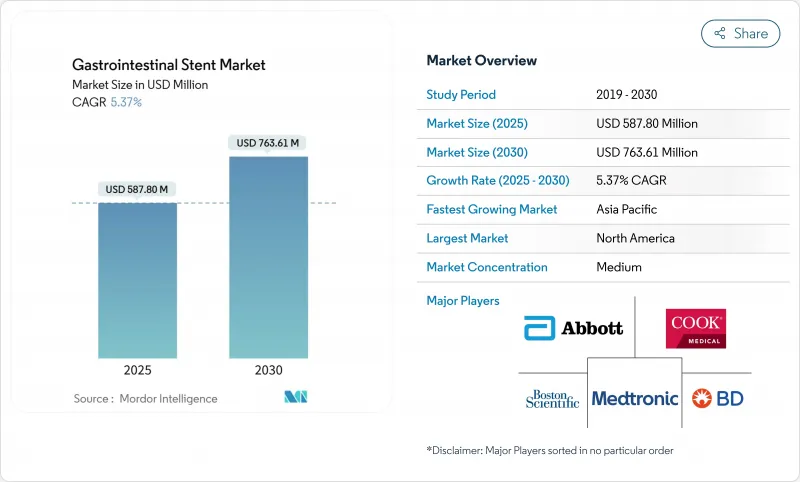

소화관 스텐트 시장은 2025년에 5억 8,780만 달러를 창출하고 예측 기간 중 CAGR은 5.37%를 나타내, 2030년에는 7억 6,361만 달러에 달할 것으로 예상되고 있습니다.

위장(GI) 암 증가, 저침습 내시경 검사에 대한 결정적인 임상적 축족, 스텐트 설계의 지속적인 진보, 특히 생분해성 및 약제 용출 형식이 이 확대를 지원하고 있습니다. 초음파 내시경(EUS) 및 인공지능 가이드 아래 계획의 광범위한 사용은 기술적 장벽을 낮추고 환자별 맞춤화를 개선하고, 특히 복잡한 췌장도 질환에 대한 절차 적합성을 넓혔습니다. 북미는 검사 건수의 리더를 유지하고 있지만, 대장암의 이환율이 높고, 병원망의 근대화가 급속히 진행되는 아시아태평양이 가장 진보가 빠른 지역입니다. 비용 절감, 회복 시간 단축, 높은 개존율을 강조하는 확고한 임상 증거는 지불자의 수용을 강화하고 악성과 양성 모두의 적응증에서의 채용을 가속화하고 있습니다.

아시아에서의 대장암의 이환율은 2024년에는 인구 10만명당 23.88명까지 상승하여 위암을 빼고 지배적인 소화기계 악성 종양이 되어 수술까지의 연결로서 대장 스텐트에 대한 지속적인 수요를 만들어냈습니다. 자기 확장형 금속 스텐트는 현재 악성 위 출구 폐색에 대해 89.7%의 임상적 성공을 거두었으며 지속적인 개존과 긴급 수술 감소를 실현하고 있습니다. 네오애쥬번트 화학요법과 스텐트 유치의 통합은 종양 축소와 수술 성적을 최적화하고 수술 건수를 더욱 강화합니다. 암 검진의 보급은 생존율의 향상과 함께 팔로우 업이나 완화를 목적으로 한 수술의 빈도를 증가시키고 있습니다.

인구 역학의 고령화는 양성 담도 협착과 췌장염 관련 합병증을 증가시키고 개복 수술에 적합하지 않은 경우가 많습니다. 짧은 풀 커버 메탈 스텐트는 노인 코호트에서 양성 협착의 99%를 해결하고 수술에 비해 수술 위험과 입원 기간을 단축합니다. 가치관에 기반한 의료를 요구하는 의료 시스템은 이러한 낮은 침습 경로를 선호하며 성숙 시장 전체에서 장기적인 이용을 강화하고 있습니다.

FDA의 보고에 따르면 스텐트의 위치 문제(35.6%)와 이동(12.4%)이 주요 장치에 대한 클레임으로 언급되었으며, 출혈과 천공은 환자 관련 사건의 상위를 차지하고 있습니다. 이동률은 40%에 달할 수 있으며 비용과 환자 안전에 대한 우려가 높아지고 있습니다. 플라스틱 담도 스텐트를 잊어 버리면 담관염의 위험과 막힘 사고가 증가하므로 자동 회수 알림이 필요합니다. 차세대 마이그레이션 방지 핀과 생분해성 형식은 2차 처리를 줄이고 품질 지표를 향상시키는 것을 목표로 합니다.

분석되는 기타 성장 촉진요인 및 억제요인

담도 스텐트는 악성 및 양성 담도 폐색증에서 확고한 역할을 반영하여 소화관 스텐트 시장에서 2024년 매출의 37.23%를 차지했습니다. 레이저 컷 모양, 친수성 코팅, 얇은 배달 카테터는 좁은 관과 복잡한 폐문 병변에 정확한 유치를 촉진합니다. 식도 스텐트와 십이지장 스텐트는 삼키는 장애를 개선하는 역류 방지 밸브의 개선으로 인해 용량이 증가하고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 것은 대장 스텐트에서 8.94%를 나타낼 전망입니다. 비교 연구에 따르면, 자기 확장형 금속 스텐트는 인공 항문의 형성을 피하면서 긴급 수술과 동등한 생존율과 QOL을 초래합니다. 내부 플랩이 없는 췌장의 디자인은 80.7%의 자연 이동을 기록하고, 회수 절차를 면제하고, 외래 환자의 프로토콜을 따릅니다. 약물 용출성 제형의 개선은 조직 내 증식 억제를 표적으로 하고 모든 제품 클래스에서 새로운 가치 제안을 제시합니다.

자체 확장형 금속 장치는 2024년 매출의 61.67%를 차지했으며, 반경방향 강도와 유연성의 균형을 강조했습니다. 임상시험에서는 회맹부폐색에 대한 100%의 기술적 성공과 92.3%의 임상적 성공이 확인되어 기존의 좌측 결장 이외에의 적응성이 검증되었습니다. 레이저 커팅에 의한 마이크로 메쉬 패턴을 포함한 고급 니티놀 가공은 구부러진 해부학적 구조에 대한 적합성을 향상시킵니다.

CAGR 8.79%를 나타내는 생분해성 및 약물용출성의 포맷은 제거할 필요가 없는 일시적인 비계로서의 요구에 응하고 있습니다. 철을 기반으로 한 프로토타입은 기계적 예비력을 높이는 동시에 X선 투과성을 추적 할 수 있습니다. 하이브리드 구조물은 금속 백본의 신뢰성과 함께 시간적 분해를 가져오고 양성 질환 관리의 적응 경계를 바꿀 것으로 예측됩니다. 플라스틱은 조기 회수가 계획된 경우 단기 배수에 적합하며 소화관 스텐트 시장에서 틈새 시장을 유지합니다.

북미는 2024년 매출의 35.47%를 차지하며, 확립된 상환경로와 절차에 대한 깊은 전문지식을 받았습니다. 메디케어에 의한 소화관 스텐트 유치술의 보험 적용은 예측 가능한 지불 사이클을 지원하는 것이며, 제조업체 주도의 등록은 지불측의 갱신을 가속화하는 실제 임상 증거를 제공하는 것입니다. 미국의 센터는 스텐트 치료, 화학요법, 수술을 통합한 집학적 종양보드를 중시하고 성숙한 수요를 유지하고 있습니다. 캐나다의 국민 모두 보험 제도도 마찬가지로 공평한 액세스를 보증해, 안정된 베이스 라인량을 키우고 있습니다.

아시아태평양은 인구동태의 고령화, 대장암 이환율 증가, 공적보험의 확충에 힘입어 2030년까지의 CAGR이 가장 빠른 8.23%를 나타낼 전망입니다. 중국 병원 업그레이드 프로그램과 지역 CRC 스크리닝은 절차의 대응 가능성을 확대합니다. 일본의 초고령화 사회는 낮은 침습 접근을 의무화하고 인도의 장비 판매 행동 규범은 상업적인센티브와 윤리적 아웃리치의 균형을 추구합니다. 그러나, 상환의 편차와 가격 상한이 여전히 결정적인 채용의 발판이 되고 있어, 저렴한 가격을 타겟으로 한 단계적인 제품 포트폴리오를 강요하고 있습니다.

유럽은 일관된 MDR 프레임워크와 견고한 임상 네트워크를 지원하여 한 자릿수 중반의 꾸준한 성장을 보여줍니다. ESGE가 표준화한 교육은 운영자의 숙련도를 높이고 국경을 넘어서는 데이터 공유는 기술 평가 사이클을 가속화합니다. 라틴아메리카와 중동 및 아프리카는 신흥 지역이며 인프라 확장과 민간 병원 투자로 고도 내시경 검사에 대한 길이 열리고 있지만, 환율 변동과 세분화 된 보험이 즉각적인 보급을 방해하고 있습니다.

The gastrointestinal stent market generated USD 587.80 million in 2025 and is projected to reach USD 763.61 million by 2030, reflecting a CAGR of 5.37% over the forecast window.

Rising gastrointestinal (GI) cancer prevalence, a decisive clinical pivot toward minimally invasive endoscopy, and sustained advances in stent design-especially biodegradable and drug-eluting formats-anchor this expansion. Broader use of endoscopic ultrasound (EUS) and artificial-intelligence-guided planning has lowered technical barriers, improved patient-specific customization, and widened procedural suitability, especially for complex pancreaticobiliary disease. North America maintains volume leadership, yet high incidence of colorectal cancer and rapidly modernizing hospital networks position Asia-Pacific as the fastest-advancing region. Robust clinical evidence highlighting cost savings, shorter recovery times, and high patency levels reinforces payer acceptance and accelerates adoption across both malignant and benign indications.

Colorectal cancer incidence in Asia climbed to 23.88 per 100,000 population in 2024, overtaking stomach cancer as the dominant GI malignancy and creating sustained demand for colonic stents as bridge-to-surgery aids. Self-expandable metal stents now achieve 89.7% clinical success for malignant gastric outlet obstruction, delivering durable patency and fewer emergency surgeries.Integration of neoadjuvant chemotherapy with stent placement optimizes tumor shrinkage and surgical outcomes, further strengthening procedure volumes. Broadening cancer screening initiatives coupled with improved survival rates sustains procedure frequency into follow-up and palliative contexts.

Demographic ageing increases benign biliary strictures and pancreatitis-related complications, conditions often unsuitable for open surgery. Short fully covered metal stents resolve 99% of benign strictures in older cohorts, while lowering procedural risk and hospital stay relative to surgery.Enhanced anti-migration features address fragile tissue architecture common in geriatric patients. Health systems seeking value-based care favor these minimally invasive routes, reinforcing long-term utilization across mature markets.

FDA reports list stent positioning issues (35.6%) and migration events (12.4%) as leading device complaints, with hemorrhage and perforation topping patient-related events. Migration rates can approach 40%, raising cost and patient-safety concerns. Forgotten plastic biliary stents increase cholangitis risk and clogging incidents, prompting calls for automated retrieval reminders. Next-generation anti-migration fins and biodegradable formats aim to cut secondary procedures and enhance quality metrics.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Biliary stents held 37.23% share of 2024 revenues in the gastrointestinal stent market, reflecting their entrenched role in malignant and benign biliary obstructions. Laser-cut geometries, hydrophilic coatings, and low-profile delivery catheters foster accurate placement in narrowed ducts and complex hilar lesions. Esophageal and duodenal stents follow in volume, benefitting from improved anti-reflux valves that enhance dysphagia relief.

Colonic stents supply the fastest 8.94% CAGR through 2030. Comparative studies show self-expandable metal stents deliver survival and quality-of-life outcomes on par with emergent surgery while avoiding colostomy formation. Pancreatic designs without internal flaps record 80.7% spontaneous migration, sparing retrieval procedures and aligning with outpatient protocols. Drug-eluting refinements now target tissue in-growth inhibition, signaling new value propositions across all product classes.

Self-expanding metal devices captured 61.67% of 2024 revenue, underlining their balance of radial strength and flexibility. Clinical trials confirm 100% technical success for ileocecal obstruction and 92.3% clinical success, validating adaptability outside the traditional left-sided colon. Advanced nitinol processing, including laser-cut micro-mesh patterns, improves conformability across tortuous anatomy.

Biodegradable and drug-eluting formats, posting an 8.79% CAGR, answer the call for temporary scaffolding without removal. Iron-based prototypes enhance mechanical reserve while enabling radiopacity tracking. Hybrid constructs bring metallic backbone reliability alongside timed degradation, promising to shift indication boundaries for benign disease management. Plastic remains relevant for short-term drainage when retrieval is planned early, preserving a niche position in the gastrointestinal stent market.

Gastrointestinal Stent Market Report is Segmented by Product Type (Biliary Stent, Colonic Stent and More), Material (Self-Expanding Metal Stent, Plastic Stent and More), Application (Biliary Disease, Colorectal Cancer and More), End User (Hospitals, Ambulatory Surgical Centers and More) and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 35.47% of 2024 turnover, buoyed by established reimbursement pathways and deep procedural expertise. Medicare's defined coverage for GI stenting underpins predictable payment cycles, while manufacturer-driven registries furnish real-world evidence that speeds payer updates. United States centers emphasize multidisciplinary tumor boards integrating stenting, chemotherapy, and surgery, sustaining mature demand. Canada's universal insurance similarly ensures equitable access, fostering stable baseline volumes.

Asia-Pacific delivers the fastest 8.23% CAGR through 2030, propelled by aging demographics, growing colorectal cancer incidence, and expanded public insurance. China's hospital upgrade program and regional CRC screening widen procedural addressability. Japan's super-aged population mandates minimally invasive approaches, while India's device-marketing code of conduct seeks to balance commercial incentives with ethical outreach. Reimbursement variability and price caps, however, remain decisive adoption throttles, compelling tiered product portfolios targeting affordability.

Europe displays steady mid-single-digit growth underpinned by harmonized MDR frameworks and robust clinical networks. ESGE-standardized training expands operator proficiency, while cross-border data sharing accelerates technology assessment cycles. Latin America and Middle East & Africa constitute emerging arenas; infrastructure expansion and private-sector hospital investment create runway for advanced endoscopy, yet currency volatility and fragmented insurance dampen immediate penetration.