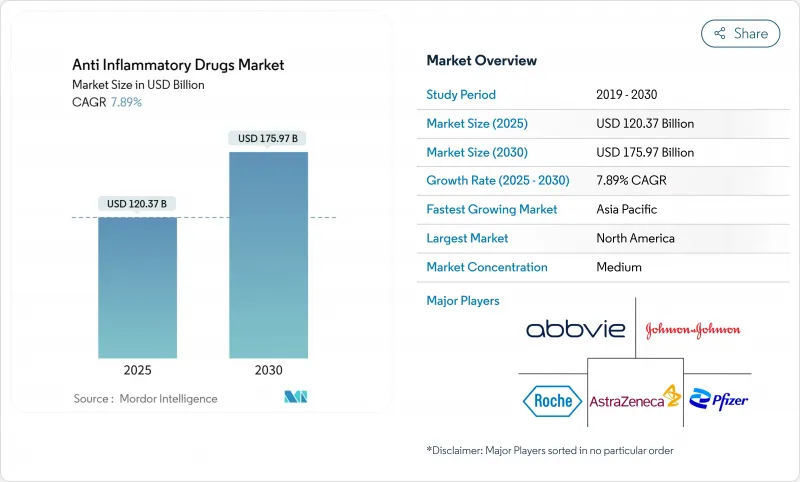

항염증약 시장은 2025년에 1,203억 7,000만 달러로 추정되고, 2030년에는 1,759억 7,000만 달러에 이를 전망이며, CAGR 7.89%로 성장할 것으로 예측됩니다.

성장은 세계 인구의 고령화, 만성 질환 이환율 증가, 인공지능이 가능하게 하는 생물학적 제제 발견의 속도 향상에 지지되고 있습니다. 또한, 비스테로이드성 항염증약(NSAIDs) 외용약의 매장 판매 확대, 안전성 표시 통일 후 JAK 억제제 채용 확대, 정밀의료에 대한 지속적인 투자도 수요를 지원하고 있습니다. 경쟁 구도는 계속 완만하며, 주요 제약 그룹이 파이프라인 다양화를 통해 점유율을 지키는 반면, 바이오시밀러 진출기업은 가격 차이를 줄이고 환자 접근을 확대하고 있습니다. COX-2 심혈관계의 안전성에 대한 우려가 뿌리깊고, 원약 공급망이 아시아에 의존하고 있기 때문에 기세는 약해지는 한편, 콜히친의 심혈관계 질환에 대한 적응 등 새로운 적응증에 의해 새로운 임상 및 수익 경로가 나타나고 있습니다. 따라서 항염증약 시장은 안정적인 기초 요법의 소비와 치료 가치를 높이는 기술 혁신의 물결의 균형을 맞추고 있습니다.

비만 및 장수 증가는 골관절염 환자 수를 증가시키고 항염증약 시장을 자극합니다. 기계적 부하와 낮은 수준의 전신 염증은 연골 손실을 가속화하고 안전한 진통제에 대한 지속적인 수요를 촉진합니다. 관찰 연구에 의하면, 디클로페낙 겔 외용제는 사용자의 74.2%가 부작용을 보고하지 않고 증상을 완화시키는 것으로 나타났으며, 이는 심혈관계를 합병하는 비만 환자에게 있어서 유의한 안전성의 이점입니다. 지불자는 체중에 중립적인 치료제와 대사성 염증 치료제를 지지하고 비스테로이드성 항염증약 외용제와 글루코사민 제제의 처방을 확대하고 있습니다. 약물 전달과 코르티코 스테로이드의 단일 주사는 더욱 복용 어드히어런스를 향상시킵니다. 이들을 종합하면 비만으로 인한 골관절염은 항염증약 시장에 장기적인 볼륨 앵커가 됩니다.

발전 알고리즘은 표적 식별을 단축하고, 결합 친화성을 최적화하며, 리드 후보의 위험을 줄임으로써 생물학적 제제의 조기 시행을 가능하게 합니다. 인실리코 메디신은 염증성 장 질환 치료제 ISM5411을 인실리코 컨셉에서 1단계까지 30개월 만에 진전시켰습니다. 선도적 제약 회사는 현재 내부 라이브러리와 AI 플랫폼을 결합하여 면역학 포트폴리오를 쇄신하고 차별화된 메커니즘으로 항염증약 시장을 강화하고 있습니다. 유전체학에서 파생된 동반자 진단은 환자 선택을 정교하게 하고 임상시험의 성공률 및 지불자의 수용을 강화합니다. 데이터, 모델링, 임상 검증의 선순환은 2030년까지 지속적인 생물제제 혁신을 약속합니다. 특히 미국, 독일, 영국 등 강력한 디지털 인프라가 있는 지역이 이 활동의 대부분을 담당하고 있지만 전략적 파트너십으로 중국과 싱가포르의 연구 허브에도 능력이 확대되고 있습니다.

PRECISION 시험에서 셀레콕시브는 나프록센과 이부프로펜에 대해 주요 심장 부작용에 대해 비열성으로 자리매김했지만, 처방자에 대한 주의는 여전히 계속되고 있습니다. FDA 자문위원회는 셀레콕시브의 경고를 검토했지만 삭제하지 않았고, 인지 장애물을 유지 관절염 재단 강직성 척추염에 대한 한국의 보험 데이터는 심부전의 조정 후 위험 비율이 1.12이며, 용량 의존적인 심혈관 위험이 나타났습니다. 따라서 임상의는 특히 노인 환자 및 위험이 높은 환자에서 COX-2 NSAID의 대량 투여와 장기 사용을 제한합니다. 이 억제요인에 의해 전신성 NSAIDs의 성장이 억제되어 외용 NSAIDs 및 생물학적 제제로 사용량이 이동하고, 항염증약 시장은 약간 감속하고 있습니다.

관절염 영역은 2024년에 27.84% 시장 점유율을 차지했는데, 이는 이 영역의 확립된 치료 프로토콜과 만성 관리를 필요로 하는 환자 수의 많음을 반영하고 있습니다. 그러나 조기 개입 및 표적화 항염증 접근을 중시하는 치료 패러다임의 진화에 견인되어 2030년까지 CAGR 8.34%로 성장할 전망이며, 건염이 가장 급성장하는 용도로 부상하고 있습니다. 최근의 전임상 연구는 국소 및 경구 NSAIDs가 힘줄 사용과 관련된 통증을 단기적으로 효과적으로 완화시키고, 특히 급성 견건염과 활액포염에 효과적인 것으로 입증되었습니다. 다발성 경화증 및 염증성 장 질환에의 적용은 새로운 표적 치료제가 치료 옵션을 넓히면서 강력한 성장을 이루고 있으며, COPD에 대한 적용은 장기적인 합병증을 감소시키는 스테로이드 온존 요법으로부터 이익을 얻고 있습니다.

특정 염증 경로를 표적으로 한 개입에 맞추는 정밀의료 접근법으로 애플리케이션의 전망이 재구성되고 있습니다. 힘줄과 뼈의 치유에 관한 연구는 염증 조절의 중요한 역할을 강조하고 있으며, 대식세포의 분극화와 사이토카인 조절에 초점을 맞추어 복구 과정을 최적화하는 새로운 치료법이 등장하고 있습니다. 천식 치료는 JAK 억제제가 여러 염증 캐스케이드에 걸쳐 효능을 보이고 다른 치료 범주에서는 급성 증상과 기초 질환 진행 모두를 다루는 병용 접근법이 유익한 등 큰 혁신을 보여줍니다. 특히, 여러 염증 경로가 병태에 관여하는 복잡한 병태에 있어서는 용도에 특화된 바이오마커와 동반진단약으로의 시프트가 보다 정확한 치료 선택을 가능하게 하고 있습니다.

항염증성 생물학적 제형은 표적 면역조절의 지속적인 기술 혁신 및 적응증의 확대를 반영하여 2024년에는 32.56%의 점유율로 시장의 리더를 유지했으며, 2030년까지 연평균 복합 성장률(CAGR) 8.43%로 성장을 견인할 전망입니다. 발전 플랫폼은 보다 정확한 표적 식별 및 분자 최적화를 가능하게 하여 개발 기간을 단축하고 성공률을 향상시킵니다. 비스테로이드성 항염증약는 여전히 급성기 치료에 필수적이지만, 한편 코르티코스테로이드는 동등한 효능과 부작용 프로파일의 감소를 제공하는 스테로이드 온존 대체물로부터의 압력에 직면하고 있습니다. 면역선택적 항염증약 유도체는 전신작용이 적고 보다 정확한 염증 조절을 약속하는 새로운 카테고리입니다.

최근의 약사 승인은 우파다시티닙이 거세포성 동맥염에서 8번째 적응을 얻고 위약의 29.0%에 비해 46.4%의 관해 지속률을 보이는 등 생물학적 제형 부문의 기세를 보여줍니다. 또, 머크의 PRA-023이 크론병 환자에 있어서 49.1%의 관해율을 달성하는 등, 염증성 장 질환에 있어서 뛰어난 효능을 나타내는 TL1A 억제제 등, 신규 작용기전의 약도 동 부문에 공헌하고 있습니다. 다른 약물 클래스별로는 병용 요법이나 서방형 제제의 개발이 진행되고 있어 투여 횟수나 전신 노출량을 줄이면서 환자의 컴플라이언스 및 치료 성적을 향상시키고 있습니다.

북미는 첨단 상환제도, 신규약제의 급속한 도입, 엄격한 임상연구 능력에 힘입어 2024년 세계 매출의 38.72%를 유지했습니다. 미국에서는 급성 통증에 대한 최초의 비오피오이드 NaV1.8 차단제인 JOURNAVX가 승인되어 치료의 리더십이 강화되었습니다. 아달리무맙 대체품을 포함한 바이오시밀러의 침투는 지급자의 비용 억제 목표에 부합하며 매출 증가는 약간 완만해졌습니다. 주요 원료의 재보유와 조달 대상의 다양화에 대한 연방 정부의 인센티브는 2024년 물류 중단 시 노출된 공급 취약성을 해결합니다. 캐나다에서는 실제 임상 증거 요건이 확대되고 시판 후 조사가 강화되고 처방의 정화가 촉진됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 최고 8.53%를 기록할 전망입니다. 중국의 집중조달로 인해 생물학적 제제의 가격이 저하되고 병원 도입이 가속화되는 한편 국내 업체들은 TNF 억제제 바이오시밀러의 규모를 확대하고 있습니다. 인도의 아유슈만 발라트 보험 제도는 환자의 보험 적용 범위를 확대하고 소매 OTC 수요를 밀어 올립니다. 일본은 계속해서 노화에 따른 염증성 질환의 지표가 되어 안정된 생물학적 제제의 이용을 지원합니다. 동남아시아 시장은 임상시험 인프라에 투자하고 다국적 스폰서를 유치하고 있습니다. 전반적으로 소득 증가, 도시화, 만성질환의 만연이 이 지역 항염증약 시장 확대에 박차를 가하고 있습니다.

유럽은 큰 점유율을 가지고 있지만, 바이오시밀러에 의한 가격 침식의 격화에 직면하고 있습니다. 독일의 얼리 액세스 패스웨이와 디지털 치료제 파일럿은 기술 혁신에 대한 헌신을 보여주는 것이지만, 의료 기술 평가에서는 확고한 비용 효율적인 증거가 요구됩니다. 영국의 의약품 및 헬스케어 제품 규제청(MHRA)은 브렉시트 후 유연한 대응으로 승인을 가속화하고 경쟁과 환자 접근의 균형을 맞추고 있습니다. 중동 및 아프리카에서는 단계적 포뮬러 시스템과 바이오시밀러 도입에 투자하여 치료 범위를 넓히고, 라틴아메리카에서는 규제 프레임워크을 근대화하며, 다국적 기업에 의한 생산의 현지화를 촉진하고 있습니다. 이러한 개발은 항염증약 시장의 세계적인 기세를 유지하는 동시에 지역적인 뉘앙스의 차이를 부각하고 있습니다.

The anti-inflammatory drugs market generated USD 120.37 billion in 2025 and is forecast to touch USD 175.97 billion by 2030, advancing at a 7.89% CAGR.

Growth is anchored in global population aging, higher chronic disease incidence, and faster biologics discovery enabled by artificial intelligence. Demand is further supported by broader over-the-counter access to topical non-steroidal anti-inflammatory drugs (NSAIDs), expanding adoption of JAK inhibitors after unified safety labeling, and continued investment in precision medicine. Competitive activity remains moderate, with large pharmaceutical groups defending share through pipeline diversification, while biosimilar entrants narrow price gaps and expand patient access. Persistent concerns over COX-2 cardiovascular safety and active-pharmaceutical-ingredient (API) supply chain exposure to Asia temper momentum, yet novel indications such as colchicine for cardiovascular disease reveal new clinical and revenue pathways. The anti-inflammatory drugs market therefore balances steady base-therapy consumption with waves of innovation that raise therapeutic value.

Growing obesity and longevity are jointly raising osteoarthritis caseloads, stimulating the anti-inflammatory drugs market. Mechanical strain and low-grade systemic inflammation accelerate cartilage loss, driving sustained demand for safe analgesia. Observational studies indicate topical diclofenac gel yields symptom relief with 74.2% of users reporting no adverse events, a meaningful safety edge for obese patients with cardiovascular comorbidity. Payers endorse weight-neutral therapeutics and integrated metabolic-inflammation regimens, expanding formularies for topical NSAIDs and glucosamine combinations. Device-coupled drug delivery and single-visit depot corticosteroid injections further heighten adherence. Collectively, obesity-driven osteoarthritis provides a long-run volume anchor for the anti-inflammatory drugs market.

Generative algorithms shorten target identification, optimize binding affinity and de-risk lead candidates, enabling faster biologic entry. Insilico Medicine progressed ISM5411 for inflammatory bowel disease from in-silico concept to Phase 1 inside 30 months. Big Pharma now pairs internal libraries with AI platforms to refresh immunology portfolios, enhancing the anti-inflammatory drugs market with differentiated mechanisms. Companion diagnostics derived from genomics refine patient selection, bolstering trial success rates and payer acceptance. The virtuous cycle of data, modeling and clinical validation promises sustained biologics innovation through 2030. Regions with strong digital infrastructure, notably the United States, Germany and the United Kingdom, capture much of this activity, but strategic partnerships extend capacity into China and Singapore research hubs.

Although the PRECISION trial positioned celecoxib as non-inferior to naproxen or ibuprofen for major adverse cardiac events, prescriber caution persists. FDA advisory committees considered but did not remove celecoxib warnings, sustaining perception hurdles Arthritis Foundation. Korean insurance data on ankylosing spondylitis indicated dose-dependent cardiovascular risk with adjusted hazard ratio of 1.12 for heart failure Annals of the Rheumatic Diseases. Clinicians therefore limit high-dose or long-term COX-2 NSAID use, especially in older or high-risk patients. The restraint caps systemic NSAID growth and shifts volume toward topical NSAIDs and biologics, marginally slowing the anti-inflammatory drugs market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Arthritis applications command 27.84% market share in 2024, reflecting the segment's established treatment protocols and large patient population requiring chronic management. However, tendonitis emerges as the fastest-growing application at 8.34% CAGR through 2030, driven by evolving treatment paradigms that emphasize early intervention and targeted anti-inflammatory approaches. Recent preclinical research demonstrates that both local and oral NSAIDs provide effective short-term relief for tendon overuse-related pain, with particular efficacy in acute shoulder tendonitis and bursitis. Multiple sclerosis and inflammatory bowel disease applications are experiencing robust growth as new targeted therapies expand treatment options, while COPD applications benefit from steroid-sparing regimens that reduce long-term complications.

The application landscape is being reshaped by precision medicine approaches that match specific inflammatory pathways to targeted interventions. Tendon-bone healing research emphasizes the critical role of inflammatory modulation, with emerging therapies focusing on macrophage polarization and cytokine regulation to optimize repair processes. Asthma applications are witnessing significant innovation with JAK inhibitors demonstrating efficacy across multiple inflammatory cascades, while other treatment categories benefit from combination approaches that address both acute symptoms and underlying disease progression. The shift toward application-specific biomarkers and companion diagnostics is enabling more precise treatment selection, particularly in complex conditions where multiple inflammatory pathways contribute to disease pathology.

Anti-inflammatory biologics maintain market leadership with 32.56% share in 2024 and drive growth at 8.43% CAGR through 2030, reflecting continued innovation in targeted immunomodulation and expanding indication approvals. The class benefits from AI-accelerated drug discovery, with generative platforms enabling more precise target identification and molecular optimization that reduces development timelines and improves success rates. Non-steroidal anti-inflammatory drugs remain essential for acute management, while corticosteroids face pressure from steroid-sparing alternatives that offer comparable efficacy with reduced adverse effect profiles. Immune-selective anti-inflammatory derivatives represent an emerging category that promises more precise inflammatory modulation with fewer systemic effects.

Recent regulatory approvals demonstrate the biologics segment's momentum, with upadacitinib receiving its eighth indication for giant cell arteritis and demonstrating 46.4% sustained remission rates compared to 29.0% for placebo. The segment is also benefiting from novel mechanisms of action, including TL1A inhibitors that are showing superior efficacy in inflammatory bowel disease, with Merck's PRA-023 achieving 49.1% remission rates in Crohn's disease patients. Other drug classes are evolving toward combination approaches and sustained-release formulations that improve patient compliance and therapeutic outcomes while reducing dosing frequency and systemic exposure.

The Anti-Inflammatory Drugs Market Report Segments the Industry Into by Application (Arthritis, Chronic Obstructive Pulmonary Disease, and More. ), Drug Class (Anti-Inflammatory Biologics, Nsaids, and More), Route of Administration (Oral, Parenteral, and More), Sales Channel (Prescription, Over the Counter), and Geography (North America, Europe, Asia-Pacific, and More. The Market Forecasts are Provided in Terms of Value (USD).

North America retained 38.72% of global revenue in 2024, underpinned by advanced reimbursement, rapid uptake of novel agents and rigorous clinical research capacity. The United States approved JOURNAVX, the first non-opioid NaV1.8 blocker for acute pain, reinforcing therapeutic leadership. Biosimilar penetration, including adalimumab alternatives, aligns with payer cost-containment goals, slightly moderating net sales growth. Federal incentives to reshore key APIs and diversify sourcing address supply vulnerabilities exposed during 2024 logistics disruptions. Canada expands real-world evidence requirements, enhancing post-marketing surveillance and driving formulary refinement.

Asia-Pacific records the highest 8.53% CAGR through 2030. China's centralized procurement lowers biologic prices and accelerates hospital uptake, while domestic manufacturers scale TNF inhibitor biosimilars. India's Ayushman Bharat insurance scheme enlarges patient coverage and boosts retail OTC demand. Japan remains a bellwether for aging-related inflammatory disease, supporting steady biologic utilization. Southeast Asian markets invest in clinical trial infrastructure, attracting multinational sponsors. Collectively, rising income, urbanization and chronic disease prevalence fuel anti-inflammatory drugs market expansion in the region.

Europe holds meaningful share but faces intensified price erosion from biosimilars. Germany's early access pathways and digital therapeutics pilots demonstrate commitment to innovation, yet health technology assessments demand robust cost-effectiveness evidence. The United Kingdom's Medicines and Healthcare products Regulatory Agency (MHRA) post-Brexit flexibility expedites approvals, balancing competition with patient access. The Middle East and Africa invest in tiered formulary systems and biosimilar adoption to widen therapy reach, while Latin America modernizes regulatory frameworks, encouraging multinationals to localize production. Those developments collectively sustain global momentum for the anti-inflammatory drugs market while highlighting regional nuances.