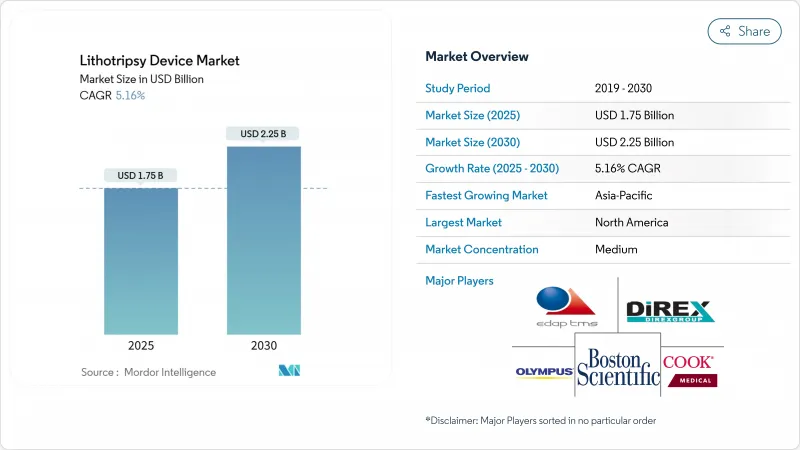

결석파쇄기 시장의 규모는 2025년에 17억 5,000만 달러로 추정되고, 예측기간(2025-2030년)의 CAGR은 5.16%를 나타낼 전망이며, 2030년에는 22억 5,000만 달러에 달할 것으로 예측됩니다.

이 가치 궤도는 기존의 체외 충격파 시스템에서 워크플로우를 단순화하고 결석 제거율을 높이는 정밀 유도 저침습 플랫폼으로 업계가 전환하고 있음을 보여줍니다. 고급 이미지 통합, 툴륨 파이버 및 기타 차세대 레이저의 상업적 개발, 무마취 치료를 가능하게 하는 초음파 기반 기술의 확대로 성장이 강화되고 있습니다. 휴대용 솔루션은 포인트 오브 케어 능력을 확대하는 반면, 대규모 경제권에서 유리한 진료 보수 개정으로 입원 환자의 수술실에서 외래수술센터(ASC)로 진료량의 변화가 지속되고 있습니다. 아시아태평양의 인프라 정비는 규제의 근대화와 함께 결석파쇄기 시장에서 새로운 수요를 창출하고, 지리적 수익의 흐름을 다양화하고 있습니다.

식생활의 변화, 앉기 쉬운 생활 습관, 요로의 미네랄 결정화를 촉진하는 탈수 패턴에 의해 결석증의 유병률은 모든 주요 지역에서 상승하고 있습니다. 충격파 결석파쇄술은 대상 환자의 50-75%의 성공률을 나타내고 있지만, 한계로 인해 보다 단단한 결석이나 보다 폭넓은 환자상에 대응할 수 있는 여지가 있습니다. 임상시험에서는 파열파 초음파에 의한 결석의 파쇄율은 88%, 무결석률은 약 49%로 보고되어, 종래의 시스템보다 효율성이 향상하고 있는 것을 나타내고 있습니다. 결과적으로 시장 수요는 적은 세션에서 더 높은 클리어런스를 보장하는 솔루션을 선호하고 결석파쇄기 시장의 꾸준한 양적 성장을 강화하고 있습니다.

툴륨 파이버 레이저, 볼텍스 빔 초음파, 최적화된 에너지 공급 알고리즘은 장비 사양과 임상 프로토콜을 대체하고 있습니다. 올림푸스의 SOLTIVE 플랫폼은 포르뮴 YAG 레이저와 비교하여 치료 시간을 20% 단축하고 단편화 효율을 33% 향상시킵니다. 보스턴 사이언티픽의 MOSES 2.0은 후퇴를 50% 감소시키고 90%의 당일 퇴원을 가능하게 하여 외래 워크플로우에 매력적입니다. Lithovortex와 같은 학술적인 프로토타입은 보다 폭넓은 환자층에 비침습적인 단편화를 보장하는 저가의 초음파 디자인을 제공합니다. 이러한 진보는 의료 제공업체가 마취 사용을 줄이면서 치료 결과를 향상시키는 데 도움을 주며, 결석파쇄기 시장 전체의 고가 시스템 수요에 박차를 가하고 있습니다.

충격파 치료로 인한 결석 가로 형성 및 기타 부작용은 임상 우려 사항으로 남아 있습니다. 특히 저극신 결석에서는 연성 요관경에 의한 결석 제거율이 90.2%인 반면 ESWL에서는 61.5%로 예상됩니다. 제조업체가 ESWL 부문에서 철수하고 임상의가 내시경 치료로 이동하는 것은 선택성이 높아지고 있음을 나타냅니다. 버스트 파의 개선에 의해 체외식 치료가 활성화될 가능성은 있지만, 안전성에 대한 인식은 결석파쇄기 시장에서 ESWL에 대한 지출을 계속 제한하고 있습니다.

체외 충격파 장치는 2024년에 결석파쇄기 시장 점유율의 53.16%를 차지했지만, 체내 플랫폼은 2030년까지 연평균 복합 성장률(CAGR) 5.89%로 상승할 것으로 예측됩니다. 레이저 기반 시스템 가운데 특히 툴륨 파이버 모델은 이전 레이저의 절반 출력에서 두 배의 속도로 결석을 파쇄합니다. 전자식 ESWL 장치는 기술의 친숙성으로 인해 대량 생산 센터에서의 지지를 유지하는 반면, 압전식 장치는 정확한 에너지 표적이 필수적인 특수한 틈새를 개척하고 있습니다.

체외식 ESWL의 동향은 정확성과 최소한의 조직 침습을 목표로 하는 외과적 경향과도 일치합니다. 최적화된 설정 하에서 92%의 분쇄율을 보여주는 실험 결과로 인해 이러한 도구의 임상적 수용을 넓히고 있습니다. 흡입 기능이 있는 초음파 결석파쇄기는 경피적 워크플로우를 향상시키고 기계적 충격을 필요로 하는 경우에는 공압식 장치가 사용되고 있습니다. 이러한 역학을 종합하면, 결석파쇄기 시장의 체강내 부분이 활성화되는 한편, 벤더는 종래의 체외 유닛 이외의 포트폴리오를 다양화하는 추세에 있습니다.

2024년의 결석파쇄기 시장 규모의 65.42%는 독립형 스위트가 차지하였고, 화상 진단이 통합된 복잡한 사례에 대응하는 설비가 완비된 병원 유닛이 중심이 되었습니다. 그러나 휴대용 및 탁상형 디자인은 CAGR 6.25%로 모달리티 경쟁을 선도하고 있습니다. Break Wave 초음파는 휴대성과 무마취 성능을 제공하여 응급실과 지방 클리닉에 대한 접근을 확대할 수 있는 방법을 제시합니다. Lithovortex 프로토타입은 볼텍스 빔 기능을 예산에 제한이 있는 환경에 적합한 합리적인 패키지로 제공하여 이러한 시프트를 증폭시킵니다.

운영의 유연성은 매우 중요합니다. 휴대용 시스템은 방 회전율을 줄여 여러 부서에서의 사용에 적합하며 시설 오버헤드를 낮추므로 강력한 처리량을 목표로 하는 ASC 관리자에게 인기가 있습니다. 따라서 공급업체는 운송에 충분히 컴팩트하면서도 투시 검사와 통합할 수 있을 만큼 견고한 하이브리드 구성을 설계하여 결석파쇄기 시장에서 여러 의료 환경에서 지속적인 관련성을 확보하고 있습니다.

북미는 2024년에 결석파쇄기 시장 점유율의 32.56%를 차지하며 투명성이 높은 환급 경로와 ASC의 치밀한 네트워크에 의해 뒷받침되고 있습니다. 병원은 장비의 갱신주기를 정당화하기 위해 Medicare 코딩의 안정성을 활용하고, 공급업체는 조기 도입을 요구하는 의사의 지원을 받고 있습니다. 이 지역의 견고한 애프터서비스 네트워크는 장비의 가동률을 더욱 높이고 교체 수요를 지원합니다.

유럽 시장은 성숙하면서도 꾸준히 현대화하는 의료 제도로 인해 뒤를 잇고 있습니다. 국가의 의료기금이 저침습치료를 장려해, 신형 레이저나 휴대용 초음파의 채용을 가속시키고 있습니다. 국경을 넘어서는 구매 프레임워크는 종합적인 교육과 유지보수를 제공하는 공급업체에게 유리한 다자간 입찰을 지원하고 범지역적 제품의 발자취를 강화하는 요인이 되고 있습니다.

아시아태평양은 인프라 확대, 규제 개혁, 1인당 소득 증가로 CAGR 7.53%의 성장이 예상됩니다. 일본의 400억 달러에 상당하는 의료기기 부문은 수술실 생산성을 극대화하는 IoT 대응 기기에 많은 투자를 하고 있습니다. 중국의 채무 구제 전략은 병원의 CAPEX 예산을 지원하고 인도의 행동 규범은 시장의 투명성을 촉진하고 있습니다. 중동 및 아프리카와 남미는 절대적인 금액으로는 뒤쳐져 있으나 새로운 민간병원이나 공공 부문의 프로젝트가 수술실을 정비함에 따라 성장이 가속하고 있어, 결석파쇄기 시장의 세계적인 저변을 확대하고 있습니다.

The lithotripsy device market size is estimated at USD 1.75 billion in 2025, and is expected to reach USD 2.25 billion by 2030, at a CAGR of 5.16% during the forecast period (2025-2030).

The value trajectory signals an industry pivot from traditional extracorporeal shock-wave systems toward precision-guided, minimally invasive platforms that simplify workflows and raise stone-clearance rates. Growth is reinforced by advanced imaging integration, the commercial rollout of thulium-fiber and other next-generation lasers, and expanding ultrasound-based technologies that permit anesthesia-free treatment. Portable solutions are broadening point-of-care capacity, while favorable reimbursement revisions in large economies continue to shift volumes from inpatient suites to ambulatory surgical centers. Asia Pacific's infrastructure build-out, combined with regulatory modernization, is unlocking new demand pockets and diversifying geographic revenue streams within the lithotripsy device market.

Stone disease prevalence is climbing across every major region due to diet shifts, sedentary habits, and dehydration patterns that potentiate mineral crystallization in urinary tracts. Shock-wave lithotripsy still posts 50-75% success among eligible patients, yet its limitations open room for modern devices that can address harder stones and wider patient profiles. Clinical trials report 88% fragmentation and nearly 49% stone-free status with burst-wave ultrasound, illustrating efficacy gains over legacy systems. Market demand consequently favors solutions that secure higher clearance in fewer sessions, reinforcing steady volume growth within the lithotripsy device market.

Thulium-fiber lasers, vortex-beam ultrasound, and optimized energy-delivery algorithms are rewriting device specifications and clinical protocols. Olympus's SOLTIVE platform lowers procedure time by 20% and boosts fragmentation efficiency by 33% compared with Holmium YAG lasers. Boston Scientific's MOSES 2.0 reduces retropulsion by 50% and enables 90% same-day discharge, making it attractive for outpatient workflows. Academic prototypes such as Lithovortex showcase low-cost ultrasound designs that promise non-invasive fragmentation for broader patient cohorts. These advances help providers elevate outcomes while trimming anesthesia use, fueling premium-priced system demand across the lithotripsy device market.

Stone street formation and other side effects from shock-wave therapy remain clinical concerns, especially for lower-pole renal stones where flexible ureteroscopy achieves 90.2% stone-free rates versus ESWL's 61.5%. Manufacturer exits from the ESWL segment and clinician shifts toward endoscopic modalities illustrate growing selectivity. Although burst-wave refinements may revitalize extracorporeal offerings, safety perceptions continue to cap ESWL spend within the lithotripsy device market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Extracorporeal shock-wave units captured 53.16% of lithotripsy device market share in 2024, yet intracorporeal platforms are forecast to rise at 5.89% CAGR through 2030. Laser-based systems, especially thulium-fiber models, fragment stones twice as quickly at half the power of earlier lasers, a performance win that has shifted hospital investment priorities. Electromagnetic ESWL devices keep traction in high-volume centers because of their procedural familiarity, while piezoelectric variants carve out specialized niches where precise energy targeting is essential.

Intracorporeal advances dovetail with the broader surgical trend toward precision and minimal tissue insult. Laboratory evidence shows 92% fragmentation under optimized settings, widening clinical acceptance of these tools. Ultrasonic lithotrites with aspiration enhance percutaneous workflows, and pneumatic devices persist in difficult cases needing mechanical impact. Collectively, these dynamics lift the intracorporeal portion of the lithotripsy device market while pushing vendors to diversify portfolios beyond legacy extracorporeal units.

Stand-alone suites held 65.42% of the lithotripsy device market size in 2024, anchored by well-equipped hospital units handling complex cases with integrated imaging. Yet portable and tabletop designs are pacing the modality race with a 6.25% CAGR. Break Wave ultrasound shows how mobility and anesthesia-free performance can broaden access to emergency departments and rural clinics. The Lithovortex prototype amplifies this shift by packaging vortex-beam capability into an affordable footprint suited for budget-restricted settings.

Operational flexibility is critical. Portable systems shorten room turnover, fit multi-department use, and lower facility overhead, making them popular with ASC administrators aiming for strong throughput. Vendors are thus engineering hybrid configurations-compact enough for transport yet robust enough to integrate with fluoroscopy-ensuring continued relevance across multiple care environments within the lithotripsy device market.

The Lithotripsy Devices Market Report is Segmented by Device Type (Extracorporeal Shock-Wave Lithotripters and Intracorporeal Lithotripters), Modality (Stand-Alone Systems and Portable / Table-Top Systems), Application (Kidney Stones, Ureteral Stones, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 32.56% of lithotripsy device market share in 2024, supported by transparent reimbursement pathways and a dense ASC network. Hospitals exploit Medicare coding stability to justify equipment refresh cycles, while vendors enjoy receptive early-adopter physician bases. The region's robust after-sales service networks further safeguard utilization uptime, sustaining replacement demand.

Europe follows with mature yet steadily modernizing health systems. National health funds encourage minimally invasive interventions, accelerating adoption of newer lasers and portable ultrasound. Cross-border purchasing frameworks support multicountry tenders that often favor vendors offering comprehensive training and maintenance, a factor strengthening pan-regional product footprints.

Asia Pacific is forecast to grow at 7.53% CAGR thanks to infrastructure expansion, regulatory reforms, and rising per-capita income. Japan's USD 40 billion medical-device sector is investing heavily in IoT-enabled equipment that maximizes operating-room productivity. China's debt-relief strategy is unblocking hospital CAPEX budgets, and India's conduct code is fostering market transparency. Middle East & Africa plus South America trail in absolute value but are accelerating as new private hospitals and public-sector projects equip operating theaters, broadening the global footprint of the lithotripsy device market.