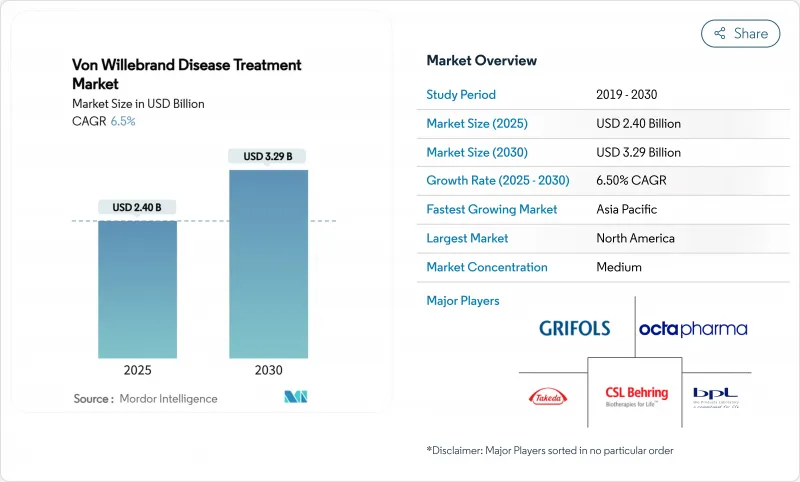

폰빌레브란트병 치료 시장은 2025년에 24억 달러, 2030년에는 32억 9,000만 달러에 이를 전망으로, 예측 기간 중 CAGR은 6.5%로 예상됩니다.

근치적인 유전자 치료의 보급, AI가 지원하는 진단의 급속한 보급, 가치에 기초한 환급을 수용하는 지불자로 인해 수익의 성장이 가속화하고 있는 한편, 병원의 처방전에서는 혈장 유래의 선택보다 재조합형의 병원체를 포함하지 않는 농축 제제가 점점 선호되고 있습니다. 북미의 연방 정부에 의한 환자 지원 제도의 확대, 아시아태평양에서의 신생아 유전자 스크리닝의 확대, 데스모프레신 나노 피하 제제의 신속 심사 등도 대응 가능한 수요를 확대하고 있습니다. 2024-2025년에 승인된 화이자의 BEQVEZ나 CSL 베링의 HEMGENIX와 같은 유전자 치료제는 평생의 인자 소비를 줄이는 일회성 개입이라는 전망을 만들어 냈습니다. 강력한 모멘텀에도 불구하고 폰빌레브란트병 치료 시장은 저소득 지역에서의 과소 진단, 유전자 치료의 높은 초기 비용, 혈장 제품의 온도에 민감한 공급망에 여전히 직면하고 있습니다.

141개의 혈우병 치료 센터에 대한 연방 정부의 자금 지원을 통해 공급자는 340B 프로그램 하에서 할인된 가격으로 인자 제제를 조제할 수 있게 되며, 자기 부담액을 줄이고 어드히어런스를 향상시킬 수 있습니다. 캘리포니아의 All Copays Count 법과 같은 주 차원의 조치는 경제적 장애물을 더욱 낮추고 CMS는 응고 인자 제제 제공료를 꾸준히 인상하고 예측 가능한 환급을 보장합니다. 이러한 조치는 충분한 치료를 받지 않은 환자도 치료를 받을 수 있게 하고, 폰빌레브란트병 치료 시장 전체 수요를 유지하고 있습니다. 이 멀티스테이크 홀더 모델이 유럽이나 신흥국에서도 실현되면 세계적인 확산이 기대됩니다. 자선재단은 보험에 가입하지 않은 성인의 예방약에도 자금을 제공하고 있으며, 치료 건수를 밀어 올리고 있습니다.

신생아 스크리닝에 건조 혈액 스팟 바이오마커 패널을 추가하고 있는 국가에서는 루틴 검사에서는 발견에 실패한 출혈성 질환의 검출 정밀도가 95%에 달하고 있습니다. 아시아태평양 보건부는 유사한 프로그램을 확대하고 시험적인 주에서는 VWD의 인지 인구를 두 배로 늘리고 있습니다. 스웨덴에서는 NT-proBNP와 IL-1 RL1의 바이오마커를 도입함으로써 조기 발견이 어떻게 진단을 유아기로 이동시켜 시기 적절한 개입을 촉진하고 폰빌레브란트병 치료 시장을 확대하는지를 보여줍니다. ATHN의 자연사 레지스트리와 함께 실제 임상 치료 성적 데이터는 적극적인 치료에 대한 지불 보험 회사의 보험 적용을 뒷받침하고 있습니다. 진단의 급증으로 평생 치료 또는 근치 치료가 필요한 환자의 안정적인 파이프라인이 구축됩니다.

많은 개발도상국에서는 예상되는 사례의 10% 미만만이 진단되어 치료에 대한 수요의 성장을 억제하고 있습니다. 검사 능력이 제한되어 있고, 응고 시약이 부족하며, 임상의의 의식이 낮기 때문에 VWD의 증상이 부인과 질환이나 감염증으로 오인되는 경우가 많습니다. 투자의 우선순위가 전염병에 편향되어 있기 때문에 전문가의 진단 도입이 늦어지고 있습니다. 국제 기부자와의 파트너십은 여전히 소규모이기 때문에 커버 갭이 조기에 해소될 전망이 없으며, 세계의 폰빌레브란트병 치료 시장의 확대를 저해하고 있습니다.

1형 VWD는 2024년 세계 매출액의 72.35%를 차지하면서 같은 해 폰빌레브란트병 치료 시장 규모의 대부분을 차지했습니다. 경증 VWD는 저렴한 데스모프레신에 의존하며 예측 가능한 시장 규모를 유지합니다. 후천성 VWD는 현재 규모는 작으나, 암 전문의나 순환기 전문의가 환자의 전처리를 실시하기 때문에 2030년까지의 CAGR이 11.25%로 가장 급속하게 확대될 전망입니다. 2A형은 특히 고분자량 다량체를 회복시켜 연간 출혈률을 저하시키는 유전자 재조합 VWF 제제가 유효합니다.

중증이지만 드문 3형 코호트에서는 집중적인 인자 수주와 정형외과 수술을 위해 불균형적인 비용이 초래되며, 신흥국에서의 환급 과제가 부각되고 있습니다. 장기간의 센터에서의 경험은 모든 유형에서 진단 부족이 계속되고 있음을 보여 주며, 레지스트리의 확대와 유전자 검사에 대한 지불자의 지원이 요구되고 있습니다. 고령화 사회에서의 약제성 VWD에 대한 인식 증가는 VWD 치료 시장을 더욱 확대시킵니다.

북미는 2024년 매출의 38.82%를 차지하였으며 제품 접근을 보장하는 340B 할인과 종합적인 치료 시설 네트워크에 뒷받침되고 있습니다. 유전자 치료 보험 환급의 틀은 미국에서 최초로 확립되어 조기 도입과 높은 가격 설정이 가능하게 되었습니다. 캐나다는 각 주의 처방 검토에 따라 다소 늦어지지만 혈장 조달의 중앙 집중화에서 혜택을 누릴 수 있습니다.

유럽에서는 각국의 지불자가 바이러스에 안전한 농축 제제를 요구하고 있기 때문에 유전자 재조합 제제의 채용률은 높지만, 의료 기술 평가가 엄격하기 때문에 일부 신규 치료가 늦어지고 있습니다. 서유럽시장에서는 유전자치료의 위험분담에 대해 협상을 하고 있으며 지속적인 요인에 의존하지 않는 것을 지불에 반영함으로써 폰빌레브란트병 치료제 시장의 구매 동역학을 형성하고 있습니다. 동유럽에서는 예산이 적고 진단약의 보급이 늦어져 양극화의 양상을 나타내고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.61%로 성장을 이끌 전망이며, 이는 규제 당국이 심사 경로를 합리화하고 각국 정부가 현지 제조에 투자하고 있기 때문입니다. 중국, 인도, 한국은 신생아 스크리닝 패널을 확대하고 농후제제의 수입에 보조금을 내는 것으로 두 자릿수의 수량 증가를 견인하고 있습니다. 남미에서는 특히 브라질이 경제적 제약에도 불구하고 집중 구매와 임상 프로토콜의 표준화를 활용하여 액세스를 확대하고 있습니다. 대조적으로 중동 및 아프리카에서는 진단과 콜드체인의 결함이 진전을 방해하고 있지만, 재조합 가격 하락으로 예측 후반부에 잠재 수요가 발굴될 수 있습니다.

The Von Willebrand disease treatment market stood at USD 2.40 billion in 2025 and is on track to reach USD 3.29 billion by 2030, translating into a 6.5% CAGR over the forecast window.

Uptake of curative gene therapies, rapid adoption of AI-supported diagnostics, and payer acceptance of value-based reimbursement are accelerating revenue growth, while hospital formularies increasingly favor recombinant, pathogen-free concentrates over plasma-derived options. Expansion of federal patient-assistance schemes in North America, wider newborn genetic screening in Asia-Pacific, and fast-track review of subcutaneous desmopressin nano-formulations also deepen addressable demand. Gene therapies such as Pfizer's BEQVEZ and CSL Behring's HEMGENIX, both cleared in 2024-2025, create the prospect of one-time interventions that reduce lifelong factor consumption. Despite strong momentum, the Von Willebrand disease treatment market still contends with under-diagnosis in low-income geographies, high upfront gene-therapy costs, and temperature-sensitive supply chains for plasma products.

Federal funding for 141 Hemophilia Treatment Centers lets providers dispense discounted factor products under the 340B program, reducing out-of-pocket costs and improving adherence. State action, such as California's All Copays Count law, further lowers financial hurdles, while CMS has steadily raised the clotting-factor furnishing fee, ensuring predictable reimbursement. These measures make therapies accessible to underserved patients, sustaining demand across the Von Willebrand disease treatment market. Replication of this multi-stakeholder model in Europe and emerging economies is expected to widen global reach. Charitable foundations also finance prophylaxis for uninsured adults, boosting treatment volume.

Countries adding dried-blood-spot biomarker panels to newborn screening achieve 95% detection accuracy for bleeding disorders that routine tests miss. Asia-Pacific health ministries are scaling similar programs, doubling the recognized VWD population in pilot provinces. Sweden's inclusion of NT-proBNP and IL-1 RL1 biomarkers illustrates how early detection shifts identification to infancy, prompting timely intervention and enlarging the Von Willebrand disease treatment market. Together with ATHN's natural-history registry, real-world outcome data now drives payer coverage for proactive treatments. The diagnostic surge builds a stable pipeline of patients requiring lifelong or curative therapies.

Many developing countries identify fewer than 10% of expected cases, curbing demand growth for therapies. Limited laboratory capacity, scarce coagulation reagents, and low clinician awareness mean VWD symptoms are often misattributed to gynecological or infectious conditions. Investment priorities favor communicable diseases, delaying introduction of specialist diagnostics. International donor partnerships remain small-scale, so coverage gaps are unlikely to close quickly, weighing on the global Von Willebrand disease treatment market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Type 1 VWD generated 72.35% of global revenue in 2024, anchoring the Von Willebrand disease treatment market size for that year. Prevalent mild phenotypes rely on affordable desmopressin, sustaining predictable volumes. Acquired VWD, while smaller today, delivers the fastest expansion at 11.25% CAGR through 2030 as oncologists and cardiologists test patients pre-procedure. Type 2 sub-variants together add clinical complexity because they require concentrate prophylaxis; Type 2A cases especially benefit from recombinant VWF-only products that restore high-molecular-weight multimers, reducing annual bleed rate.

The severe but rare Type 3 cohort incurs disproportionate costs due to intensive factor infusions and orthopedic surgeries, highlighting reimbursement challenges in emerging economies. Long-term center experience shows persistent under-diagnosis across all types, prompting calls for registry expansion and payer support for genetic testing. Growing awareness of drug-induced VWD in aging populations further enlarges the Von Willebrand disease treatment market.

The Von Willebrand Disease Treatment Market Report is Segmented by Disease Type (Type 1, Type 2, Type 3, and Acquired VWD), Treatment Type (Desmopressin, VWF/FVIII Combination Concentrates, Recombinant VWF-Only Concentrates, and More), Route of Administration (Oral, Intravenous, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America contributed 38.82% of 2024 revenue, underpinned by 340B discounts and comprehensive treatment-center networks that guarantee product access. Gene therapy reimbursement frameworks emerge first in the United States, enabling earlier adoption and supporting premium pricing. Canada trails slightly due to provincial formulary reviews but benefits from centralized plasma procurement.

Europe exhibits high recombinant uptake as national payers demand virus-safe concentrates, yet stringent health-technology assessments delay some novel therapies. Western European markets negotiate risk-sharing deals for gene therapy, tying payment to sustained factor independence, which shapes purchasing dynamics in the Von Willebrand disease treatment market. Eastern Europe faces tighter budgets and slower diagnostic rollout, creating a two-tier landscape within the region.

Asia-Pacific leads growth with a 10.61% CAGR through 2030 because regulators are streamlining review pathways and governments are investing in local manufacturing. China, India, and South-Korea expand newborn-screening panels and subsidize concentrate imports, driving double-digit volume gains. South America, notably Brazil, leverages centralized purchasing and clinical-protocol standardization to broaden access despite economic constraints. In contrast, Middle East and Africa progress is hampered by diagnostic and cold-chain deficits, although recombinant price declines could unlock latent demand later in the forecast.