 당국은 2024년 9월에 FARAPULSE를 인가했으며, 병원의 조기 수요는 비가열 기술에 대한 강한 의욕을 보여줍니다. 고령화 사회로의 인구 역학 변화와 만성 질환 증가는 지역에서 절제 기기 시장의 지속적인 성장을 보장합니다.

유럽에서는 의료기기 규제 프레임워크이 정합화되어 환자를 보호하면서 기술 혁신을 촉진함으로써 꾸준히 시장이 확대되고 있습니다. Abbot의 Volt PFA 시스템이 2025년 3월에 CE 마크를 조기에 승인한 것은 이 지역이 첨단 플랫폼의 런치패드 역할을 하고 있음을 보여줍니다. 학술 병원은 특히 종양학 및 신경학 용도 분야에서 연구자 중심의 연구를 주도하고 있으며, 유럽의 임상의가 세계에 퍼져있는 프로토콜을 개선하는 데 도움이 됩니다.

The ablation device market reached USD 8.05 billion in 2025 and is forecast to rise to USD 13.20 billion by 2030, registering a 10.41% CAGR.

Strong demand for minimally invasive care, rapid regulatory clearances for pulsed-field ablation, and the growing burden of chronic diseases sustain this upward curve. Radiofrequency platforms still anchor revenues, yet non-thermal systems gain traction as early data confirm shorter procedures and lower complication risks. Regional growth tilts toward Asia-Pacific, where healthcare modernization widens access to advanced therapies, while North America maintains revenue leadership through premium pricing and steady replacement cycles. Consolidation and aggressive R&D spending sharpen competitive rivalry, but the market continues to reward firms that can pair energy delivery innovations with precise imaging and mapping solutions.

Pulsed-field ablation (PFA) delivers tissue-selective energy that avoids thermal injury to adjacent organs and cuts procedure times nearly in half. In the ADVENT trial, Boston Scientific's FARAPULSE achieved 81.6% arrhythmia-free survival at 12 months while completing most cases under 60 minutes. Medtronic's PulseSelect posted 88% freedom from recurrence and similar time savings, and Abbott's Volt platform reported 94.5% freedom from repeat ablation. FDA approvals for multiple PFA systems in 2024-2025 signal regulatory confidence and encourage global roll-outs. Broader portfolios that integrate advanced mapping and closed-loop control are expected to further expand the ablation device market.

Hospitals justify PFA investment through measurable operating gains. European centers reported per-patient savings of USD 850 versus cryoablation and USD 1,301 against radiofrequency as fewer complications and shorter room times trimmed resource use. More than 200,000 patients have already been treated worldwide with FARAPULSE, and early adopter feedback notes average procedure times near 30 minutes, an efficiency that accelerates learning curves for new users. As physicians gain confidence across paroxysmal and persistent atrial fibrillation, PFA transitions from niche to platform technology, reinforcing growth across the ablation device market.

Capital investments above USD 500,000 and single-use catheter prices ranging from USD 3,000 to USD 8,000 deter small facilities from adopting next-generation systems. Annual service contracts add 15-20% to ownership costs. Providers now request value-based pricing that links payments to clinical outcomes, compelling manufacturers to craft shared-savings or pay-per-use models that temper upfront spending.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Radiofrequency ablation retained 43.55% ablation device market share in 2024 through decades of clinical familiarity and efficient reimbursement pathways. However, pulsed-field systems are forecast to post a 23.25% CAGR, the fastest within the ablation device market, as physicians embrace shorter cases and improved safety. Cryoablation remains important for pulmonary vein isolation, while microwave systems gain ground in oncology where larger, uniform ablation zones are prized. Histotripsy recently secured FDA clearance for liver tumors with 85-95% success, signaling broader acceptance of mechanical energy therapies.

The technology mix is also influenced by artificial intelligence that tailors power delivery to patient anatomy, producing consistent lesion sets and reducing operator variability. Laser and high-intensity focused ultrasound are expanding beyond dermatology into pain and gynecology, while integrated mapping plus therapy catheters shorten lab time. As capital budgets migrate toward multi-energy consoles, suppliers able to consolidate modalities on one platform are positioned to capture greater ablation device market opportunity.

Oncology commanded 39.53% of the ablation device market in 2024 thanks to established protocols for liver, lung, and renal tumors. Cardiovascular ablation is projected to grow at 12.35% CAGR, sharpening competition for share of the ablation device market size among EP labs that increasingly ablate early in atrial fibrillation. Ophthalmology and pain management niche uses expand steadily due to micro-catheters that target delicate tissues without open surgery. In gynecology, minimally invasive fibroid treatment gains traction as fertility-preserving options rise in demand.

Clinical data continue to validate cardiac growth. Durability rates above 90% at 12 months have been reported when advanced 3-D mapping guides lesion placement. AI-driven algorithms further personalize ablation lines, while wearable monitors capture post-procedure rhythm metrics, reinforcing physician confidence and boosting volumes within the ablation device market.

The Ablation Devices Market Report is Segmented by Device Technology (Radiofrequency (RF), Cryoablation, Ultrasound, and More), Application (Oncology, Cardiovascular Disease, Ophthalmology, and More), End-Users (Hospitals and Clinics, Ambulatory Surgical Centers, and More), Mode of Procedure (Percutaneous, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 38.82% of global revenue in 2024. A mature reimbursement system, accelerated FDA approvals, and strong replacement cycles sustain leadership. Boston Scientific treated more than 40,000 patients with FARAPULSE during its first commercial year, underscoring rapid uptake. The region also hosts leading research centers that generate pivotal data supporting new indications, which reinforces confidence across hospitals and ambulatory centers.

Asia-Pacific is the fastest-growing territory, projected at 12.52% CAGR to 2030. National health reforms and expanding device manufacturing in China and India lower procurement costs and improve availability. Japanese regulators authorized FARAPULSE in September 2024, and early hospital demand signals strong appetite for non-thermal technologies. Demographic shifts toward older populations and rising chronic disease prevalence assure continued growth of the ablation device market in the region.

Europe delivers steady expansion under a harmonized Medical Device Regulation framework that still promotes innovation while safeguarding patients. The early CE Mark approval of Abbott's Volt PFA system in March 2025 illustrates the region's role as a launchpad for advanced platforms. Academic hospitals continue to lead investigator-initiated studies, especially in oncology and neurologic uses, helping European clinicians refine protocols that ripple worldwide.