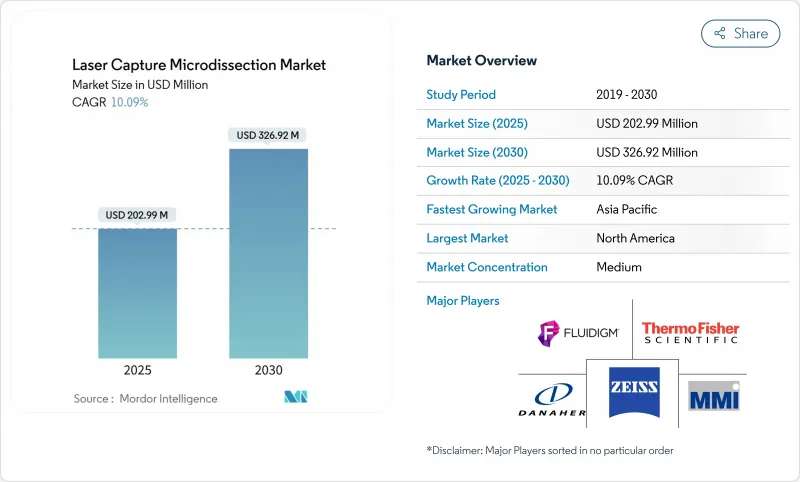

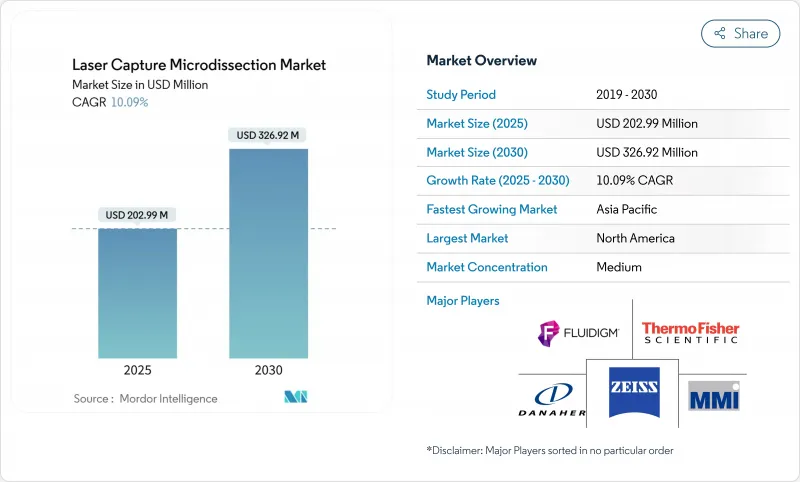

레이저 캡처 현미해부 시장 규모는 2025년에 2억 299만 달러로 추정되고, 2030년에는 3억 2,692만 달러에 달할 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 10.09%를 나타낼 전망입니다.

이 기술이 병리조직학과 분자생물학을 결합하여 과학자가 멀티오믹스 연구의 공간적 배경을 지키면서 정확한 세포군을 추출할 수 있게 됨에 따라 수요가 급증합니다. 인공지능은 현재 공간 생물학 워크플로우에 통합되어 실험실이 대상 인식을 자동화하고 분석주기를 단축하는 데 도움이 됩니다. 제약 회사 및 생명 공학 회사는 레이저 캡처 현미해부 플랫폼을 도입하여 혼합 조직 절편에서 종양 세포를 분리하고 바이오 마커 탐색 및 약물 반응 프로파일 링을 가속화하고 있습니다. 소모품은 캡처 필름과 시약의 정기적인 구매가 높은 처리량 연구를 지원하기 때문에지지를 모으고 적외선 시스템은 DNA 및 단백질 취급에 친화적이기 때문에지지를 수집합니다. 아시아태평양은 중국, 일본, 인도의 정부 프로그램이 새로운 공간 오믹스 연구센터를 건설하고 있기 때문에 가장 빠른 확대를 기록하고 있습니다.

암과 신경 퇴행성 질환의 부담은 레이저 캡처 현미해부를 학술 및 상업 연구소의 스테디셀러로 만드는 자금 원에 박차를 가하고 있습니다. 중국과 일본의 보조금은 단일 세포 유전체학을 위한 이 기술에 의존하는 국가적 공간 오믹스의 허브를 지원합니다. 각 종양학 프로젝트는 일반적으로 종양 미세환경 매핑에서 치료 모니터링에 이르기까지 여러 단계로 레이저 캡처 현미해부를 반복합니다. 이 요구 사항은 현재 경쟁 의약품 파이프라인의 베팅으로 읽혀지고 있으며, 제약 스폰서는 연구 계약에 레이저 캡처 현미해부를 지정합니다. 이 안정적인 현금 흐름은 모든 주요 지역에서 장기적인 성장 전망을 지원합니다.

레이저 캡처 현미해부은 인접한 세포 사이의 누화의 위험이있는 수동 암컷 방법과는 달리 일관된 성공률로 오염이없는 절편을 만듭니다. 온전한 분자를 필요로 하는 단일 셀 전사체학로 실험실이 이동할 때 RNA 무결성을 유지하는 것이 중요합니다. 자동화는 운영자의 바이어스를 제거하고 재현성을 향상시키고 비용이 많이 드는 재실행을 줄입니다. 이미징 모듈은 형태 및 형광에 의한 세포 클러스터의 동정을 서브셀 해상도로 지원하여 수동 추출에서는 불가능했던 발생 생물학이나 질병 진행의 연구를 가능하게 합니다. 이러한 장점을 결합하면 워크플로우 시간이 단축되고 다운스트림 분석에 대한 신뢰도가 높아집니다.

완벽한 레이저 캡처 현미해부 워크스테이션은 50만 달러를 넘는 경우가 많으며 많은 중견 실험실에 손이 닿지 않습니다. 연간 서비스 계약은 구매 금액의 15-20%에 도달하고 레이저 교정 및 광학 시스템 교체를 다룹니다. 예산이 제한되어 있기 때문에 연구 기관은 기간 시설을 공유해야 하며 예약 일정이 늘어나 처리 능력이 저하됩니다. 신흥 시장의 대학에서는 조달주기에 시간이 걸리고, 조성금 경쟁력을 지지하는 설치가 늦어지고 있습니다. 부유한 지역에서도 소모품 및 데이터 분석에 대한 예산 재분배는 새로운 장비의 주문을 지연시킬 수 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

소모품은 가장 급성장하는 카테고리이며, 높은 처리량 파이프라인에는 캡처 필름, 슬라이드, 시약의 지속적인 공급이 필요하기 때문에 2030년까지 13.23%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되고 있습니다. 2024년 레이저 캡처 현미해부 시장 점유율은 44.35%였으나 구독 스타일의 주문 모델로의 전환은 장기적인 워크플로우의 일관성을 중시하는 구매층의 성숙을 보여줍니다. 소프트웨어 및 서비스는 매출이야말로 작은 것, 현미해부 하드웨어를 다운스트림 시퀀싱이나 바이오인포매틱스에 연결시키는 턴키 에코시스템을 구매자가 요구하게 되어 관련성을 늘리고 있습니다.

이 마이그레이션은 안정적인 소모품 수요를 통해 공급업체를 설치 기반에 고정하여 이익 풀을 확장합니다. 새로운 폴리머 멤브레인은 현재 특정 조직 등급에 맞게 접착력과 두께를 조정하여 포획 효율을 향상시키고 있습니다. 공급업체는 소모품에 RFID 태그를 추가하여 실험실이 배치 사용량을 추적하고 재주문을 자동화할 수 있도록 했습니다. 마이크로유체와 LCM의 하이브리드가 시장에 나오게 되면 완전히 새로운 카트리지 형태가 분리와 용해를 결합하여 제공되어 하드웨어와 소모품의 경계를 모호하게 하는 번들로 이루어진 수익 스트림이 가능해집니다.

자외선 시스템은 2024년에 52.11%의 수익을 올렸지만, 적외선 플랫폼은 하류 오믹스를 위해 DNA와 단백질을 보호하는 온화한 열 시그니처 덕분에 연간 15.61% 확대될 것으로 예측되고 있습니다. 적외선 장치는 또한 세포를 더 깨끗하게 캡처하기 때문에 오류가없는 라이브러리를 찾는 단일 셀 파이프라인에 적합합니다. UV 시스템은 현미해부를 기존 조직학과 결합하는 교육 병원과 같은 형태 보존이 필수적인 경우에 여전히 인기가 있습니다.

벤더는 자동화 깊이, 샘플 네비게이션 속도, 고 컨텐츠 이미지 분석과의 호환성 등으로 차별화를 도모하고 있습니다. 적외선 플랫폼은 낮은 출력 임계값에서 작동하고, 에지의 탄화를 차단하고, 포착률을 향상시킵니다. 한편, 레이저 현미해부의 압력 투과 시스템은 법의학에서 틈새 수요를 발견하고 비접촉 배출을 통해 미량 DNA 작업에서 오염 위험을 제거합니다. 이러한 진보로 레이저 캡처 현미해부 시장은 변화하는 연구의 우선순위에 대응하고 있습니다.

북미는 2024년에 레이저 캡처 현미해부 시장 점유율의 42.82%를 유지했고, 지속적인 국립위생연구소의 자금과 성숙한 의약품 R&D 클러스터에 지지를 받고 있습니다. 디지털 퍼솔로지의 보급은 워크플로우 통합을 간소화하고 AI 지원 현미해부은 노동 병목 현상을 줄여줍니다. 하지만 인원 부족과 상환 압력이 당면 성장을 억제합니다.

유럽은 정밀의료 연구를 지원하는 관민 협동 프로그램에 의해 2위의 지역이 되고 있습니다. 독일, 영국, 프랑스는 레이저 캡처 현미해부의 여러 핵심 시설을 보유하고 있으며 공유 허브로 운영되므로 장비 사용률이 향상되었습니다. 동반진단 약물의 규제 조화는 장비 제조업체가 현지 바이오 의약품 회사와 제휴하도록 권장합니다. 그러나 EU 회원국 간의 자금 조달 변동과 EU 이탈 후 연구 불확실성으로 인해 EU 전역에서의 도입률은 불균형합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 13.44%를 나타낼 전망입니다. 중국의 5개년 계획에서는 공간 생물학이 우선되어 대규모 연구소 건설과 대량 구매 계약이 진행되고 있습니다. 일본의 연구기관은 고충실도 적외선 현미해부에 의존하는 종양학과 신경변성 연구를 진행하고 있습니다. 인도의 위탁연구기관에서는 레이저 캡처 현미해부를 세계 의약품 스폰서의 서비스 메뉴에 추가하고 있지만, 인프라 격차와 인력 부족으로 인해 1급 도시 이외의 전개가 지연될 수 있습니다. 이 지역 전체의 투자는 평균을 초과하는 지속적인 확대를 시사합니다.

The Laser Capture Microdissection Market size is estimated at USD 202.99 million in 2025, and is expected to reach USD 326.92 million by 2030, at a CAGR of 10.09% during the forecast period (2025-2030).

Demand surges as the technology links histopathology to molecular biology, allowing scientists to extract precise cell groups while safeguarding spatial context for multi-omics studies. Artificial intelligence is now stitched into spatial biology workflows, helping laboratories automate target recognition and shorten analysis cycles. Pharmaceutical and biotechnology firms deploy laser capture microdissection platforms to isolate tumor cells from mixed tissue sections, accelerating biomarker discovery and drug-response profiling. Consumables gain traction because recurring purchases of capture films and reagents support high-throughput studies, while infrared systems win favor for gentler DNA and protein handling. Asia-Pacific records the fastest expansion as government programs in China, Japan, and India build new spatial-omics research centers, even as North America retains leadership through mature research funding and early AI adoption.

Cancer and neurodegenerative disease burdens spur funding streams that make laser capture microdissection a staple in academic and commercial labs. Chinese and Japanese grants bankroll national spatial-omics hubs that rely on the technique for single-cell genomics. Each oncology project typically loops laser capture microdissection into several stages, from tumor microenvironment mapping to therapy monitoring. The requirement now reads as table stakes for competitive drug pipelines, causing pharmaceutical sponsors to specify laser capture microdissection in research contracts. This steady cash flow underpins long-term growth prospects in every major region.

Laser capture microdissection produces contamination-free sections with consistent success, unlike manual scalpel methods that risk cross-talk between adjacent cells. Preservation of RNA integrity matters when labs shift toward single-cell transcriptomics requiring intact molecules. Automation removes operator bias and improves reproducibility, reducing costly re-runs. Imaging modules help scientists identify cell clusters by morphology or fluorescence at sub-cellular resolution, enabling studies in developmental biology and disease progression once impossible with manual extraction. These combined benefits shorten workflow times and raise confidence in downstream analytics.

Full laser capture microdissection workstations often top USD 500,000, placing them beyond reach for many mid-tier labs. Annual service contracts reach 15-20% of purchase value, covering laser calibration and optics replacement. Limited budgets force institutions to share core facilities, stretching booking schedules and lowering throughput. Emerging-market universities find procurement cycles lengthy, delaying installations that could support grant competitiveness. Even in wealthier regions, budget reallocations toward consumables and data analysis sometimes slow new equipment orders.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Consumables are the fastest rising category, projected to climb at a 13.23% CAGR through 2030 as high-throughput pipelines require continuous supplies of capture films, slides, and reagents. Instruments retained a 44.35% laser capture microdissection market share in 2024, yet the shift to subscription-style ordering models signals a maturing buyer base focused on long-term workflow consistency. Software & services, though smaller in sales, gain relevance as buyers seek turnkey ecosystems that link microdissection hardware to downstream sequencing and bioinformatics.

This transition widens profit pools by anchoring vendors to installed bases through steady consumable demand. Novel polymer membranes now tailor adhesion and thickness to specific tissue classes, improving capture efficiency. Suppliers add RFID tags to consumables so laboratories can track batch usage and automate re-ordering. As microfluidic-LCM hybrids reach market, entirely new cartridge formats could deliver combined isolation and lysis, enabling bundled revenue streams that blur the boundary between hardware and consumables.

Ultraviolet systems owned 52.11% revenue in 2024, yet infrared platforms are forecast to expand 15.61% yearly thanks to milder thermal signatures that protect DNA and proteins for downstream omics. Infrared devices also capture cells more cleanly, which suits single-cell pipelines seeking error-free libraries. UV systems remain popular where morphological preservation is essential, such as teaching hospitals that pair microdissection with conventional histology.

Vendors differentiate through automation depth, sample navigation speed, and compatibility with high-content image analysis. Infrared platforms operate at lower power thresholds that cut edge carbonization, enhancing capture yield. Meanwhile, laser microdissection pressure-catapulting systems find niche demand in forensic science, where non-contact ejection eliminates contamination risk in trace DNA work. Together these advances keep the laser capture microdissection market responsive to shifting research priorities.

The Laser Capture Microdissection Market is Segmented by Product (Instruments, and More), System Type (Ultraviolet LCM, and More), Application (Research & Development [Genomics, Proteomics], and More), End User (Academic & Government Research Institutes, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America retained 42.82% of laser capture microdissection market share in 2024, supported by sustained National Institutes of Health funding and mature pharmaceutical R&D clusters. Widespread adoption of digital pathology simplifies workflow integration, while AI-assisted microdissection reduces labor bottlenecks. Nevertheless, staffing shortages and reimbursement pressures temper near-term growth.

Europe follows as the second-largest region through concerted public-private programs that back precision-medicine research. Germany, the United Kingdom, and France house multiple laser capture microdissection core facilities that operate as shared hubs, improving equipment utilization. Harmonized companion diagnostic regulations encourage device makers to partner with local biopharma companies. Still, funding variability among EU states and post-Brexit research uncertainties create uneven adoption rates across the continent.

Asia-Pacific posts the fastest 13.44% CAGR to 2030. China's Five-Year Plan prioritizes spatial biology, prompting large-scale laboratory construction and bulk purchasing agreements. Japanese institutes pursue oncology and neurodegeneration studies that depend on high-fidelity infrared microdissection. India's contract research organizations add laser capture microdissection to service menus for global drug sponsors, yet infrastructure gaps and talent shortages may slow rollout outside tier-one cities. Collective investment across the region points to sustained, above-average expansion.