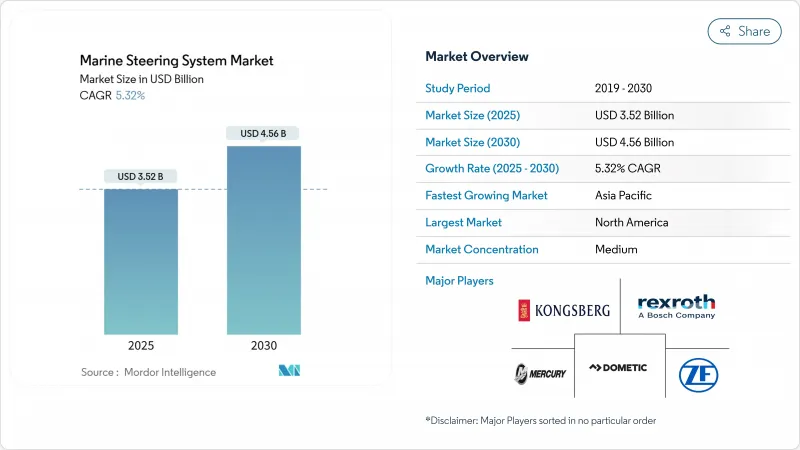

선박 조향 시스템 시장 규모는 2025년 35억 2,000만 달러로 평가되었고, 2030년에 CAGR 5.32%로 확대되어 45억 6,000만 달러에 이를 것으로 예측됩니다.

디지털 통합, 자율운항 준비형 제어 아키텍처, 강화되는 규제 감독이 이러한 성장 궤도를 유지하는 구조적 동력입니다. 레저용 소형 보트부터 해군 호위함에 이르기까지 선박들은 이제 전기 추진 및 동적 위치 유지 시스템과 원활하게 연동되는 사이버 보안이 적용된 소프트웨어 정의 조향 장비를 탑재하고 있습니다. 아시아의 가속화된 함대 교체, 북미의 꾸준한 개조 수요, 유럽의 탈탄소화 규정이 합쳐져 신조 및 애프터마켓 솔루션에 대한 광범위한 지역적 수요를 보장합니다. 전통적인 유압 전문업체들이 전자 기술에 능숙한 신규 진입업체들과 경쟁하며 국제해사기구(IMO)의 진화하는 조향장치 시험 프레임워크를 준수하는 통합 조향 장치, 액추에이터, 센서 패키지를 선보이면서 경쟁 강도가 높아지고 있습니다.

증가하는 국방 예산으로 중국, 한국, 일본, 독일, 네덜란드에서 다목적 호위함, 상륙함, 잠수함의 꾸준한 조달이 추진되고 있습니다. 각 함체는 통합 함교 및 전투 관리 시스템과 연동 가능한 사이버 보안이 강화되고 중복성이 풍부한 조향 시스템을 요구합니다. 2024년 중국 인민해방군 해군은 234척의 주요 수상 전투함을 운용하여 미 해군의 219척을 초과했으며, 이러한 함대 확장은 국내 조선소를 풀가동 상태로 유지하고 지역 공급망 전반의 조향 하청업체를 활용하고 있습니다. 유럽의 동시 진행 중인 NATO 프로그램은 음향 신호를 최소화하고 동적 위치 유지 기능을 수용하며 무인 윙맨(wingman) 항공기를 지원하는 전기식 또는 전기유압식 액추에이터에 대한 수요를 강화하고 있습니다.

2024년 미국 내 파워보트 및 개인용 수상 레저 장비 판매량은 23만-24만 대를 기록했습니다. 구매자들은 초보 소유주도 쉽게 조종할 수 있도록 조이스틱 계류, 무선 조향 장치, 통합 자동 조종 장치를 선호했습니다. OEM 업체들은 스마트 조향 시스템을 추진 시스템 업그레이드와 결합해 기존 선체에 대한 매력적인 애프터마켓 수요를 창출했습니다. 이 부문의 국내 경제적 영향력은 부품, 서비스 및 전자기기 매출을 유지하여 신규 보트 등록의 주기적 변동을 완화합니다.

컨테이너선 신규 건조 수주는 역사적으로 높은 수준을 유지하고 있으나, 탱커선, 벌크선 및 일반 화물선 계약은 2024년 내내 운영사들의 자본 지출 지연으로 인해 약화되었습니다. 아시아 조선소들은 이러한 수주 구성에 맞춰 생산량을 조정하며, 용량 변동을 상쇄하기 위한 개조 작업이 증가하는 가운데 표준 조향 장치에 대한 기본 수요는 감소하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

로터리 베인 설계는 신뢰성과 간단한 서비스 프로토콜을 바탕으로 2024년 선박 조향 시스템 시장 점유율의 42.67%를 유지했습니다. 그러나 조선소가 정밀 제어, 소음 감소 및 내장형 진단을 요구함에 따라 전기-기계 통합 유닛이 2030년까지 연평균 복합 성장률(CAGR) 9.24%로 성장을 주도할 전망입니다. 램 실린더는 극한 토크와 중복성이 필수인 중량물 수송 해군 및 해양 지원 선박에서 계속 사용됩니다. 랙 앤 피니언 어셈블리는 컴팩트한 설치 공간이 필요한 틈새 내륙 및 소형 선박 부문에 적용됩니다.

수요는 자체 보정 및 충돌 방지 알고리즘과 연동되는 소프트웨어 정의 액추에이터로 기울고 있습니다. 선급협회는 이제 사이버 보안 펌웨어를 인증하며, 운영사들이 기존 유압 시스템을 개조하기보다 차세대 전기 또는 하이브리드 제품으로 전환하도록 유도하고 있습니다. 이에 따라 선박 조향 시스템 시장은 선박 등급 전반에 걸쳐 적용 가능한 모듈식 전기-기계식 카트리지로 제품 로드맵이 수렴되는 모습을 보입니다.

유압 회로는 2024년 설치량의 52.38%를 차지했으나, 완전 전기식 파워 스티어링은 연간 16.43%의 가속도를 보이고 있습니다. 하이브리드 전기-유압 패키지는 전환을 연결하며, 명령 시에만 작동하는 온디맨드 펌프를 제공해 공회전 손실을 줄이고 엔진 정지 상태에서의 조종을 가능하게 합니다. 기계식 케이블 시스템은 저출력 선박에서 지속 사용되지만, 조이스틱 및 자동조종 기능이 대중화되면서 점진적인 교체를 맞이하고 있습니다.

전기 액추에이터는 1밀리초 미만의 지연 시간을 달성하며, 하이브리드 선박의 호텔 부하 요구를 완화하는 회생 제동을 통합합니다. 선박 등록국들이 기름-물 배출 한계를 강화함에 따라, 운영사들은 유체 없는 구조를 규정 준수 촉진제이자 수명 주기 비용 절감 수단으로 인식합니다. 이러한 성능과 지속가능성의 조합은 전기 기술을 선박 조향 시스템 시장에서 가장 혁신적인 트렌드로 자리매김하게 합니다.

북미는 2024년 선박 조향 시스템 시장의 46.34%를 차지했으며, 강력한 선택적 지출과 8,500만 명의 보트 이용자들이 파워보트 재고의 높은 회전율을 유지함에 따라 성장할 것으로 전망됩니다. 한편 미국 해안경비대의 사이버 보안 지침은 상업용 함대 전반에 걸쳐 암호화된 디지털 조향 장치의 채택을 가속화하고 있습니다. 캐나다 북극 순찰 프로그램은 빙해 등급 선체에 대한 정교한 조향 수요를 추가로 뒷받침합니다.

아시아태평양 지역은 2030년까지 연평균 8.52% 성장률로 시장을 주도할 전망입니다. 중국 해군 확장(현역 주요 전함 234척)은 조선소가 핵심 하위 시스템 자립을 목표로 함에 따라 국내 조선 생산을 촉진합니다. 일본, 한국, 싱가포르는 자율 표면 연구를 선도하며 AI 호환 조향 장치 수요를 창출합니다. 지역별 전기화 정책이 추진력을 더하며, 특히 무공해 의무화가 시행되는 연안 관광 및 섬 물류 선단에서 두드러집니다.

유럽은 NATO 프리깃함 프로그램과 엄격한 환경 법규에 힘입어 성장을 기록합니다. 유럽해상안전청(EMSA)의 STEERSAFE 권고사항은 키 각도, 부하, 반응 시간의 지속적인 모니터링을 의무화하여 운영사들이 센서 집약형 조향 장비를 요구하게 만듭니다. 노르웨이의 자율 여객 페리 시범 운항은 디지털 조향 솔루션의 실용성을 입증하며 유럽 전역의 지자체 확산을 촉진합니다. 동시에 EU 인공지능법은 조향 펌웨어 내 기계학습 기능에 대한 법적 명확성을 제공해 공급업체 투자를 촉진합니다.

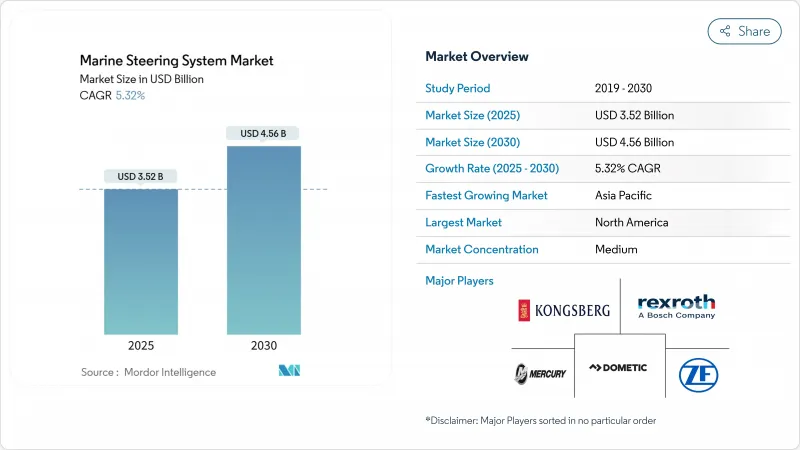

The marine steering systems market size reached USD 3.52 billion in 2025 and is forecast to expand at a 5.32% CAGR to USD 4.56 billion by 2030.

Digital integration, autonomous-ready control architectures, and tightening regulatory oversight are the structural forces sustaining this trajectory. Vessels ranging from recreational runabouts to naval frigates now embed cyber-secure, software-defined steering gear that links seamlessly with electric propulsion and dynamic-positioning suites. Accelerated fleet renewal in Asia, steady retrofit demand in North America, and Europe's decarbonization rules collectively ensure broad geographic pull for new-build as well as aftermarket solutions. Competitive intensity is rising as traditional hydraulic specialists race against electronics-savvy entrants to field integrated helm, actuator, and sensor packages compliant with the International Maritime Organization's evolving steering-gear testing framework.

Rising defense budgets propel steady procurement of multi-role frigates, amphibious carriers, and submarines across China, South Korea, Japan, Germany, and the Netherlands. Each hull specifies cyber-secure, redundancy-rich steering systems capable of mating with integrated bridge and combat-management suites. China's People's Liberation Army Navy operated 234 major surface combatants in 2024, outnumbering the 219 units fielded by the U.S. Navy, a fleet expansion that keeps domestic yards at full tilt and draws on steering subcontractors throughout regional supply chains. Parallel NATO programs in Europe reinforce demand for electric or electro-hydraulic actuators that minimize acoustic signatures, accommodate dynamic-positioning holds, and support unmanned wingman craft.

Powerboat and personal-watercraft sales recorded 230,000-240,000 units in the United States during 2024 as buyers sought joystick docking, wireless helm controls, and integrated autopilots that simplify skippering for novice owners. OEMs bundle smart steering with propulsion upgrades, creating a compelling aftermarket funnel for older hulls. The segment's domestic economic footprint sustains parts, service, and electronics revenues that cushion cyclical swings in new-boat registrations.

Container-ship new-build bookings remain historically elevated, yet tanker, bulk, and general-cargo contracts softened through 2024 as operators delayed capital expenditures. Asian yards adjust output to match this mix, reducing baseline demand for standard helm sets even as retrofit work rises to offset capacity fluctuations.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Rotary-vane designs retained 42.67% of the marine steering systems market share in 2024, anchored by reliability and simple service protocols. Yet electro-mechanical integrated units headline growth with a 9.24% CAGR through 2030 as shipyards specify precision control, noise reduction, and embedded diagnostics. Ram cylinders continue in heavy-lift naval and offshore support craft where extreme torque and redundancy are mandatory. Rack-and-pinion assemblies serve niche inland and small-craft segments needing compact footprints.

Demand tilts toward software-defined actuators that self-calibrate and interface with collision-avoidance algorithms. Classification societies now certify cyber-secure firmware, nudging operators toward new-generation electric or hybrid products rather than refurbishing legacy hydraulics. Consequently, the marine steering systems market sees product road-maps converge on modular electro-mechanical cartridges deployable across vessel classes.

Hydraulic circuits still delivered 52.38% of 2024 installations, yet fully electric power steering is accelerating at 16.43% annually. Hybrid electro-hydraulic packages bridge the transition, offering on-demand pumps that spin only when commanded, trimming idle losses, and enabling engine-off maneuvering. Mechanical cable systems persist in low-horsepower craft but face gradual replacement as joystick and autopilot features move down-market.

Electric actuators achieve sub-millisecond lag and integrate regenerative braking that eases hotel-load demands on hybrid vessels. As flag administrations tighten oil-to-water discharge limits, operators view fluid-free architectures as both compliance facilitators and lifecycle cost reducers. This performance-plus-sustainability mix cements electric technology as the marine steering systems market's most disruptive trend.

The Marine Steering System Market Report is Segmented by Product Type (Rotary Vane Type, Ram Type, and More), Actuation Technology (Conventional Hydraulic, Electro-Hydraulic, and More), Control Mode (Manual, and More), Vessel Type (Passenger and More), Propulsion Configuration (Inboard and More), Distribution Channel (OEM Fitment and Aftermarket Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 46.34% of the marine steering system market in 2024 and is forecast to grow on robust discretionary spending and 85 million boating participants maintain high turnover in powerboat inventories, while U.S. Coast Guard cybersecurity directives accelerate the adoption of encrypted digital helms across commercial fleets. Canadian Arctic patrol programs further support the sophisticated steering demand for ice-classified hulls.

Asia-Pacific leads growth with an 8.52% CAGR to 2030. Chinese naval expansion, underscored by 234 major warships in active service, fuels domestic shipbuilding production as yards aim for self-reliance in critical subsystems. Japan, South Korea, and Singapore pioneer autonomous surface research, seeding demand for AI-compatible helm actuators. Regional electrification policies add momentum, particularly in coastal tourism and island logistics fleets where zero-emission mandates emerge.

Europe records growth, anchored by NATO frigate programs and stringent environmental statutes. The European Maritime Safety Agency's STEERSAFE recommendations obligate continuous monitoring of rudder angle, load, and response times, leading operators to specify sensor-rich steering gear. Norway's operational autonomous passenger ferry pilot validates real-world readiness of digital helm solutions, encouraging wider municipal deployments across the continent. Concurrently, the EU AI Act provides legal clarity for machine-learning functions embedded in steering firmware, spurring vendor investments.