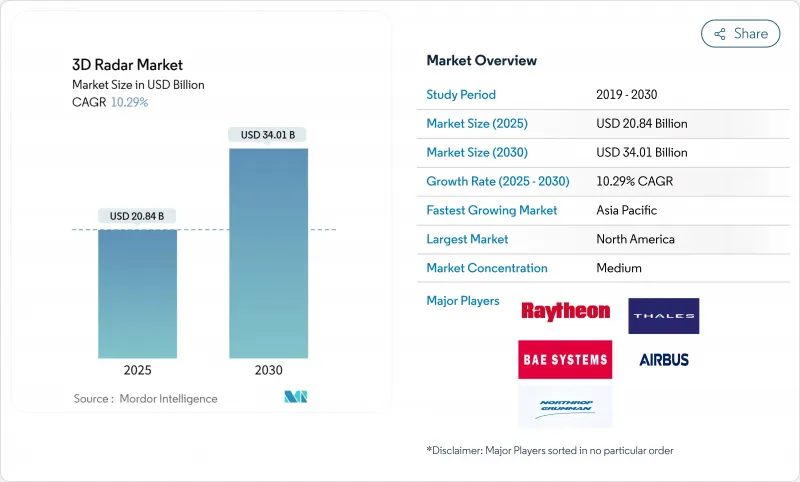

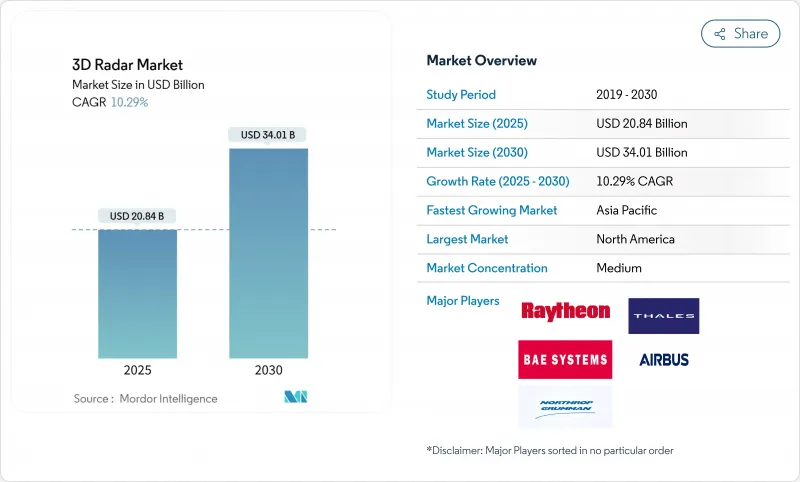

세계의 3D 레이더 시장은 2025년 208억 4,000만 달러로 평가되며, CAGR 10.29%를 나타내 2030년에는 340억 1,000만 달러에 달할 것으로 예상됩니다.

확대의 배경으로는 방어의 현대화 진전, 레이더 기반 운전 지원 기술의 자동차 채택 확대, 우주 기반 모니터링에 대한 왕성한 투자가 있습니다. GaN을 탑재한 AESA 아키텍처는 경쟁하는 전자기 환경에서 검출 범위를 25% 가까이 확대해, 인공지능은 타겟 분류 사이클을 수분에서 수초로 단축하고 있습니다. 지구 저궤도(LEO) 위성 추적, 대무인 항공기 시스템(C-UAS), 기후 변화에 강한 기상 모니터링에 대한 새로운 요구사항은 대응 가능한 기회를 넓히고 있습니다. 이러한 배경에서 제조업체는 개방형 시스템 아키텍처 및 소프트웨어 정의 업그레이드를 선호하고 3D 레이더 시장에서 수명 주기 가치를 극대화하고 지속적인 수익원을 확보하고자 합니다.

유럽 전역에서 조달 당국은 단일 어레이 내에서 항공 감시, 지상 감시 및 해안 감시 역할을 융합할 수 있는 멀티미션 레이더에 자금을 제공합니다. 이탈리아의 7,300만 유로 Skynex 계약은 이 변화를 보여주며, 라인 메탈의 대포와 저고도로 회전익 드론을 추적하는 50km 범위의 3D 레이더를 결합한 것입니다. 이 시스템은 드론 식별에 머신러닝을 활용하여 거의 실시간 위협 평가를 가능하게 하고 운영자의 작업 부하를 줄입니다. 모듈형 아키텍처는 기존 C-UAS 명령 네트워크에 대한 플러그 앤 파이트 통합을 지원하고 배포 일정을 가속화합니다. NATO가 위협 라이브러리와 소프트웨어 업데이트를 표준화함에 따라 대량 주문이 비용 곡선을 낮추고 3D 레이더 시장 수요를 강화하고 있습니다.

상업 위성 사업자는 광대역, 지구관측 및 궤도 서비스를 위해 수백 개의 소형 위성을 발사하고 있습니다. 그 결과 발생하는 트래픽을 관리하기 위해 각국 정부는 고도 500-1,200km로 1cm 이하의 물체를 카탈로그화할 수 있는 고정밀 3D 추적 레이더를 조달하고 있습니다. 록히드 마틴의 아키텍처 확산 전략은 우주 감시가 현재 AI 주도 지상 부문와 연결된 Ku/Ka 대역 어레이를 필요로 하는 방법을 보여줍니다. 북미 최종 사용자는 민군 공유 우주 지역 인식 플랫폼을 선호하고 3D 레이더 시장의 장기 전망을 강화하고 있습니다.

사이클론이 발생하기 쉬운 섬 섬나 아프리카 국가들은 기존의 2D 기상 레이더를 폭풍우의 구조를 실시간으로 해명할 수 있는 이중 편파 3D 시스템으로 대체하려고 합니다. 다자간 기후 적응 프로그램을 통해 자금을 지원하는 프로젝트는 훈련 및 유지보수 패키지가 번들로 제공되어 지속 가능한 운영을 보장합니다. 농업이 GDP의 20% 이상을 차지하는 지역에서는 3D 레이더의 도입이 가장 진행되고 있으며 3D 레이더 시장의 발전에 미치는 영향을 더욱 강화하고 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

국경 감시, 조기 경계, C-UAS 미션에서 매우 중요한 역할을 반영하여 지상 설치형이 2024년 3D 레이더 시장 점유율의 46.2%를 획득했습니다. 전력 최적화된 GaN T/R 모듈은 4시간 이내에 배포하여 Software-Defined Radio를 통해 전술 네트워크에 연결하는 휴대용 어레이를 가능하게 합니다. 지상 기반 레이더는 2kg 미만의 무인 항공기를 분류하는 AI 알고리즘의 혜택을 누리고 레이어드 디펜스 아키텍처의 의사 결정을 개선합니다.

5세대 전투기가 900개가 넘는 모듈을 탑재한 국산 AESA 레이더를 통합하여 낮은 시인성 타겟에 대한 내려다보는 감지를 확대함에 따라 항공기 부문은 CAGR 12.4%를 나타낼 전망입니다. 모듈식 라인 교환 가능한 유닛은 유지보수 턴어라운드를 30% 절감하고 3D 레이더 시장의 프리미엄 슬라이스로 에어본 솔루션을 자리잡고 있습니다. 해군 플랫폼은 배타적 경제 수역을 경비하는 해상 순찰선을 위해 설계된 경량 솔리드 스테이트 회전 어레이로 성장세를 늘리고 있습니다.

장거리 시스템은 2024년 3D 레이더 시장 규모의 41%를 차지하며 방공 식별권과 전략적 자산을 보호했습니다. 최근 배포에서는 디지털 파형의 민첩성과 에지 처리를 통해 1,500개의 물체를 추적하면서 600km의 장비 거리를 달성했습니다. AI 지원 클러터 맵은 극초음속 미사일 경보에 필수적인 산악지대에서 낮은 RCS 감지를 향상시킵니다.

CAGR 14.6%를 나타내는 단거리 레이더는 차량 탑재형 C-UAS 키트나 경계 경비 타워에 통합됩니다. 코프라임 샘플링 기술은 채널 수를 줄이고 옥상 설치를 위한 안테나 설치 면적을 줄입니다. 중거리 어레이는 최소 도달거리 3km와 최대 도달거리 120km의 균형을 맞추면서 기동부대의 방호에 대응하여 중층 방어의 교리상의 갭을 메우고 3D 레이더 시장 전체의 기회를 넓히고 있습니다.

3D 레이더 시장은 플랫폼별(공중, 지상, 기타), 레인지 유형별(장거리, 중거리, 기타), 주파수대별(L-band, S-band, 기타), 구성 요소별(하드웨어, 소프트웨어, 기타), 용도별(방어 및 보안, 항공관제, 기타), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 3D 레이더 시장 점유율의 38.7%를 차지하며 미사일 방어 시스템에 284억 달러, 태평양 억지 구상에 99억 달러의 추가 예산이 계상된 것으로 뒷받침되었습니다. AN/TPY-4 원정 레이더에 대한 최근 계약은 운송 가능한 장거리 커버리지를 향한 추진력을 보여줍니다. 지역 공급업체는 개방형 시스템 인터페이스와 AI 중심의 센서 퓨전을 강조하고 서비스 간의 상호 운용성을 강화합니다.

아시아태평양은 국산 프로그램이 능력의 격차를 메우기 때문에 CAGR 12.7%를 나타낼 전망입니다. 인도에서는 장거리 AESA 레이더의 자급 자족이 국경 감시를 강화하고 일본에서는 방위비를 GDP의 2%를 나타내 배가시킬 계획이 있어 하늘과 미사일의 통합 방위 지출이 가속되고 있습니다. PULSE 합작 사업과 같은 현지 생산 이니셔티브는 3D 레이더 시장에서 이 지역의 주권 생산에 대한 의욕을 반영합니다.

유럽은 NATO 대 UAS 요건과 방어 예산 증가를 통해 기세를 유지하고 있으며, 23개 회원국이 2% 목표를 달성하는 기세입니다. 이탈리아의 스카이넥스, 폴란드의 GDP 4.7%의 야망, EDF의 인지 레이더 연구에 대한 자금은 유럽 대륙의 투자 궤도를 돋보이게 합니다. 스펙트럼 관리 개혁은 도시 지역의 배치를 형성하고 장기적인 3D 레이더 시장의 성장에 영향을 미칠 것으로 보입니다.

중동 및 아프리카에서는 무인 항공기가 침입하는 동안 대부분의 경우 현지 조립에 박차를 가하는 오프셋 협정을 통해 중층 방공 체제를 업그레이드하고 있습니다. 남미 국가들은 재해에 강한 기상 레이더의 근대화를 우선시하고, 다국간 금융기관과 협력하여 위상 어레이 기술을 확보하고 있습니다. 이러한 지역이 통합되어 수요 증가에 기여하고 3D 레이더 시장의 세계 확대를 뒷받침하고 있습니다.

The global 3D radar market is valued at USD 20.84 billion in 2025 and is forecast to reach USD 34.01 billion by 2030, reflecting a 10.29% CAGR.

Expansion stems from rising defense modernization, wider automotive adoption of radar-based driver-assistance technologies, and strong investment in space-based surveillance. GaN-powered AESA architectures are extending detection ranges by nearly 25% in contested electromagnetic environments, while artificial intelligence is shortening target-classification cycles from minutes to seconds. Emerging requirements for low-Earth-orbit (LEO) satellite tracking, counter-unmanned-aircraft systems (C-UAS), and climate-resilience weather monitoring are widening the addressable opportunity set. Against this backdrop, manufacturers are prioritizing open-system architectures and software-defined upgrades to maximize lifecycle value and capture recurring revenue streams in the 3D radar market.

Across Europe, procurement authorities are funding multi-mission radars that can fuse air-surveillance, ground-surveillance, and coastal-surveillance roles within a single array. Italy's EUR 73 million Skynex contract exemplifies this shift, pairing Rheinmetall cannons with a 50 km-range 3D radar that tracks rotary-wing drones at low altitude. These systems leverage machine learning for drone discrimination, enabling near-real-time threat assessment and reducing operator workload. Their modular architecture supports plug-and-fight integration into existing C-UAS command networks, accelerating fielding schedules. As NATO standardizes threat libraries and software updates, volume orders are driving cost curves lower, reinforcing demand in the 3D radar market.

Commercial operators are launching hundreds of small satellites for broadband, Earth-observation, and in-orbit servicing. To manage the resulting traffic, governments are procuring precision 3D tracking radars capable of cataloguing objects below 1 cm at altitudes of 500-1,200 km. Lockheed Martin's strategy for proliferated architectures illustrates how space surveillance now demands Ku/Ka band arrays linked to AI-driven ground segments. North America's end-users are prioritizing shared civil-military space domain awareness platforms, bolstering the long-term outlook for the 3D radar market.

Cyclone-prone island states and African nations are replacing legacy 2D weather radars with dual-polarization 3D systems that can resolve storm structure in real time. Projects funded via multilateral climate-adaptation programs are bundling training and maintenance packages, ensuring sustainable operations. Adoption is strongest where agriculture contributes more than 20% of GDP, reinforcing the developmental impact of the 3D radar market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ground-based installations captured 46.2% of 3D radar market share in 2024, reflecting their pivotal role in border surveillance, early-warning, and C-UAS missions. Power-optimized GaN T/R modules enable transportable arrays that deploy within four hours and connect to tactical networks via software-defined radios. Ground-based radars are benefiting from AI algorithms that classify drones under 2 kg, improving decision-making for layered defense architectures.

The airborne segment is forecast to expand at 12.4% CAGR as fifth-generation fighters integrate indigenous AESA radars with over 900 modules, extending look-down detection against low-observable targets. Modular line-replaceable units cut maintenance turnaround by 30%, positioning airborne solutions as a premium slice of the 3D radar market. Naval platforms add growth momentum through lightweight solid-state rotating arrays designed for offshore patrol vessels guarding exclusive economic zones.

Long-range systems commanded 41% of the 3D radar market size in 2024, protecting air-defense identification zones and strategic assets. Recent deployments achieve 600 km instrumented range while tracking 1,500 objects, enabled by digital waveform agility and edge processing. AI-assisted clutter maps improve low-RCS detection over mountainous terrain, vital for hypersonic-missile warning.

Short-range radars, expanding at a 14.6% CAGR, are integrated into vehicle-mounted C-UAS kits and perimeter-security towers. Coprime-sampling techniques reduce channel counts, shrinking antenna footprints for rooftop installation. Medium-range arrays address mobile-force protection, balancing 3 km minimum range with 120 km maximum reach, thereby filling doctrinal gaps in layered defense and broadening opportunities across the 3D radar market.

3D Radar Market Segmented by Platform (Airborne, Ground and More), Range Type (Long Range, Medium Range and More), Frequency Band (L Band, S Band and More), Component (Hardware, Software and More), Application (Defense & Security, Air Traffic Control and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America led with 38.7% of 3D radar market share in 2024, underpinned by USD 28.4 billion earmarked for missile-defeat systems and an additional USD 9.9 billion Pacific Deterrence Initiative allocation. Recent contracts for AN/TPY-4 expeditionary radars illustrate the push toward transportable long-range coverage. Regional suppliers emphasize open-system interfaces and AI-driven sensor fusion, strengthening inter-service interoperability.

Asia-Pacific is climbing at a 12.7% CAGR as indigenous programs close capability gaps. India's self-sufficiency in long-range AESA radars bolsters border surveillance, while Japan's plan to double defense outlays to 2% of GDP accelerates integrated air-and-missile defense spending. Local manufacturing initiatives such as the PULSE joint venture reflect the region's appetite for sovereign production within the 3D radar market.

Europe maintains momentum through NATO counter-UAS requirements and rising defense budgets, with 23 member states on track to hit the 2% target. Italy's Skynex, Poland's 4.7% GDP ambition, and EDF funding for cognitive-radar research highlight the continent's investment trajectory. Spectrum-management reforms will shape urban deployments, influencing long-term 3D radar market growth.

The Middle East and Africa are upgrading layered air defenses amid drone incursions, often via offset agreements that spur local assembly. South American states prioritize weather-radar modernization for disaster resilience, working with multilateral financiers to secure phased-array technology. Collectively these regions contribute incremental demand, reinforcing the global expansion of the 3D radar market.