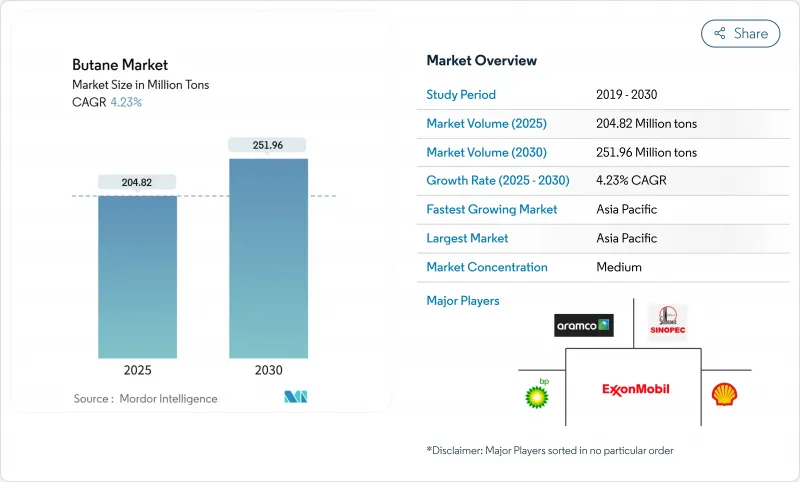

부탄 시장 규모는 2025년에 2억 482만 톤으로 평가되었고, 2030년에 2억 5,196만 톤에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR 4.23%로 성장할 전망입니다.

탄화수소는 주거용 LPG 및 석유화학 원료, 특히 에틸렌 및 프로필렌 체인의 핵심 컴포넌트 역할을 하며, 아시아태평양 지역 사업자들은 세계적 규모의 크래커를 추가하고 있습니다.

n-부탄은 겨울철 가솔린 혼합을 지원하며, 이소부탄은 고옥탄가 알킬레이트 스트림을 향상시킵니다. 북미 셰일 생산 증가는 천연가스 액체 회수율을 높여 가격 급등을 억제하고 지역적 공급 부족을 해소합니다(달라스 연방준비은행 지적). 저장 터미널의 디지털 트윈은 취급 손실을 줄이고 선적 창구를 최적화합니다. 이러한 요소들은 원유 연계 가격 변동성을 완화하고 생산, 물류, 다운스트림 전환 자산에 대한 투자를 촉진합니다.

분해 설비 증설로 구조적 부탄 수요가 촉진되며, 중국의 LPG 원료 수요는 2019년부터 2024년까지 일일 210만 배럴 증가했고 2030년까지 추가 증설이 예정되어 있습니다. 국제에너지기구(IEA)는 2025년 액체 수요 증가분의 절반 이상이 부탄과 같은 천연가스 액체(NGL) 원료에서 발생할 것으로 전망합니다. 신규 플랜트 증설로 마진이 축소되면서 운영사들은 장기 공급 계약 및 효율성 제고 방안을 모색하고 있습니다.

산업용 사용자들은 일정한 화염 온도와 낮은 그을음 발생으로 용접 품질과 절단 정밀도를 높이는 부탄 토치를 선호합니다. LPG 실린더를 사용하는 휴대용 히터는 전력 공급이 불안정한 추운 기후 지역 현장 작업을 지원합니다. 고소득 경제권에서는 전기화가 확산되고 있으나, 신흥 시장 건설사들은 여전히 비용 효율적인 LPG 솔루션을 선호합니다. 따라서 성장은 아시아의 신축 활동과 아프리카의 인프라 업그레이드 추이를 따릅니다. 채택 여부는 또한 라스트마일 물류를 단축하는 실린더 유통망에 달려 있어, 미드스트림 업체들에게 기회를 시사합니다.

부탄은 원유 및 천연가스 지수와 밀접하게 연동되어 사용자들이 급격한 가격 변동에 노출되어 조달 예산을 복잡하게 만듭니다. 원유 가격 하락은 NGL 가격 약세로 이어지지만, 갑작스러운 에탄 약세는 부탄과의 동조성을 강화해 헤지 복잡성을 증가시킵니다. 미국 생산자물가지수는 2025년 1월 210.934에서 2025년 4월 144.296으로 32% 하락하며 재고 계획에 불안을 초래했습니다. 가격 리스크는 자본이 부족한 지역의 신규 설비 확장을 저해하고, 지역별 스프레드를 차익 거래하는 유연한 물류 시스템으로 투자를 유도합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

n-부탄은 2024년 부탄 시장 규모의 56.19%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR)은 가장 빠른 4.94%로 성장할 전망입니다. 겨울용 휘발유는 리드 증기압 한계를 충족하기 위해 더 높은 정상 부탄 혼합 비율이 필요하여 정유사로부터 일관된 구매량을 확보합니다. 석유화학 기업들은 부타디엔과 라피네이트 생산 사이를 유연하게 전환하는 C4 추출 스트림을 목표로 하는 스팀 크래커에 정상 부탄을 통합합니다.

부탄 시장 보고서는 제품 유형(n-부탄 및 이소부탄), 최종 사용자 산업(주거/상업, 산업(화학 원료 포함), 엔진 연료, 정유소 및 기타 최종 사용자 산업), 원천(천연 가스 및 정제), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 업계를 세분화합니다. 시장 전망은 물량(톤) 기준으로 제공됩니다.

아시아태평양 지역은 2024년 부탄 시장 점유율 54.18%를 차지했으며 가장 빠른 5.28% 연평균 복합 성장률(CAGR)을 유지했습니다. 중국의 스팀 크래커 붐은 계속해서 미국산 NGL 화물을 끌어들이고 있으며, 이는 2024년 중국 LPG 수입량의 56%를 차지했습니다.

북미는 풍부한 셰일 유래 생산량으로 증가하는 수출 물량을 공급하는 핵심 공급처로 남아 있습니다. 미국은 2024년 약 50만 배럴/일의 부탄을 수출했으며, 이 중 41%는 아시아로, 36%는 아프리카로 운송되었습니다. 유럽은 균형 잡힌 양상을 보입니다 : 선제적인 기후 정책이 수요 성장을 억제하지만, 기존 석유화학 자산이 기본 수요를 안정적으로 유지합니다.

중동은 유리한 원료 공급을 활용해 석유화학 확장을 지속하는 반면, 아프리카와 남미는 콜롬비아와 나이지리아의 보조금 체계에 힘입어 실린더 보급률이 점진적으로 증가하고 있습니다.

The Butane Market size is estimated at 204.82 Million tons in 2025, and is expected to reach 251.96 Million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).Hydrocarbons serve as key components for residential LPG and petrochemical feedstocks, particularly in ethylene and propylene chains, with Asia-Pacific operators adding world-scale crackers.

Normal butane supports winter gasoline blending, while isobutane enhances high-octane alkylate streams. North American shale output boosts natural gas liquids recovery, curbing price spikes and addressing regional tightness, as noted by the Dallas Fed. Digital twins at storage terminals reduce handling losses and optimize ship-loading windows. These factors mitigate crude-linked pricing volatility and drive investments in production, logistics, and downstream conversion assets.

Expanding cracker capacity spurs structural butane uptake, with China's LPG feedstock pull rising 2.1 million b/d between 2019 and 2024 and more additions scheduled to 2030. The International Energy Agency projects that over half of the 2025 liquids-demand increase will come from NGL feedstocks such as butane. Downstream margins tighten as new plants dilute spreads, pushing operators toward long-term offtake contracts and efficiency measures.

Industrial users favour butane-fired torches for consistent flame temperatures and lower soot formation, enhancing weld quality and cutting precision. Portable heaters using LPG cylinders support site work in cold climates where the electric supply is unreliable. While electrification gains traction in high-income economies, emerging-market contractors still prefer cost-effective LPG solutions. Growth, therefore, tracks new-build activity in Asia and infrastructure upgrades in Africa. Adoption also hinges on cylinder distribution networks that shorten last-mile logistics, signalling opportunity for midstream players.

Butane's close linkage to crude and natural gas indices exposes users to rapid swings that complicate procurement budgets. Lower crude leads to softer NGL pricing, but sudden ethane weakness heightens co-movement with butane, increasing hedge complexity. The US producer-price index dropped from 210.934 in January 2025 to 144.296 in April 2025, a 32% slide that unsettled inventory planning. Price risk discourages greenfield capacity in capital-scarce zones and channels investment into flexible logistics that arbitrage regional spreads.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

n-Butane held 56.19% of the butane market size in 2024 and posts the fastest 4.94% CAGR to 2030. Winter-grade gasoline necessitates higher normal-butane blend ratios to meet Reid-vapor-pressure limits, securing consistent off-take from refiners. Petrochemical players integrate normal butane into steam crackers oriented toward C4 extraction streams that switch flexibly between butadiene and raffinate production.

The Butane Market Report Segments the Industry by Product Type (n-Butane and Iso-Butane), End-User Industry (Residential/Commercial, Industrial (Including Chemical Feed Stock), Engine Fuel, Refinery, and Other End-User Industries), by Source (Natural Gas and Refining), and by Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Ton).

Asia-Pacific commanded 54.18% butane market share in 2024 and sustained the fastest 5.28% CAGR. China's steam-cracker wave continues to pull US NGL cargoes, accounting for 56% of Chinese LPG imports in 2024.

North America remains the supply powerhouse, with ample shale-derived output feeding rising export volumes. The US shipped roughly 500 thousand b/d of butane in 2024, routing 41% to Asia and 36% to Africa. Europe presents a balanced picture: forward-looking climate policy checks demand growth, but legacy petrochemical assets keep baseline offtake steady.

The Middle East leverages advantaged feedstock to sustain petrochemical expansions, while Africa and South America see incremental cylinder penetration supported by subsidy frameworks in Colombia and Nigeria.