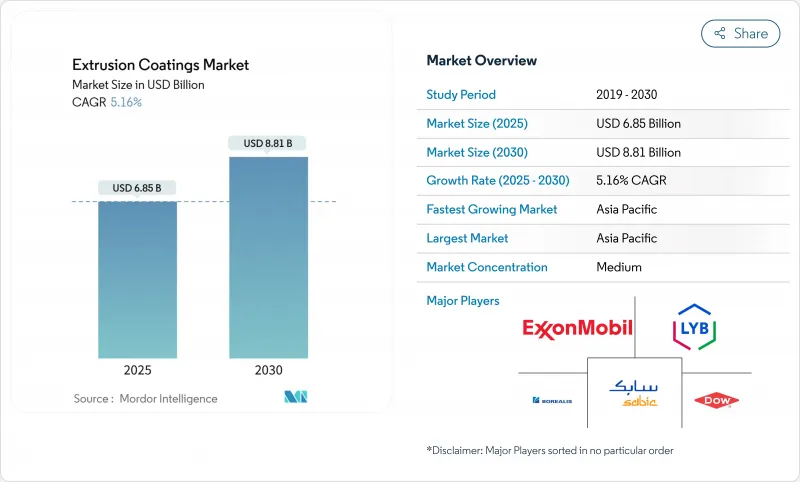

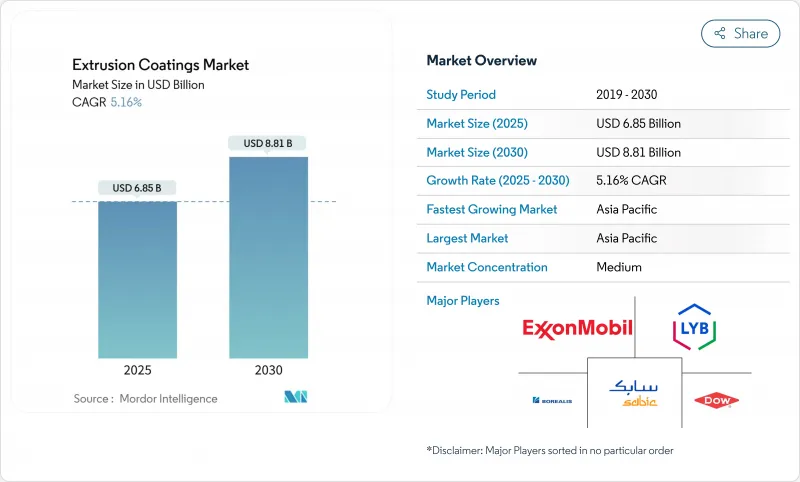

압출 코팅 시장은 2025년에 68억 5,000만 달러에 이르고, 2030년에는 88억 1,000만 달러에 달할 것으로 예상되며, 예측 기간의 CAGR은 5.16%를 나타낼 전망입니다.

액체 식품, 전자상거래용 메일러, 무균 의약품 팩 등 장벽 강화 폴리머의 급속한 보급이 현재 수요 기반을 지원하고 있습니다. 유럽연합(EU)의 포장·용기 포장 폐기물 규제부터 각국의 재활용 함량 의무화에 이르기까지, 규제의 추풍이 단일 소재 구조로의 변화를 가속시키고 있는 한편, 아시아태평양의 꾸준한 도시화에 의해 최종 시장의 수량이 확대되고 있습니다. 폴리올레핀 원료의 가격 변동과 이 분야의 탄소 발자국은 여전히 역풍이지만, 바이오 수지와 고급 기계적 재활용에 대한 지속적인 투자는 이러한 위험을 완화시키고 있습니다. 시장 리더는 수직 통합, 장기 공급 계약 및 재활용 가능한 코팅 구조를 상업적 규모로 검증하는 파일럿 라인을 통해 비용 압력에 대응하고 있습니다.

액체 식품 판지 및 경량 파우치는 2024년 압출 코팅 시장의 48.95%를 차지했지만, 이 점유율은 신흥 경제국에서 제한된 콜드체인 인프라와 브랜드 소유자의 보존 안정 형식에 대한 선호에 의해 강화됩니다. 2024년에 발매된 바이오매스 유래의 LDPE와 EVA의 신그레이드는 기존 배리어 성능에 필적하면서, 화석 원료를 20% 삭감했습니다. 포장 컨버터는 이러한 수지를 활용하여 히트 씰의 무결성을 희생하지 않고 라미네이트의 두께를 얇게 하여 물류 중량을 줄입니다. 식물 유래 대체 유제품이 선반에 늘어서고 아시아와 라틴아메리카에서 수량이 꾸준히 증가할 전망입니다.

완성 센터는 자동 성형, 고속 밀봉 및 라스트 마일 처리를 견딜 수 있는 코팅층이 필요합니다. 메탈로센 촉매를 사용한 PE는 이러한 워크플로우에 필요한 투명성, 미끄럼성, 내관통성을 제공하기 때문에 브랜드 소유자는 ASTM의 출하 낙하 시험을 충족하면서 30-50%의 재활용률을 가진 필름을 지정하게 되었습니다. 이 분야에서는 세계적인 수량 데이터가 부족하지만, 컨버터의 수주 대장에서는 2023년 이후 2자리 성장을 나타내고 있으며, 전자상거래가 압출 코팅 시장 진출기업에 있어서 회복력 있는 수요의 기둥임을 뒷받침하고 있습니다.

중국의 폴리올레핀 평균 계약 가격은 2024년 1분기부터 4분기까지 120달러/톤 이상 변동하여 컨버터 마진을 압박하고 스팟 구매로 조달 이동을 일으켰습니다. 종합 제조업체는 에틸렌의 내부 공급에 의해 변동을 완화하고 있지만, 중소의 코팅업자는 운전자금의 부담에 직면해, 신규 라인 투자가 지연될 수도 있습니다. 선물계약과 전략적 비축이 부분적인 완화책으로 되어 있는 것, 원재료의 불확실성이 압출 코팅 시장의 당면의 발판이 되고 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

폴리에틸렌은 2024년에 압출 코팅 시장 점유율의 42.65%를 차지했으며, 계속 대용량의 액체 및 연포장을 지지하고 있습니다. 메탈로센 촉매의 진보는 강인성과 광학 특성을 향상시키는 반면, 화학 재활용에 대한 노력은 규모가 큰 순환 원료를 약속합니다. 한 상업 라인은 이미 연산 3만 톤을 공급하고 있으며 2026년까지 연산 50만 톤을 목표로 하고 있습니다. CAGR 5.78%를 나타내는 에틸 아세테이트는 우수한 접착성과 저온 유연성으로 의료용 및 특수 식품의 틈새를 확보하고 있습니다. EVA를 LDPE와 혼합하면 기계적 재활용 흐름에 맞는 단일 소재 라미네이트 아키텍처도 가능합니다. 폴리프로필렌, PET, 특수 아크릴레이트는 내구성, 고배리어성, 고열 슬롯을 채우지만, 2차적인 체적 기여에 머무릅니다. 끊임없는 수지 혁신은 서큘러 이코노미(순환형 경제)가 의무화된 현재에도 압출 코팅 시장이 다양한 폴리머의 구색을 유지하고 있는 이유를 명확하게 보여줍니다.

두 번째 성장 파도는 씰 시작 온도를 낮추고 에너지 사용량을 줄이고 생물학적 제형의 글리콜 기반 멸균 사이클에 해당하는 엔지니어링 블렌드에서 두드러집니다. 이러한 기능 강화는 컨버터의 전환 비용을 끌어올려 폴리에틸렌의 압출 코팅 업계에서 주력 수지로서의 역할을 확고하게 하고 있습니다. 이와는 대조적으로, EVA 생산량이 증가함에 따라 일관된 VA 함량과 식품 접촉 규정 준수를 보장하려는 아시아태평양공급업체 간에는 후방 통합의 움직임이 활발해지고 있습니다.

판지와 골판지는 2024년 압출 코팅 시장 규모의 52.58%를 차지했으며, 이는 무균 카톤과 테이크아웃 푸드서비스에서의 역할이 정착되어 있음을 반영했습니다. 2025년에 출시된 특수 바이오폴리머 첨가제는 내그리스성을 유지하면서 최대 50%의 다운가우징을 가능하게 하고 브랜드 소유자가 섬유 재활용의 목표에 부합하는 것을 지원했습니다. CAGR 6.50%를 나타내는 폴리머 필름은 고속 라인, 다운 게이지된 두께, 대조 수축이나 메일러 필름에서의 용도 확대로부터 혜택을 받습니다. 캐스트 PP 필름은 BO-PP 필름에 필적하는 투명성과 제봉 효율을 가지면서, 비용이 최대 15% 낮기 때문에 드라이 푸드나 퍼스널케어 랩에의 침투가 가속하고 있습니다. 금속박은 재활용 과제에도 불구하고 수분이 중요시되는 의약용 팩에 필수적인 존재로 남아 있습니다. 특수 섬유와 부직포는 내화학성이 있는 산업용 슬롯을 채우고 있지만 채택은 비용과 공정의 복잡성에 의해 억제됩니다.

원래 필름용으로 개발된 무용제 프라이머가 판지용으로 재조합되어 컨버터에 기재 플랫폼 공통의 툴킷을 제공합니다. 이 수렴은 압출 코팅 시장이 장벽 성능, 재활용성 및 비용 규율의 균형을 동시에 취해야 하는 시대에 기판의 민첩성이 가져오는 전략적 가치를 강조합니다.

아시아태평양은 2024년 압출 코팅 시장 규모의 57.19%를 차지했으며 대규모 수지 확대와 가처분소득 증가를 배경으로 2030년까지 연평균 복합 성장률(CAGR) 6.25%를 나타낼 전망입니다. 중국의 지속적인 폴리머 자급 자족 전략과 인도의 870억 달러에 이르는 석유화학 사업이 풍부한 원재료를 공급하는 한편, 급속한 도시화에 의해 포장 식품이나 전자상거래의 보급이 가속화되고 있습니다. 2024년에 착공한 SABIC의 복건성의 합작 에틸렌 유닛은 2027년까지 수지의 현지 공급을 강화할 것으로 예상됩니다.

북미는 첨단 재활용 시험과 FDA의 엄격한 포장 기준을 활용하여 기술 측면에서 리더십을 유지합니다. 다우는 2024년 후반에 비중핵 사업인 접착제 자산을 매각하고 미래 수요를 전망한 서큘러 폴리머의 스케일 업을 위한 자금을 확보했습니다. 유럽은 재활용 및 탄소 목표를 통해 정책적 영향력을 유지하고 신속한 재제조를 촉구하지만 적합 배리어 솔루션의 프리미엄 가격도 인출합니다. 악조노벨의 360만 달러의 압출 코팅 라인 등 멕시코에서의 생산 능력 증강은 지역의 컨버터에 대응하기 위한 북미의 재조합을 나타내는 것입니다.

남미, 중동, 아프리카는 저수준에서 확대하면서도 견조한 성장을 보였습니다. 사우디아라비아에서는 1조 5,000억 달러의 인프라 파이프라인이 내식성 랩 수요를 끌어올려 GCC의 페인트 및 코팅 부문은 2027년까지 45억 달러에 달할 것으로 예측되고 있습니다. 이 지역은 포화 상태에 있는 서양 시장 이외의 다각화를 목표로 하는 중견기업에 전략적 그린필드 기회를 제공합니다.

The extrusion coatings market stands at USD 6.85 billion in 2025 and is projected to reach USD 8.81 billion by 2030, registering a 5.16% CAGR over the forecast period.

Rapid uptake of barrier-enhanced polymers in liquid food formats, e-commerce mailers, and sterile pharmaceutical packs anchors the current demand base. Regulatory tailwinds-from the European Union's Packaging and Packaging Waste Regulation to national recycled-content mandates-are accelerating shifts toward mono-material structures, while steady urbanization in Asia-Pacific expands end-market volumes. Volatility in polyolefin feedstock pricing and the sector's carbon footprint remain headwinds, yet sustained investments in bio-based resins and advanced mechanical recycling temper these risks. Market leaders are countering cost pressure through vertical integration, long-term supply contracts, and pilot lines that validate recyclable coating architectures at commercial scale.

Liquid food cartons and lightweight pouches capture 48.95% of the extrusion coatings market in 2024, a share reinforced by limited cold-chain infrastructure in emerging economies and brand owner preference for shelf-stable formats. New biomass-derived LDPE and EVA grades launched in 2024 match incumbent barrier performance yet cut fossil feedstock by 20%. Packaging converters are leveraging these resins to downgauge laminate thickness and reduce logistics weight without sacrificing heat-seal integrity. Combined with plant-based dairy alternatives gaining shelf space, the outlook affirms steady volume gains across Asia and Latin America.

Fulfilment centers require coating layers that withstand automated forming, high-speed sealing and last-mile handling. Metallocene-catalyzed PE delivers the clarity, slip, and puncture resistance needed for this workflow, prompting brand owners to specify films with 30-50% recycled content that still meet ASTM shipping drop tests. Although the sector lacks definitive global volume data, converter order books reveal double-digit growth since 2023, confirming e-commerce as a resilient demand pillar for extrusion coatings market participants.

Average PE contract prices in China swung by more than USD 120/ton between Q1 and Q4 2024, compressing converter margins and triggering procurement shifts toward spot purchases. Integrated producers buffer volatility through internal ethylene supply, yet small and midsized coaters face working-capital stress, occasionally delaying new line investments. While futures contracts and strategic stockpiling offer partial relief, raw-material uncertainty remains a near-term drag on the extrusion coatings market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyethylene captured 42.65% of the extrusion coatings market share in 2024 and continues to anchor high-volume liquid and flexible packaging. Advancements in metallocene catalysis lift toughness and optics, while chemical-recycling initiatives promise circular feedstock at scale; one commercial line already delivers 30,000 t/y and targets 500,000 t/y by 2026. Ethyl vinyl acetate, expanding at 5.78% CAGR, secures medical and specialty food niches due to superior adhesion and low-temperature flexibility. Blending EVA with LDPE also enables mono-material laminate architectures that fit mechanical recycling streams. Polypropylene, PET, and specialty acrylates fill durability, high-barrier, or high-heat slots but remain secondary volume contributors. Continuous resin innovation underscores why the extrusion coatings market maintains a diversified polymer slate even as circular-economy mandates tighten.

A second wave of growth is evident in engineered blends that lower seal initiation temperature, cut energy use, and meet glycol-based sterilization cycles for biologics. These functional enhancements raise switching costs for converters, cementing polyethylene's role as the workhorse resin within the broader extrusion coatings industry. By contrast, EVA's rising volume encourages backward-integration moves among Asia-Pacific suppliers keen to ensure consistent VA content and food-contact compliance.

Paperboard and cardboard accounted for 52.58% of the extrusion coatings market size in 2024, reflecting their entrenched role in aseptic cartons and take-out foodservice. Specialty biopolymer additives launched in 2025 allow downgauging up to 50% while maintaining grease resistance, helping brand owners align with fibre-recycling goals. Polymer films, growing at 6.50% CAGR, benefit from high line speeds, downgauged thickness, and expanding applications in collation shrink and mailer films. Cast PP variants now match BO-PP clarity and bag-making efficiency yet cost up to 15% less, accelerating their penetration into dry food and personal-care wraps. Metal foils remain indispensable for moisture-critical pharma packs despite recyclability challenges. Specialty fabrics and non-wovens fill chemical-resistant industrial slots, but their adoption is tempered by cost and process complexity.

Technological cross-pollination is notable: solvent-less primer chemistries originally developed for film lines are being re-formulated for paperboard, giving converters a common toolkit across substrate platforms. This convergence emphasizes the strategic value substrate agility provides in an era where the extrusion coatings market must balance barrier performance, recyclability, and cost discipline simultaneously.

The Extrusion Coatings Market Report Segments the Industry by Material (Polyethylene, Ethyl Vinyl Acetate (EVA), and More), Substrate (Paperboard and Cardboard, Polymer Films, and More), Application (Liquid Packaging, Flexible Packaging, and More), End-User Industry (Food and Beverage, Healthcare and Pharma, and More) and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 57.19% of the extrusion coatings market size in 2024 and is poised to compound at 6.25% CAGR through 2030 on the back of large-scale resin expansion and rising disposable incomes. China's sustained polymer self-sufficiency strategy and India's USD 87 billion petrochemical build-out furnish abundant raw materials, while rapid urbanization intensifies packaged-food and e-commerce penetration. SABIC's joint venture ethylene unit in Fujian, breaking ground in 2024, reinforces localized resin supply circa 2027.

North America leverages advanced recycling pilots and stringent FDA packaging norms to sustain technology leadership. Dow's divestment of non-core adhesive assets in late 2024 frees capital for circular-polymer scale-ups aimed at future demand. Europe maintains policy influence via recycling and carbon targets that compel rapid reformulation but also unleash premium pricing for compliant barrier solutions. Capacity additions in Mexico-such as AkzoNobel's USD 3.6 million extrusion-coatings line-signal North American realignment to serve regional converters.

South America, the Middle East, and Africa expand from a lower base yet post robust gains. Saudi Arabia's USD 1.5 trillion infrastructure pipeline lifts demand for corrosion-resistant wraps, while the GCC paints and coatings sector is projected to reach USD 4.5 billion by 2027. These regions offer strategic greenfield opportunities for mid-tier players aiming to diversify beyond saturated Western markets.