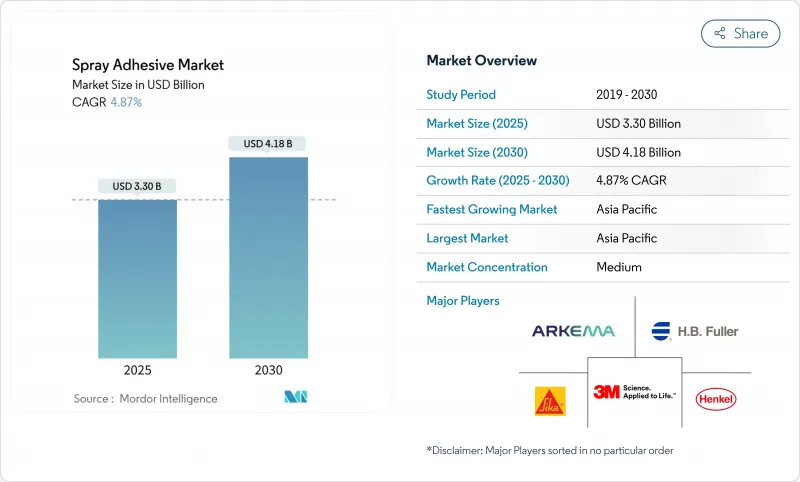

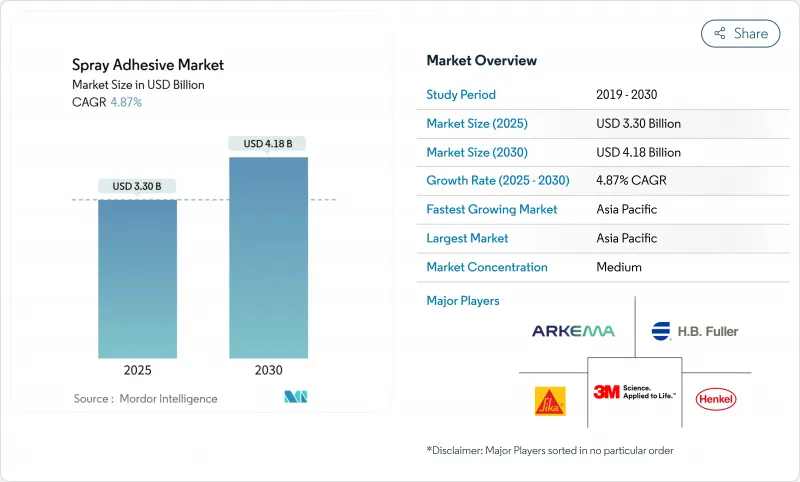

스프레이 접착제 시장은 2025년 33억 달러로 평가되며, 안정적인 4.87%의 연평균 복합 성장률(CAGR)을 나타내 2030년까지 41억 8,000만 달러로 상승할 것으로 예측됩니다.

VOC 규제가 강화되었음에도 불구하고 수요가 견조한 이유는 생산자가 기존의 솔벤트 제품의 접착 강도에 필적하는 수성 및 핫멜트 화학제품을 지속적으로 개선하고 있기 때문입니다. 아시아의 태평양 지역은 성장이 집중되는데, 대규모 인프라 정비 계획, 확대되는 가구 수출 거점, 자동차 공급망 등 모두 신속하고 대량의 접착 솔루션이 필요합니다. 또한 세계 전자상거래 물류도 기세를 늘리고 있으며, 풀 필먼트 센터는 포장 시간을 단축하는 에어로졸과 핫멜트의 변형을 지정하게 되었습니다. 경쟁 압력은 완만하지만, 가격에 민감한 구매자는 지속 가능한 성능 업그레이드로 차별화를 도모하는 반면, 저렴한 비용으로 프리미엄 화학을 재현하는 지역 공급업체로부터 새로운 옵션을 얻을 수 있습니다. 차량 경량화, 조립식 건설, 위생 식품 포장 등의 구조 촉진요인은 단일 섹터 변동으로부터 스프레이 접착제 시장을 보호하고 최종 용도의 다양성을 넓게 유지합니다.

중국, 인도, 인도네시아, 걸프 국가에서 공공 및 민간 인프라 투자의 급증은 스프레이 접착제를 포함한 건설용 화학제품의 지속적인 수량 성장을 가속하고 있습니다. 조립식 벽면 패널, 방음 보드 및 단열 시징은 모두 온도 변화와 지진 하중을 견디는 고성능 접착제에 의존합니다. 일부 지방 자치 단체의 주택 프로그램은 그린 빌딩 코드를 충족하기 위해 낮은 VOC 접착제를 지정하고 계약자를 수성 스프레이 시스템으로 유도합니다. 모듈식 건축업자는 오버 스프레이와 노동 시간을 줄이고 대규모 프로젝트의 처리 능력을 향상시키는 휴대용 캐니스터 장비를 지원합니다. 도시화가 가속화됨에 따라 현지 기업은 즉시 경화되는 핫멜트 스프레이 라인을 채택하여 고층 개발 내 주방 캐비닛과 인테리어 장비를 신속하게 조립할 수 있습니다. 이러한 복합적인 힘으로 스프레이 접착제 시장은 특히 아시아태평양의 급성장하는 거대 도시에서의 건축 활동과 깊게 연결되어 있습니다.

3 대륙의 규제 당국이 배출 상한을 낮추면 접착제 제조업체는 솔벤트 등급에 필적하는 탁과 내열성을 가진 수성 시스템을 출시했습니다. 텍사스 주 환경 품질위원회는 휴스턴 주변에서 하루에 3.12톤의 VOC를 제거하는 규칙을 개정하고, 캘리포니아의 유해물질 관리국은 2024년부터 2026년까지 우선 제품 작업 계획에 스프레이 접착제를 배치했습니다. 다우의 PRIMAL CA 750과 3M Fastbond 1049는 수성 폴리머가 비싼 환기 장비 업그레이드 없이 산업 처리 능력 목표를 달성할 수 있음을 보여줍니다. 선도적인 구매자, 특히 EU로 배송되는 가구 수출업체는 현재 구매 계약에 낮은 VOC 요구 사항을 통합하여 수성 화학 물질의 침투를 가속화하고 있습니다. 이러한 배합은 경화로의 소비 에너지가 적기 때문에 사용자는 광열비와 스코프 2 배출량의 직접적인 절약을 실현하고 있습니다.

대기질 기관은 제품 카테고리의 상한선을 강화하고 강용제 캐리어에 여전히 의존하는 브랜드에 즉각적인 컴플라이언스 부담을 강요합니다. 캘리포니아주 대기자원국은 웹 스프레이와 특수 용도 제제의 상한을 낮췄습니다. 뉴저지의 규칙안은 건축용 접착제의 허용 VOC를 절반 이상 줄이기 위한 것입니다. 새로운 규제가 마련될 때마다 라벨의 교체 및 재인증, 때로는 폭발성 대기 오염 지역을 위한 지게차 업그레이드가 필요합니다. 세계 생산자는 여러 관할 구역의 임계값을 조정해야 하며, 생산량은 세분화되고 규모의 경제성은 깎여집니다. 신속한 재제조 자금을 조달할 수 없는 기업은 선반 공간을 잃고 스프레이 접착제 시장의 성장을 일시적으로 억제할 위험이 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

수성 등급은 2024년 매출의 42.78%를 차지하며 저배출 화학물질에 대한 업계의 노력을 뒷받침했습니다. 이 부문은 규제 지원과 수분산물에 120℃ 이상의 내열성을 제공하는 고분자 설계 업그레이드로 혜택을 받으며, 그 적용 범위가 넓어졌습니다. 아시아태평양 컨버터는 합판 라미네이션 라인으로의 침투를 촉진하기 위해 세척 가동 중지 시간을 최소화하는 캐니스터 스프레이 시스템을 채택했습니다. 이와 병행하여, 핫멜트 카테고리가 5.16%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이것은 순간 취급 강도와 제로 건조 오븐을 중시하는 자동화 가구 라인에 견인됩니다. 솔벤트 제품은 항공우주 산업의 복합재 보수와 같은 틈새 분야를 여전히 차지하고 있지만, 스프레이 접착제 시장 규모는 환경 규제의 높아짐에 따라 축소해 갈 것으로 보입니다.

수성 도료 채택을 촉진하는 두 번째 요인은 작업 가능 시간을 연장하고 과도한 분사량을 줄이는 휴대용 장비 개발에서 비롯됩니다. Worthington Enterprises는 3M사와 협력하여 완전 충전되고 균일한 스프레이 패턴을 유지하는 경량 가압 캐니스터를 제공하여 공장 내 반송 효율을 80%까지 높였습니다. 이러한 개선은 이 범주가 2030년까지 지속적인 리더십을 발휘하기 위해 수성 접착제 라인을 수립하고 기존 솔벤트 사용자에 대항하여 스프레이 접착제 시장 점유율을 보호하는 데 도움이 됩니다.

아시아태평양은 2024년 매출액에서 46.76%를 차지했으며 CAGR 전망에서는 가장 빠른 5.91%를 나타냅니다. 저렴한 주택에 대한 중국의 자극책과 인도의 고속도로 회랑 프로젝트는 패널 라미네이트 스프레이와 타일 접착제의 안정적인 수요를 보장합니다. 현지 컨버터는 미국 및 유럽 연합(EU)을 위한 가구 수출 주문을 충족하기 위해 생산 능력을 강화하고, 목적지 규정에 따라 낮은 VOC 지표를 통합합니다. 일본의 전자기기 조립 제조업체는 프린트 기판상의 결로 리스크를 저감하는 고고형분의 수성 스프레이를 지지해, 현지의 컴파운드 제조업체가 하청 파트너에게 배합을 확대하는 것에 박차를 가하고 있습니다. 한국의 배터리 산업은 폴리우레탄 스프레이 라인을 통합하여 고밀도 EV 팩의 방진성을 확보하고 있습니다.

북미는 주택 리폼, 상업시설의 지붕 교체, 국내 자동차 생산의 부활에 의존하고 있습니다. 유타주 환경질국은 소비자를 위한 제품규칙이 발효되면 연간 4,000톤의 VOC 삭감 가능성이 있다고 추정하고 있습니다. 이것은 이미 수성 캐니스터 구입으로 이동 한 컴플라이언스 시계입니다. 멕시코의 수출용 의자 공장은 자동 핫멜트 스프레이 부스에 투자하여 미국을 위한 극장용 좌석 및 접객용 가구의 처리 능력을 향상시키고 있습니다. 캐나다의 조립식 주택 공장은 엄격한 주법에 부합하는 난연성 스프레이를 지정하고 스프레이 접착제 시장의 지역 다양화를 지원합니다.

유럽은 성숙하면서도 기술 혁신 주도의 양상을 나타내고 있습니다. 독일의 고급 자동차 OEM은 무취 콕핏용 접착제를 요구하고 있으며, 공급업체는 단량체가 없는 폴리우레탄 분산액의 조정에 방향타를 끊고 있습니다. 영국에서는 건축용 수성 스프레이로 고정된 저배기 가스 스프레이 폼 패널이 채택되어 있어 후퇴 단열재를 추진합니다. Seka의 118억 스위스 프랑의 세계 매출은 EMEA의 건축용 화학물질로 7.3%의 성장을 보여 접착제 수요의 회복력을 증명하고 있습니다. 이탈리아와 폴란드의 가구 제조업체는 온라인 소매업체의 리드 타임 단축의 기대에 부응하기 위해 스프레이 라인을 자동화. EU의 녹색 거래 정책이 솔벤트 대체를 가속화하고 유럽이 스프레이 접착제 시장에서 지속가능성 기준 시장이 되도록 합니다.

The spray adhesive market is valued at USD 3.30 billion in 2025 and is forecast to climb to USD 4.18 billion by 2030 on a steady 4.87% CAGR.

Demand holds firm despite tightening VOC rules because producers continue to refine water-based and hot-melt chemistries that match the bonding strength of legacy solvent products. Growth concentrates in Asia-Pacific, where large-scale infrastructure programs, expanding furniture export hubs, and a deep automotive supply chain all require fast-tack, high-volume bonding solutions. Momentum also comes from global e-commerce logistics, which pushes fulfillment centers to specify aerosol and hot-melt variants that shorten pack-out time. Competitive pressure stays moderate, yet price-sensitive buyers have new choices from regional suppliers that replicate premium chemistries at lower cost while multinational leaders differentiate through sustainable performance upgrades. Structural drivers such as vehicle lightweighting, prefab construction, and hygienic food packaging keep end-use diversity wide, shielding the spray adhesive market from volatility in any single sector.

Surging public and private infrastructure investment across China, India, Indonesia, and the Gulf states is driving relentless volume growth for construction chemicals, including spray adhesives. Prefabricated wall panels, acoustic boards, and insulation sheathing all rely on high-performance bonding to withstand temperature swings and seismic loading. Several municipal housing programs specify low-VOC adhesives to meet green-building codes, nudging contractors toward water-based spray systems. Modular builders favor portable canister rigs that reduce overspray and labor time, increasing throughput on large projects. As urbanization accelerates, local firms adopt hot-melt spray lines that cure instantly, allowing rapid assembly of kitchen cabinets and interior fixtures inside high-rise developments. These combined forces keep the spray adhesive market deeply tied to building activity, particularly in Asia-Pacific's fast-growing megacities.

Regulators on three continents have enacted lower emission ceilings, prompting adhesive formulators to launch waterborne systems with comparable tack and heat resistance to solvent grades. The Texas Commission on Environmental Quality amended rules that will eliminate 3.12 tons per day of VOCs around Houston, while California's Department of Toxic Substances Control placed spray adhesives on its 2024-2026 priority product work plan. Dow's PRIMAL CA 750 and 3M's Fastbond 1049 demonstrate that water-based polymers can meet industrial throughput targets without costly ventilation upgrades. Large buyers, especially furniture exporters shipping into the EU, now embed low-VOC requirements in purchase contracts, accelerating penetration of waterborne chemistries. As curing ovens consume less energy with these formulations, users realize direct savings on utility expenses and scope-2 emissions.

Air-quality agencies have tightened product-category caps, placing immediate compliance burdens on brands that still rely on strong-solvent carriers. The California Air Resources Board lowered limits on web-spray and special-purpose formulations. New Jersey's draft rule aims to cut allowable VOCs in construction adhesives by more than half. Every new limit triggers relabeling, re-qualification, and sometimes forklift upgrades for explosive-atmosphere zones. Global producers must juggle multiple jurisdictional thresholds, fragmenting volume runs and trimming economies of scale. Firms unable to finance rapid reformulation risk losing shelf space, temporarily suppressing growth in the spray adhesive market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Water-based grades held the largest 42.78% portion of 2024 revenue, confirming industry commitment to low-emission chemistries. The segment benefits from regulatory support and from upgrades in polymer design that give water dispersions heat resistance above 120 °C, widening their application window. Asia-Pacific converters adopted canister spray systems that minimize cleaning downtime, advancing penetration across plywood lamination lines. In parallel, the hot-melt category is charting the quickest 5.16% CAGR, driven by automated furniture lines that value instant handling strength and zero drying ovens. Solvent products still occupy niche spaces such as aerospace composite repair, but their spray adhesive market size is set to shrink as environmental levies rise.

A second boost to water-based adoption comes from portable equipment developments that extend pot life and reduce overspray. Worthington Enterprises collaborated with 3M to deliver lightweight pressurized canisters that maintain uniform spray patterns for the full charge, lifting in-plant transfer efficiency to 80%. These improvements help the category defend its spray adhesive market share against entrenched solvent users, positioning water-based lines for sustained leadership through 2030.

The Spray Adhesive Market Report Segments the Industry by Type (Solvent-Based, Water-Based, and Hot Melt), Resin Type (Epoxy, Polyurethane, Synthetic Rubber, and More), Application (Building and Construction, Packaging, Furniture, Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Million)

Asia-Pacific dominates with 46.76% revenue in 2024 and exhibits the fastest 5.91% CAGR outlook. China's stimulus for affordable housing and India's highway corridor projects ensure consistent demand for panel lamination sprays and tile adhesives. Local converters boost capacity to satisfy furniture export orders to the United States and the European Union, embedding low-VOC metrics that align with destination regulations. Japan's electronics assemblers champion high-solids water-based sprays that reduce condensation risk on printed-circuit boards, spurring local compounders to scale formulations for subcontract partners. South Korea's battery vertical integrates polyurethane spray lines to secure vibration isolation in high-density EV packs.

North America relies on strong residential remodeling, commercial reroofing, and resurgent domestic auto production. The Utah Department of Environmental Quality estimates a potential 4,000-ton annual VOC cuts once its consumer-product rule takes effect. This sets a compliance clock that already shifts purchase preference toward water-based canisters. Mexico's export-oriented upholstery factories invest in automated hot-melt spray booths that boost throughput for theater seating and hospitality furniture destined for the United States. Canadian prefab home plants specify flame-retardant sprays that meet stringent provincial codes, underpinning regional diversification within the spray adhesive market.

Europe shows a mature yet innovation-driven profile. Germany's premium auto OEMs require odor-free cockpit adhesives, steering suppliers to tailor monomer-free polyurethane dispersions. The United Kingdom's retrofit insulation drive deploys low-emission spray foam panels secured with construction-grade water-based sprays. Sika's CHF 11.8 billion global sales, with 7.3% growth in EMEA construction chemicals, evidence adhesive demand resilience. Italian and Polish furniture clusters automate spray lines to meet shorter lead-time expectations from online retailers. EU Green Deal policies accelerate solvent replacement, ensuring that Europe remains a reference market for sustainability in the spray adhesive market.