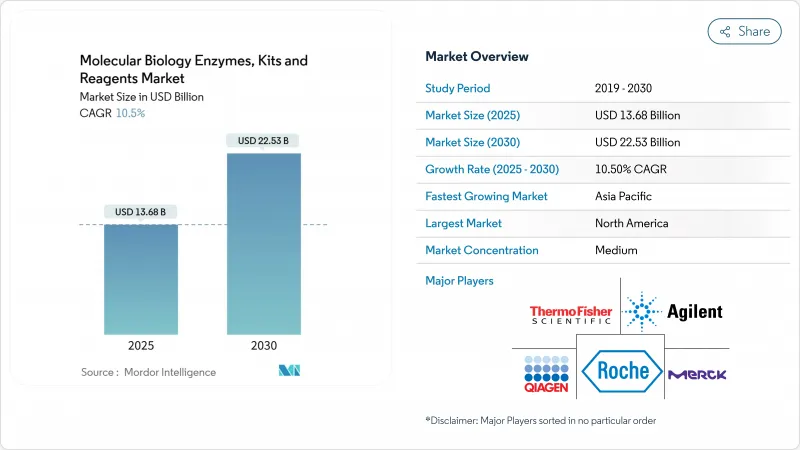

분자생물학용 효소, 키트 및 시약 시장은 2025년에 136억 8,000만 달러로 평가되며, CAGR 10.5%를 나타내 2030년에는 225억 3,000만 달러에 달할 것으로 예상됩니다.

차세대 시퀀싱 플랫폼 업그레이드, 싱글셀 멀티오믹스 분석의 임상 채용 확대, 현장 전개 가능한 동결건조 진단제로의 변화가 이 시장을 강력하게 견인하고 있습니다. 초고충실도 효소의 혁신은 분석 정밀도를 높이고 희귀 돌연변이의 검출을 가능하게 하며 CRISPR 기반 치료 파이프라인을 지원합니다. 동시에 북미와 유럽 연방 정부의 연구 개발비의 지속적인 지출과 아시아태평양의 생명 과학 투자의 활성화로 고가치 소모품의 고객 기반이 확대되고 있습니다. 경쟁사 간의 적대관계는 대기업 공급업체들이 샘플 준비, 증폭, 검출, 데이터 분석 능력을 통합하기 위한 전략적인수를 추구하는 한편, 중소의 전문업체가 지속 가능한 소모품이나 머신러닝에 의한 효소공학 분야에서 기회를 보고 있기 때문에 격화하고 있습니다.

COVID-19는 신속한 핵산 검사의 가치를 강조하여 mpox 검출로 96.1%의 감도를 달성한 동결건조 LAMP 기반의 Dragonfly 시스템과 같은 휴대용 분자 플랫폼에 대한 수요를 가속화했습니다. 의료 시스템은 현재 조기 분자 감시가 아웃 브레이크 억제 및 비용 관리에 필수적인 것으로 간주하고 있습니다. 신생아의 유전자이상 스크리닝과 집단 수준의 보인자 검사의 확대에는 희귀한 변이체를 검출하기 위한 에러율이 매우 낮은 효소가 필요합니다. CRISPR 기반 검출 화학물질 및 마이크로플루이딕스 카트리지가 최전선 검사실에 도입되어 고가치 시약의 대응 시장이 확대되고 있습니다.

2025년 설문조사에 따르면 일부 자본설비가 평평했음에도 불구하고 전체 학술예산은 4% 증가하여 회전율이 높은 소모품에 대한 경사를 보였습니다. 수탁 연구 기관이 대량 공급 계약을 획득하는 경향이 강해지고 있으며, 벤더는 커스터마이즈된 마스터 믹스와 지속 가능한 패키지 키트를 제공하게 되었습니다.

Medicare의 MolDX 프로그램은 엄격한 임상적 유용성 임계값을 사용하기 때문에 많은 새로운 분석법은 발견되지 않았거나 비용을 낮추고 있습니다. 민간 보험 회사는 현재 실제 증거를 요구하고 있으며 검사 시작에 시간과 비용이 듭니다. 소규모 실험실은 다시설 시험에 자금을 공급하는 데 어려움을 겪고 있으며, 지급자가 증거 기준을 조화시킬 때까지 기술 혁신이 제한됩니다.

보고서에서 분석되는 기타 성장 촉진요인과 억제요인

키트 및 시약은 2024년 매출의 65.52%를 차지하며 일상적인 워크플로우에서 소모품임을 뒷받침했습니다. 효소의 부분은 작지만 연구자가 단일 셀 시퀀싱에 대한 초고충실도 폴리머라제를 요구하고 있기 때문에 CAGR 12.25%를 나타낼 전망입니다. DNA 폴리머라제는 매일 1,000만 개의 변이체를 분석할 수 있는 스크리닝 플랫폼에 의해 강화되고 여전히 지배적인 효소 클래스입니다. 분자생물학용 효소, 키트 및 시약 시장 규모에서는 타카라 바이오의 변이형 T7 RNA 폴리머라제가 이중 가닥 RNA를 90% 절단하여 mRNA 치료제의 품질 요구에 대응합니다.

PCR 마스터 믹스와 NGS 라이브러리 키트의 판매는 시약의 리더십을 확고하게합니다. 그러나 효소는 단일 아미노산을 조정하여 오류율을 반감시키고 CRISPR의 특이성을 향상시킬 수 있기 때문에 프리미엄 가격을 획득하고 있습니다. 머신러닝을 통한 진화를 통해 공급업체는 새로운 시퀀싱 화학에 가장 적합한 촉매를 조정할 수 있게 되어 분자생물학용 효소, 키트 및 시약 시장의 효소 슬라이스의 2자리 성장을 확실히 하고 있습니다.

PCR의 2024년 시장 점유율은 45.53%를 나타내 진단 및 품질보증의 편재성을 반영했습니다. 그러나 NGS는 유전체당 비용 저하와 종양학에서의 급속한 채용을 배경으로 CAGR 16.53%를 나타낼 전망입니다. 새로운 증폭 방법인 AMPLON은 정확도를 희생하지 않고도 런타임을 50% 단축하여 PCR의 신속한 스크리닝 범위를 넓히고 있습니다.

CRISPR 워크플로우는 분자생물학용 효소, 키트 및 시약 시장에서 가장 급성장하고 있는 틈새 분야이며, 대립유전자 특이적인 편집을 실시하는 Cas12a의 유전자 변이체가 그 원동력이 되고 있습니다. 후성 유전 분석 및 단백질 분석 키트는 멀티오믹스 연구가 급증함에 따라 통합 시약 번들의 교차 판매 가능성을 창출하여 견인 역할을 하고 있습니다.

북미는 2024년 매출액의 38.82%를 차지하며, NIH와 NSF의 보조금 라인이 학술실과 임상실의 시약 소비를 지원했습니다. MolDX의 장애물에도 불구하고 분자검사에 대한 상환이 호조로 병원의 처리능력이 높게 유지되고 미국의 신흥기업은 신규 효소의 스핀아웃을 계속해 지역의 리더십을 유지하고 있습니다.

유럽은 한 자릿수 중반의 꾸준한 성장을 기록했습니다. IVDR 기반 규제 강화로 검증된 키트 구성요소에 대한 수요가 증가하고 있으며 CE-IVD 표준을 준수하는 성능을 문서화할 수 있는 공급업체가 이익을 얻고 있습니다. 항균제 내성 감시에 투자하면 한 번의 실행으로 수천 개의 반응이 가능한 고밀도 qPCR 시스템이 전개되어 시약 풀스루에 박차를 가하고 있습니다.

아시아태평양은 CAGR 11.32%를 나타내 가장 빠른 속도로 추이하고 있습니다. 중국은 2023년 의약품 및 디바이스 신청 건수가 35.84% 급증해 IVD 시약이 신청 건수의 1/4 가까이를 차지했습니다. 일본에서는 임상검사실 개발검사의 틀이 재검토되어 국내의 이노베이터에 있어서 명확한 것이 되고 있습니다. 한국의 단계적 승인 패스웨이는 저위험 분자 분석을 가속화하고 시장 접근을 확대합니다. APAC의 공중위생기관도 농촌의 진료소용으로 현장 배치 가능한 진단약에 투자하고 있으며, 분자생물학용 효소, 키트 및 시약 시장 규모에서 동결건조 포맷의 보급을 가속화하고 있습니다.

중동 및 아프리카는 현재 규모는 작지만 키트의 현지화를 의무화하는 국가 유전체학 프로그램을 추진하고 있으며 장기적인 상승을 시사하고 있습니다. 라틴아메리카에서는 환율 변동이 지출주기를 완만하게 하는 것, 질병 감시 캠페인과 관련된 조달이 급증하고 있습니다.

The molecular biology enzymes, kits & reagents market is valued at USD 13.68 billion in 2025 and is forecast to reach USD 22.53 billion by 2030, reflecting a 10.5% CAGR.

Strong momentum comes from next-generation sequencing platform upgrades, growing clinical adoption of single-cell multi-omics assays, and the shift toward field-deployable, lyophilized diagnostics. Ultra-high-fidelity enzyme innovations are raising analytical precision, enabling detection of rare mutations and supporting CRISPR-based therapeutic pipelines. At the same time, sustained federal R&D spending in North America and Europe, coupled with intensified life-science investment in Asia-Pacific, is enlarging the customer base for high-value consumables. Competitive rivalry is intensifying as large suppliers pursue strategic acquisitions to integrate sample preparation, amplification, detection, and data-analysis capabilities, while smaller specialists stake out opportunities in sustainable consumables and machine-learning-guided enzyme engineering.

COVID-19 highlighted the value of rapid nucleic-acid testing, accelerating demand for portable molecular platforms such as a lyophilized LAMP-based Dragonfly system that achieved 96.1% sensitivity for mpox detection. Health systems now view early molecular surveillance as essential for outbreak containment and cost control. Expanded newborn genetic-disorder screening and population-level carrier testing require enzymes with extremely low error rates to spot rare variants. CRISPR-based detection chemistries and microfluidic cartridges are entering frontline laboratories, enlarging the addressable market for high-value reagents.

A 2025 survey showed overall academic research budgets rising 4%, even as some capital-equipment lines stayed flat, signaling a tilt toward high-turnover consumables. Contract research organizations increasingly win bulk-supply agreements, encouraging vendors to offer customized master mixes and sustainably packaged kits.

Medicare's MolDX program uses stringent clinical-utility thresholds, leaving many novel assays uncovered or reimbursed below cost. Private insurers now demand real-world evidence, adding time and expense to test launches. Smaller labs struggle to fund multi-site trials, constraining innovation until payers harmonize evidence standards.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Kits & reagents contributed 65.52% of 2024 revenue, underlining their consumable nature in routine workflows. The enzymes portion, though smaller, is climbing at 12.25% CAGR as researchers demand ultra-high-fidelity polymerases for single-cell sequencing. DNA polymerases remain the dominant enzyme class, bolstered by a screening platform that can assay 10 million variants daily. Within the molecular biology enzymes, kits & reagents market size, Takara Bio's mutant T7 RNA polymerase cuts double-stranded RNA by 90%, addressing mRNA-therapeutics quality needs.

Recurrence-driven revenue from PCR master mixes and NGS library kits cements reagent leadership. Yet enzymes capture premium pricing because single-amino-acid tweaks can halve error rates and improve CRISPR specificity. Machine-learning-aided evolution lets vendors tailor catalytic optima to new sequencing chemistries, ensuring double-digit growth for the enzymes slice of the molecular biology enzymes, kits & reagents market.

PCR held 45.53% market share in 2024, reflecting ubiquity in diagnostics and QA. However, NGS is expanding at 16.53% CAGR on the back of falling per-genome costs and rapid oncology adoption. A new amplification method, AMPLON, shortens run time 50% without sacrificing accuracy, widening PCR's reach into rapid screening.

CRISPR workflows are the fastest-growing niche inside the molecular biology enzymes, kits & reagents market, fueled by engineered Cas12a variants that deliver allele-specific edits. Epigenetics assays and protein-analysis kits also gain traction as multi-omic studies proliferate, creating cross-selling potential for integrated reagent bundles.

The Molecular Biology Enzymes, Kits & Reagents Market Report is Segmented by Product (Enzymes, Kits and Reagents), Application (Polymerase Chain Reaction, Next-Generation Sequencing, and More), End Users (Hospitals and Diagnostic Centers, Academic and Research Institutes, and More), Form (Liquid, and Lyophilized), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 38.82% of 2024 revenue, anchored by NIH and NSF funding lines that sustain reagent consumption across academic and clinical labs. Strong reimbursement for molecular tests, despite MolDX hurdles, keeps hospital throughput high, and U.S. start-ups continue to spin out novel enzymes, maintaining regional leadership.

Europe posted steady mid-single-digit growth. Regulatory alignment under IVDR is driving demand for validated kit components, benefiting suppliers able to document performance to CE-IVD standards. Investment in antimicrobial-resistance surveillance has led to rollout of high-density qPCR systems capable of thousands of reactions per run, spurring reagent pull-through.

Asia-Pacific registers the fastest trajectory at 11.32% CAGR. China recorded a 35.84% jump in drug and device filings in 2023, with IVD reagents comprising nearly one-quarter of submissions. Japan is revising laboratory-developed-test frameworks, giving clarity to local innovators. South Korea's tiered approval pathway expedites low-risk molecular assays, widening market access. APAC public-health agencies also invest in field-deployable diagnostics for rural clinics, accelerating uptake of lyophilized formats within the molecular biology enzymes, kits & reagents market size.

The Middle East & Africa are smaller today but pursue national genomics programs that mandate kit localization, signaling long-run upside. Latin America sees procurement spikes tied to disease-surveillance campaigns, though currency volatility moderates spending cycles.