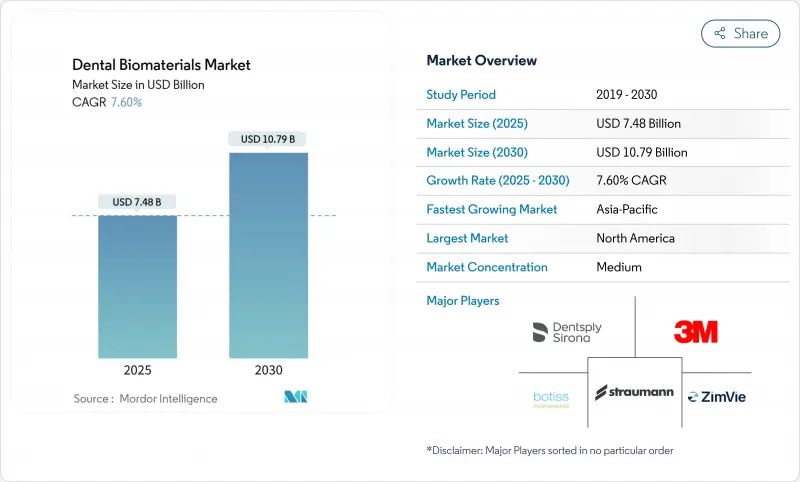

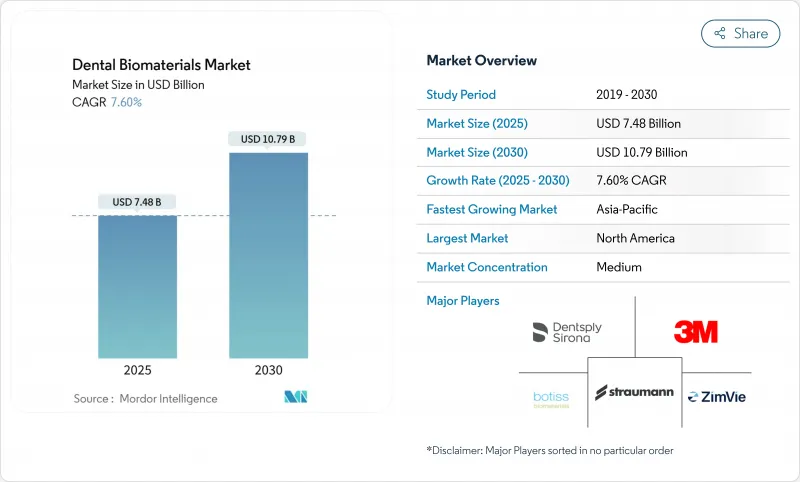

치과용 바이오소재 시장은 2025년에 74억 8,000만 달러, 2030년에는 107억 9,000만 달러에 이를 전망으로, CAGR 7.6%로 성장할 것으로 예측됩니다.

고령화에 따른 무치악증 증가, 임플란트 치료 보험 적용 범위 확대, 치과 관광의 확대로 구매 의사결정과 공급망 우선순위가 변화하고 있습니다. CAD/CAM 밀링, 3D 프린팅, 나노엔지니어링의 급속한 도입으로 보수 사이클이 단축되어 생체활성 세라믹과 하이브리드 컴포지트의 프리미엄 가격대가 확대되고 있습니다. 2025년 이후 출시되는 뼈 형성을 자극하는 재생 스캐폴드는 수동적 적합성에서 능동적인 조직 통합으로의 전환을 보여줍니다. 아시아태평양 기공소와의 가격 경쟁이 치열해지면서 유럽과 미국의 제조업체는 지르코니아 조달을 강화하고 진료 디지털 워크플로우를 강화하며 편의성과 심미성에 대한 진화하는 환자의 기대에 따라 당일 크라운과 브리지를 실현합니다.

평균 수명의 장기화와 구강 기능에 대한 기대 증가는 치과용 바이오소재 시장의 수요를 변화시키고 있습니다. 무치악률은 여전히 65세 이상에서 가장 높고, 이 층에서는 금속을 사용하지 않고, 천연의 에나멜질에 가까운 심미성이 높은 재료를 요구하는 경향이 강해지고 있습니다. 탈착식 의치에서 임플란트 고정 수복물로의 전환은 북미와 서유럽에서 특히 두드러지며, 공공 및 민간 보험 회사가 임플란트 치료의 적용 범위를 점차 넓히고 있습니다. 또한 노인은 뼈가 점점 약화되기 때문에 부식 위험을 피하고 연조직 반응을 촉진하기 위한 산화 세라믹 임플란트로의 전환이 임상가에게 촉구되었습니다. 2025년부터 2030년까지 활동적인 노인 인구가 가장 큰 구매층을 차지할 것으로 예상되며, 이들의 고급 소재에 대한 지불 의향을 바탕으로 밸류체인의 다른 부분에서 발생하는 가격 압력을 상쇄해야 합니다.

임플란트의 평균 5년 보존율은 현재 95%를 넘어 임상에서의 망설임이 해소되어 환자 적용 범위가 넓어졌습니다. CBCT 이미지, 수술 가이드 슬리브, 즉석 밀링을 통합한 치료 워크플로우는 수술 시간을 크게 단축하여 바쁜 도시의 클리닉에서도 임플란트 치료를 시행할 수 있게 되었습니다. Straumann과 같은 공급업체는 환자 방문 횟수를 40% 줄이는 프로토콜을 도입했으며, 클리닉은 환자 만족도를 높이면서 일일 치료량을 향상시킬 수 있습니다. 표면 텍스처링 기술과 생물학적 활성 코팅은 골유착의 속도를 높이고 치유에 오랜 시간을 투자할 수 없는 젊은 세대 환자에게 호소하는 즉각적인 프로토콜을 실현합니다. 이러한 역학은 치과용 바이오소재 시장의 규모를 확대시키고 픽스처 자체를 보완하는 이식편, 멤브레인, 어버트먼트 재료 수요를 자극하고 있습니다.

프리미엄 지르코니아 블랭크, 골유도성 이식편, 나노코팅된 임플란트는 기본 등급 대체품의 2배에서 5배의 가격으로 판매되는 경우가 많으며, 저소득 환경에서 현금으로 결제하는 환자는 접근하기 어렵습니다. OECD 회원국의 대부분에서 치과의 보험 급여 상한액은 연간 2,000달러 이하로 하락하였으며 환자는 자비로 대규모 재활을 수행해야 합니다. 2025년 4월, 새로운 관세로 인해 미국의 특정 수입 치과 재료의 육상 가격에 최대 54% 인상되었으며, 임상의는 재고 전략을 재검토해야만 했습니다. 이러한 가격 충격은 혁신적인 치과 재료의 보급을 지연시킬 수 있습니다. 공급업체는 계층화된 제품 라인과 구독 기반 소모품 번들로 지원되지만, 합리적인 가격은 여전히 치과 바이오소재 시장의 중대한 발판이 되고 있습니다.

2024년 치과 바이오소재 시장 점유율은 금속이 44.56%를 차지하였으며 티타늄의 입증된 생체역학적 프로파일과 임상의에 대한 친숙함에 의해 뒷받침되고 있습니다. 단위 수량은 내피로성이 심미적인 우려보다 우선시되는 어금니 후부의 내하중 구역과 풀 아치 보철로 높은 수준을 유지하고 있습니다. 그러나 지르코니아로 대표되는 세라믹은 투광성의 진보에 의해 리튬 디실리게이트 유리와의 시각적인 차이가 줄어들어 CAGR 8.97%로 성장하고 있습니다. 금속이 없는 수복물에 대한 소비자 수요 증가와 알레르기 반응에 대한 민감성이 증가함에 따라 세라믹으로의 전환이 가속화되고 있습니다. 공급업체는 현재 굽힘 강도의 코어와 에나멜질과 같은 표면층을 혼합한 다층 지르코니아 디스크를 판매하고 있으며, 베니어 없이 의자 측면에서 깎아내는 원피스 풀 콘터 크라운을 실현하고 있습니다. 이러한 능력은 일회 방문으로 끝나는 치과 치료의 동향과 일치하고 있으며, 세라믹은 치과용 바이오소재 시장에서 지속적인 점유율 확대를 기대할 수 있습니다.

디지털 설계 요구 사항은 모든 재료 클래스에서 R&D 과제를 재구성합니다. 폴리머를 침투시킨 새로운 세라믹 네트워크는 하이브리드 적응증을 목표로 하고 있으며, 금속에 필적하는 파괴 내성과 길항 마모를 완화하는 연마 특성이 기대되고 있습니다. 동시에, 나노필러를 스캐폴드로 하는 수지 매트릭스 복합재는 경량화가 중요한 중기 및 장기 적응증을 해결하고 있습니다. 금속 분야에서 콜드 스프레이와 선택적 레이저 용융 공정은 다공성을 감소시키고 피질골에 가까운 탄성을 조절하는 격자 구조가 가능해지고 있습니다. 이러한 개선은 심미 치과가 세라믹으로 기울어지는 가운데 특수 증례에서 금속의 지위를 강화합니다. 그 결과, 경쟁 구도는 미묘하게 변화하고 각 제제는 가격과 성능의 틈새가 명확하게 구분되어 광범위한 치과용 바이오소재 시장에서 복수의 재료가 공존하고 있습니다.

2024년 치과용 바이오소재 시장 규모에서는 픽스처, 어버트먼트, 이식편, 배리어 등의 복합적인 수요로 임플란트 치료가 49.76%의 점유율을 차지하였습니다. 임플란트는 생존 가능한 뼈가 존재하는 경우 언제든지 기본 표준 치료가 되고 있으며, 위험한 경우에도 임상의는 탈착 가능한 인공 치아를 선택하는 것이 아니라 가이드가 있는 뼈 재생에 의존하는 경우가 많습니다. 그러나 재생 치과는 세포 함유 하이드로겔과 성장 인자를 침투시킨 막의 획기적인 진보에 힘입어 CAGR 9.23%로 다른 그룹을 압도하고 내인성 치유를 자극하고 있습니다. 산학 연계에 의해 에나멜 매트릭스 유도체는 치주 치료에서 치조골로의 폭넓은 응용으로 이행하고 있으며, 치과용 바이오소재 시장에서 장래적으로 큰 수익을 기대할 수 있는 가능성을 보여주고 있습니다.

분야 간 중복이 증가하고 있으며 복잡한 풀 아치의 경우에는 임플란트 치료와 사이너스 리프트 이식과 온레이 재생막을 병용하는 경우가 많아 카테고리의 경계가 모호해지고 환자 1인당 평균 판매 가격이 상승하고 있습니다. 치내 치료는 또한 바이오 세라믹 실러를 사용하여 재생 가능한 치근 형성을 가능하게 하고 발치를 지연시킬 수 있기 때문에 활성화되었습니다. 베타 티타늄 합금으로 만들어진 치열 교정용 앵커 스크류는 임플란트 주변의 염증을 억제하기 위해 항균 나노 실버로 전처리되어 재료 과학의 지속적인 상호 발전을 보여줍니다. 따라서 경쟁 기회는 단일 제품보다 응용 분야에 관계없이 적응 가능한 플랫폼 기술에 달려 있으며, 치과용 바이오소재 시장에서 광범위한 포트폴리오를 가진 공급업체가 유리한 동향이 나타나고 있습니다.

북미는 임플란트 수술의 이환율이 높고, 보험 진료의 보급률이 높으며, 디지털 진료 시스템의 급속한 보급으로 치과용 바이오소재 시장에서 유일하게 가장 규모가 큰 지역입니다. 미국에서는 노인 퇴직자들이 모이는 선벨트 지역의 주에서 현저한 수요가 나타나고 있으며 치과 개업의가 재료 프로토콜을 표준화한 확장 가능한 케어 모델을 전개하고 있습니다. 캐나다는 이러한 동향을 반영하여 규모는 작지만, 공적 환급의 틀의 혜택을 받고 있으며 현재는 고령자를 위한 특정 임플란트 치료에 자금이 제공되어 대응 가능한 증례 수가 확대되고 있습니다.

유럽은 하위 지역에 따라 성장 패턴이 다르게 나타나고 있습니다. 서유럽에서는 노후화된 고정식 인공 치근의 교체 주기를 유지하고, 금속이 없는 치아를 요구하는 환자의 요구에 부응하여 세라믹 기반 재료를 선호하는 경향이 강해지고 있습니다. 폴란드와 헝가리로 대표되는 중유럽과 동유럽은 주로 독일과 북유럽 환자를 대상으로 한 치과 관광이 활성화되면서 더 저렴한 치료비를 요구받고 있습니다. 이러한 유입으로 클리닉은 브랜드 임플란트와 고투과성 지르코니아를 구매하게 되고 평균 판매 가격이 상승하여 치과 바이오소재 시장이 성장하고 있습니다.

아시아태평양은 가처분 소득 증가, 적극적인 인프라 투자, 한국과 일본의 노인 임플란트 치료 보조금 등 정부의 지원책에 힘입어 가장 급속한 확대를 기록하고 있습니다. 중국의 대형 도시에서는 나노가공 인공 치근을 생산하는 최첨단 대학 스핀오프가 진행되고 있지만, 보험 적용에는 변동이 있기 때문에 도입은 해안부의 대도시로 치우칩니다. 인도와 동남아시아는 의료관광객의 귀국과 비용경쟁력 있는 노동력으로 인해 이익을 얻고 있지만 고급 바이오소재에 대한 수입관세가 클리닉을 국내 대체품으로 향하게 하고 있습니다. 이러한 벡터를 종합하면 이 지역은 세계의 치과용 바이오소재 시장에서 사업을 전개하는 공급업체에게 가장 큰 성장 엔진이 됩니다.

The dental biomaterials market stands at USD 7.48 billion in 2025 and is forecast to reach USD 10.79 billion by 2030, advancing at a 7.6% CAGR.

Rising edentulism in aging populations, broader insurance coverage for implantology, and expanding dental tourism corridors are reshaping purchase decisions and supply-chain priorities. Rapid adoption of CAD/CAM milling, 3D printing, and nano-engineering is shortening restoration cycles and opening premium pricing tiers for bioactive ceramics and hybrid composites. Post-2025 launches of regenerative scaffolds that stimulate osteogenesis represent a pivot from passive compatibility to active tissue integration. Intensifying price competition from Asia-Pacific laboratories compels Western manufacturers to refine zirconia sourcing and intensify chair-side digital workflows, allowing same-day crowns and bridges that align with evolving patient expectations for convenience and aesthetics.

Longer life expectancy combined with higher expectations for oral function is transforming demand in the Dental biomaterials market. Edentulous rates remain highest in people over 65, and this cohort increasingly requests metal-free, highly aesthetic materials that closely replicate natural enamel. The pivot from removable dentures to implant-anchored restorations is especially clear in North America and Western Europe, where public and private insurers are slowly broadening coverage for implant therapy. Senior patients also present more challenging bone physiology, which has encouraged clinicians to switch toward oxide-ceramic implants to avoid corrosion risk and facilitate soft-tissue response. Between 2025 and 2030, active seniors are expected to constitute the single largest purchasing segment, and their willingness to pay for premium materials should offset pricing pressure elsewhere in the value chain.

Average five-year implant survival now exceeds 95%, a milestone that has removed long-standing clinical hesitancy and widened patient eligibility. Treatment workflows that integrate CBCT imaging, guided-surgery sleeves and chair-side milling cut operative times dramatically, making implant therapy viable for busy urban clinics. Suppliers such as Straumann have introduced protocols that trim patient visits by 40%, allowing practices to generate higher daily throughput while improving patient satisfaction. Surface-texturing technologies and bioactive coatings push osseointegration speed higher, enabling immediate-load protocols that appeal to younger, working-age patients who cannot accommodate lengthy healing periods. These dynamics are multiplying unit volumes in the Dental biomaterials market and stimulating demand for grafts, membranes and abutment materials that complement the fixture itself.

Premium zirconia blanks, osteoinductive grafts and nano-coated implants often retail at two to five times the price of base-grade alternatives, placing them out of reach for cash-pay patients in low-income settings. Insurance cover remains patchy; in many OECD countries the benefit caps for dental still sit below USD 2,000 per year, forcing patients to self-fund extensive rehabilitation. In April 2025, new tariffs added up to 54% to the landed price of certain imported dental materials in the United States, prompting clinicians to reassess inventory strategies. These price shocks threaten to slow diffusion of innovative materials just as clinical evidence mounts in their favour. Suppliers are responding with tiered product lines and subscription-style consumable bundles, but affordability remains a critical drag on the Dental biomaterials market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Metals commanded 44.56% capture of the Dental biomaterials market share in 2024, underpinned by titanium's proven biomechanical profile and clinician familiarity. Unit volumes remain high in posterior load-bearing zones and full-arch prosthetics, where fatigue resistance overrides aesthetic concerns. Yet ceramics, led by zirconia, are growing at an 8.97% CAGR as translucency advances narrow the visual gap with lithium-disilicate glass. Elevated consumer demand for metal-free restorations along with growing sensitivity to allergic reactions accelerates the ceramic migration path. Suppliers now pitch multi-layer zirconia discs that blend flexural strength cores with enamel-like surface layers, allowing one-piece full-contour crowns milled chair-side without veneering. That capability aligns neatly with single-visit dentistry trends and positions ceramics for continued share gain inside the Dental biomaterials market.

Digital design requirements are reshaping R&D agendas across all material classes. New polymer-infiltrated ceramic networks target hybrid indications, promising fracture toughness comparable to metals and polishing behaviour that mitigates antagonist wear. At the same time, resin-matrix composites with nano-filler scaffolds are capturing interim and long-span indications where weight savings matter. In the metals segment, cold-spray and selective-laser-melting processes are lowering porosity and enabling lattice-style structures that tune elasticity closer to cortical bone. Such improvements reinforce the incumbent position of metals in specialty cases even as cosmetic dentistry swings toward ceramics. The result is a nuanced competitive landscape in which each formulation occupies a clearly delineated price-performance niche, sustaining multi-material coexistence within the broader Dental biomaterials market.

Implantology retained 49.76% share of the Dental biomaterials market size in 2024 thanks to its composite demand for fixtures, abutments, grafts and barriers that extend the revenue footprint of every procedure. Implants have become the default standard of care whenever viable bone is present, and even in compromised cases clinicians increasingly rely on guided-bone-regeneration rather than opting for removable prostheses. However, regenerative dentistry outpaces all other groups with a 9.23% CAGR, propelled by breakthroughs in cell-laden hydrogels and growth-factor soaked membranes that stimulate endogenous healing. Academic-industry partnerships are moving enamel-matrix derivatives from periodontal therapy into broader alveolar-bone applications, setting the stage for a sizeable future revenue pocket inside the Dental biomaterials market.

Interdisciplinary overlaps are rising. Complex full-arch cases often marry implantology with sinus-lift grafts and onlay regenerative membranes, blurring category lines and lifting average selling prices per patient. Endodontics too is being revitalised as bioceramic sealers enable regenerative apexification protocols that keep teeth viable and delay extraction. Orthodontic anchorage screws fabricated from beta-titanium alloys now come pretreated with antibacterial nano-silver to limit peri-implantitis, illustrating continuous cross-pollination of material science. The competitive opportunity therefore hinges on platform technologies adaptable across applications rather than on standalone products, a trend that favours suppliers with broad portfolios in the Dental biomaterials market.

The Dental Biomaterials Market Report Segments Into by Type (Metallic Biomaterials, Ceramic Biomaterials, and More), by Product Category (Dental Bone Graft Substitutes, Barrier Membranes and More), by Application (Orthodontics, Prosthodontics, and More), by End User (Dental Clinics, Dental Laboratories and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remains the single largest regional contributor to the Dental biomaterials market, driven by a high incidence of implant procedures, robust insurance penetration, and rapid adoption of digital chair-side systems. The United States sees pronounced demand in sun-belt states where older retirees cluster and where DSOs roll out scalable care models that standardise material protocols. Canada mirrors these trends on a smaller scale but benefits from public reimbursement frameworks that now fund select implant cases for seniors, extending addressable volume.

Europe follows closely, though growth patterns vary by sub-region. Western Europe sustains replacement cycles for ageing fixed prostheses and increasingly favours ceramic-based materials in response to patient demand for metal-free smiles. Central and Eastern Europe, led by Poland and Hungary, have built a thriving dental tourism corridor catering primarily to German and Nordic patients seeking lower procedure costs. This inflow pushes clinics to stock branded implants and high-translucency zirconia, lifting average selling prices and enriching the Dental biomaterials market.

Asia-Pacific records the fastest aggregate expansion, propelled by rising disposable incomes, aggressive infrastructure investments, and supportive government measures in South Korea and Japan that subsidise implant therapy for seniors. China's tier-one cities host cutting-edge university spin-offs producing nano-engineered grafts, yet uneven insurance cover keeps adoption skewed toward coastal metros. India and Southeast Asia benefit from returning medical tourists and cost-competitive labour, though import tariffs on premium biomaterials push clinics toward domestic alternatives. Collectively these vectors position the region as the foremost incremental growth engine for suppliers operating in the global Dental biomaterials market.