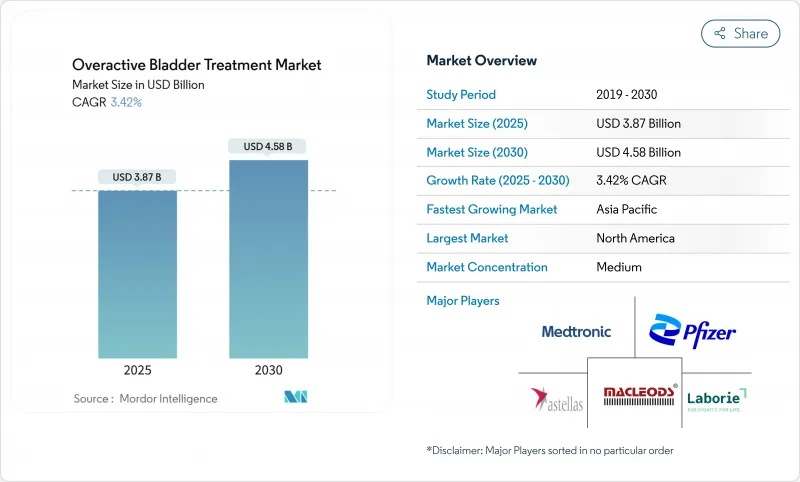

과민성 방광 치료 시장은 2025년에 38억 7,000만 달러로 추정되고, 2030년에는 45억 8,000만 달러에 이를 전망이며, CAGR 3.42%로 성장할 것으로 예측됩니다.

인구 고령화, B3 아드레날린 작용제로의 임상 이동, 장치 기반 선택의 확대가 수요를 지원합니다. 항콜린제는 여전히 규모의 이점을 제공하지만 처방전 변경을 가속화하는 인지 안전성의 역풍에 직면합니다. B3 아고니스트는 신규 승인에 의해 점유율을 확대하고, 신경조절과 보툴리눔툭신(보톡스)의 상환 확대에 의해 서드라인 치료에 대한 액세스가 확대됩니다. 디지털 진단제는 특히 비뇨기과 의사가 부족한 지역에서 더욱 보급되어 기업 통합은 제약 및 의료기기 양쪽의 경쟁 역학을 재구축하고 있습니다.

65세 이상의 과민성 방광 유병률은 30%를 넘고 있으며, 일반 성인에서는 16-18%입니다. 일본에서는 약 1,240만 명의 성인이 증상 관리를 필요로 하고 있으며, 지불자는 비용 효과적인 케어 모델을 우선하고 있습니다. 중국, 한국, 유럽 국가에서 유사한 인구통계학적 변화는 과민성 방광 치료 시장을 확대하는 동시에 의료 제도에 의한 비뇨기과에 대한 투자를 촉진하고 있습니다. 보험제도가 확대되고 배설개조 서비스도 커버되게 되면 약물요법이나 기구를 이용한 치료에 대한 수요가 모든 경제층에서 높아집니다.

옥시부티닌은 65세 이상 여성의 치매 위험을 12% 상승시키는 장기적인 연구 결과가 발표되어 임상의의 B3 작용제에 대한 기울기가 가속화되고 있습니다. 149만 명이 참가한 일본의 코호트에서는 미라베글론과 비베그론에서 치매 위험이 낮은 것으로 확인되었습니다. 2024년 12월, FDA는 전립선 비대증 관련 증상이 있는 남성에게 비베글론을 승인했습니다.

한국의 전국 코호트에서 항콜린제와 B3-효능제의 비교로 치매 발병률이 높은 것이 밝혀졌고 보험 계획의 처방 순위가 변경되었습니다. 미국 메디케어는 현재 인지기능을 온존하는 옵션을 우선하고 기존의 약제량을 억제하는 한편, 신규 메커니즘에 대한 투자를 유도하고 있습니다. 임상의는 증상 완화와 인지 위험을 비교 검토하는 의사 결정 도구를 채택하여 항콜린제의 매출을 감속시키고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

항콜린제의 과민성 방광 치료 시장 규모는 2024년 17억 1,000만 달러에 이르렀고, 총 매출의 44.35%에 해당했습니다. 비용 우위와 지침에 대한 적합성은 항콜린제의 우위를 유지하지만, 인지에 대한 우려 증가는 성장을 억제합니다. B3- 작용제는 2024년에 22.9%를 차지하고, CAGR 8.25%로 확대될 것으로 예측되며, 다른 모든 모달리티를 웃돌았습니다. 비베글론이 전립선 비대증 남성에게 새로운 효능을 추가한 것이 이 급성장의 뒷받침이 되고, 미라베글론의 장기 데이터가 안전성에 대한 인식을 강화하고 있습니다. 보툴리눔툭신(보톡스)는 틈새 지위를 유지하고 있지만, 15년간 74.5%의 패드 완전 중지율을 자랑하고 있으며, 난치성 증례를 끌고 있습니다. 2024년 보스턴 사이언티픽에 의한 악소닉스 인수는 천골신경조절술의 경쟁을 격화시킵니다.

임상 현장에서는 듀록세틴 톨테로진과 같은 하이브리드 프로토콜의 시도가 증가하고 있으며, 혼합 실금 코호트에서는 77.4%의 환자 만족도를 얻고 있습니다. 린코필린을 포함한 식물 유래 후보 약물은 M3 수용체 조절에 초점을 맞춘 탐색적 임상시험에 들어가고 저비용의 혁신적인 레이어를 추가합니다. 특허 절벽이 기존의 연구개발비를 낮추는 가운데 디지털 진단기업과 제약기업의 제휴가 환자의 특정을 가속화시켜 과민성 방광 치료 시장 전체의 치료 흡수를 촉진합니다.

특발성 사례는 2024년 29억 4,000만 달러를 창출하였고, 과민성 방광 치료 시장 점유율은 75.53%에 달할 전망입니다. 합리화된 워크업과 1차 케어에 대한 정통이 일관된 수요를 지지하고 있습니다. 2024년에 9억 5,000만 달러로 평가된 신경원성 사례는 척수 손상, 파킨슨병, 다발성 경화증 집단에서의 모니터링 강화에 힘입어 2030년까지 매년 6.85% 성장할 것으로 예측됩니다. 초음파 가이드 아래 보툴리눔툭신(보톡스) 주사는 절차 위험을 줄이고 의료 제공업체의 채택을 확대합니다. 장비 기반 처방 및 복잡한 약리학적 제형의 프리미엄 가격은 적은 용량을 상쇄하고 환자 1인당 수익을 올리고 제조업체의 마진을 개선합니다.

정책 입안자는 적극적인 신경원성 관리에 의해 요로 감염이나 신 합병증이 억제되어 하류 절약으로 이어지는 것을 지적하고 있습니다. 이러한 경제적 논거는 천골 신경 자극과 경골 신경 자극과 같은 고액 치료에 대한 지불자의 보험 적용을 정당화하는 데 도움이 되며, 과민성 방광 치료 시장에서 신경 원성 수익 풀을 강화하고 있습니다.

북미는 2024년 15억 달러를 생산했으며, 과민성 방광 치료 시장의 38.82%에 해당합니다. 확고한 보험 적용과 B3-효능제의 조기 도입이 수익을 유지하고, 메디케어의 신경조절에 대한 명확한 알고리즘이 장비 채널을 건강하게 유지하고 있습니다. 병원 시스템의 통합은 포뮬러의 활용을 촉진하고 인가 후 인지 기능을 온존하는 새로운 분자의 신속한 전개를 보장합니다.

유럽은 2024년 7월 vibegron의 모든 EU 승인을 통해 2024년에 11억 3,000만 달러의 기여가 평가되었습니다. 라벨링이 통일됨에 따라, 상시 코스트가 합리화되어, 약물 감시 보고도 통일되었습니다. 특히 독일과 북유럽에서는 국가의 의료 서비스가 장기적인 증상 통제에 보상하는 일괄 지불을 시험적으로 도입하고 있으며, 장비 제조업체에 이익을 가져다줍니다.

아시아태평양의 2024년 시장 규모는 8억 7,000만 달러로 평가되었고, 2030년까지 CAGR 7.81%로 성장할 전망이며, 전 지역 중 가장 급속히 확대될 전망입니다. 일본은 고령화가 진행되고 있어 임상시험의 인프라가 갖추어져 있으므로, 가이드라인의 준수가 진행되고 있습니다. 대만과 한국에서는 미라베글론의 지속률이 68.5%인 반면, 항무스카린 약은 60.4%입니다. 중국과 인도에서는 관민 연계에 의한 진단 능력의 향상으로 과활동 방광을 정상적인 노화 현상이 아닌 치료 가능한 질환으로 자리 매김하고 있습니다. 장비 상환 개선과 현지 제조 거점이 인수 비용을 절감하고 과민성 방광 치료 시장에서 신경조절 플랫폼의 침투가 깊어집니다.

The overactive bladder treatment market was valued at USD 3.87 billion in 2025 and is forecast to reach USD 4.58 billion by 2030, advancing at a 3.42% CAGR.

Demand is sustained by population aging, the clinical shift toward B3-adrenergic agonists, and expanding device-based options. Anticholinergics still provide scale advantages but face cognitive-safety headwinds that accelerate prescribing changes. B3-agonists gain share on the back of new approvals, while reimbursement expansion for neuromodulation and botulinum toxin widens access to third-line care. Digital diagnostics further broaden reach, especially in regions with urologist shortages, and corporate consolidation is reshaping competitive dynamics in both pharma and devices.

People aged 65 years and older experience overactive bladder prevalence above 30%, compared with 16-18% in general adult cohorts. In Japan, roughly 12.4 million adults require symptom management, prompting payers to prioritize cost-effective care models. Similar demographic shifts in China, South Korea, and European countries enlarge the overactive bladder treatment market while encouraging health-system investment in urological capacity. As national insurance schemes expand to cover continence services, demand for pharmacologic and device-based therapies rises across all economic strata.

Long-term studies link oxybutynin to a 12% higher dementia risk in women older than 65, accelerating clinician pivot toward B3-agonists. A 1.49-million-participant Japanese cohort confirmed lower cognitive risk with mirabegron and vibegron. The December 2024 FDA approval of vibegron for men with benign prostatic hyperplasia-related symptoms opens a new addressable population and reinforces the safety narrative.

A Korean national cohort revealed increased dementia incidence with anticholinergics versus B3-agonists, triggering formulary re-ranking across insurance plans. U.S. Medicare now favors cognitive-sparing options, constraining legacy drug volumes while directing investment toward novel mechanisms. Clinicians adopt shared-decision tools that weigh symptom relief against cognitive risk, slowing anticholinergic unit sales.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The overactive bladder treatment market size for anticholinergics reached USD 1.71 billion in 2024, equal to 44.35% of total revenue. Cost advantage and guideline familiarity sustain their lead, yet mounting cognitive concerns restrain growth. B3-agonists captured 22.9% in 2024 and are forecast to expand at an 8.25% CAGR, outpacing all other modalities. Vibegron's new indication for men with benign prostatic hyperplasia underpins this surge, while mirabegron's long-term data reinforce safety perceptions. Botulinum toxin retains niche status but boasts 74.5% complete pad discontinuation over 15 years, attracting refractory cases. Boston Scientific's 2024 purchase of Axonics intensifies competition in sacral neuromodulation, promising next-generation lead technology and rechargeable IPGs that lengthen device life cycles.

Clinical practice increasingly trials hybrid protocols-such as duloxetine-tolterodine-returning 77.4% patient satisfaction in mixed incontinence cohorts. Plant-derived candidates, including rhynchophylline, enter exploratory trials focused on M3 receptor modulation, adding a low-cost innovation layer. As patent cliffs depress traditional R&D spend, alliances between digital diagnostic firms and pharma players accelerate patient identification, amplifying therapy uptake across the overactive bladder treatment market.

Idiopathic presentations generated USD 2.94 billion in 2024, translating to a 75.53% share within the overactive bladder treatment market. Streamlined work-ups and primary-care familiarity underpin consistent demand. Neurogenic cases, valued at USD 0.95 billion in 2024, will grow 6.85% annually through 2030, fueled by heightened surveillance in spinal cord injury, Parkinson's disease, and multiple sclerosis populations. Ultrasound-guided botulinum toxin injections reduce procedural risks, broadening provider adoption. Premium pricing for device-based regimens and complex pharmacologic formulations offsets smaller volumes, lifting revenue per patient and improving manufacturer margins.

Policy makers note that aggressive neurogenic management curbs urinary tract infections and renal complications, generating downstream savings. These economic arguments help justify payer coverage for high-ticket interventions such as sacral and tibial nerve stimulation, fortifying the neurogenic revenue pool in the overactive bladder treatment market.

The Overactive Bladder Treatment Market Report is Segmented by Therapy (Anticholinergics, Botulinum Toxin Injections, Intravesical Instillation, and More), Disease Type (Idiopathic Overactive Bladder and Neurogenic Overactive Bladder), Route of Administration (Oral, Transdermal, and More), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America produced USD 1.50 billion in 2024, equivalent to 38.82% of the overactive bladder treatment market. Robust insurance coverage and early uptake of B3-agonists sustain revenue, while Medicare's clear algorithms for neuromodulation keep device channels healthy. Hospital system consolidation encourages formulary leverage, ensuring rapid deployment of new cognitive-sparing molecules once licensed.

Europe contributed USD 1.13 billion in 2024, buttressed by the July 2024 pan-EU authorization for vibegron. Harmonized labeling streamlines launch costs and unifies pharmacovigilance reporting. National health services, particularly in Germany and the Nordics, pilot bundled payments that reward longitudinal symptom control, benefiting device makers.

Asia-Pacific, valued at USD 0.87 billion in 2024, is on track for a 7.81% CAGR to 2030, the fastest expansion among all regions. Japan's advanced aging profile and clinical trial infrastructure elevate guideline compliance, while Taiwan and South Korea report 68.5% persistence on mirabegron versus 60.4% for antimuscarinics. China and India ramp diagnostic capacity through public-private partnerships, framing overactive bladder as a treatable disorder rather than a normal aging outcome. Improved device reimbursement and local manufacturing hubs shrink acquisition costs, deepening penetration of neuromodulation platforms within the overactive bladder treatment market.