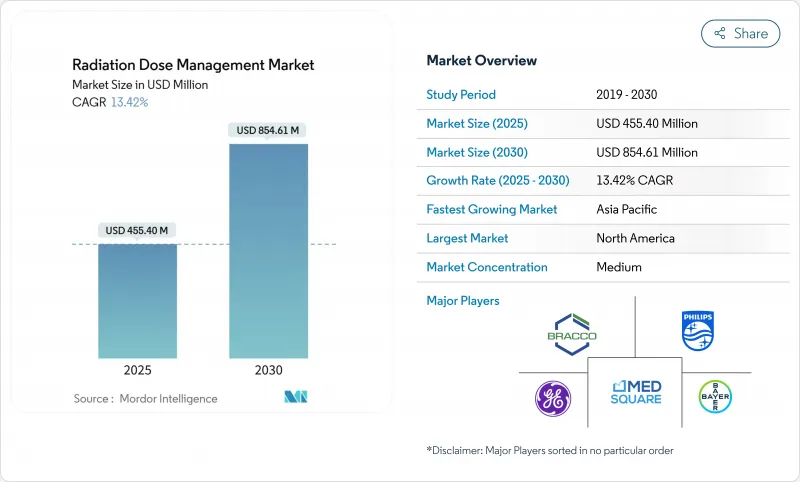

방사선량 관리 시장은 2025년에 4억 5,540만 달러에 이르고, 2030년에는 8억 5,461만 달러에 달하며, CAGR 13.42%를 나타내 강력하게 전진하고 있습니다.

성장의 배경은 방사선 안전 규제 강화, 종양학에서 정밀 이미징으로의 급속한 이동, AI 기반 선량 최적화 도구의 성숙을 포함합니다. 새로운 진단 기준 수준의 의무화에는 금전적인 벌칙이 수반되기 때문에 병원은 현재 컴플라이언스를 이사회 수준의 우선순위로 취급하고 있습니다. 클라우드 분석은 자원에 제약이 있는 시설의 소유 비용을 낮추고 통합 플랫폼은 의료 시스템이 원활한 워크플로우를 요구하는 가운데 포인트 솔루션을 대체합니다. 이미지 처리 OEM이 기존 기기에 선량 추적 기능을 번들해 퓨어 플레이 벤더가 AI 기능을 강조함으로써 경쟁 구도이 격화되고, 상호 운용성과 실시간 분석이 구매 의사 결정을 좌우하는 상황이 탄생하고 있습니다.

규제 당국은 자발적인 지침에서 강제 복용량 한도로 이동하고 모든 이미지 제공업체는 스캐너 수준에서 추적을 통합해야 합니다. FDA는 현재 CT 시스템에 누적 선량을 표시하고 자동 로그를 유지할 것을 의무화하고 있습니다. 합동위원회(Joint Commission)는 2024년의 인정조항으로 병원에 대해 방사선 안전 프로그램을 매년 감사할 것을 의무화하고 보고용 소프트웨어 수요에 박차를 가했습니다. 유럽에서는 의료기기 규제를 통해 시장 진입을 선량 최적화의 증거와 연결함으로써 이 자세를 반영하고 있습니다. 미국에서는 CMS의 품질 측정이 보험 상환을 컴플라이언스와 연결하기 때문에 경영진은 선량 관리를 선택적 업그레이드가 아닌 수익 보호로 간주합니다. 이러한 규칙을 종합하면 방사선량 관리 시장은 모든 영상 진단 양식에 필수적인 계층이 됩니다.

암 치료는 현재 치료 효과를 모니터링하기 위해 연속 CT, PET-CT, SPECT-CT에 의존하고 있으며 환자의 누적 피폭량을 증가시키고 감시를 강화하고 있습니다. 한 번의 PET-CT가 20mSv를 초과할 수 있으며, 직원의 연간 노출 한도에 가까워지는 기세이며, 환자는 대개 치료 주기마다 여러 번 검사를 받습니다. 전신 PET 시스템은 노출을 줄이지만 여전히 전문 시설에 국한되어 있으며 선량에 대한 우려가 여전히 높습니다. 소아 및 청소년 성인 종양학에서는 평생 위험 모델이 과도한 방사선에 페널티를 부과하기 때문에 긴급성이 증가하고 있습니다. AI에 의한 프로토콜의 개인화가 여기에 추가되어 환자의 병력에 따라 설정을 좁히면 화질을 떨어뜨리지 않고 총 선량을 낮출 수 있습니다. 이와 같이 워크플로우가 고도의 모니터링에 의존하는 것으로, 방사선량 관리 시장의 중심적인 부문으로서 종양과가 자리잡고 있습니다.

이익률이 낮은 시설에서는 선량 추적 장치의 구입과 환자 관리의 즉각적인 요구를 비교 검토하고 있습니다. 풀플랫폼은 5만 달러에서 20만 달러를 넘기 때문에 직접적인 상환 인센티브가 없으면 정당화하기가 어렵습니다. 중저소득 국가의 대부분은 여전히 기본적인 이미지 처리 능력을 확대하는 데 중점을 두고 있기 때문에 고급 모니터링은 두 번째입니다. 공급업체는 임대 및 SaaS 조건을 제공하지만 자본 부족으로 인해 널리 보급되어 방사선량 관리 시장의 2층 구조가 유지됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

통합 플랫폼은 2024년에 방사선량 관리 시장의 45.23%를 차지했으며 CAGR 17.12%를 나타낼 전망입니다. 이 이점은 하나의 워크플로우에서 피폭선량 추적, 프로토콜 최적화, 규제 보고서 자동 생성을 위한 통합 대시보드 때문입니다. 의료 시스템은 적은 공급업체, 적은 훈련 오버헤드, 싱글 사인온의 사용 편의성을 선호합니다. 독립형 트래커는 예를 들어 핵의학 선량 측정과 같은 틈새 시장을 유지하지만 플랫폼 제공 업체가 동등한 모듈을 매력적인 가격으로 번들로 제공하므로 마진 압력에 직면합니다. 관리 서비스는 병원이 의료 물리학 과제를 아웃소싱하기 때문에 가장 빠르게 이익을 얻고 있습니다. 따라서 임상 지원이 충실한 벤더는 장기 계약을 확보하고 방사선량 관리 시장에서 플랫폼의 안정성을 높이고 있습니다.

전문가의 서비스도 의료기관이 벤치마크 해석과 규정 준수 갭 해소를 요구함에 따라 증가하고 있습니다. 권고 소득은 소프트웨어 구독을 보완하고 고객의 평생 가치 전체를 확대합니다. 전반적으로, 통합된 접근법에 의한 설명은 사일로화된 용도으로부터 모달리티를 넘어 확장하는 생태계로의 전환을 강화하고, 통합된 제품군을 방사선량 관리 시장 전략의 중심에 둡니다.

On-Premise는 여전히 59.45%의 점유율을 차지하고 있지만, 이는 개인정보보호규칙과 뿌리를 둔 위험 회피의 증거이며 클라우드 솔루션은 CAGR 16.78%를 나타낼 전망입니다. 대기업에서는 데이터를 클라우드로 분석하고 이미지를 로컬로 유지하는 하이브리드 모델을 채용하는 경우가 많습니다. 이 전략은 AI와 고급 벤치마킹을 실현하면서 거주에 관한 법률을 존중합니다. 지역 병원에서는 종량 과금제에 의해 대액의 자본 지출을 없애, 방사선량 관리 업계의 최신 툴에의 액세스를 넓히고 있습니다.

GPU를 많이 사용하는 AI 추론과 지속적인 소프트웨어 업데이트가 방정식에 추가되면 총 소유 비용이 클라우드로 더욱 기울어집니다. 공급업체는 규제 당국을 진정시키기 위해 암호화 오버레이와 지역별 스토리지 영역을 소개합니다. 주권에 대한 논의는 계속되고 있지만 성능과 경제적 이점으로 인해 클라우드로의 전환이 꾸준히 진행되고 있습니다. 그 결과 클라우드 아키텍처는 2030년까지 특히 여러 시설을 동시에 현대화하는 시스템에서 방사선량 관리 시장에서 훨씬 더 큰 비율을 차지할 것으로 예측됩니다.

북미는 Joint Commission(합동위원회) 시행과 CMS가 최적화를 진료보수에 연결시키고 있는 것을 배경으로 2024년에는 방사선량 관리 시장의 33.23%를 차지했습니다. FDA에 의한 AI 툴의 조기 인가는 미국의 의료 시스템에 선행자 이익을 가져오고, 캐나다도 독자적인 선량 보고 기준으로 추종합니다. 멕시코에서는 민간 병원 체인에서 도입이 진행되고 있지만, 미국에 비하면 아직 늦어지고 있습니다. 레거시 PACS의 포화로 인해 도입이 지연될 수 있지만, EHR 연결의 보급이 기업 전체의 벤치마크를 지원하고, 이 지역은 절대적인 지출액으로 우위를 유지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 15.03%를 나타내 가장 급성장하고 있는 지역입니다. 인도의 대규모 병원 건설 계획과 중국의 디지털 헬스에 대한 투자가 지출을 선도하는 한편, 일본은 고령화 사회에 직면하고 있어 화상 처리에 힘을 쏟고 있습니다. 호주와 한국은 선진국 시장의 패턴을 반영하여 하이브리드 배포의 선호와 AI 모듈의 신속한 도입을 볼 수 있습니다. 동남아시아 국가들은 우선 스캐너 조달을 선호하지만, 새로운 국가 가이드라인을 충족하기 위해 선량 관리를 번들로 늘고 있습니다. 이처럼 성숙도의 폭이 넓기 때문에 APAC는 벤더가 가격설정과 도입모델을 지역별로 적응시켜야 하는 패치워크와 같은 상태로 되어 있지만, 그래도 방사선량 관리 시장의 가장 역동적인 부문임에 변함이 없습니다.

유럽은 MDR의 하모나이제이션으로 회원국 간의 벤더 인증을 간소화하여 꾸준히 성장하고 있습니다. 독일, 프랑스, 영국이 도입의 선진을 끊고, 북유럽 국가들은 통합 의료 시스템에 의해 거의 보편적인 컴플라이언스를 달성하고 있습니다. 재정적 제약이 완화되고 디지털 헬스에 대한 자금 지원이 증가함에 따라 남유럽 국가들이 추격해 옵니다. 데이터 주권을 고려할 때 로컬 스토리지와 클라우드 분석을 결합한 하이브리드 솔루션이 권장됩니다. Brexit에 의한 규제의 괴리는 사무 작업을 늘리지만, NHS의 현대화 계획에 선량 안전성 지표가 포함되어 있는 영국에서는 수요를 억제하고 있지 않습니다.

The radiation dose management market reached USD 455.40 million in 2025 and is on track to generate USD 854.61 million by 2030, advancing at a strong 13.42% CAGR.

Growth rests on tighter radiation-safety regulations, the rapid shift to precision imaging in oncology, and the maturing of AI-based dose-optimization tools. Hospitals now treat compliance as a board-level priority because new diagnostic reference level mandates carry financial penalties, while CT and hybrid-imaging volumes keep rising in cancer care. Cloud analytics lower ownership costs for resource-constrained facilities, and integrated platforms replace point solutions as health systems seek seamless workflows. Competition intensifies as imaging OEMs bundle dose-tracking into existing equipment and pure-play vendors highlight AI capabilities, creating a landscape in which interoperability and real-time analytics sway purchasing decisions.

Regulators have moved from voluntary guidance to mandatory dose ceilings, forcing every imaging provider to embed tracking at the scanner level. The FDA now requires CT systems to display cumulative dose and maintain automated logs, a shift that steers procurement toward scanners with built-in monitoring. The Joint Commission followed with 2024 accreditation clauses that oblige hospitals to audit radiation safety programs annually, spurring demand for reporting software. Europe mirrors this stance through the Medical Device Regulation, which ties market access to evidence of dose optimization. In the United States, CMS quality measures link reimbursement to compliance, so executives view dose management as revenue protection rather than an optional upgrade. Collectively, these rules turn the radiation dose management market into a must-have layer across all imaging modalities.

Cancer care now relies on serial CT, PET-CT and SPECT-CT to monitor therapy response, raising cumulative patient exposure and intensifying oversight. A single PET-CT can exceed 20 mSv, edging close to annual occupational limits for staff, and patients typically undergo several scans per treatment cycle. Total-body PET systems mitigate exposure yet remain limited to specialized centers, keeping dose concerns high. Pediatric and young-adult oncology heightens the urgency because lifetime risk models penalize excess radiation. AI-driven protocol personalization enters here, refining settings per patient history and thus lowering total dose without compromising image quality. This workflow dependence on advanced monitoring cements oncology as the anchor segment for the radiation dose management market.

Facilities operating on slim margins weigh dose-tracking purchases against immediate patient-care needs. A full platform can cost USD 50,000-200,000, a figure difficult to justify without direct reimbursement incentives. Many low-to-middle-income nations still focus on expanding basic imaging capacity, so sophisticated monitoring remains secondary. While vendors offer leasing and SaaS terms, capital scarcity keeps uptake uneven and sustains a two-tier structure within the radiation dose management market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Integrated platforms accounted for 45.23% of the radiation dose management market in 2024 and are growing at 17.12% CAGR. This dominance stems from unified dashboards that track exposure, optimize protocols and auto-generate regulatory reports in one workflow. Health systems prefer fewer vendors, lower training overhead and single-sign-on usability. Standalone trackers retain niches-for example, nuclear-medicine dosimetry-yet face margin pressure because platform providers bundle equivalent modules at attractive prices. Managed services post the fastest gains as hospitals outsource medical-physics tasks. Vendors with deep clinical support therefore secure long-term contracts, reinforcing platform stickiness within the radiation dose management market.

Professional services also rise as institutions seek help interpreting benchmarks and closing compliance gaps. Advisory revenue complements software subscriptions, enlarging total customer lifetime value. Overall, the integrated-approach narrative reinforces a migration away from siloed applications toward ecosystems that scale across modalities, keeping integrated suites at the center of the radiation dose management market strategy.

On-premise installations still hold 59.45% share, a testament to privacy rules and ingrained risk aversion, yet cloud solutions are climbing at 16.78% CAGR. Larger enterprises often adopt hybrid models that analyze data in the cloud while retaining images locally. This strategy respects residency laws while unlocking AI and advanced benchmarking. For community hospitals, pay-as-you-go pricing eliminates large capital outlays, widening access to the radiation dose management industry's newest tools.

Total cost of ownership tilts further toward the cloud when GPU-intensive AI inference and continuous software updates enter the equation. Vendors showcase encrypted overlays and region-specific storage zones to soothe regulators. Although the debate on sovereignty persists, the performance and economic benefits keep migration steady. As a result, cloud architectures are projected to command a far larger slice of the radiation dose management market by 2030, especially in systems modernizing multiple sites simultaneously.

The Radiation Dose Management Market Report is Segmented by Products & Services (Stand-Alone Dose-Tracking Software, Integrated Dose-Management Platforms, and More), Deployment Mode (OnPremise and Cloud), Modality (CT, Nuclear Medicine, and More), Application (Oncology, Cardiology and More), End User (Hospital, Ambulatory & Imaging Centers and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America owned 33.23% of the radiation dose management market in 2024 on the strength of the Joint Commission's enforcement and CMS linking optimization to reimbursements. Early FDA clearances for AI tools give U.S. health systems first mover advantage, and Canada follows with its own dose-reporting standards. Mexico shows rising traction in private hospital chains, though adoption still lags the United States. Legacy PACS saturation occasionally slows rollouts, yet widespread EHR connectivity supports enterprise-wide benchmarking, keeping the region firmly ahead in absolute spending.

Asia-Pacific is the fastest-growing arena, posting a 15.03% CAGR through 2030. India's expansive hospital-building program and China's digital-health investments lead volumes, while Japan confronts aging demographics that drive imaging intensity. Australia and South Korea mirror developed-market patterns with hybrid deployment preferences and quick uptake of AI modules. Southeast Asian countries prioritize scanner procurement first but increasingly bundle dose management to satisfy new national guidelines. This broad spectrum of maturity turns APAC into a patchwork where vendors must adapt pricing and deployment models locally, yet the aggregated opportunity remains the most dynamic segment of the radiation dose management market.

Europe grows steadily as MDR harmonization simplifies vendor certification across member states. Germany, France and the United Kingdom spearhead installations, with Nordic nations achieving near-universal compliance due to integrated care systems. Southern Europe catches up as fiscal constraints ease and digital health funding rises. Data-sovereignty considerations encourage hybrid solutions that couple local storage with cloud analytics, a configuration vendors now bake into proposals by default. Brexit's regulatory divergence adds paperwork but has not curtailed demand in the UK, where NHS modernization plans include dose safety metrics. Collectively, European procurement maintains a disciplined, safety-first posture that sustains predictable expansion of the radiation dose management market.