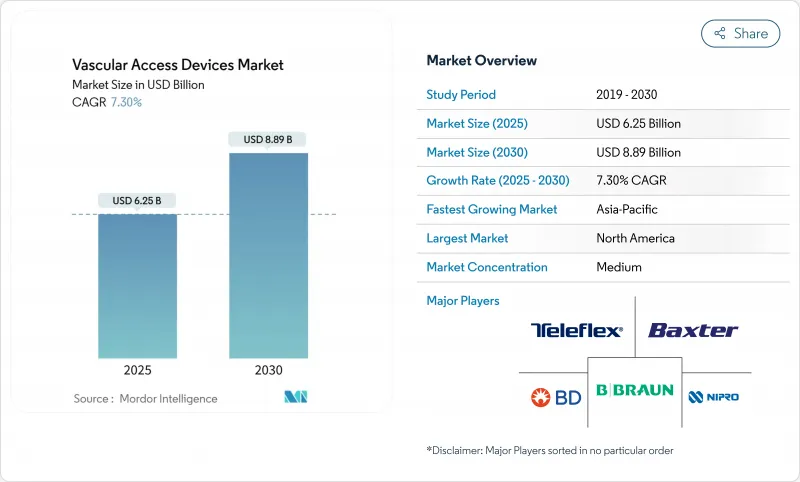

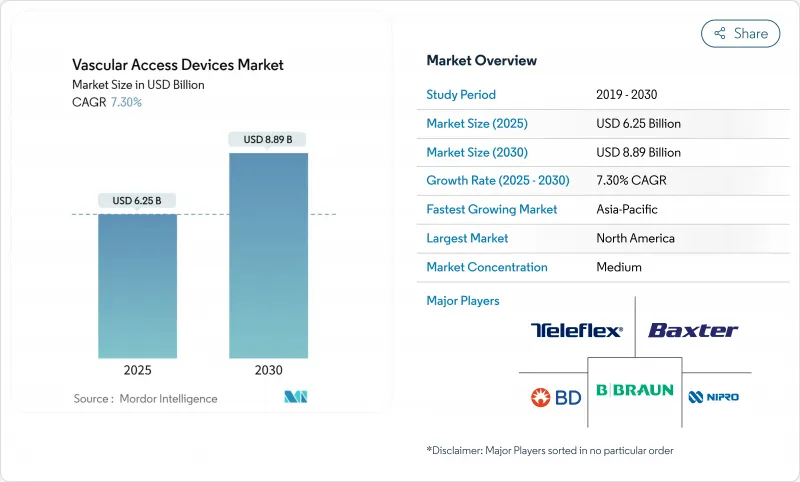

세계의 혈관 접근 기기 시장은 2025년 62억 5,000만 달러로 추정되고, 2030년 88억 9,000만 달러에 이를 전망이며, CAGR 7.30%로 성장할 것으로 예측됩니다.

이 확장은 감염 예방, 재료 내구성 및 절차의 효율성을 우선하는 가치 기반 혁신을 위한 헬스케어 제공업체의 축족을 반영합니다. 만성 질환 부담 증가, 초음파 가이드 하 삽입의 광범위한 채용, 외래 환자 관리 모델로의 전환은 총체적으로 지속적인 수요를 지원합니다. 동시에 친수성 바이오 재료 및 항균 코팅의 진보는 제품 차별화를 강화하고 공급망 재조달은 제조업체의 원재료 위험을 줄이는 데 도움이 됩니다. 따라서 경쟁 역학에서는 제조 규모의 확대와 신속한 기술 전개의 조합이 가능한 기업이 유리해지고, 혈관 접근 기기 시장은 안정된 성장 궤도를 유지하고 있습니다.

당뇨병과 심부전과 같은 만성 질환은 세계에서 장기적인 정맥 내 치료의 필요성을 높이고 있습니다. 재택 수액은 현재 연간 320만 명 이상의 미국인에게 사용되고 있으며, 그 지출액은 1,100억 달러를 넘어 매년 5-7% 증가하고 있습니다. 내구성있는 미드라인 카테터와 체류 시간이 긴 말초 장치는 합병증 위험을 줄이고 보다 광범위한 외래 환자 관리를 지원합니다. 혈관 접근의 MIMIX와 같은 친수성 바이오머티리얼은 고장률을 감소시키고, 1,000개의 바닥 병원에서는 연간 180만 달러를 절약할 수 있습니다. 이러한 경제성으로 인해 혈관 접근 기기는 일용품에서 필수적인 인프라로 승화됩니다.

개별화된 종양학 요법은 빈번하게 샘플링이 가능하면서 베시클란트 약물에 내성이 있는 중심 정맥 카테터에 의존하게 되어 왔습니다. 말초 삽입형 중심 정맥 카테터(PICC)는 외래 환자의 유연성을 향상시켜 치료 지연과 입원 기간을 단축합니다. 클로르헥시딘을 함침시킨 드레싱재는 시험에 있어서 혈류 감염을 52% 감소시켜, 감염 방지 기구의 프리미엄 가격을 지지하고 있습니다.

집중치료실에서는 카테터 사용일수 1,000일당 4.9건의 감염을 기록하고 있으며, 에피소드마다 치료비 및 사망 위험이 증가하고 있습니다. 디지털 대시보드는 CLABSI 발생률을 최대 73%까지 줄이지만 자본 투자가 필요합니다. 클로르헥시딘 드레싱은 카테터의 콜로니 형성을 54% 감소시킵니다. 그 결과, 병원은 통합된 감염 제어 번들을 선호하게 되었고, 고급 코팅이 없는 상품 공급업체를 압박하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

2024년 혈관 접근 기기 시장 점유율은 중앙 장치가 56.78%를 차지했습니다. PICC는 여전히 암 치료 및 치명적인 치료 현장에서 주력이며, 터널형 카테터는 1년간의 치료를 지원합니다. 병원은 상환 압력에 의해 감염 위험 및 체류 시간의 조사가 강화되는 가운데 신뢰할 수 있는 흐름과 재삽입 빈도가 낮음을 평가했습니다.

그러나 말초 카테터는 CAGR 7.89%로 가장 빠르게 성장하고 있습니다. 체류 시간의 연장 설계는 표준 PIVC와 PICC 간극을 메우고 중간 치료 비용과 합병증 발생률을 줄입니다. B. Braun의 Introcan Safety 2와 같은 FDA 승인 장치는 중앙값으로 5.7일까지 연장됩니다. 초음파 가이드 하에서의 유치가 임상적으로 널리 받아들여지고, 항균성 폴리우레탄의 업그레이드에 의해 제품의 차별화가 더욱 진행되고 있습니다. 외래 환자의 주입량이 증가함에 따라 말초 기술 혁신이 혈관 접근 기기 시장을 더욱 견인하게 될 것으로 보입니다.

약물 투여는 2024년 매출의 39.89%를 차지했으며, 안전한 정맥 내 약물 전달의 필수적인 역할을 뒷받침합니다. 복잡한 생물학적 제형, 화학요법 칵테일, 고삼투 용액은 무결성을 손상시키지 않고 반복적으로 접근할 수 있는 견고한 중심 라인과 포트가 필요합니다. 코팅된 루멘과 내압 허브가 표준이 되어 가격 상승을 지원합니다.

진단 및 검사는 정밀의료 프로토콜이 연속 바이오마커 샘플링을 요구하고 있기 때문에 CAGR 7.97%를 보일 것으로 예측됩니다. 포인트 오브 케어 기기는 소요 시간을 단축하기 때문에 용혈률이 낮고 채혈이 용이한 카테터가 병원의 지지를 모으고 있습니다. 멀티루멘 구성과 AI 최적화 지오메트리를 통합하는 제조업체는 구체적인 워크플로우를 절약하고 혈관 접근 기기 시장에서 경쟁력을 강화합니다.

북미는 정교한 헬스케어 인프라 및 감염 저감 기술에 보답하는 보험 구성을 배경으로 2024년 매출의 40.21%를 차지했습니다. BD는 2024년 1,000만 달러 이상을 투자하여 미국에서 카테터 생산을 확대하고 연간 수억 병을 추가하여 국내 공급의 회복력을 강화했습니다. Termo는 푸에르토리코의 Angio Seal의 생산 능력 증대에 3,000만 달러를 기록해, 이 지역의 제조업의 견인력을 강조하고 있습니다.

아시아태평양의 CAGR은 2030년까지 8.23%로 예측되며, 이는 만성 질환 증가와 헬스케어 지출 증가를 반영하고 있습니다. 중국의 가치 기준 조달로의 전환은 가격 압력이지만, 국내 기업은 국내 마진의 압축을 상쇄하기 위해 수출 시장에 눈을 돌리고 있습니다. 일본 본사의 Termo는 회사의 리카 미드 클램프 플랫폼이 지역 내 98개 시설에 도입되어 100개 시설의 달성에 가까워지고 있다고 보고했습니다.

유럽에서는 엄격한 감염 예방 의무와 HTA의 조기 도입으로 견고한 설치 기반이 유지되고 있습니다. 한편 중동의 의료시스템 구축과 남미의 경기 회복에 의해 특히 공적보험사가 외래 수액을 지원하고 있는 지역에서는 고성장의 포켓이 형성되고 있습니다. 지정학적 마찰 및 원재료의 제약이 계속되고 있기 때문에 기업은 멀티 허브 조달 모델을 개발해, 혈관 접근 기기 시장이 혼란 없이 다양한 지역 수요에 대응할 수 있도록 하고 있습니다.

The global vascular access devices market stands at USD 6.25 billion in 2025 and is forecast to reach USD 8.89 billion by 2030, advancing at a 7.30% CAGR.

This expansion reflects healthcare providers' pivot toward value-based innovation that prioritizes infection prevention, material durability and procedural efficiency. A rising chronic disease burden, broader adoption of ultrasound-guided insertion and the shift to outpatient care models collectively underpin sustained demand. At the same time, advances in hydrophilic biomaterials and antimicrobial coatings intensify product differentiation, while supply-chain reshoring helps manufacturers mitigate raw-material risk. Competitive dynamics therefore favor firms able to pair scale manufacturing with rapid technology roll-outs, keeping the vascular access devices market on a steady growth trajectory.

Chronic conditions such as diabetes and heart failure are driving long-term intravenous treatment requirements worldwide. Home infusion now serves more than 3.2 million Americans annually, with spending exceeding USD 110 billion and rising 5-7% each year. Durable midline catheters and extended-dwell peripheral devices lower complication risk, supporting broader outpatient management. Hydrophilic biomaterials like Access Vascular's MIMIX reduce failure rates and can save a 1,000-bed hospital USD 1.8 million a year. These economics elevate vascular access devices from commodity supplies to essential infrastructure.

Personalized oncology regimens increasingly depend on central venous catheters that tolerate vesicant drugs while permitting frequent sampling . Peripherally inserted central catheters (PICCs) improve outpatient flexibility, cutting treatment delays and hospital stays. Chlorhexidine-impregnated dressings have trimmed bloodstream infections by 52% in trials, underpinning premium pricing for infection-resistant devices .

Intensive-care units still record 4.9 infections per 1,000 catheter days, with every episode adding treatment cost and mortality risk. Digital dashboards cut CLABSI rates by up to 73% but require capital investment. Chlorhexidine dressings reduce catheter colonization by 54%. Hospitals consequently favor integrated infection-control bundles, squeezing commodity vendors that lack advanced coatings.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Central devices captured 56.78% of vascular access devices market share in 2024. PICCs remain the workhorse for oncology and critical-care settings, whereas tunneled catheters support year-long therapies. Hospitals value their reliable flow and lower reinsertion frequency, even as reimbursement pressures intensify scrutiny of infection risk and dwell time.

Peripheral catheters, however, are the fastest-growing class at a 7.89% CAGR. Extended-dwell designs bridge the gap between standard PIVCs and PICCs, reducing cost and complication rates for intermediate therapies. FDA-cleared devices such as B. Braun's Introcan Safety 2 extend median dwell to 5.7 days. Ultrasound-guided placement has broadened clinical acceptance, and antimicrobial polyurethane upgrades further differentiate offerings. As outpatient infusion volumes swell, peripheral innovations are positioned to gain additional vascular access devices market traction.

Medication administration commanded 39.89% of 2024 revenue, underlining the indispensable role of safe intravenous drug delivery. Complex biologics, chemotherapy cocktails and high-osmolar solutions necessitate robust central lines and ports capable of repeated access without integrity loss. Coated lumens and pressure-tolerant hubs have become standard, supporting price premiums.

Diagnostics and testing is forecast to grow at a 7.97% CAGR as precision-medicine protocols demand serial biomarker sampling. Point-of-care devices shorten turnaround times, spurring hospitals to favor catheters with low hemolysis rates and easy blood-draw access. Manufacturers integrating multi-lumen configurations and AI-optimized geometries offer tangible workflow savings, strengthening competitive positioning within the vascular access devices market.

The Vascular Access Device Market is Segmented by Device Type (Central Vascular Access Devices and Peripheral Vascular Access Devices), Application (Medication or Drug Administration, Fluid and Nutrition Administration, and More), End User (Hospitals & Clinics, and More), Material (Polyurethane, Silicone, and Others), and Geography (North America and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America commanded 40.21% of 2024 revenue on the back of sophisticated healthcare infrastructure and an insurance mix that rewards infection-reduction technologies. BD invested more than USD 10 million in 2024 to expand U.S. catheter production, adding hundreds of millions of units annually and reinforcing domestic supply resilience. Terumo earmarked USD 30 million for Angio-Seal capacity in Puerto Rico, underscoring the region's manufacturing pull.

Asia-Pacific is projected to post an 8.23% CAGR through 2030, reflecting rising chronic disease prevalence and healthcare spending. China's shift to value-based procurement is exerting price pressure, yet local champions eye export markets to offset domestic margin compression. Japan-headquartered Terumo reported that its Rika mid-clamp platform is now installed in 98 centers across the region, nearing its 100-site milestone.

Europe maintains a robust installed base driven by strict infection-prevention mandates and early HTA adoption. Meanwhile, Middle Eastern health-system build-outs and South American economic recovery create pockets of high growth, especially where public insurers support outpatient infusion. Ongoing geopolitical frictions and raw-material constraints are encouraging firms to develop multi-hub sourcing models so the vascular access devices market can meet varied regional demand without disruption.