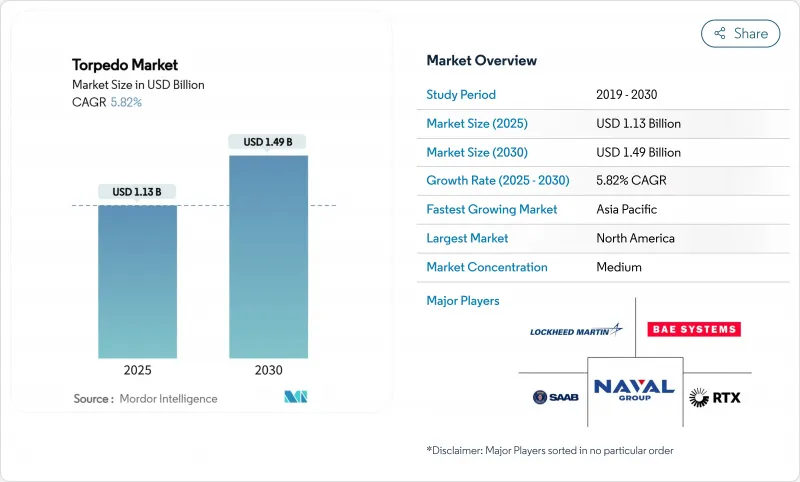

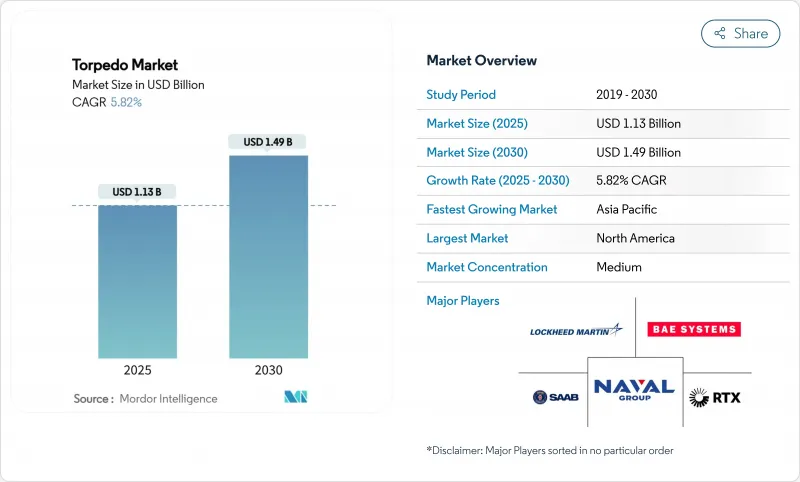

어뢰 시장 규모는 2025년에 11억 3,000만 달러로 추정되고, 2030년에는 14억 9,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 5.82%로 성장할 전망입니다.

남중국해, 발트해 및 기타 종로에서의 해전 경쟁의 격화에 의해 방위성은 억지력을 중량 어뢰나 경량 어뢰에 의존하는 잠수함 중심의 전력 구성으로 방향타를 끊고 있습니다. AUKUS와 유사한 동맹 하에서 함대 재편 계획은 MK-48, F21 및 기타 플래그쉽 모델의 주문 잔여를 계속 증가시키고 있습니다. 한편, 리튬 이온 배터리를 중심으로 구축된 전기 추진 설계는 음향 시그니처를 저감하고 초계 내구성을 연장함으로써 점유율을 획득하고 있습니다. 게다가 초경량 어뢰를 발사하는 무인 수중 차량(UUV)과 무인 수상 함정(USV)이 비용 효과적인 영역 거부와 기뢰 대책의 선택을 제공해 수요를 뒷받침하고 있습니다. 은과 희토류 원소 공급망에 대한 노출은 여전히 구조적 우려이지만, 각국 정부는 이러한 투입물을 재활용하고 수입 의존도를 줄일 수 있는 폐쇄 루프 회수 라인에 자금을 제공합니다.

해군은 기록적인 페이스로 신형 공격형 잠수함 및 탄도 미사일 잠수함을 배치하고 있으며, 중량급 어뢰의 지속적인 수요를 만들어내고 있습니다. 호주는 2025년 3월에 MK-48 Mod 7탄을 추가 발주하여 콜린스급정의 원자력 대체에 앞서 잠정적인 살상력을 확보했습니다. 브라질은 2024년에 F21 무기와 통합 전투 스위트를 장비한 후마이타를 취역시켰습니다. 그리스 214형에서 씨헤이크 모드 4로의 업그레이드는 중형 함대조차 50km 사거리의 탄두로 탄창을 현대화하는 것을 강조합니다. 수중 억제력이 수상 전력보다 예산의 우선순위가 높다는 패턴은 분명합니다.

따라서 장거리 미사일의 확산에도 불구하고 어뢰는 여전히 필수적입니다. 일본의 12식 미사일의 증강은 P-1 항공기와 '모가미'급 프리게이트함의 대잠 펀치를 유지하는 전국적인 스팅레이의 갱신과 공존하고 있습니다. 영국은 2025년에 7,500만 달러를 스팅 레이의 서비스 연수 중기 정비에 할당하여 2040년까지 가용성을 확보했습니다. 독일은 포세이돈 함대를 위해 동일한 경량 라운드를 조달하고 상호 운용성이 조달 주기를 가속화하는 방법을 보여줍니다. 이러한 움직임은 해군이 미사일이 고갈되거나 고장나면 어뢰가 유일한 입증된 근거리 살상 솔루션으로 간주됨을 나타냅니다.

새로운 유도 패키지인 MK-48 Mod 7탄은 600만 달러를 초과할 수 있어 해군 예산이 잠수함과 미사일에 자금을 제공할 때 구매력을 압박합니다. 미국 해군이 2025년도에 버지니아급 선체를 2척에서 1척으로 한다는 결정을 내린 것은 얼마나 비싼 탄약이 보다 광범위한 전력 구조의 트레이드오프에 연쇄되는지를 부각하고 있습니다. 윤택한 자금을 가진 사우디아라비아조차도 MK-54를 주문하기 전에 의회의 승인을 기다리고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

중량급 모델은 2024년에 어뢰 시장 점유율의 53.78%를 차지했으며, 고수율 탄두와 50km 이상의 사정이 결정적인 블루워터 억제에 있어서의 우위성을 강조했습니다. 호주의 2억 달러를 들인 보충 및 브라질 스콜펜의 의장은 중량급 등급의 안정적인 수량을 뒷받침합니다. 반대로 초경량 설계는 2030년까지 연평균 복합 성장률(CAGR) 8.24%의 궤도에 있을 전망이며, 컴팩트한 총알을 선호하는 무인 통합과 연안 방위 임무에 의해 추진됩니다. 스웨덴의 어뢰 47과 미국 국방부가 자금을 제공하는 Skelmir 컨셉은 25kg 이하의 초소형 어뢰가 해안에서 기뢰와 소형 잠수함을 무력화할 수 있음을 보여줍니다.

해군은 포화 커버를 위해 경량의 탄환 무리를 채용하는 한편, 료함과의 교전을 위해 수는 적지만 스마트한 중량급의 총알을 조달합니다. 이 균형 잡힌 포트폴리오는 일상적인 순찰에서 한 발당 비용을 낮추지만 쟁탈전이 되는 심해에서의 교전에서는 전략적 펀치를 유지합니다. 따라서 어뢰 시장은 다양화를 계속하고 있으며, 프라임이 중량급 유지에 주력하는 반면, 틈새 공급업체는 더 가벼운 틈새 시장에 진입하고 있습니다.

해중 발사 무기는 잠수함의 스텔스성을 활용하여 해중 및 지상 위협에 대한 선제 공격 능력을 제공하며, 2024년에는 62.33%로 여전히 우세했습니다. 그러나 해군이 Anduril의 Dive-LD와 같은 10일간의 임무로 자기 회수할 수 있는 UUV를 배치함에 따라 무인 플랫폼 발사 시스템이 CAGR 8.80%에서 가장 빠르게 성장하고 있습니다. 항공 발사는 고정 날개 기계를 방공 우산에서 떼어낼 수 있는 고도의 키트에 의해 사용률이 상승하고 있어 지휘관은 선체를 위험에 빠뜨리지 않고 보다 넓은 교전 아크를 얻을 수 있습니다.

무인 플랫폼의 어뢰 시장 규모는 높은 센서 대사자의 자동화율을 반영하여 2030년까지 2억 2,000만 달러에 달할 것으로 예측됩니다. 자율성이 확대됨에 따라 기존의 프리깃함은 충실한 날개를 가진 수상 무인 항공기에 매거진의 무게를 오프로드하여 어뢰 살보를 더 분산시키고 생존할 수 있습니다.

북미는 2024년 매출의 33.90%를 차지했으며, 미국 해군의 버지니아급 건조 대기열과 캐나다의 AUKUS 기술 공유 진입에 뒷받침되었습니다. 현재 설계 초기 단계에 있는 SSN(X) 컨셉은 모듈형 페이로드 베이가 장착된 차세대 전기 어뢰를 탑재할 것으로 예상되며, 이 지역이 2030년대까지 가장 큰 구매자임을 보장합니다. 그러나 예산 한도는 새로운 산업 능력이 단가를 낮출 때까지 연간 구매량을 압축할 수 있습니다.

아시아태평양은 CAGR 7.21%에서 가장 빠르게 성장하는 지역입니다. 중국의 Yu-10 개발과 인도의 DRDO 파이프라인은 자급자족에 축발을 보여줍니다. 동시에 일본의 모가미급 프리게이트함은 성숙해지고 있는 PLAN의 잠수함 부대에 대항하기 위해 97식 어뢰와 개량형 소나 체인을 통합하고 있습니다. 한국의 슈퍼 캐비테이션 프로토타입 함과 대만의 무인 함대는 기술의 도약을 시사하고 있으며, 미래에는 서양 주도에서 현지 주도로 이행할 가능성이 있습니다.

유럽, 남미, 중동 및 아프리카은 꾸준하지만 다양한 궤도를 보여줍니다. 독일이 영국의 스팅 레이를 조달하는 등 유럽의 공동구매는 NATO 임무부대 하에서 상호운용성을 최적화하고 있습니다. 브라질의 프로서브 조선소는 2029년경 이 지역 최초의 원자력 공격형 잠수함을 건조할 예정입니다. 이집트와 사우디아라비아는 각각 039A형과 MK-54 패키지를 평가하고 있으며, 어뢰 시장이 기존의 세력권을 넘어 신뢰할 수 있는 수중 억제력을 요구하는 연안 국가로 퍼져 있음을 보여주고 있습니다.

The torpedo market size is estimated at USD 1.13 billion in 2025, and is expected to reach USD 1.49 billion by 2030, reflecting a CAGR of 5.82% during the forecast period.

Escalating naval competition in the South China Sea, Baltic Sea, and other chokepoints is steering defense ministries toward submarine-centric force structures that rely on heavyweight and lightweight torpedoes for deterrence. Fleet recapitalization programs under AUKUS and similar alliances continue to enlarge backlogs for MK-48, F21, and other flagship models, while electric-propelled designs built around lithium-ion batteries are carving out a share by lowering acoustic signatures and lengthening patrol endurance. Demand is further buoyed by unmanned underwater vehicles (UUVs) and unmanned surface vessels (USVs) that now launch very-lightweight torpedoes, offering cost-effective area denial and mine-countermeasure options. Supply-chain exposure to silver and rare-earth elements remains a structural concern, yet governments are funding closed-loop recovery lines that can recycle those inputs and reduce import dependence.

Navies are fielding new attack and ballistic-missile submarines at a record pace, generating sustained demand for heavyweight torpedoes. Australia's March 2025 order for additional MK-48 Mod 7 rounds positions Collins-class boats for interim lethality ahead of nuclear-powered replacements. Brazil followed by commissioning Humaita in 2024, equipped with F21 weapons and an integrated combat suite. Greece's Type 214 upgrade to the SeaHake Mod 4 underscores how even mid-sized fleets modernize magazines with 50 km-range warheads. The pattern is clear: underwater deterrence outranks surface power in budget priority.

Multi-domain doctrines emphasize layered defense; thus, torpedoes remain indispensable despite long-range missile proliferation. Japan's Type 12 missile expansion coexists with a nationwide Sting Ray refresh that keeps antisubmarine punch aboard P-1 aircraft and Mogami-class frigates. The UK allocated USD 75 million in 2025 for Sting Ray mid-life work, ensuring availability through 2040. Germany sourced the same lightweight round for its Poseidon fleet, illustrating how interoperability accelerates procurement cycles. These moves signal that navies view torpedoes as the only proven close-range kill solution once missiles exhaust or fail.

A MK-48 Mod 7 round with a new guidance package can exceed USD 6 million, compressing buying power when naval budgets fund submarines and missiles. The US Navy's FY 2025 decision to accept only one Virginia-class hull instead of two highlights how expensive ammunition cascades into wider force-structure trade-offs. Though flush with funds, Saudi Arabia still awaits Congressional clearance before ordering MK-54s, signaling that even cash-rich customers weigh cost-to-benefit carefully.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Heavyweight models captured 53.78% of the torpedo market share in 2024, underlining their dominance in blue-water deterrence, where high-yield warheads and 50 km+ ranges remain decisive. Australia's USD 200 million restock and Brazil's Scorpene fitout confirm steady volume in the heavyweight class. Conversely, very-lightweight designs are on an 8.24% CAGR path to 2030, propelled by unmanned integration and coastal defense missions that favor compact rounds. Sweden's Torpedo 47 and the Pentagon-funded Skelmir concept show how micro-torpedoes weighing under 25 kg can neutralize mines and midget subs in littorals, often at one-tenth the cost of a traditional weapon.

Growth signals a bifurcating toolkit: navies procure fewer but smarter heavyweights for peer engagements while adopting swarms of light rounds for saturation coverage. This balanced portfolio lowers per-shot cost for routine patrol but retains strategic punch for contested deep-water engagements. The torpedo market, therefore, continues to diversify, with niche suppliers entering lighter niches as primes focus on heavyweight sustainment.

Sea-launched weapons still dominate at 62.33% in 2024, leveraging submarines' stealth to provide first-strike capacity against undersea and surface threats. Yet, unmanned-platform-launched systems are growing fastest at 8.80% CAGR as navies deploy UUVs such as Anduril's Dive-LD that can self-recover after 10-day missions. Air-launched usage is rising through high-altitude kits that allow fixed-wing aircraft to stand off from air-defense umbrellas, giving commanders wider engagement arcs without risking hulls.

The torpedo market size for unmanned platforms is projected to reach USD 0.22 billion by 2030, reflecting high sensor-to-shooter automation rates. As autonomy scales, traditional frigates may offload magazine weight to loyal-wingman surface drones, making torpedo salvos more distributed and survivable.

The Torpedo Market Report is Segmented by Weight (Heavy, Light, and Very Light), Launch Platform (Sea and Air), Propulsion Type (Electric and Conventional), Guidance System (Wire-Guided, Acoustic, and Optical), Application (Anti-Submarine Warfare and Anti-Surface Warfare), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 33.90% of 2024 sales, supported by the US Navy's Virginia-class construction queue and Canada's entry into AUKUS technology sharing. The SSN(X) concept, now in early design, is expected to carry next-generation electric torpedoes with modular payload bays, ensuring the region stays the largest buyer well into the 2030s. Budget ceilings, however, may compress annual buy quantities until new industrial capacity reduces unit costs.

Asia-Pacific is the fastest-growing territory at 7.21% CAGR. China's Indigenous Yu-10 development and India's DRDO pipeline exemplify the pivot toward self-sufficiency. At the same time, Japan's Mogami-class frigates integrate Type 97 torpedoes and improved sonar chains to counter a maturing PLAN submarine arm. South Korea's supercavitating prototype and Taiwan's expanding unmanned fleet signal a technology leap that could shift future volume away from Western primes toward local champions.

Europe, South America, and the Middle East and Africa regions show steady but varied trajectories. Europe's collaborative buys-such as Germany procuring UK Sting Ray stocks-optimize interoperability under NATO task force constructs. Brazil's ProSub yard is turning out the region's first nuclear attack submarine around 2029. Egypt and Saudi Arabia are evaluating Type 039A and MK-54 packages, respectively, indicating that the torpedo market is widening beyond traditional power blocks into littoral states seeking credible underwater deterrence.