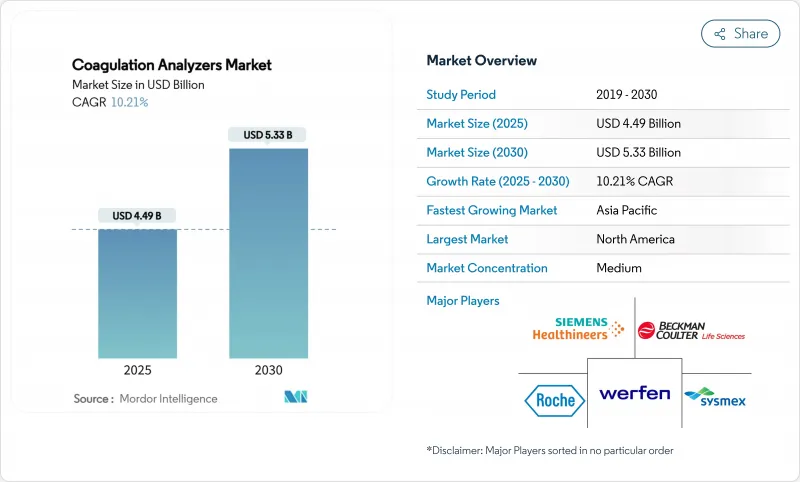

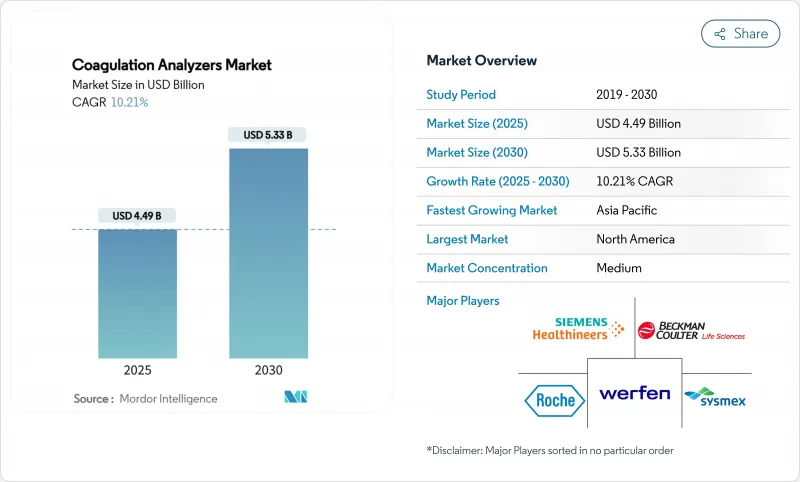

응고 분석기 시장의 규모는 2025년 44억 9,000만 달러, 2030년 53억 3,000만 달러에 이를 전망으로, CAGR 6.2%로 성장할 것으로 예측됩니다.

성장의 배경에는 실시간 점탄성 플랫폼으로의 이동, 품질 규제 강화, 기존 모니터링과 비교하여 유해 에피소드를 30% 삭감하는 AI 유도 투여의 보급 등이 있습니다. 점탄성 분석기는 수 분 내에 완전한 응고 프로파일을 제공하므로 수술 팀은 혈액 제형을 절약하고 수술 시간을 단축할 수 있습니다. 동시에 2025년 5월 클래스 II로 재분류되어 규제 장벽이 낮아지면서 지역 제조업체의 응고 분석기 시장 진입과 공급의 다양화를 촉진하고 있습니다. Werfen의 Accriva 인수와 Siemens와 Sysmex의 장기 OEM 계약 등 M&A의 활성화는 시약 라인과 임베디드 분석 확보 경쟁을 시사합니다.

혈우병은 27만 3,000명이 진단되었으며, 56만 3,000명이 질병을 가졌음에도 진단받지 못했을 가능성이 있습니다. 따라서, 정확한 응고 모니터링에 대한 수요가 증가하고 있습니다. 폰윌브렌트병은 여전히 가장 흔한 유전성 출혈성 질환으로, 환자의 72-94%가 임상 출혈 에피소드를 경험하고 있으며, 신속한 검사실에서의 확인이 필요합니다. 2025년 3월에 FDA로부터 인가된 fitusiran과 같은 새로운 치료제는 안티트롬빈 측정이 필요하며, 응고 분석기 시장은 더욱 확대되고 있습니다.

노인 인구에서 심방 세동의 급증은 장기적인 항응고 요법의 필요성을 높입니다. 트롬보엘라스토그래피는 노인 집단에서 기존 검사보다 우수한 출혈 예측 정확도를 보여줍니다. 아픽사반으로 대표되는 직접 경구 항응고제의 사용은 신약에 대한 시장의 이동을 보여주지만 여전히 정기적인 응고 검사가 필요합니다.

2024년 응고 분석기 시장에서 시스템 및 분석기는 60.2%의 점유율을 차지했습니다. 이는 검사실이 직원을 늘리지 않고 검사량 증가를 제어하기 위해 워크 어웨이 자동화를 선호했기 때문입니다. TEG 6s의 클리어런스로 점탄성 검사가 심장 수술로 확대되었기 때문에 포인트 오브 케어 장치가 가장 빠르게 보급되었습니다. 하이엔드 모델은 시간당 402건의 검사가 가능하며, 오전 사혈 피크시의 병목 현상을 줄이고 소모품 계약에서의 공급업체 종속을 강화하고 있습니다.

소모품은 응고 분석기 시장의 경상적인 백본을 형성합니다. 돼지 헤파린 혼입 경고가 세계적인 리콜의 방아쇠가 된 이후 시약 무결성에 대한 요구는 첨예해지고 있습니다. 이에 반해 2024년 지멘스와 시스멕스 협정과 같은 OEM 제휴는 안정적인 시약 파이프라인과 AI 대응 QC 팩의 전방 통합을 보장하고 있습니다. 캘리브레이션 재료는 CLIA의 정확도 목표를 강화함으로써 혜택을 받고 있으며, 실험실은 검증된 로트 간의 일관성을 갖춘 최고급 관리로 이동하고 있습니다.

PT/INR은 계속 만성 와파린 모니터링의 중심이며 2024년 응고 분석기 시장 규모의 30.6%를 차지하였습니다. 그럼에도 불구하고, 저분자 헤파린에 대한 항-Xa 측정을 선호하는 임상가가 증가하고 있으며, 이는 치료의 전환을 반영합니다. 한편 D 다이머는 CAGR 12.4%로 가장 빠르게 성장하고 있습니다. 응급 부문이 정맥 혈전 색전증의 치료와 COVID 후 응고 장애 모니터링에 D 다이머를 이용하고 있기 때문입니다.

피브리노겐과 혈소판 기능 패널은 외상 프로토콜과 항혈소판 약물의 조정을 지원합니다. 2025년 5월 클래스 II 재분류를 통해 새로운 카트리지 시장 출시 시간이 단축되어 세계의 지혈 애플리케이션(TEG과 ROTEM)은 수술실 뿐만 아니라 집중 치료 환경으로도 확대하고 있습니다.

북미는 자금력 있는 병원, 급속한 AI 도입, 유리한 환급제도에 힘입어 응고 분석기 시장을 선도하고 있습니다. 2025년 3월 FDA가 승인한 피투시란과 안티트롬빈 동반 분석은 치료 혁신이 진단 수요를 즉시 유도한다는 것을 보여줍니다. 캐나다에서는 단일 지불 모델이 전국적인 INR 관리 네트워크를 추진하고, 멕시코에서는 신흥 민간 병원 체인이 응급 외래 체류 시간을 단축하기 위해 포인트 오브 케어 장비에 투자하고 있습니다.

아시아태평양은 가장 빠르게 발전하는 지역으로, 인프라의 신속한 정비와 정기적인 응고 모니터링이 필요한 노인 인구 증가를 반영합니다. 세계 최대의 헤파린 공급국인 중국의 역할은 비용면에서 유리한 반면 원료 충격의 영향을 받기 쉽습니다. 한편, 인도에서는 최근의 규제 개혁에 의해 중처리량 분석기의 국내 제조의 길이 열렸습니다. 시스멕스의 2025년 1분기 지역별 매출은 두 자릿수의 증가를 보였으며 시약과 통제 수요가 충족되지 않았다는 것이 밝혀졌습니다.

유럽은 높은 과학적 능력과 IVDR 준수라는 부담 사이에서 균형을 맞추고 있습니다. 독일, 프랑스, 영국은 대규모 레퍼런스 랩 네트워크를 운영하고 있으며, 대부분의 새로운 문서화 의무를 다루고 있지만 소규모 센터에서는 비용이 많이 드는 검증 작업에 직면하고 있습니다. 또한 영국에서는 NHS의 혈액 부족 에피소드가 적절한 수혈을 위한 점탄성 검사의 중요성을 돋보이게 합니다.

The coagulation analyzers market size stands at USD 4.49 billion in 2025 and is forecast to touch USD 5.33 billion by 2030, advancing at a 6.2% CAGR.

Growth stems from the shift toward real-time viscoelastic platforms, tighter quality regulations, and wider adoption of AI-guided dosing that trims adverse events by 30% compared with conventional monitoring. Viscoelastic analyzers deliver complete clotting profiles within minutes, enabling surgical teams to save blood products and shorten operating room time. At the same time, Class II re-classification in May 2025 has lowered regulatory barriers, encouraging regional manufacturers to enter the coagulation analyzers market and diversify supply. Intensifying M&A activity-such as Werfen's purchase of Accriva and the long-term Siemens-Sysmex OEM pact-signals a race to secure reagent lines and embedded analytics.

Hemophilia affects 273,000 diagnosed individuals, with an additional 563,000 likely undiagnosed, elevating demand for precise coagulation monitoring.Von Willebrand disease remains the most common hereditary bleeding disorder, and 72-94% of patients experience clinical bleeding episodes that benefit from rapid laboratory confirmation. New therapies such as fitusiran, cleared by the FDA in March 2025, require antithrombin assays, further broadening the coagulation analyzers market.

Surging atrial fibrillation prevalence in seniors heightens long-term anticoagulation needs. Thromboelastography demonstrates superior bleed-prediction accuracy versus conventional tests in elderly cohorts. Direct oral anticoagulant uptake, led by apixaban, underlines a market pivot toward newer drugs that still warrant episodic coagulation checks.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Systems and analyzers held a 60.2% share of the coagulation analyzers market in 2024 as laboratories prioritized walk-away automation to control rising test volumes without adding staff. Point-of-care units posted the quickest uptake, supported by the TEG 6s clearance that expanded viscoelastic testing into cardiac theaters. Robust throughput-402 tests per hour on high-end models-reduces bottlenecks during morning phlebotomy peaks, cementing vendor lock-in through consumable contracts.

Consumables form the recurring backbone of the coagulation analyzers market. Reagent integrity demands have sharpened since porcine-heparin contamination alerts triggered global recalls. In response, OEM alliances such as the 2024 Siemens-Sysmex pact guarantee steady reagent pipelines and forward-integration of AI-enabled QC packs. Calibration materials also benefit from stricter CLIA precision goals, nudging laboratories toward premium controls with validated lot-to-lot consistency.

PT/INR continues to anchor chronic warfarin surveillance, capturing 30.6% of coagulation analyzers market size in 2024. Nonetheless, clinicians increasingly prefer anti-Xa assays for low-molecular-weight heparin, reflecting therapy migration. D-Dimer, meanwhile, is posting the fastest 12.4% CAGR as emergency departments rely on it to triage venous thromboembolism and monitor post-COVID coagulopathy.

Fibrinogen and platelet-function panels round out the catalog, supporting trauma protocols and antiplatelet agent adjustment. Global hemostasis applications-TEG and ROTEM-are expanding beyond operating theaters into intensive-care settings, fueled by the May 2025 Class II reclassification that trimmed time-to-market for new cartridges.

The Coagulation Analyzers Market is Segmented by Product (Systems/Analyzers {High, and More} and Consumables {Reagents & Assays, and More), Test Type (Prothrombin Time, and More), Technology (Optical, Mechanical, and More), Modality (Central-Laboratory Platforms, and More), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America leads the coagulation analyzers market, supported by well-funded hospitals, rapid AI adoption, and favorable reimbursement frameworks. The March 2025 FDA approval of fitusiran with a companion antithrombin assay illustrates how therapeutic innovation immediately triggers diagnostic demand. Canada's single-payer model drives nationwide INR management networks, while Mexico's emerging private hospital chains are investing in point-of-care devices to shorten emergency room stay times.

Asia Pacific is the fastest-advancing region, reflecting swift infrastructure upgrades and growing senior populations that require routine coagulation surveillance. China's role as the world's largest heparin supplier offers cost advantages but also vulnerability to raw-material shocks. Japan's stringent device review process ensures high laboratory standards, whereas recent regulatory reforms in India have opened pathways for domestic manufacturing of mid-throughput analyzers. Sysmex reported double-digit regional sales growth in Q1 2025, underscoring unmet demand for reagents and controls.

Europe balances strong scientific capability with the added burden of IVDR compliance. Germany, France, and the United Kingdom operate expansive reference-lab networks that already meet most new documentation mandates, but smaller centers face costly validation work. Supply concerns around porcine-derived reagents have sparked pilot studies into bovine alternatives, while NHS blood shortage episodes in England spotlight the importance of viscoelastic testing for judicious transfusion practice.