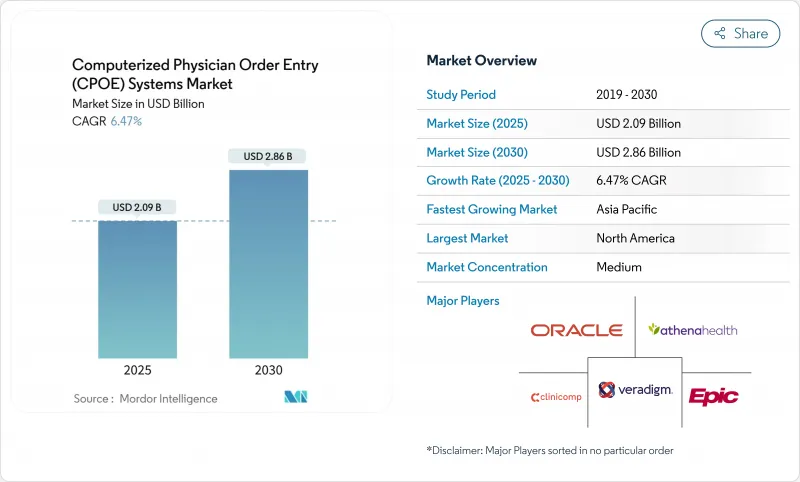

세계의 CPOE(Computerized Physician Order Entry Systems) 시스템 시장은 2025년 20억 9,000만 달러에 이르고, 2030년에는 28억 6,000만 달러로 확대될 것으로 예측됩니다.

연방정부에 의한 강력한 의무화, 어카운터블 케어의 약정 확대, 급속히 성숙하는 인공지능형 의사결정 엔진이 결합되어 입원환자와 외래환자의 모든 환경에서의 도입이 가속화되고 있습니다. 에픽 시스템즈가 2024년 말까지 모든 고객 사이트를 Trusted Exchange Framework 및 Common Agreement에 링크시킨 것은 상호 운용성에 대한 기대에 새로운 기준을 설정하는 것이었지만, Oracle 헬스가 외래 점유율 25.06%에서 23.1%를 나타내의 침체를 막으려고 분투하고 있다는 것은 데이터 교환 실적 지연이 경쟁에 미치는 영향을 보여주었습니다. 밸류 베이스 케어의 추진은 도입의 부담을 경감하는 클라우드 네이티브의 도입 모델과 함께, 비용면에서 압박되고 있는 의료 제공업체의 사이에서도 높은 투자 수준을 유지하고 있습니다. 종양과, 순환기과, 감염증과의 워크플로우에서는 AI가 작성한 주문 세트가 오류율을 줄이고 측정 가능한 품질을 향상시켜 CPOE가 순수한 트랜잭션 자산이 아니라 전략적 자산이라는 인식을 강화하고 있습니다.

연방규칙이 전자적인 주문과 임상 판단 지원의 사용과 상환을 직접 연관시키면서, 소극적인 의료 제공업체도 준거한 시스템을 도입하게 되었습니다. Medicare Promoting Interoperability 프로그램은 의미 있는 CPOE 사용을 입증할 수 없는 병원에서 최대 4%의 지불을 보류합니다. 동시에 21세기 치료법은 정보 차단을 금지하고 있으며, 공급업체는 타사 도구가 주문 시점에 구조화된 데이터를 검색할 수 있도록 표준화된 API를 공개해야 합니다. 규정 준수 기한이 24개월 이내에 집중되기 때문에 많은 의료 시스템은 계약 주기를 가속화하고 검증된 감사 추적 및 TEFCA 연결이 있는 공급업체를 선호합니다. 또한 대규모 그룹은 여러 시설에 걸친 인증을 간소화하기 위해 기업 전체의 라이선스를 협상하고 있으며 의사 CPOE(Computerized Physician Order Entry Systems) 시스템 시장의 기존 리더들이 이미 누리고 있는 규모의 우위를 강화하고 있습니다.

의료 기관은 On-Premise 하드웨어를 폐지하고 자본 지출을 예측 가능한 운영 비용으로 향하는 구독 모델로 전환하고 있습니다. Epic이 최근에 시작한 완전 관리형 호스팅 옵션을 통해 병원 체인은 자체 데이터센터를 구축하지 않고도 완전한 주문 엔트리 스택을 도입할 수 있습니다. Oracle 헬스도 마찬가지로 포트폴리오를 멀티 테넌트 클라우드로 마이그레이션했습니다. 클라우드 아키텍처는 긴 버전 업 사이클을 제거하고 공급업체가 몇 시간 안에 보안 패치를 제공할 수 있게 하고, 전문 분야에 특화된 주문형 라이브러리와 같은 마이크로서비스 애드온에 대한 문을 엽니다. 인터시스템즈의 클라우드 네이티브 IntelliCare 네트워크로 대표되는 바와 같이, 동일한 인프라가 전국 수준의 의료 정보 교환을 지원합니다. 사이버리스크가 높은 보험사가 최신 소프트웨어와 불변 백업을 추구하고 있기 때문에 CIO는 클라우드 채용을 재량적인 프로젝트가 아니라 회복에 필요한 것으로 자리매김하고 있으며 CPOE(Computerized Physician Order Entry Systems) 시스템 시장의 거의 모든 하위 부문에서 매출을 늘리고 있습니다.

서버에 대한 지출이 감소하고 있는 것, 레거시 프로세스 매핑, 수식 조정, 다직종 팀 교육 등 인적 자본 부담이 크므로 소규모 또는 지방 의료 기관의 경우 프로젝트의 총 예산이 어려워지고 있습니다. 많은 조직은 현금 흐름의 부담을 줄이기 위해 부서 간의 롤아웃을 어긋나지만, 단계적 가동은 보안 이점의 실현을 늦추고 인터페이스 유지보수를 복잡하게 합니다. HL7-FHIR의 전문가가 제한되어 있기 때문에 특히 의료 IT 노동력이 미숙한 신흥 시장에서는 컨설팅 비용이 더욱 상승하고 일정이 장기화됩니다. 상업 금융 기관은 여전히 대규모 CPOE 전환을 위험시하고 있기 때문에 병원 이사회는 자금 갭을 채우기 위해 공동 구매 얼라이언스와 공적 보조금의 공동 출자를 요구하는 경우가 많습니다. 이러한 재정적 및 자원적 장애물은 "긴 꼬리"공급자에 대한 침투를 지연시키고 CPOE(Computerized Physician Order Entry Systems) 시스템 시장의 견조한 성장 전망에서 약간의 포인트를 깎을 것입니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

클라우드 및 웹 호스팅 솔루션은 2024년 수익의 65.45%를 창출하여 의사 CPOE(Computerized Physician Order Entry Systems) 시스템 시장에서 탄력적 아키텍처의 이점을 강화했습니다. 병원은 계절적인 서지 및 자동 패치 적용에 대응하는 확장 가능한 용량을 중시하고, 여러 거점을 가진 IDN은 지역을 가로지르는 통일된 거버넌스 대시보드를 높이 평가했습니다. 이와는 대조적으로, On-Premise 계약은 점유율이 감소한 것, CAGR7.12%와 가장 빠른 페이스로 추이하고 있습니다. 이는 데이터 주권 관련 법률에 따라 유럽 및 걸프 제공업체가 기밀 정보를 국경 내에 유지하도록 요구되기 때문입니다. 2024년 11월에 시행된 프랑스의 의료 데이터 호스팅 규칙은 프로덕션 데이터베이스가 EEA 범위를 벗어나지 않는지 확인하도록 시설에 의무화되어 있으며, 분석 노드를 로컬 랙에 연결하는 프라이빗 클라우드와 하이브리드 모델의 틈새를 지원합니다.

퍼블릭 클라우드에서 프론트엔드 주문 화면을 스트리밍하면서 법적 보관을 위해 사내 아카이브에 미러링하는 하이브리드 토폴로지는 일반적인 타협으로 부상하고 있습니다. 공급업체는 컨테이너화된 마이크로서비스를 지원하고 코드를 포크하지 않고 모드를 전환할 수 있으므로 검증 오버헤드를 최소화할 수 있습니다. 이러한 유연한 배치의 청사진은 이전에 노후화된 모노리스에 갇혀 있던 중견 시장 병원의 벤더 선택 장벽을 낮추고 도달 가능한 의사 CPOE(Computerized Physician Order Entry Systems) 시스템 시장 전체를 확장합니다.

이 소프트웨어는 2024년 지출액의 51.66%를 차지했으며, 이는 지속적인 라이선스 업데이트 및 기능 세트를 최신으로 유지하기 위한 모듈의 점진적인 업그레이드 때문입니다. 그러나 서비스 라인(구현, 최적화, 사용자 경험 재설계)은 코어 코드가 아닌 구성 선택이 측정 가능한 성과 향상을 좌우하는 경우가 많다는 경영진의 인식으로 연간 7.23% 증가하고 있습니다. CEO는 분기별 경보 거버넌스 검토, 항균제, 스튜어드십, 오더셋 튜닝, AI 바이어스 감사에 대한 예산을 점점 늘리고 서비스를 연금으로 바꾸고 있습니다.

하드웨어 수요는 모바일 카트, 러기드 태블릿, Wi-Fi 6E 네트워크 장비에 중점을두고 있으며 침대 옆에서의 액세스가 중단되지 않습니다. 클라우드를 채택하면 로컬 서버 룸이 필요하지 않으므로 시설은 자본을 랙에서 엔드포인트 장치로 향하게 하여 사용자 인터페이스 응답성 장애물을 높입니다. 서비스 편중의 전달 모델은 정착성을 향상시켜 공급자가 상시 이용할 수 있는 컨설팅을 다년간의 구독층에 번들하는 동기부여가 되어, CPOE(Computerized Physician Order Entry Systems) 시스템 시장 전체의 평생 고객 가치를 높이는 변화가 됩니다.

북미는 2024년 매출의 42.56%를 차지하며 엄격한 메디케어 인센티브, 성숙한 광대역 연결, 깊은 벤더 실적가 요인이 되었습니다. 이 지역의 의사 CPOE(Computerized Physician Order Entry Systems) 시스템 시장 규모는 2030년에는 12억 1,000만 달러에 달할 것으로 예측되며, 고객을 다중 사이클 관계로 고정하는 AI 풍부한 모듈 업그레이드를 통해 리더십을 유지하고 있습니다. 지속적인 TEFCA 배포는 '전국 의료 IT 백본'을 제공하여 소규모 지역 병원이 맞춤형 인터페이스 없이 3차 의료 센터와 상호 운용될 수 있도록 합니다.

아시아태평양은 CAGR이 가장 빨리 7.43%를 나타내 성장을 지속하고 있으며, 이는 현재 3억 건의 장기 건강 기록을 연결하고 있는 인도의 아유슈만 바랏 디지털 미션과 같은 대규모 공공 부문의 디지털화 보조금에 의해 지원되고 있습니다. 싱가포르의 협조적인 IoT 전략은 모든 공공 병동 내에 안전한 Wi-Fi 엔드포인트를 설치하고 휴대용 무선 주문 입력을 위한 길을 열고 있습니다. 태국 지역의 원격 약국 간이 건축물은 의사의 주문을 지역 창고에 자동으로 전송하여 CPOE 기능이 물리적인프라 제약을 극복하는 방법을 보여줍니다. 이러한 종합적인 확대는 시설 당 예산이 겸손하더라도 전체 지역의 지출을 증가시킵니다.

유럽, 중동, 라틴아메리카, 아프리카는 함께 한 자리 대 중반의 꾸준한 성장을 보여줍니다. EU와 GCC는 소블린 클라우드의 지시에 따라 다국적 기업과 통합하는 현지 호스팅 파트너를 활성화하고 있습니다. 중동에서는 2028년까지 79억 달러를 의료 IT 업그레이드에 충당할 계획으로, 그 대부분을 신설의 제3차 의료시설 내의 전자 처방과 오더 세트 엔진에 충전하려고 하고 있습니다. 라틴아메리카의 각 부처는 공립 병원 재건시 CPOE 도입에 자금을 제공하기 위해 다자간 은행과 양허 대출을 협상하고 있습니다. 이 파이프라인은 거시 경제적인 역풍이 완화되면 의사 CPOE(Computerized Physician Order Entry Systems) 시스템 시장을 가속화할 수 있습니다.

The global Computerized Physician Order Entry (CPOE) Systems market stands at USD 2.09 billion in 2025 and is forecast to advance to USD 2.86 billion by 2030, translating into a 6.47% CAGR over the period.

Robust federal mandates, expanding accountable-care arrangements, and fast-maturing artificial-intelligence decision engines are together accelerating adoption across inpatient and ambulatory settings. Epic Systems' plan to link every client site with the Trusted Exchange Framework and Common Agreement by year-end 2024 sets a new baseline for interoperability expectations, while Oracle Health's struggle to stem a 25.06% to 23.1% ambulatory share slide illustrates the competitive repercussions of lagging data-exchange performance. The push toward value-based care, coupled with cloud-native deployment models that ease implementation burdens, keeps investment levels high even among cost-pressured providers. Across oncology, cardiology, and infectious-disease workflows, AI-curated order sets are reducing error rates and driving measurable quality gains, reinforcing the perception of CPOE as a strategic rather than purely transactional asset.

Federal rules now link reimbursement directly to electronic ordering and clinical-decision-support usage, pushing even reluctant providers to deploy compliant systems. The Medicare Promoting Interoperability Program withholds up to 4% of payments from hospitals that fail to demonstrate meaningful CPOE use. Simultaneously, the 21st Century Cures Act bars information blocking, forcing vendors to publish standardized APIs that let third-party tools pull structured data at the point of order. Because compliance deadlines cluster within 24 months, many health systems accelerate contracting cycles, favoring suppliers with proven audit trails and TEFCA connectivity. Large groups also negotiate enterprise-wide licenses to streamline attestation across multiple facilities, reinforcing the scale advantages already enjoyed by the incumbent leaders in the Computerized Physician Order Entry (CPOE) Systems market.

Providers are shedding on-premise hardware in favor of subscription models that shift capital outlays toward predictable operating expenses. Epic's recently launched fully managed-hosting option enables hospital chains to deploy the complete order-entry stack without building their own data centers. Oracle Health likewise pivoted its portfolio to a multi-tenant cloud after high-profile implementation setbacks. Cloud architectures eliminate lengthy version-upgrade cycles, let suppliers roll out security patches in hours, and open the door to micro-service add-ons such as specialty-specific order-set libraries. The same infrastructures underwrite national-level health-information exchanges, exemplified by InterSystems' cloud-native IntelliCare network that shares medication orders across disparate facilities. As cyber-risk insurers increasingly require up-to-date software and immutable backups, CIOs frame cloud adoption as a resilience necessity rather than a discretionary project, boosting bookings across nearly every sub-segment of the Computerized Physician Order Entry (CPOE) Systems market.

Despite falling server expenditures, the human-capital intensity of mapping legacy processes, reconciling formularies, and training multidisciplinary teams keeps total project budgets daunting for small or rural institutions. Many organizations stagger roll-outs across departments to soften cash-flow strain, yet staged go-lives elongate realization of safety benefits and complicate interface maintenance. Limited pools of HL7-FHIR specialists further inflate consulting rates and extend timelines, particularly in emerging markets with nascent health-IT labor forces. Commercial lenders still view large-scale CPOE conversions as risky, so hospital boards often seek joint-purchasing alliances or public-grant co-funding to bridge financing gaps . These financial and resource hurdles slow penetration among the "long-tail" of providers and shave incremental points from the otherwise robust growth outlook for the Computerized Physician Order Entry (CPOE) Systems market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cloud and web-hosted solutions generated 65.45% of 2024 revenue, reinforcing the primacy of elastic architectures in the Computerized Physician Order Entry (CPOE) Systems market. Hospitals emphasize scalable capacity for seasonal surges and automatic patching, while multi-site IDNs appreciate unified governance dashboards that span geographies. In contrast, on-premise contracts, though a diminished share, clock the quickest 7.12% CAGR as data-sovereignty statutes push some European and Gulf providers to retain sensitive information within national borders. French Health-Data-Hosting rules effective November 2024 compel facilities to verify that production databases never exit the EEA, sustaining a niche for private-cloud or hybrid models that tether analytics nodes to local racks.

A hybrid topology-front-end order screens streamed over public cloud yet mirrored to an in-house archive for legal holding-emerges as a common compromise. Vendors respond with containerized micro-services that can flip between modes without code forks, minimizing validation overhead. These flexible deployment blueprints lower vendor-selection barriers for mid-market hospitals previously locked into aging monoliths, broadening the total reachable Computerized Physician Order Entry (CPOE) Systems market.

Software retained 51.66% of 2024 spending, owing to perpetual license renewals and incremental module upgrades that keep feature sets current. Yet service lines-implementation, optimization, user-experience redesign-advance 7.23% per year as executives realize that configuration choices, not core code, often dictate measurable outcome gains. Chief medical information officers increasingly budget for quarterly alert-governance reviews, antimicrobial-stewardship order-set tuning, and AI bias audits, turning services into an annuity.

Hardware demand now centers on mobile carts, rugged tablets, and Wi-Fi 6E network gear that ensure uninterrupted bedside access. Because cloud adoption removes local server rooms, facilities redirect capital from racks to endpoint devices, which in turn raises the bar for user-interface responsiveness. The service-heavy delivery model improves stickiness, motivating suppliers to bundle evergreen consulting in multi-year subscription tiers, a shift that inflates lifetime customer value across the Computerized Physician Order Entry (CPOE) Systems market.

The Computerized Physician Order Entry (CPOE) Systems Market is Segmented by Delivery Mode (Web-Based and Cloud-Based, and More), Component (Software, Hardware, and More), Type (Integrated CPOE and Stand-Alone CPOE), End User (Hospitals and Clinics, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America commands 42.56% of 2024 revenue, attributable to stringent Medicare incentives, mature broadband connectivity, and deep vendor footprints. The Computerized Physician Order Entry (CPOE) Systems market size for the region is projected to close 2030 at USD 1.21 billion, sustaining leadership through AI-rich module upgrades that lock customers into multi-cycle relationships. Continuous TEFCA rollouts provide a "nationwide health-IT backbone," allowing smaller community hospitals to interoperate with tertiary centers without bespoke interfaces.

Asia-Pacific logs the quickest 7.43% CAGR, underwritten by large public-sector digitization grants such as India's Ayushman Bharat Digital Mission, which now links 300 million longitudinal health records. Singapore's concerted IoT strategy places secure Wi-Fi endpoints inside every public ward, paving the way for wireless order entry on handhelds. Thailand's rural tele-pharmacy kiosks automatically transmit physician orders to provincial warehouses, showcasing how CPOE functionality can leapfrog physical-infrastructure constraints. This inclusive expansion lifts total regional spending even where per-facility budgets remain modest.

Europe, the Middle East, Latin America, and Africa together provide steady mid-single-digit growth. Sovereign-cloud mandates in the EU and GCC energize local hosting partners that integrate with multinational suites. The Middle East's plan to allocate USD 7.9 billion to health-IT upgrades by 2028 directs a significant tranche to e-prescribing and order-set engines within new tertiary campuses. Latin American ministries negotiate concessional financing with multilateral banks to fund CPOE rollouts inside public hospital rebuilds, a pipeline that could accelerate the Computerized Physician Order Entry (CPOE) Systems market once macro-economic headwinds ease.