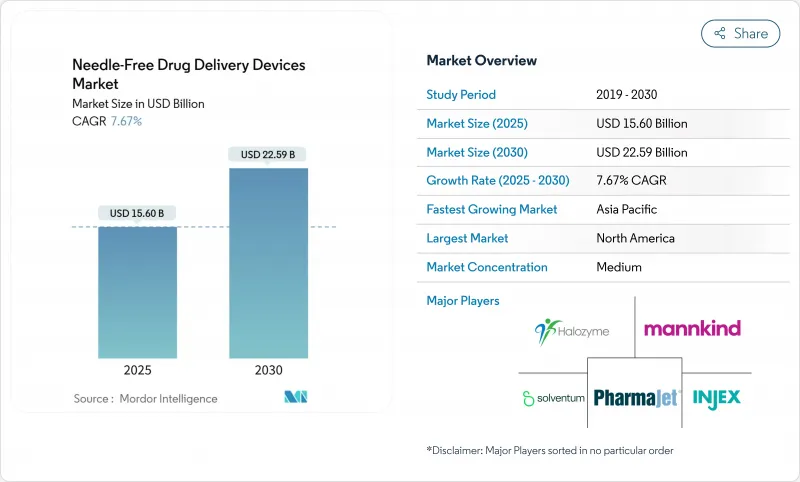

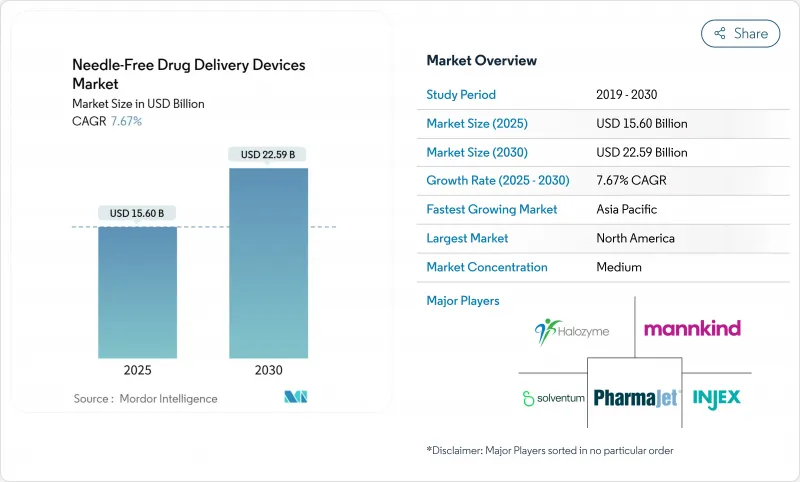

무바늘 약물전달 기기 시장은 2025년에 156억 달러로 추정되고, 2030년에는 225억 9,000만 달러에 이를 전망이며, CAGR 7.67%로 확대될 것으로 예측됩니다.

자기 투여에 대한 왕성한 수요, 생물 제제 파이프라인 증가, 디지털 헬스 통합에 대한 지속적인 투자가 이 상승 궤도를 뒷받침하고 있습니다. 북미가 지역별 점유율에서 최대를 차지하는 한편, 아시아태평양은 헬스케어에 대한 접근이 확대되고 만성 질환의 이환율이 상승함에 따라 급성장하고 있습니다. 제트 인젝터가 지배적인 지위를 유지하고 있지만, 3D 프린팅과 생분해성 재료가 새로운 제형의 가능성을 풀어 가면서 마이크로니들 패치가 빠르게 확대되고 있습니다. 정밀의료 전략으로 전신 독성을 최소화하고 어드히어런스를 향상시키는 전달 플랫폼이 요구되고 있기 때문에 암 치료가 가장 높은 용도 성장률을 보여줍니다. 규제의 복잡성은 여전히 주요 역풍이지만 진화하는 지침을 다루는 기업은 지속적인 경쟁 우위를 확보할 수 있습니다.

당뇨병, 암, 심혈관 질환의 세계적인 확산은 안전하고 통증이 없는 플랫폼으로의 전달 우선순위를 재설정하고 있습니다. 2024년 미국의 헬스케어 시설에서는 60만-80만 건의 바늘 찔림 손상이 기록되어 각각 500-3,000달러의 경과 관찰 비용이 들었습니다. 바늘이 없는 주사기는 날카로운 노출을 줄이고 평생 치료가 필요한 만성 질환 프로토콜에 적합합니다. 제조업체 각사는 현재 최대 72시간 유량이 유지되는 웨어러블 주사기 등 만성 질환의 이용 사례에 특화된 기기를 설계하고 있습니다. 이러한 환자 중심 설계는 무바늘 약물전달 기기 시장의 지속적인 수요를 지원합니다.

재택 케어 모델은 케어 경제를 재구성하고 있으며, enFuse 온바디 시스템 사용자의 87.5%가 자기 치료에 자신이 있다고 응답하고 있습니다. 의료 시스템은 시설 비용 절감의 혜택을 받으며 환자는 자율성을 얻을 수 있습니다. 인체 공학적 트리거, 촉각 피드백, 직관적인 그래픽 프롬프트와 같은 휴먼 팩터 엔지니어링은 확대되는 무바늘 약물전달 기기 시장에서 점유율을 얻는 중요한 차별화 요인이 되었습니다.

미국 FDA의 2024년 필수 약물전달 출력 지침은 콤비네이션 제품에 엄격한 검증 프로토콜을 도입하여 개발 사이클의 연장과 비용 상승을 가져왔습니다. EU와 아시아는 규칙이 다르기 때문에 기업은 지역별 버전을 개발할 수밖에 없으며 연구개발 예산이 분리되었습니다. 소규모 이노베이터는 이 부담을 가장 강하게 느끼고 있으며, 무바늘 약물전달 기기 시장에 대한 신규 진입의 발판이 되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

제트 인젝터는 2024년 매출의 61.3%를 차지했는데, 이는 백신 대응의 범용성과 고점도의 생물제제를 취급하는 능력을 반영한 것입니다. 이 이점을 통해 성숙한 기업은 무바늘 약물전달 기기 시장의 상당 부분을 확보하고 있습니다. 그러나 마이크로니들 패치는 CAGR 10.63%로 확대될 것으로 예측됩니다. 이는 용해가능한 폴리머가 샤프스 폐기물을 발생시키지 않고, 투과성이 강화되고 생체이용률이 최대 40% 향상되는 것으로 입증되었기 때문입니다.

폼 팩터 혁신은 경쟁 요인을 재정의합니다. 레이저 지원 시스템과 전기천공 장치는 틈새 단백질 치료 및 유전자 치료 파이프라인에 도움이 되어 무바늘 약물전달 기기 시장의 폭을 두드러지게 합니다. 3D 프린팅 금형은 제조업체가 미세 구조를 신속하게 반복할 수 있기 때문에 프로토타입 사이클을 단축하고 선행자 이점을 향상시킵니다.

일회용 유형의 점유율은 66.8%이지만, 환경 규제 및 비용 억제의 압력에 의해 재이용 가능 기기의 CAGR은 9.15%로 되고 있습니다. 수명 주기 분석에 따르면 일회용 주사기와 비교하여 폐기물을 85% 줄일 수 있습니다. 무바늘 약물전달 기기 시장에서는 이동식 약물 카트리지와 오토클레이브 가능한 하우징을 특징으로 하는 디자인이 점점 더 평가되고 있습니다.

사용자 중심 평가는 촉각 신호와 모바일 앱 튜토리얼을 통해 투여를 유도할 때 더 높은 신뢰성 점수를 얻을 수 있음을 보여줍니다. 재사용 가능한 시스템에 내장된 스마트 센서는 투약 데이터를 클라우드 대시보드로 전송하여 지속가능성 뿐만 아니라 어드히어런스 인텔리전스까지 가치를 확장합니다.

북미는 바이오의약품 연구개발 정착, 만성질환의 높은 보급률, 고도의 전달 시스템에 대한 상환으로 2024년 매출의 38.6%를 차지했습니다. FDA가 2024년에 승인한 조합 제품은 2023년 대비 32% 증가했으며, 무바늘 약물전달 기기 시장에 유리한 파이프라인임을 나타냅니다. 매사추세츠 공과 대학의 임상 데이터에서 마이크로니들 패치는 기존의 피하 경로보다 생물학적 제형을 40% 높은 생체이용률로 전달하는 것으로 나타났습니다. 디지털 건강의 성숙은 의료 제공업체의 대시보드에 어드히어런스 지표를 브로드캐스트하는 커넥티드 인젝터의 급속한 보급을 지원합니다.

아시아태평양은 중국과 인도가 만성기 의료 인프라를 정비함에 따라 CAGR 10.50%로 가장 급성장하고 있는 지역입니다. 현지 기업은 독자적인 제트 인젝터와 마이크로니들의 개발을 가속화하고 있으며, 수탁 제조에서 혁신 주도로의 전환을 시사하고 있습니다. 일본의 초고령화 인구 역학은 피부 취약성에 적합한 저하중 액추에이터 수요를 촉진하고 지역 설계 지침에 영향을 미칩니다. 아시아태평양경제협력의 틀 아래 규제조화는 국경을 넘어서는 전개를 용이하게 하지만 여전히 국가별 서류가 필요하며 무바늘 약물전달 기기 시장에서 점유율 획득을 목표로 하는 진입기업에 전략적인 뉘앙스가 더해집니다.

유럽은 임상적 유용성을 입증하는 가치 기반 상환으로 의미있는 규모를 유지하고 있습니다. 독일은 국내 제약 대기업과 결과에 연동한 가격 설정에 긍정적인 지불자에게 지지되어 지역별 매출에서 최고가 되었습니다. 지속가능성이 요구되는 가운데 EU의 그린딜 목표에 따라 재활용 가능한 인클로저와 바이오 유래 폴리머의 연구 개발에 박차가 걸리고 있습니다. 자동 주사기는 유리 프리필드 주사기를 대체합니다. 유럽 의약청은 환자 보고 결과에 중점을 두어 승인 시 인체공학적 시험의 중요성을 높이고 무바늘 약물전달 기기 시장 전반에 걸쳐 전체 기기 설계를 장려합니다.

The needle free drug delivery devices market is valued at USD 15.60 billion in 2025 and is forecast to reach USD 22.59 billion by 2030, expanding at a 7.67% CAGR.

Robust demand for self-administration, rising biologics pipelines, and sustained investment in digital-health integrations are powering this upward trajectory. North America contributes the largest regional share, while Asia-Pacific is growing fastest as healthcare access broadens and chronic-disease incidence rises. Jet injectors maintain a dominant device position, yet microneedle patches are scaling rapidly as 3D printing and biodegradable materials unlock new formulation possibilities. Oncology therapies anchor the highest application growth as precision-medicine strategies demand delivery platforms that minimize systemic toxicity and elevate adherence. Regulatory complexity remains the primary headwind, though firms that master evolving guidance can secure durable competitive advantages.

Global prevalence of diabetes, cancer, and cardiovascular disease is resetting delivery priorities toward safer, pain-free platforms. In 2024, U.S. healthcare facilities recorded 600,000-800,000 needlestick injuries, each costing USD 500-3,000 in follow-up care. Needle free injectors reduce sharps exposure and align with chronic-disease protocols requiring lifelong therapy. Manufacturers now design devices expressly for chronic use cases, such as wearable injectors that maintain flow rates for up to 72 hours. These patient-centric designs underpin sustained demand within the needle free drug delivery devices market.

Home-based models are reshaping care economics, and 87.5% of users of the enFuse on-body system report confidence in self-therapy. Health systems benefit from lower facility overhead, while patients gain autonomy. Human-factors engineering-ergonomic triggers, tactile feedback, and intuitive graphical prompts-has become a critical differentiator, enabling firms to capture share in the expanding needle free drug delivery devices market.

The U.S. FDA's 2024 Essential Drug Delivery Outputs guidance introduced rigorous verification protocols for combination products, extending development cycles and raising costs. Divergent rules in the EU and Asia compel firms to engineer region-specific versions, fragmenting R&D budgets. Smaller innovators feel the strain most acutely, slowing novel entrants into the needle-free drug delivery devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Jet injectors captured 61.3% of 2024 revenue, reflecting their vaccine-ready versatility and capacity to handle high-viscosity biologics. This dominance secures a sizeable portion of the needle-free drug delivery devices market for mature players. Microneedle patches, however, are projected to expand at 10.63% CAGR, fueled by dissolvable polymers that leave no sharps waste and enhanced permeability, which have been proven to raise bioavailability by up to 40%.

Form-factor innovation is redefining competitive boundaries. Laser-assisted systems and electroporation devices serve niche protein and gene-therapy pipelines, underscoring the breadth of the needle-free drug delivery devices market. 3D-printed molds let manufacturers iterate microstructure rapidly, trimming prototype cycles and reinforcing first-mover advantages.

Disposable formats hold 66.8% share, but environmental mandates and cost-containment pressures spur a 9.15% CAGR for reusable devices. Life-cycle analyses indicate potential 85% waste reduction versus single-use injectors. The needle free drug delivery devices market increasingly rewards designs featuring detachable drug cartridges and autoclavable housings.

User-centered evaluations reveal higher confidence scores when tactile cues and mobile-app tutorials guide dose delivery. Smart sensors embedded in reusable systems transmit administration data to cloud dashboards, expanding value beyond sustainability to adherence intelligence.

Needle-Free Drug Delivery Devices Market Report is Segmented by Device Type (Jet Injectors, Inhalers, Transdermal Patches, and More), Usability (Disposable and Reusable Systems), Product Fill Type (Prefilled and Filable Injectors), Site of Delivery (Intradermal, Subcuatneous and More), Application (Insulin Delivery, Vaccine Delivery and More) and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

North America commands 38.6% of 2024 revenue thanks to entrenched biopharma R&D, high chronic-disease prevalence, and reimbursement for advanced delivery systems. The FDA approved 32% more combination products in 2024 versus 2023, signaling a favorable pipeline for the needle-free drug delivery devices market. Clinical data from MIT showed microneedle patches deliver biologics with 40% higher bioavailability than conventional subcutaneous routes. Digital-health maturity underpins rapid uptake of connected injectors that broadcast adherence metrics to provider dashboards.

Asia-Pacific is the fastest-growing arena at 10.50% CAGR as China and India scale chronic-care infrastructure. Local firms increasingly develop proprietary jet injectors and microneedles, signaling a shift from contract manufacturing to innovation leadership. Japan's super-aged demographic drives demand for low-force actuators suited to frail skin, influencing regional design cues. Regulatory harmonization under Asia-Pacific Economic Cooperation frameworks eases cross-border rollout but still requires country-specific dossiers, adding strategic nuance for entrants aiming to capture share in the needle free drug delivery devices market.

Europe sustains meaningful scale with value-based reimbursement that rewards demonstrable clinical benefit. Germany tops regional revenue, buoyed by domestic pharma giants and a payer environment receptive to outcome-linked pricing. Sustainability imperatives spur R&D into recyclable housings and bio-derived polymers, aligning with EU Green Deal targets. Autoinjectors are replacing glass prefilled syringes as safety-engineered designs mitigate accidental sticks. The European Medicines Agency's focus on patient-reported outcomes elevates importance of ergonomic testing during approvals, encouraging holistic device design across the needle free drug delivery devices market.