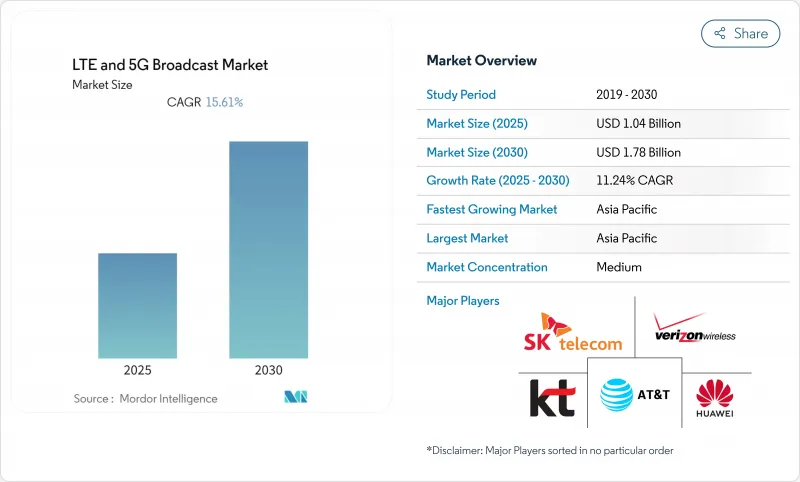

LTE 및 5G 방송 시장 규모는 2025년에 10억 4,000만 달러로 추정되고, 2030년에는 17억 8,000만 달러에 이를 것으로 예측되며, CAGR 11.24%로 성장할 전망입니다.

주파수 효율적인 비디오 전달, 긴급 경보의 현대화, 급속한 디바이스의 보급에 대한 수요 증가로 상용시험이 전국 전개로 확대되고 있습니다. 통신 사업자는 멀티캐스트 유연성과 AI 주도 자원 할당을 얻기 위해 레거시 LTE eMBMS에서 5G FeMBMS로 전환하고 있으며, 방송 사업자는 ATSC 3.0-5G의 하이브리드 워크플로우를 시도하고 있습니다. 엔드 투 엔드 셀룰러와 방송 노하우를 결합한 공급업체는 조기 계약을 획득했으며 릴리스 18의 멀티캐스트 확장에 대한 특허 출원은 경쟁을 더욱 재구성할 수 있는 새로운 라이선스 모델을 제안합니다.

모바일 시청자가 4K, 360도, 증강현실의 전달을 요구하는 가운데, 사업자는 유니캐스트의 혼잡을 억제하기 위해 멀티캐스트에 축발을 옮깁니다. 독일 텔레콤과 에릭슨은 유로 2024 무선 카메라를 위한 25ms 이하의 대기 시간과 500Mbps의 업링크를 제공하여 전문적인 프로덕션 실행 가능성을 입증했습니다. 말레이시아는 네트워크 슬라이스된 5G 링크로 내셔널 데이 퍼레이드를 스트리밍하여 피크 부하 시에도 안정적인 품질을 확보했습니다. 방송국은 현재 카메라당 50Mbps의 업링크 지속성을 요구하고 있지만, 이 요구사항은 여러 시청자가 동일한 멀티캐스트 흐름을 공유하는 경우에만 충족됩니다. 버라이즌은 프라이빗 5G 방송 스위트 내에 AI 기반 시청자 밀도 인식을 추가해 실시간으로 비트레이트 미세 조정을 합니다.

NTT 도코모는 5G 독립형 대출로 하향 6.6Gbps의 데모를 실시해, 높은 비트레이트의 방송 수신에 대응한 단말임을 나타냈습니다. BMW는 2025년의 모든 모델에 5G 안테나를 탑재해 방송 컨텐츠의 스트리밍과 펌웨어 업데이트의 동시 푸시를 실현했습니다. 중국에서는 프리미엄 휴대폰이 700MHz를 지원하도록 의무화되어 FeMBMS 수신이 가능한 설치 기반이 확대되어 서비스 이용이 가속화되었습니다. 방송에 특화된 칩셋은 아직 적지만, 차재 인포테인먼트 공급업체가 최초로 통합해, 소비자에 의해 널리 보급하기 위한 교두보를 구축하고 있습니다.

멀티캐스트 컨트롤러 추가, 안테나 재튜닝, 고밀도 mmWave 스몰셀 배포로 데이터 통신 전용 5G에 비해 사이트당 비용이 50% 상승할 수 있습니다. 노키아는 사업자가 현금 절약을 위해 방송 모듈을 연기했기 때문에 2024년 장비 수주가 감소한다고 지적했습니다. 경기장에 필수적인 mmWave 방송은 Sub-6GHz보다 1.5-2배 더 많은 기지국이 필요하며 예산이 더욱 늘어납니다. 일부 통신 사업자는 피크 시 비디오 트래픽의 70%를 전송하는 셀의 10%에서만 방송을 가능하게 하는 단계적인 롤아웃을 채용하고 있지만, 이 전술은 전국적인 커버리지의 스케줄을 장기화시킵니다.

라이브 이벤트 스트리밍은 보증된 품질 수준이 요구되는 스포츠 및 문화적으로 대대적인 방송을 이용함으로써 2024년 수익의 28%를 유지했습니다. 그러나 커넥티드 차량은 자동차 OEM이 수백만 대의 자동차에 동시에 무선 업데이트를 푸시하기 때문에 2030년까지 12.12%의 연평균 복합 성장률(CAGR)을 기록할 전망입니다. BMW의 완전한 5G 탑재 모델 라인과 테슬라의 공장 내 사설망은 생산 분석과 자동차 인포테인먼트에서 방송의 이중 역할을 보여줍니다. LTE 및 5G 방송 시장은 원격 진단, V2X 안전 메시지, 사용자 개입 없이 지도 데이터 업데이트를 지원합니다.

두 번째 성장 레인은 공공 안전입니다. FirstNet 업그레이드는 무인 항공기 멀티캐스트 이미지와 실시간 바디 카메라 피드를 추가하여 응급 인력의 상황 인식을 향상시킵니다. 모바일 TV와 주문형 비디오는 선거 밤과 같은 플래시 클라우드 상황에서 백홀을 줄이기 위해 방송에 의존하며, 광고 네트워크는 전국적인 동영상 스트림에 로컬 오퍼를 삽입하는 위치 기반 멀티캐스트 스팟을 테스트하고 있습니다. 이와 같이 이용 사례가 다양화됨으로써 애플리케이션 레이어의 다양성이 확보되고 단일 부문 불황에 대한 탄력성이 유지됩니다.

LTE eMBMS는 2024년 LTE 및 5G 브로드캐스트 시장 점유율의 61%를 차지했으며, 사업자가 기존 5G 코어에 릴리스 18 소프트웨어를 오버레이함으로써 5G FeMBMS는 매년 14.23% 성장하고 있습니다. 중국 모바일의 100개 도시에서의 시작은 FeMBMS의 확장성을 입증하고 2025년까지 커버리지를 3배로 늘리는 계획은 적극적인 일정을 보여줍니다. 운영자는 시청자 임계값이 충족될 때 FeMBMS 유니캐스트와 멀티캐스트 간의 원활한 전환을 평가하여 모든 메가헤르츠를 최적화합니다.

ATSC 3.0 하이브리드 방송은 지상파 미디어 회사에 모바일 전달에 대한 진입점을 제공합니다. 브라질은 2026년 월드컵까지 ATSC 3.0을 전국에 보급한다는 로드맵을 보여주며 미국에서는 FCC에 의한 시험이 진행 중이며 휴대전화와 지상파의 융합 규격이 실증되고 있습니다. 릴리스 18의 AI 스케줄러는 셀 에지의 패킷 손실을 줄이고 이동성을 향상시킵니다. 디바이스 생태계가 성숙함에 따라 향후 10년 동안 LTE eMBMS 마이그레이션 시나리오는 공존에서 선셋 계획으로 마이그레이션할 것으로 보입니다.

LTE 및 5G 방송 시장 보고서는 용도별(공공 안전, 커넥티드카, 광고 등), 방송 기술별(LTE EMBMS, 5G FeMBMS, 기타), 주파수 대역별(서브 6GHz(6GHz 미만), L-band별(1-2GHz), 기타), 최종 사용자별(모바일 네트워크 사업자, 자동차 OEM 등), 지역별로 분류되고 있습니다.

아시아태평양은 2024년 매출의 38%를 차지했으며, CAGR 14.43%로 성장이 전망됩니다. 중국, 일본, 한국의 정부 지원에 의한 5G-Advanced 전개에서는 첫날부터 멀티캐스트가 포함됩니다. 중국 이동통신(China Mobile)은 100개 도시를 다루고, 2025년에는 300개 도시로 확장될 것으로 추정되며, 동일한 플랫폼에서 UHD 스트리밍, 산업용 IoT 및 대량 경고를 제공합니다. 일본 통신사업자는 2024년 기지국을 20% 증설해 미드밴드와 밀리미터파를 조합해 밀집한 대도시 방송을 실현했습니다. 한국은 공장용 민간 5G 보조금으로 소비자용을 보완해 제조업과 물류에서의 방송 도입을 가속화하고 있습니다.

북미는 방송 중심 5G 강화에 충당된 63억 달러를 포함한 FirstNet 당국의 80억 달러의 10년 계획에 힘입어 2위를 차지했습니다. 포드, GM, 테슬라와 같은 자동차 대기업은 사설 5G를 도입하여 공장 로봇을 동기화하고 밤새 자동차에 소프트웨어를 푸시하고 있습니다. 장치 생태계는 성숙하지만 장비 투자 규율은 전국적인 방송의 급속한 업그레이드를 억제합니다.

유럽에서는 규제의 조화가 진행됩니다. 유럽 방송 연합(European Broadcasting Union)의 5G와 위성의 하이브리드 시험 방송은 EU의 그린딜 에너지 목표를 준수하면서 농촌 지역의 커버리지 갭을 줄입니다. 독일은 자동차 방송 통합을 이끌고 있습니다. BMW의 5G 연결 계획은 조립 라인과 판매 후 업데이트를 모두 다룹니다. 중동, 아프리카, 남미 등 소규모 지역은 5G 전체 일정을 반영합니다. 주파수 경매가 조기에 종료된 지역에서는 소규모이지만 18개월 이내에 방송 시험이 시작됩니다.

The LTE and 5G broadcast market size is USD 1.04 billion in 2025 and is forecast to reach USD 1.78 billion by 2030, advancing at an 11.24% CAGR.

Rising demand for spectrum-efficient video delivery, emergency-alert modernization, and rapid device proliferation are expanding commercial trials into nationwide rollouts. Operators are migrating from legacy LTE eMBMS toward 5G FeMBMS to gain multicast flexibility and AI-driven resource allocation, while broadcasters experiment with hybrid ATSC 3.0-5G workflows. Vendors that combine end-to-end cellular and broadcast know-how secure early contracts, and patent filings around Release 18 multicast enhancements hint at new licensing models that could further reshape competition.

Operators pivot to multicast to curb unicast congestion as mobile viewers demand 4K, 360-degree, and augmented-reality feeds. Deutsche Telekom and Ericsson delivered sub-25 ms latency and 500 Mbps uplinks for Euro 2024 wireless cameras, proving viability for professional production. Malaysia streamed its National Day parade over a network-sliced 5G link, ensuring stable quality even at peak load. Broadcasters now request 50 Mbps sustained uplink per camera, a requirement met only when several viewers share the same multicast flow. Verizon has added AI-based audience-density recognition inside its private 5G broadcast suite to fine-tune bitrate in real time.

NTT Docomo demonstrated 6.6 Gbps downlink on 5G Stand-Alone, signaling handset readiness for high-bitrate broadcast reception. BMW equips all 2025 models with 5G antennas to stream broadcast content and push simultaneous firmware updates. China's mandate that premium phones support 700 MHz expanded the installed base capable of FeMBMS reception, accelerating service availability. While broadcast-specific chipsets remain scarce, automotive infotainment suppliers are integrating them first, creating a beachhead for wider consumer adoption.

Adding multicast controllers, re-tuning antennas, and deploying dense mmWave small cells can raise per-site cost by 50% versus data-only 5G. Nokia noted weaker equipment orders in 2024 as operators deferred broadcast modules to preserve cash. mmWave broadcast, essential for stadiums, needs 1.5-2X more base stations than Sub-6 GHz, further stretching budgets. Some carriers adopt phased rollouts, enabling broadcast only on 10% of cells that carry 70% of peak video traffic, yet this tactic elongates nationwide coverage timelines.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Live Event Streaming retained 28% of 2024 revenue by exploiting marquee sports and cultural broadcasts that demand guaranteed quality levels. Still, Connected Vehicles will post a 12.12% CAGR through 2030 as automotive OEMs push over-the-air updates to millions of cars simultaneously, a task unicast networks struggle to scale. BMW's fully 5G-equipped model line and Tesla's factory private networks show broadcast's dual role in production analytics and in-vehicle infotainment. The LTE and 5G broadcast market underpins remote diagnostics, V2X safety messages, and map data refresh without user intervention.

A second growth lane appears in public safety. FirstNet's upgrade adds multicast drone imagery and real-time body-camera feeds that improve situational awareness for first responders. Mobile TV and video on demand rely on broadcast to reduce backhaul in flash-crowd situations like election nights, while advertising networks test location-based multicast spots that insert local offers into a national video stream. These varied use cases cement application-layer diversity and maintain resilience against single-segment downturns.

LTE eMBMS still commands 61% of the LTE and 5G broadcast market share in 2024 on the strength of earlier deployments, yet 5G FeMBMS grows 14.23% annually as operators overlay Release 18 software onto existing 5G cores. China Mobile's 100-city launch validated FeMBMS scalability, and plans to triple coverage by 2025 illustrate aggressive timelines. Operators appreciate FeMBMS's seamless switch between unicast and multicast when audience thresholds are met, thereby optimizing every megahertz.

ATSC 3.0 hybrid broadcast gives terrestrial media companies an entry point to mobile distribution. Brazil's roadmap to nationwide ATSC 3.0 by the 2026 World Cup and ongoing FCC trials in the United States demonstrate convergent cellular-terrestrial standards. Release 18's AI schedulers cut cell-edge packet loss and boost mobility, benefits that accrue across both LTE and 5G implementations. As device ecosystems mature, the transition narrative will shift from coexistence to sunset planning for LTE eMBMS in the next decade.

The LTE and 5G Broadcast Market Report is Segmented by Application (Public Safety, Connected Vehicles, Advertising, and More), Broadcast Technology (LTE EMBMS, 5G FeMBMS, and More), Frequency Band (Sub-6 GHz (less Than 6 GHz), L-Band (1-2 GHz), and More), End User (Mobile Network Operators, Automotive OEMs, and More), and Geography.

Asia Pacific commands 38% of 2024 revenue and grows at 14.43% CAGR. Government-backed 5G-Advanced rollouts in China, Japan, and South Korea embed multicast from day one. China Mobile's coverage of 100 cities, expanding to 300 in 2025, serves UHD streaming, industrial IoT, and mass alerts on the same platform. Japanese operators added 20% more base stations in 2024, pairing mid-band with mmWave for broadcast in dense metros. South Korea complements consumer focus with private 5G grants for factories, accelerating broadcast adoption in manufacturing and logistics.

North America ranks second, propelled by the FirstNet Authority's USD 8 billion ten-year plan, including USD 6.3 billion earmarked for broadcast-centric 5G enhancements. Automotive majors-Ford, GM, Tesla-install private 5G to synchronize plant robots and push software to vehicles overnight. The device ecosystem is mature, yet CapEx discipline tempers rapid nationwide broadcast upgrades.

Europe advances on regulatory harmonization. The European Broadcasting Union's hybrid 5G/satellite pilot reduces rural coverage gaps while complying with EU Green Deal energy targets. Germany leads automotive broadcast integration; BMW's 5G connectivity plan covers both assembly lines and post-sale updates. Smaller regions-Middle East, Africa, South America-mirror overall 5G timelines; where spectrum auctions conclude early, broadcast trials begin within 18 months, albeit at modest scale.