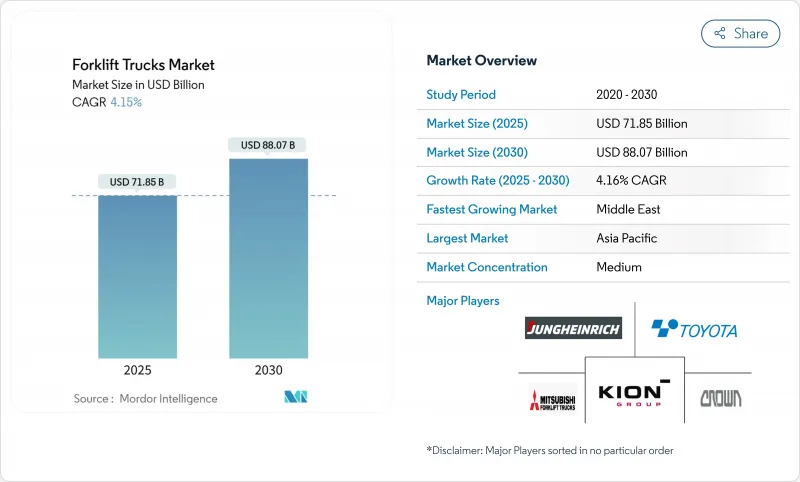

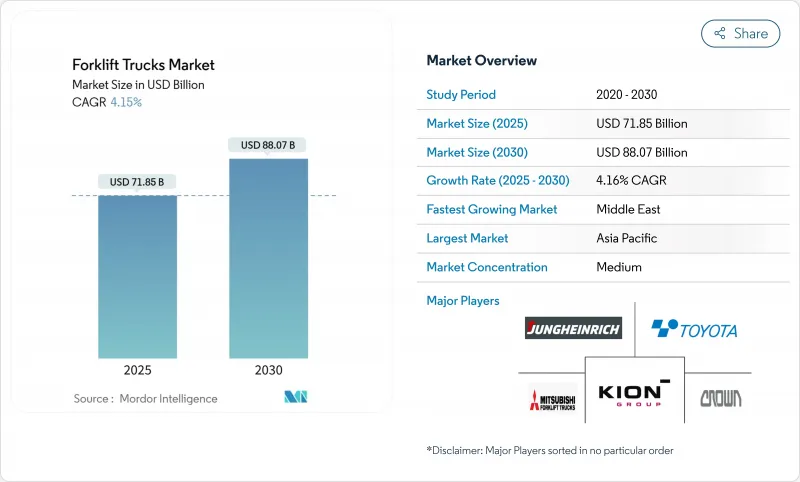

지게차 시장 규모는 2025년에 718억 5,000만 달러로 추정되고, 2030년에는 CAGR 4.16%로 성장할 전망이며, 880억 7,000만 달러에 이를 것으로 예측됩니다.

창고의 자동화에 대한 건전한 자본 지출, 보다 엄격한 배출 규제, 그리고 노후화된 플릿의 꾸준한 교환 사이클이 거시경제 센티먼트가 혼잡을 계속해도 이 전진을 지지하고 있습니다. 지게차 시장에서 내연식에서 전기 및 수소 연료전지 모델로의 축족은 파워트레인 공급망, 충전 인프라 및 애프터 판매 수익원을 재구성하기 때문에 유일하게 가장 큰 구조적 변화입니다. 리튬 이온 배터리는 배터리를 교체하지 않고 멀티 시프트 성능을 실현함으로써 이 시프트를 가속화하고 있는 한편, 수소 기술은 빠른 연료 보급이 중요한 장면에서 지지를 모으고 있습니다. 병행하여 중동과 동남아시아와 같은 고성장 지역은 성숙 지역에서의 경제 성장 둔화에도 불구하고 지게차 시장이 기세를 유지할 수 있도록 그린필드 물류 허브에서 첨단 장비를 채택하고 있습니다.

온라인 소매의 급속한 성장은 미국과 캐나다 전역에서 기록적인 창고 건설에 박차를 가하고 있습니다. 미국 전자상거래 매출은 2024년 전년 대비 8.2% 증가한 1조 1,900억 달러에 달할 전망입니다. 이러한 유닛이 창고 관리 소프트웨어와 통합되어 처리 능력을 높이고 지속적인 노동력 부족을 완화하기 때문에 자율형, 반자율형 트럭 수요가 가장 급속히 높아지고 있습니다. 그 결과, 기술 주도의 업그레이드 사이클이 태어나 GDP 성장률이 둔화해도 출하 대수는 계속 증가합니다.

독일, 프랑스, 북유럽의 콜드 스토어 오퍼레이터는 리튬 셀이 -30℃에서 95% 이상의 용량을 유지하고 충전 시간을 1-2시간으로 단축하고 배터리 수명을 3배로 하기 때문에 납 축전지식에서 리튬 이온식 트럭으로 전환하고 있습니다. 콜드체인의 음식 및 음료 부문은 이미 CAGR 4.9%를 초과했으며 냉장 창고 내에서 산성 가스 노출을 제한하는 배출 규제가 시프트를 강화하고 있습니다. 2025년까지 리튬 이온 유닛은 유럽 냉장 창고에서 새로운 전동 지게차 판매의 40%를 차지합니다. 배터리 임대와 텔레매틱스 지원을 번들로 제공하는 OEM은 기존 솔루션에 대한 총 비용의 이점을 입증함으로써 더 높은 마진을 얻습니다.

전기 모델은 동등한 ICE 유닛에 대해 20-40% 구매 프리미엄을 수반합니다. 클래스 i의 전동 트럭은 평균 36,000달러인 반면 ICE는 28,000달러로 소규모 기업에서의 보급을 제한하고 있습니다. 이 가격 차이는 자율 주행형 트럭에서 더욱 심해지며, 센서 스위트는 설치 비용을 100,000달러 이상으로 늘릴 수 있습니다. 배터리리스, 페이퍼 유스 계약, 플릿 애즈 어 서비스 패키지 등 대체 금융은 보급되고 있지만, 신용 액세스가 어려운 지역에서는 아직 초기 단계에 그치고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

수소 연료전지 모델은 다른 어떤 파워트레인보다 빠르게 확대되고 있으며 2030년까지 연평균 복합 성장률(CAGR) 10.60%로 확대될 전망입니다. 지게차 시장은 수소의 연료 보급이 3분이면 ICE의 가동 시간에 필적하는 반면 국소적인 배출이 제로이기 때문에 이익을 얻고 있습니다. 플러그 파워사는 300개 소에 6만 대 이상의 연료전지를 배치하여 상업적 가능성을 증명하고 있습니다. 2024년에는 69.20%의 전동 점유율이 지게차 시장을 독점하고 있지만, 캘리포니아, 중국, EU의 규제 기한이 전동화 플릿에의 축족을 가속하고 있습니다.

ICE 제조업체는 하이브리드 구성과 대체 연료로 대응하고 있지만, 엔진 효율 향상을 반복하는 것은 비용적으로 곤란하다는 것이 판명되었습니다. 배터리 비용 동향은 하강하는 경향이 있으며, 연료 공급업체와 물류 시설 운영자 간 수소 배급 파트너십은 2027년까지 배급 비용 절감을 약속합니다. 그 결과, 파워트레인의 다양화가 경쟁력을 높여, 셀, 스택, 충전기, 소프트웨어 공급업체와의 제휴를 확보한 브랜드는 보상됩니다.

클래스 III 팔레트 무버는 마지막 마일 크로스독 네트워크를 통해 44.70% 시장 점유율을 차지하고 있지만, 이러한 트럭은 상대적으로 상품화되어 마진 압력이 강해지고 있습니다. 수요가 다양해지면서 OEM은 마이크로 완성 센터용 컴팩트한 3륜 전동부터 컨테이너 야드용 무거운 18톤 리그까지 다양한 SKU 믹스를 관리해야 합니다. 따라서 클래스 간 전자 제품의 표준화는 비용 절감의 중요한 전략이 되었습니다.

Class i의 전동 라이더는 CAGR 4.53%를 기록했으며 배터리 교체 없이 다-시프트 실내 작업을 지원하는 리튬 이온 기술로 추진되었습니다. 협통로 클래스 II 유닛의 지게차 시장 규모도 전자상거래 시설이 높이 12m 이상의 래킹 시스템을 채용하여 보다 강화된 리프트 높이와 안정성을 가진 트럭을 요구하고 있기 때문에 확대하고 있습니다.

아시아태평양은 중국, 일본, 인도가 자동 창고와 스마트 공장에 많은 투자를 했기 때문에 2024년 지게차 시장 수익의 45.10%를 차지했습니다. 국내 브랜드는 국내 및 동남아시아에서 확대하기 위해 비용 우위와 정부 인센티브를 활용하여 유럽과 미국의 기존 기업과의 경쟁을 높이고 있습니다. 일본과 한국의 성숙한 플릿은 강제적인 교환 사이클에 들어가고 있으며, 엄격한 배기가스 규제에 의해 신규 구입은 리튬 이온과 수소 유닛으로 기울어지고 있습니다. 지역 종합적 경제 협력으로 이어지는 화물 회랑은 국경을 넘어서는 표준화를 촉진하고 대응 가능한 수요를 더욱 확대합니다.

중동은 사우디아라비아, UAE, 카타르가 장기적인 국가 비전 아래, 항만, 철도 조차장, 사막 물류 허브를 건설하고 있기 때문에 2030년까지 연평균 복합 성장률(CAGR)이 6.12%로 예측되는 가장 급성장하고 있는 지역입니다. 중국과 한국의 OEM은 지역의 자유무역구를 이용해 현지에서 유닛을 조립하는 한편, 유럽 브랜드는 애프터서비스와 자율주행 옵션으로 차별화를 도모하고 있습니다.

북미는 여전히 기술의 기수입니다. 제조업 리쇼어링, 전자상거래 완성, 캘리포니아 주 제로 방출 지게차 규정은 전기 클래스 i 및 수소 클래스 V 수요를 지원합니다. 미국은 텔레매틱스의 채용에서도 선도하고 있으며, 플릿 매니저는 배터리의 건강 상태, 운전자의 행동, 유지 보수 간격을 추적하여 가동률을 높이고 있습니다. 캐나다는 브리티시 컬럼비아와 온타리오의 새로운 내륙 항구에서 도움을 받아 비슷한 패턴을 추구하고 있습니다.

유럽의 지게차 시장은 노동력 가용성이 가혹한 가운데 제로 방출 파워트레인으로의 전환을 계속하고 있습니다. 40만 명이 넘는 공인 오퍼레이터의 기능 부족이 특히 북유럽에서 자동화 파일럿을 추진합니다. 독일은 리튬 이온 배터리의 재활용 및 세컨드라이프 용도 분야의 연구 개발을 선도하고 순환 설비 경제를 지원합니다. 동유럽 국가들은 자동차와 일렉트로닉스 공급망이 대륙의 핵심 소비자 시장에 가까워지면서 평균을 뛰어넘는 생산량의 성장을 보여줍니다.

The forklift trucks market size stands at USD 71.85 billion in 2025 and is forecast to reach USD 88.07 billion by 2030 at a 4.16% CAGR.

Healthy capital spending on warehouse automation, stricter emission rules, and a steady replacement cycle for aging fleets underpin this advance even as macro-economic sentiment remains mixed. Within the forklift trucks market, the pivot from internal-combustion to electric and hydrogen fuel-cell models is the single biggest structural change because it reshapes power-train supply chains, charging infrastructure, and after-sales revenue streams. Lithium-ion batteries are accelerating that shift by delivering multi-shift performance without battery swaps, while hydrogen technology is gaining traction where rapid refueling is critical. In parallel, high-growth geographies such as the Middle East and Southeast Asia are adopting advanced equipment at greenfield logistics hubs, ensuring that the forklift trucks market retains momentum despite slowing economic growth in mature regions.

Rapid on-line retail growth is fueling record warehouse construction across the United States and Canada. US eCommerce sales stood at $1.19 trillion in 2024, an increase of 8.2% from the previous year Autonomous and semi-autonomous truck demand is rising fastest because these units integrate with warehouse-management software, boost throughput, and mitigate a persistent labor shortage. The result is a technology-led upgrade cycle that keeps unit shipments rising even when headline GDP growth softens.

Cold-store operators across Germany, France, and the Nordics are switching from lead-acid to lithium-ion powered trucks because lithium cells retain more than 95% capacity at -30 °C, cut charging hours to 1-2, and triple battery life. The cold-chain food & beverage segment already tops 4.9% CAGR, and emissions rules limiting acid-gas exposure inside chilled warehouses are reinforcing the shift. By 2025 lithium-ion units represent 40% of new electric forklift sales in European cold rooms as operators prioritize uptime and reduced battery maintenance . OEMs that bundle battery leasing and telematics support capture higher margins by proving total-cost advantages over legacy solutions.

Electric models carry a 20-40% purchase premium over comparable ICE units. A Class I electric truck averages USD 36,000 versus USD 28,000 for ICE, limiting take-up among small enterprises . The price gap is steeper in autonomous variants, whose sensor suites can lift installed cost above USD 100,000. Alternative financing, such as battery leasing, pay-per-use contracts, and fleet-as-a-service packages, is gaining traction but remains nascent in regions where credit access is tight.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hydrogen fuel-cell models are scaling more rapidly than any other power-train, expanding at 10.60% CAGR through 2030. The forklift trucks market benefits because hydrogen refueling takes 3 minutes, matching ICE uptime while offering zero localized emissions. Plug Power has deployed over 60,000 fuel cells across 300 sites, proving commercial viability. Although the 69.20% electric share still dominates the forklift trucks market in 2024, regulatory deadlines in California, China, and the EU accelerate the pivot to electrified fleets.

ICE manufacturers respond with hybrid configurations and alternative fuels, but achieving repeated engine efficiency gains is proving to be cost-prohibitive. Battery cost curves are trending downward, and hydrogen distribution partnerships between fuel suppliers and logistics park operators promise lower dispensing costs by 2027. Consequently, power-train diversification enhances competitive intensity, rewarding brands that secure supplier alliances for cells, stacks, chargers, and software.

Class III pallet movers dominate with 44.70% market share due to last-mile cross-dock networks, but margin pressure is intensifying because these trucks are relatively commoditized. Demand diversification forces OEMs to manage a broad SKU mix ranging from compact three-wheel electrics for micro-fulfilment centers to heavy 18-ton rigs for container yards. Electronics standardization across classes is therefore a key cost-reduction strategy.

Class I electric riders book 4.53% CAGR, propelled by lithium-ion technology that supports multi-shift indoor operations without battery swaps. The forklift trucks market size for narrow-aisle Class II units is also expanding as e-commerce facilities adopt racking systems above 12 m high, demanding trucks with enhanced lift height and stability.

The Forklift Trucks Market Report is Segmented by Power-Train Type (Internal Combustion Engine, Electric and More), Vehicle Class (Class I, Class II and More), Load Capacity (Less Than 5 Tons, 5-15 Tons and More), End-User Industry (Manufacturing, Logistics and Warehousing and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Asia Pacific held 45.10% of the forklift trucks market revenue in 2024 as China, Japan, and India invested heavily in automated warehousing and smart factories. Domestic brands leverage cost advantages and government incentives to expand at home and Southeast Asia, heightening competition for European and U.S. incumbents. Mature fleets in Japan and South Korea are entering mandatory replacement cycles, and strict emission caps tilt new purchases toward lithium-ion or hydrogen units. Freight corridors linked to the Regional Comprehensive Economic Partnership foster cross-border standardization that further enlarges addressable demand.

The Middle East is the fastest-growing region, projected at 6.12% CAGR to 2030, as Saudi Arabia, UAE, and Qatar build ports, rail yards, and desert distribution hubs under long-range national visions. Chinese and Korean OEMs use regional free-trade zones to assemble units locally, while European brands differentiate on after-sales service and autonomous options.

North America remains a technology bellwether. Manufacturing reshoring, e-commerce fulfillment, and California's zero-emission forklift regulation combine to sustain demand for electric Class I and hydrogen Class V machines. The United States also leads telematics adoption, with fleet managers tracking battery health, operator behavior, and maintenance intervals to boost utilization. Canada follows similar patterns, helped by new inland ports in British Columbia and Ontario.

Europe's forklift trucks market continues to transition to zero-emission power-trains amid tight labor availability. Skill shortages exceeding 400,000 certified operators drive automation pilots, especially in the Nordics. Germany leads R&D on lithium-ion battery recycling and second-life applications, supporting a circular equipment economy. Eastern European member states exhibit above-average unit growth as automotive and electronics supply chains migrate closer to the continent's core consumer markets.