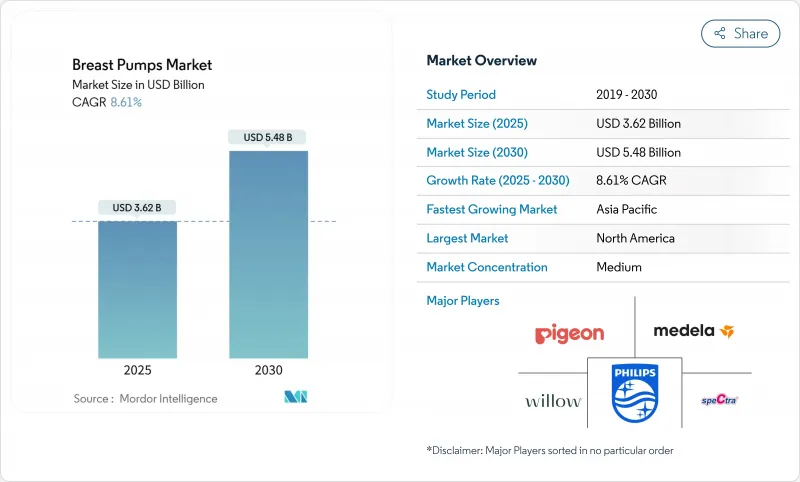

유축기 시장은 2025년 36억 2,000만 달러에 이르고, 2030년에는 54억 8,000만 달러에 달하며, CAGR 8.61%를 나타낼 것으로 예측됩니다.

모든 주요 지역에서 직장에서의 수유 의무화, 핸즈프리 웨어러블 기술 혁신, 전자상거래를 통해 소비자에게 직접 판매하는 세 가지 구조적 힘으로 최신 착유 솔루션에 대한 액세스가 확대되고 있습니다. 임신 노동자 공정법(Pregant Workers Fairness Act)의 적용을 받는 고용주는 합리적인 모유 수유를 제공해야 하기 때문에 폐쇄 시스템의 전동 모델에 대한 기업 수요는 계속 증가하고 있습니다. 한편, AI 대응으로 앱과 연동하는 펌프는 가정의 루틴을 바꾸어 프리미엄 업그레이드를 촉구합니다. 온라인 판매 채널은 보험 상환을 단순화하고 마크업을 낮추고 배송 시간을 단축합니다. 동시에 워싱턴에서 서울에 이르기까지 각국 정부는 계속해서 임산부의 건강 자금을 계상하고 있으며, 이는 연구개발 활동을 촉진하고 규제 당국의 인가를 가속화하고 있습니다.

노동 인구 증가는 일하는 어머니가 근무 시간 동안 효율적인 착유 도구를 필요로 하기 때문에 유축기 시장을 계속 확대하고 있습니다. 2024년 횡단조사에서 미국 유급휴가법이 있는 국가의 모유 육아율은 20.36%였지만, 그러한 지원이 없는 국가에서는 18.48%였습니다. 이러한 차이는 여성이 경력을 유지하면서 모유 수유 목표를 달성할 수 있도록 지원하는 휴대용 및 병원용 강력한 장비 수요에 직접 연결됩니다. 네슬레와 같은 소비재 대기업은 인도와 동남아시아에서 임산부 영양 SKU를 추가하고 민간 부문이 지속적인 성장을 확신하고 있음을 보여줍니다.

대서양 양안의 규제 당국은 수유 공간과 수유 설비의 이용을 규정함으로써 수요를 밀어 올렸습니다. 임신 노동자 공정법은 미국의 고용주에게 수유 활동을위한 합리적인 편의를 제공하도록 의무화하고 있습니다. 유럽의 지침도 유사한 개혁을 뒷받침하고 있으며 기업의 컴플라이언스 준수가 다중 사용자 대응 병원 펌프의 대량 조달을 뒷받침하고 있습니다. Mamava와 같은 턴키 포드 제공업체는 직장에서의 설치가 크게 증가하고 있다고 보고하고 있으며, 정책이 예측 가능한 수요를 창출하는 방법을 뒷받침합니다. 유급휴가 취득 기간이 길면 펌프를 사용하는 기간 전체도 길어져서 교체나 액세서리 판매가 강화됩니다.

보험이 적용되는 것은 일반적으로 기본적인 전동 모델만으로, 앱과 연동한 고급 기능은 자기 부담이 되는 경우가 많습니다. 소유 비용에 관한 연구에서는 시간 절약이라는 점에서 전동 펌프가 유리합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

폐쇄계 펌프는 2024년 매출의 69.84%를 차지했고, 2030년까지의 CAGR은 10.23%를 나타낼 것으로 예측됩니다. 오염 방지용 역류 방지 장벽은 NICU의 엄격한 프로토콜을 충족하고 시설에서 주문을 늘립니다. 다중 사용자 병원 프로그램을 위해 설계된 Medela Symphony PLUS는 이 안전 제일 추세를 상징합니다. 오픈 시스템 펌프는 구매 가격이 저렴하기 때문에 예산에 집착하는 가정에 여전히 매력적이지만 보험 회사가 상환 일정을 폐쇄 아키텍처를 포함하도록 업그레이드함에 따라 점유율은 계속 감소하고 있습니다.

소비자 환경에서는 가정에서 병원 수준의 위생을 요구하기 때문에 부모는 때때로 사용하는 경우에도 폐쇄 시스템 키트를 선택하는 것이 증가하고 있습니다. 소아과학회의 권고를 통해 흐르는 감염제어 가이드라인에 대한 의식의 고조가 이 기호를 더욱 강화하고 있습니다. 제조업체는 현재 멸균하기 쉬운 부품이나 유출 어려운 다이어프램을 마케팅 카피로 강조하고 있어 이것이 클로즈드 시스템의 채용을 한층 강화하고 있습니다.

전동식은 2024년 세계 매출의 61.23%를 차지했습니다. 전동식은 병원 수준의 흡인력, 프로그램 가능한 사이클, 우수한 수유량을 약속합니다. 전동식 부문은 CAGR 9.86%를 나타내 지속적인 모터 효율 향상과 배터리 수명 확대를 반영합니다. 수동식 펌프는 여행과 조용한 작동을 위해 매력을 유지하지만, 전기식 가격대가 낮아짐에 따라 점차 교체에 직면하고 있습니다.

배터리 구동 장치는 벽 콘센트의 성능과 장착 가능한 자유도의 갭을 메우는 것입니다. 신규 진출기업은 브러쉬리스 DC 모터와 컴팩트한 리튬 폴리머 배터리를 융합시켜 흡인력을 저하시키지 않고 무게를 삭감하고 있습니다. 스마트 센서를 통한 피드백 루프는 실시간 압력 조정을 제공하며 컴패니언 앱은 그래픽 대시보드에 출력을 기록합니다. 이러한 업그레이드를 통해 전동식은 처음 사용자나 경험이 풍부한 사용자에게 기본 옵션이 됩니다.

북미는 2024년 세계 매출의 35.43%를 차지했으며, 보험 상환, 엄격한 고용주 대응, 1인당 가처분 소득 높이에 힘입었습니다. 이 지역의 유축기 시장 규모는 2030년까지 약 19억 달러에 달할 것으로 예상됩니다. 연방 정부의 자금 지원도 AI를 활용한 수유 모니터링 연구 개발에 박차를 가해 프리미엄 채용률을 밀어 올리고 있습니다.

유럽은 관대한 출산 휴가 제도와 모유 수유를 중시하는 문화 덕분에 2위를 차지하고 있습니다. 윌로우가 엘비의 자산을 인수하고, 웨어러블의 지적 재산을 미국 브랜드의 산하에 집약함으로써 경쟁의 격렬함이 증가하고 있습니다. 데이터 보안과 CE 마크 컴플라이언스를 중시하는 판매자가 규제 당국에 우위를 둡니다.

아시아태평양의 CAGR은 10.12%를 나타낼 전망이며, 성숙한 구미 시장과의 차이를 줄이려고 합니다. 한국에서는 10조원 규모의 의료제도 개혁에 의해 임산부 케어 기기에 자금이 확보되고, 인도에서는 여성의 노동력 기반이 확대되어 도시의 견조한 수요를 지지하고 있습니다. 네슬레와 같은 다국적 기업은 보다 작은 골격과 현지 전압 기준에 맞게 설계된 펌프 등 지역 제품 현지화에 적극적으로 투자하고 있습니다.

라틴아메리카와 중동 및 아프리카는 보급의 초기 단계에 있지만 전자상거래의 강력한 성장을 보여줍니다. 현지 판매자는 브랜드 인지도의 낮음을 극복하기 위해 펌프를 임산부용 비타민 키트와 번들하는 경우가 많습니다.

The breast pumps market stands at USD 3.62 billion in 2025 and is projected to reach USD 5.48 billion by 2030, advancing at an 8.61% CAGR.

Across every major region, three structural forces-workplace lactation mandates, hands-free wearable innovation, and direct-to-consumer e-commerce-are expanding access to modern pumping solutions. Employers covered by the Pregnant Workers Fairness Act must now provide reasonable lactation accommodations, so corporate demand for closed-system electric models keeps building. Meanwhile, AI-enabled, app-linked pumps transform home routines and encourage premium upgrades. On-line sales channels simplify insurance reimbursement, lower mark-ups, and shorten delivery times, all of which enlarge the overall addressable base. At the same time, governments from Washington to Seoul continue earmarking maternal-health funds, which fosters R&D activity and accelerates regulatory clearances.

Rising labor-force participation keeps expanding the breast pumps market because working mothers need efficient pumping tools during office hours. A 2024 cross-sectional study found exclusive-breastfeeding rates of 20.36% in U.S. states with paid family-leave laws versus 18.48% in states without such support. These differences translate directly into demand for portable, hospital-strength devices that help women meet lactation goals while maintaining careers. Consumer-goods leaders such as Nestle have added maternal-nutrition SKUs in India and Southeast Asia, signaling private-sector confidence in sustained growth. As more women enter office, retail, and manufacturing jobs, the need for reliable, closed-system electric pumps rises steadily.

Regulators on both sides of the Atlantic boosted demand by stipulating access to lactation spaces and equipment. The Pregnant Workers Fairness Act obliges U.S. employers to supply reasonable accommodations for pumping activities. European directives push similar reforms, and corporate compliance is driving bulk procurement of multi-user hospital-grade pumps. Turn-key pod providers such as Mamava report a broad uptick in workplace installations, underlining how policy creates predictable demand. Longer paid-leave durations also stretch the overall pumping period, reinforcing replacement purchases and accessory sales.

Premium wearable units can exceed USD 400, which restricts uptake among price-sensitive shoppers. Insurance typically covers only basic electric models, so advanced app-linked features often still require out-of-pocket spending. While cost-of-ownership studies favor electric pumps on time savings, many families in low- and middle-income economies still view manual expression as more economical despite higher physical strain.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Closed-system pumps commanded 69.84% of revenue in 2024, and their CAGR out to 2030 is pegged at 10.23%. Contamination-prevention backflow barriers satisfy strict NICU protocols, which amplifies institutional orders. The Medela Symphony PLUS, designed for multi-user hospital programs, epitomizes this safety-first trend. Open-system pumps still appeal to budget-focused families because of lower acquisition prices, yet their share keeps sliding as insurers upgrade reimbursement schedules to include closed architectures.

In consumer environments, parents increasingly select closed-system kits even for occasional use because they want hospital-grade hygiene at home. Greater awareness of infection-control guidelines, broadcast through pediatric-society advisories, reinforces that preference. Manufacturers now emphasize easy-to-sterilize components and spill-proof diaphragms in marketing copy, which further strengthens closed-system adoption.

Electric designs held 61.23% of global revenue during 2024. They promise hospital-strength suction, programmable cycles, and superior milk output. The electric segment's 9.86% CAGR reflects continual motor-efficiency improvements and widening battery-life ranges. Manual pumps retain appeal for travel and silent operation but face gradual displacement as electric price points fall.

Battery-powered units bridge the gap between wall-plug performance and wearable freedom. New entrants are merging brushless DC motors with compact lithium-polymer cells, trimming weight without reducing suction. Smart-sensor feedback loops provide real-time pressure adjustments, and companion apps log output in graphical dashboards. These upgrades position electric formats as the default choice for both first-time and experienced users.

The Breast Pumps Market Report is Segmented by Product (Open System Breast Pump and Closed System Breast Pump), Technology (Manual Breast Pump, Battery Powered Breast Pump, and Electric Breast Pump), Application (Personal/ Home Use and Hospital Grade), Distribution Channel (Offline/ Retail and Online) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 35.43% of global revenue in 2024, propelled by insurance reimbursement, strict employer accommodations, and high per-capita disposable income. The breast pumps market size in the region is forecast to reach nearly USD 1.9 billion by 2030. Federal funding has also spurred R&D around AI-enabled lactation monitoring, which feeds premium adoption rates.

Europe ranks second thanks to generous maternity-leave statutes and a culture that values breast-feeding. Competitive intensity is rising after Willow acquired Elvie's assets, consolidating wearable intellectual property under a U.S. brand umbrella. Sellers who emphasize data security and CE-mark compliance hold an edge with regulatory bodies.

Asia-Pacific stands out with a 10.12% CAGR and is on track to narrow the gap with mature Western markets. South Korea's KRW 10 trillion healthcare overhaul reserved funds for maternal-care devices, and India's swelling female-workforce base underpins steady urban demand. Multinationals like Nestle invest aggressively in regional product localization, including pumps engineered for smaller body frames and local voltage standards.

Latin America and the Middle East & Africa are earlier in the adoption curve yet exhibit strong e-commerce growth. Local distributors often bundle pumps with prenatal vitamin kits to overcome lower brand recognition. Incentive programs run by health ministries in Brazil and the Gulf Cooperation Council frame breast-feeding as a national health priority, indirectly stimulating pump purchases.