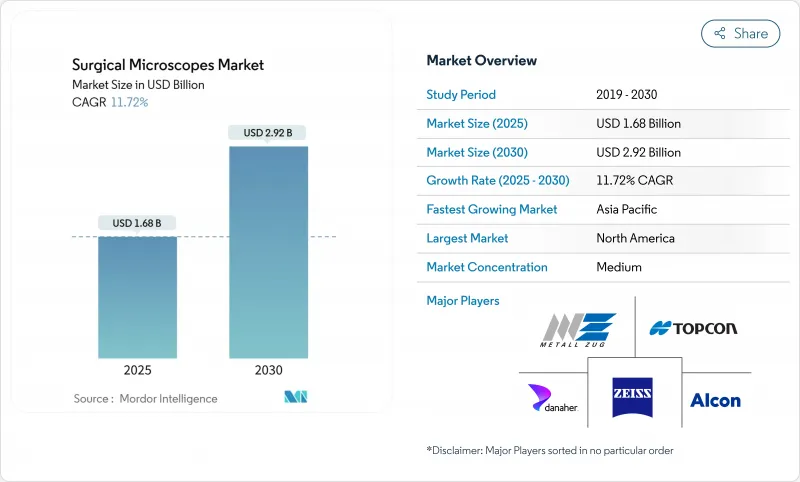

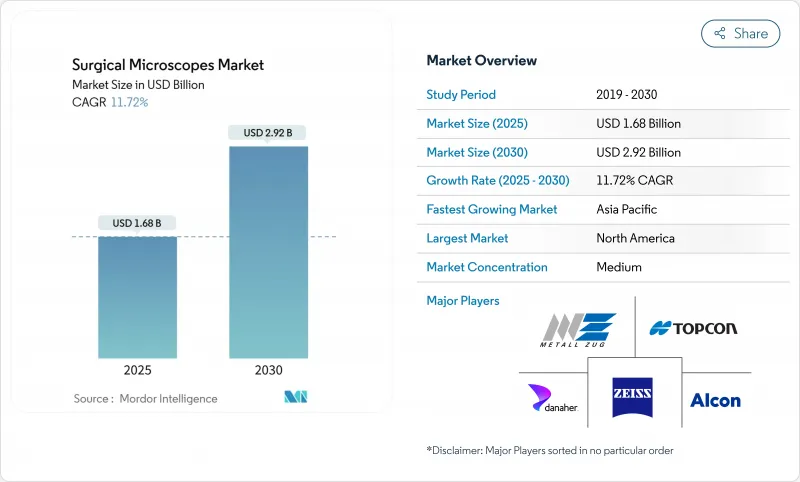

수술용 현미경 시장은 2025년에 16억 8,000만 달러로 추정되고, 2030년에는 29억 2,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR 11.72%로 성장이 전망됩니다.

저침습 수술에 대한 왕성한 수요, 4K 및 형광 이미지로의 급속한 업그레이드, 세계적인 고령화 등이 결합되어, 고급 시각화가 수술실에 대한 투자 결정의 중심에 자리잡고 있습니다. 병원은 현미경 기능을 고도로 숙련된 외과의사를 매료시키는 매력으로 간주하고 있으며, 로봇 공학 및 음성 제어 포지셔닝은 수술 시간을 단축하고 인간 공학을 개선합니다. 디지털화된 3D 뷰와 증강현실 뷰는 이제 광학 해상도 이상으로 조달 기준을 형성하고 있으며, 컴팩트한 외시경을 통한 대체 위협은 기존 기업들에게 기능 로드맵의 가속화를 촉구하고 있습니다. 성장 기회는 아시아태평양의 중견 시설에 집중되어 있으며, 하이브리드 수술실은 유연한 자금 조달 및 교육 서비스를 번들링할 수 있는 벤더에게 새로운 대응 가능 대수를 개척합니다.

외과의사는 현재 제한된 해부학적 공간 내에서 고배율 및 눈부심없는 시야를 필요로 하는 복강경 수술 및 내시경 수술을 광범위하게 실시했습니다. 뇌신경 수술팀은 혈류와 종양의 단부가 실시간으로 보이도록 형광 모듈을 추가하는 경우가 늘어나 촬영 모드를 전환할 필요가 없습니다. 병원은 현미경의 고도화와 복잡하고 진료 보상이 높은 사례를 확보하는 능력 사이에 직접적인 관련성이 있다고 생각하여 장비의 갱신 사이클을 강화하고 있습니다. 그 결과, 수술용 현미경 시장은 진료과가 개복 수술에서 키홀 수술로 이행할 때마다 시장 규모를 확대하여 여러 해에 걸친 수요를 견인하고 있습니다.

외과 수술 환자의 연령 중앙값은 꾸준히 상승하고 있으며, 2030년에는 61.5세에 이를 것으로 예측됩니다. 백내장과 망막 수술은 노인층에서 급증하기 때문에 안과가 가장 많은 혜택을 받습니다. 뇌 신경 외과 의사는 마찬가지로 노인 동맥류 및 종양 환자의 취약한 뇌 혈관을 탐색하기 위해 현미경에 의존합니다. 노인 환자에게는 여러 합병증이 있기 때문에 임상의는 수술 시간을 단축하고 노출을 줄이기 위해 형광 및 OCT 오버레이와 광학적 명료성을 결합한 시스템을 선호합니다. 이러한 인구 역학은 수술용 현미경 시장의 장기적인 건전성을 지원합니다.

연간 유지보수 비용은 구입 가격의 약 3.1%이며, 그 3분의 2는 인건비입니다. 예산이 제한되어 있기 때문에 지역 병원에서는 외과 의사가 4K 또는 형광 애드온을 요청하더라도 업데이트가 지연됩니다. 제조업체는 사용량 기반의 서비스 플랜으로 대항하고 있지만, 다년간 비용의 가시화는 여전히 저소득 지역에서의 조달을 늦추며 세계의 CAGR의 중하가 되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

이비인후과는 CAGR 15.25%로 성장하며. 수술용 현미경 시장의 임상 부문 중 가장 빠른 2025년 수익 풀을 획득했습니다. 안과는 백내장과 망막 유리체 수술의 볼륨이 크고 2024년 매출의 26.35%를 차지했습니다. 이비인후과는 부비동과 이비인후과의 수술이 헤드업 디스플레이와 형광 지침에 의존하게 되어 그 기세가 증가하고 있습니다. 병원에서는 이비인후과에서 뇌신경외과로 쉽게 이행할 수 있는 다목적 플랫폼이 선호되고 있어 부문을 넘은 자본 효율을 창출하고 있습니다.

향후 외래센터가 기능적인 내시경하 부비강 수술, 고막절제술, 두개저종양학 등 서비스 메뉴를 확대함에 따라 이비인후과 점유율이 높아질 것으로 보입니다. 벤더는 좁은 통로에도 대응할 수 있도록, 롱리치 광학계, 슬림한 대물 렌즈 하우징, 피사계 심도의 확대 등으로 대응하고 있습니다. 한때 뇌신경외과에서만 사용되었던 형광혈관조영은 현재 이비인후과의 혈관 재건에도 사용되고, 고급 모델에 대한 수요가 높아지며, 수술용 현미경 시장 전체가 활성화되고 있습니다.

병원은 여전히 모든 유닛의 절반 근처를 조달하고 있지만 외래수술센터(ASC)가 가장 높은 CAGR 14.85%로 성장을 기록하고 있습니다. ASC는 컴팩트한 실적, 신속한 드레이프 교환 및 당일 퇴원 지표를 지원하는 통합 기록을 중시합니다. 제조업체는 작은 캐스터베이스와 터치리스 포지셔닝으로 카트를 조정하고 ASC 워크 플로우에 맞는 기능을 제공합니다.

병원 내에서는 정형외과, 성형외과, 혈관외과의 각 진료실에 현미경을 할당해, 가동 시간을 극대화하는 쉐어드 오너십 풀이 서비스 라인을 리드하고 있습니다. 학술기관에서는 AI 오버레이와 원격 프로토타이핑을 시험적으로 도입하고 있으며, 조기 검증을 실시함으로써 상업적인 발매로 연결하고 있습니다. 이러한 사용자의 다양성으로 수술용 현미경 시장은 상환 제도의 변화에도 유연하게 대응하고 있습니다.

북미는 조기 도입 교육 병원, FDA의 명확한 패스웨이, 번들 서비스 자금 조달로 2024년 매출의 45.82%를 차지했습니다. 미주리 주에 새로 설립된 자이스 제조 허브는 현지 공급 및 서비스 대응 시간을 강화합니다. 자본 예산은 여전히 압박되고 있지만 형광과 로봇 옵션으로의 교체가 시급하기 때문에 한 자릿수 중반의 성장이 유지됩니다.

아시아태평양은 공공 및 민간 운영자가 하이브리드 극장을 증설하고 당일 수술 네트워크를 확대함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 16.81%로 가장 높을 것으로 전망됩니다. 중국과 인도의 국내 제조 인센티브는 수입 관세를 인하하고 현지 조립 파트너십에 스포트라이트를 적용하고 있습니다. 일본의 확립된 광학 부문은 기술 혁신을 계속 수출하고, 지역 경쟁력을 강화하며, 동남아시아 전역에서의 채용을 촉진합니다.

유럽은 근대화 보조금과 백내장 및 척추의 증례를 증가시키는 노화로 한 자릿수 중반의 안정적인 성장을 기록합니다. CE 마크의 하모나이제이션은 지역 전체 출시를 용이하게 하고 독일의 광학 클러스터는 현지 벤더의 R&D에 우위를 부여하고 있습니다. 의료관광회랑이 고급 기기의 구입을 촉구하고 세계의 수술용 현미경 시장에 새로운 층을 더하는 중동과 남미에는 작지만 유망한 비즈니스 기회가 존재합니다.

The surgical microscopes market stood at USD 1.68 billion in 2025 and is projected to reach USD 2.92 billion by 2030, translating into an 11.72% CAGR over the period.

Strong demand for minimally invasive surgery, rapid upgrades to 4K and fluorescence imaging, and an aging global population combine to keep advanced visualization at the center of operating-room investment decisions. Hospitals increasingly view microscope capabilities as a magnet for highly skilled surgeons, while robotics and voice-controlled positioning shorten procedure times and improve ergonomics. Digitally enabled 3D and augmented-reality views now shape procurement criteria more than optical resolution alone, and the substitution threat from compact exoscopes pushes incumbents to accelerate feature roadmaps. Growth opportunities concentrate in Asia-Pacific mid-tier facilities, where hybrid operating rooms open fresh addressable volume for vendors able to bundle flexible financing with training services.

Surgeons now perform a broader range of laparoscopic and endoscopic procedures that require high-magnification, glare-free views inside confined anatomical spaces. Neurosurgical teams increasingly add fluorescence modules so that blood flow and tumor margins are visible in real time, eliminating the need to switch imaging modes. Hospitals see a direct link between microscope sophistication and their ability to secure complex, high-reimbursement cases, reinforcing equipment refresh cycles. As a result, the surgical microscopes market gains volume every time a department shifts from open to keyhole techniques, driving multiyear demand visibility.

The median age of surgical patients has risen steadily, and projections show it reaching 61.5 years by 2030. Ophthalmology benefits most, as cataract and retinal interventions surge in older cohorts. Neurosurgeons similarly depend on microscopes to navigate fragile cerebral vessels in elderly aneurysm or tumor patients. Because older patients present multiple comorbidities, clinicians prioritize systems that combine optical clarity with fluorescence or OCT overlays to cut operative time and limit exposure. This demographic pull underpins the long-term health of the surgical microscopes market.

Annual service expenses equal roughly 3.1% of the original purchase price, with labor representing two-thirds of the outlay. Tight budgets delay refreshes in community hospitals even when surgeons ask for 4K or fluorescence add-ons. Manufacturers counter with usage-based service plans, but multiyear cost visibility still slows procurement in lower-income regions and weighs on global CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

ENT captured a 2025 revenue pool growing at 15.25% CAGR, the fastest among clinical segments in the surgical microscopes market. Ophthalmology kept 26.35% of 2024 revenue, powered by high-volume cataract and vitreo-retinal work. ENT momentum stems from sinus and otologic procedures that now rely on heads-up displays and fluorescence guidance. Hospitals favour multipurpose platforms that shift effortlessly from ENT to neurosurgery, creating cross-department capital efficiencies.

Over the forecast horizon, ENT's share rises as outpatient centers widen service menus to include functional endoscopic sinus surgery, stapedectomy and skull-base oncology. Vendors respond with long-reach optics, slim objective housings and extended depth-of-field to cope with narrow corridors. Fluorescence angiography that once sat exclusively in neurosurgery now migrates to ENT vascular reconstruction, reinforcing demand for premium models and lifting the overall surgical microscopes market.

Hospitals still procure nearly half of all units, but ambulatory surgical centers post the sharpest 14.85% CAGR as payors steer low-risk cases to outpatient settings. ASCs value compact footprints, rapid drape changes and integrated recording to support same-day discharge metrics. Manufacturers tailor carts with small caster bases and touchless positioning, aligning features with ASC workflow.

Within hospitals, service-line leads eye shared-ownership pools that allocate microscopes across orthopedics, plastic and vascular suites to maximize uptime. Academic institutes continue to pilot AI overlays and remote proctoring, providing early validation that filters into commercial launches. This user diversity keeps the surgical microscopes market resilient across changing reimbursement landscapes.

The Surgical Microscopes Market Report is Segmented by Application (Dentistry, Gynecology and Urology, ENT, Ophthalmology, and More), End User (Hospitals, Ambulatory Surgical Centers, and More), Mounting Type (On-Casters, Table-Top, and More), Technology (Conventional Optical, Optical + Fluorescence, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 45.82% revenue in 2024 thanks to early-adopter teaching hospitals, clear FDA pathways and bundled service financing. A new Zeiss manufacturing hub in Missouri strengthens local supply and service response times. While capital budgets remain under pressure, replacement urgency for fluorescence and robotic options sustains mid-single-digit growth.

Asia-Pacific registers the highest 16.81% CAGR through 2030 as public and private operators add hybrid theatres and expand day-surgery networks. Domestic manufacturing incentives in China and India cut import duties, spotlighting local assembly partnerships. Japan's established optics sector continues to export innovation, reinforcing regional competitiveness and elevating adoption across Southeast Asia.

Europe records steady mid-single-digit growth, driven by modernization grants and an aging population that boosts cataract and spinal cases. CE-mark harmonization eases pan-regional launches, and Germany's optical cluster gives local vendors a home-field R&D edge. Smaller but promising opportunities exist in the Middle East and South America where medical-tourism corridors stimulate premium equipment purchases, adding incremental layers to the global surgical microscopes market.