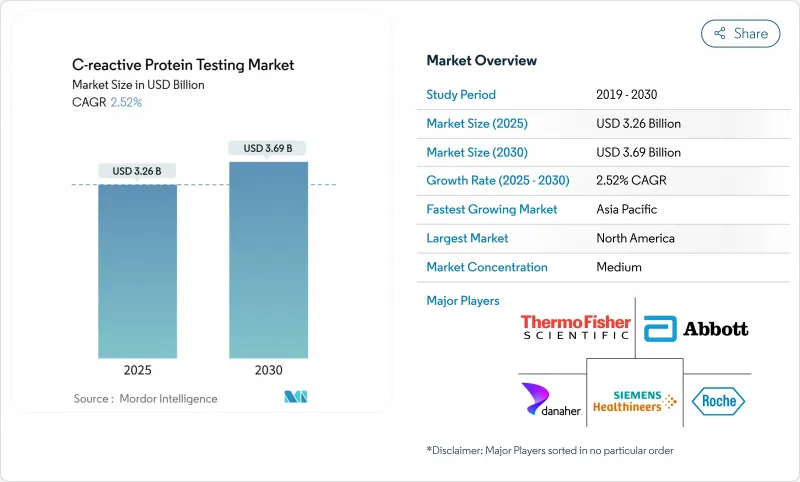

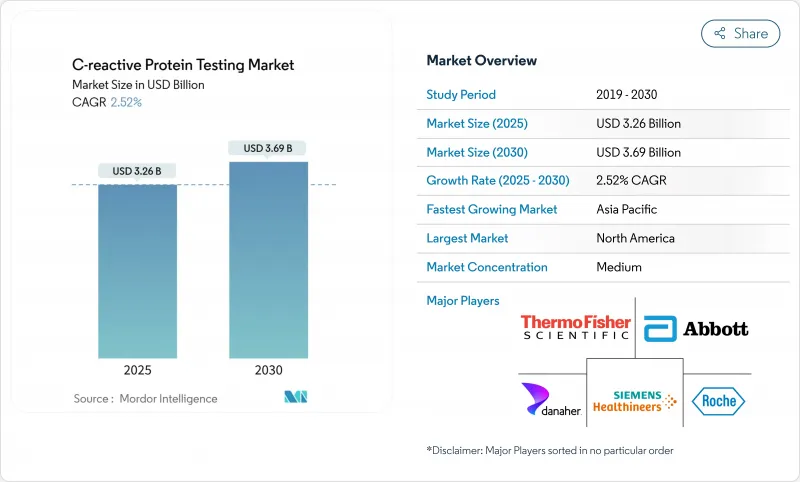

C반응성 단백질(CRP) 검사 시장은 2025년 32억 6,000만 달러로 추정되고, 2030년에는 36억 9,000만 달러에 이를 것으로 예측되며, CAGR 2.52%로 성장할 전망입니다.

이 꾸준한 성장은 고감도 분석, 다항목 염증 패널, 포인트 오브 케어 형식이 가격 결정력을 가진 정밀 진단에 대한 축족에서 발생합니다. 2025년 CLIA 승인 제한과 같은 규제의 엄격화로 분석 공차가 엄격해져 미량 수준의 정확도를 제공할 수 있는 프리미엄 플랫폼이 선호되게 되었습니다. 이와 병행하여, 미국에서는 재검사를 제한하는 진료 보수의 상한이 설정되어, 검사실은 가치 기반의 이용 모델로 방향타를 끊고 있어, 검사에 번들된 의사 결정 지원 소프트웨어의 채용이 가속하고 있습니다. 성숙 시장이든 신흥 시장이든, 1차 케어클리닉, 약국, 재택 모니터링 프로그램에 대한 검사의 급속한 분산화는 C반응성 단백질 검사 시장에서 경쟁의 경계를 재정의하고 있습니다.

만성 염증성 질환의 높은 유병률은 의료 시스템에 의한 CRP의 사용 방법을 변화시키고 있습니다. 소화기내과 의사는 궤양성 대장염의 관해를 생물학적 제제의 치료 스케줄을 조정하기 위해 CRP값이 10mg/L 미만임을 임계값으로 감시하도록 되어 있습니다. 류마티스 전문의는 장기적인 CRP 동향으로부터 질병 개질제를 점진적으로 증가시켜 비용이 많이 드는 영상 검사를 줄입니다. 인구 역학의 노화는 더 많은 환자가 정기적인 검사를 필요로 함을 의미하며, 급성기 치료로 인한 검사 건수 증가의 둔화를 상쇄하는 예측 가능한 수요를 생성합니다. 지불자는 또한 CRP를 비용 효과적인 대용 마커로 간주하고, 진보된 영상 진단으로 환자를 배분할 수 있기 때문에 의료 질을 희생하지 않고 예산을 확보할 수 있습니다. 이러한 요인들이 결합되어 C반응성 단백질(CRP) 검사 시장의 장기 시장 규모가 확대됩니다.

미국 심장협회는 2025년에 hsCRP를 심혈관 및 신장, 대사의 건강 프레임워크에 통합하여 LDL-C나 HbA1c와 나란한 역할을 공식화했습니다. Medicare의 Local Coverage Determination L34856에서는 지질저하 요법을 최적화하는 데 사용되는 경우 hsCRP는 평생 3회까지 검사로 상환되며 실험실에 수익 기준선이 형성됩니다. 지침 승인은 주문 행동을 표준화하고, 의사의 주저를 줄이며, 실용적인 바이오마커가 없었던 중간 위험 환자에 대한 검사 보급을 확대합니다. 진단기기 제조업체는 0.1mg/L단위에서의 고정밀도 캘리브레이션을 우선하고, hsCRP값을 치료 알고리즘으로 변환하는 의사 결정 지원 분석을 통합함으로써 C반응성 단백질(CRP) 검사 시장에서의 프리미엄 가격을 지원하고 있습니다.

광범위한 증거가 있음에도 불구하고 많은 임상의는 CRP 측정을 심장혈관계로 제한합니다. 전문 학회는 현재 CRP가 ESR과 프로 칼시토닌을 능가하는 경우를 명확히 한 빠른 참조 알고리즘을 발표하고 있습니다. 인지도가 향상될 때까지, 비순환기과 수요는 잠재적인 것으로부터 지연되고, 지속적인 의학교육 자원이 부족한 지역에서는 성장이 억제될 것입니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

효소 결합 면역흡착 측정법은 통합된 전달 네트워크에서 정착된 분석기와 표준화된 프로토콜 덕분에 2024년 수익의 45.35%를 차지했습니다. 그러나 래터럴 플로우의 기술 혁신이 이 부문의 CAGR을 7.25% 끌어올려 ELISA의 우위성을 축소시켰습니다. DNA 나노테크놀로지는 검출 감도를 3배로 높여 집중분석법과의 정밀도 차이를 줄이고 약국 기반 검사레인을 개방했습니다. 화학 발광 장치는 200개 샘플 랙과 자동 시약 로딩으로 인건비를 절감하는 고처리량 코어 랩에서 타당성을 유지합니다. 앞으로 ELISA 벤치탑은 번들된 멀티 분석 메뉴와 연결 훅에 초점을 맞추고 급속 카세트 공급업체는 분산형 구매자를 대상으로 합니다. 이 이분화는 C반응성 단백질(CRP) 검사 시장이 대량 검사실로의 통합과 환자에게 가까운 초고속 편의성 모두를 보상하는 것으로, 중간 선택이 거의 남아 있지 않다는 것을 강조합니다.

즉답을 요구하는 환자의 선호도가 증가함에 따라 병원의 벽 밖으로 검사를 계속 끌고 있습니다. 래터럴 플로우 공급업체는 현재 전자 기록과 동기화되는 디지털 리더를 번들로 제공하며 주관적인 컬러 밴드가 아닌 추적 가능한 정량값을 제공합니다. 동남아시아의 농촌에서는 정부의 예방접종 클리닉이 일회용 카세트를 채용해, 레퍼런스 랩에서의 확인을 며칠 기다리지 않고 항생제의 스튜어드십을 지도하고 있습니다. 한편, ELISA 벤더는 CRP가 3mg/L을 넘으면 사이토카인 패널이 자동 트리거되는 반사 검사 알고리즘을 통합함으로써 중앙 검사실을 원스톱 염증 허브로 자리매김하고 점유율을 지키고 있습니다. 이러한 이중 진화는 C반응성 단백질(CRP) 검사 시장이 진단학에서 가장 기술적으로 다양한 분야 중 하나가 되는 이유를 부각하고 있습니다.

고감도 시약은 2024년 매출의 60.53%를 차지하였고, CAGR은 6.85%로 성장이 전망됩니다. 규제기관은 보다 엄격한 숙련도의 역치를 의무화하고 있으며, 벤더는 IFCC 표준 물질에 트레이서블한 캘리브레이터의 표준화를 추진하고 있습니다. CRP가 50mg/L를 초과하는 경우 폐렴과 맹장염을 진단하기 위해 기존의 범위 테스트는 여전히 급성기 의료 워크플로를 지원합니다. 그러나 진료 보상의 차이는 검사실이 경계 영역의 심혈관 사례에 대해 hsCRP를 보고하는 인센티브를 점점 높여 보험료화를 강화하고 있습니다. 따라서 공급업체는 0.5mg/L의 변동 계수를 3% 미만으로 억제하기 위해 측광 광학계 및 시약의 화학적 설계를 재검토하여 고가격을 정당화하고 있습니다.

전통적인 검사 방법의 성장이 둔화되는 것은 불필요한 박테리아 스크리닝을 제한하는 항생제 스튜어드십 프로그램에 기인합니다. 그럼에도 불구하고 신흥 시장은 기본적인 임상 요구를 충족시키기 위해 저렴한 가격의 기존 키트를 사용합니다. 분석 모드 전환이 가능한 듀얼 레인지 분석 장치는 검사실이 구매를 단일화할 수 있는 헤지가 됩니다. 이러한 역학에 의해 C반응성 단백질 검사 시장에서의 경쟁 우위는 검출 범위의 세분화에 의해 형성되고 있습니다.

북미의 2024년 매출 점유율 38.82%는 보험사에 의한 상환의 명확화와 임상의의 hsCRP에 대한 정통에 기인합니다. 메디케어의 3검사 생애상한은 루틴의 반복 주문을 줄여 실험실이 최초의 정밀도와 디지털 의사결정 지원에 집중하도록 촉구하고 있습니다. Quest Diagnostics의 LifeLabs 인수와 같은 서비스 제공업체 간의 통합은 구매력을 강화하고 분석기 계약을 엔드 투 엔드 자동화 제품군으로 유도합니다. 캐나다의 각 주는 45-75세의 심혈관 스크리닝에 hsCRP를 통합하여 공공 실험실 전체의 기준선량을 고정하고 있습니다.

아시아태평양의 CAGR은 가장 빠른 7.21%로 1차 케어의 현대화와 전염병 용도 분야에 힘입고 있습니다. 중국의 HIV 양성자 집단에서 CRP 기반 결핵 퇴치는 민감도 72.23%, 특이도 77.66%를 달성하고 지역에 맞는 이용 사례를 나타냈습니다. 베트남 약국에서의 시험 운영은 항생제 오용을 줄이고 CRP의 보다 광범위한 전개에 대한 정부의 지원을 강화했습니다. 일본의 건강 장수 정책에서는 대사 검진 프로그램에서 성인용 hsCRP에 보조금을 내고 대응 가능한 기반을 넓히고 있습니다. 지역 공급업체는 국내 제조 인센티브를 활용하여 단가를 낮추고 기존에는 브랜드 분석에서 가격을 낮추고 있던 지방 클리닉에도 침투하여 C반응성 단백질(CRP) 검사 시장의 저변을 넓히고 있습니다.

유럽은 엄격한 표준화로 안정적인 수요를 유지하고 있습니다. IFCC의 실험실 의학 가이드라인 구상은 회원국 간의 검량선을 조화시켜 검사실 간의 편차를 줄이고 임상의의 신뢰를 높이고 있습니다. 영국의 국민 보건 서비스는 CRP를 1차 케어의 호흡기 감염 번들에 추가하고 항생제 스튜어드십을 지원하는 검사에 보험 적용했습니다. 중동 및 아프리카와 남미에서는 m헬스 프로그램이 원격지를 순회하는 다항목 진단차에 CRP를 탑재하는 것으로, 전체적으로 점유율은 1자리대이지만 2자리대의 성장을 이루고 있습니다. 이와 같이 각 지역은 진화하는 C반응성 단백질(CRP) 검사 시장에 명확하게 매핑되어 민첩한 기업에게 지역 특유의 기회를 창출하고 있습니다.

The C-Reactive Protein testing market reached USD 3.26 billion in 2025 and is forecast to reach USD 3.69 billion by 2030, expanding at a 2.52% CAGR.

This steady growth stems from the pivot toward precision diagnostics, where high-sensitivity assays, multi-analyte inflammation panels and point-of-care formats command pricing power. Heightened regulatory scrutiny-such as the 2025 CLIA acceptance limits that tightened analytical tolerances-favors premium platforms able to deliver trace-level accuracy. In parallel, reimbursement caps that limit repeat testing in the United States are steering laboratories toward value-based utilization models, accelerating adoption of decision-support software bundled with assays. Across mature and emerging markets alike, rapid decentralization of testing to primary care clinics, pharmacies and home-monitoring programs is redefining competitive boundaries within the C-Reactive Protein testing market.

High prevalence of chronic inflammatory disorders is transforming how health systems use CRP. Gastroenterologists increasingly monitor ulcerative colitis remission with threshold CRP levels below 10 mg/L to adjust biologic therapy schedules. Rheumatologists rely on longitudinal CRP trends to titrate disease-modifying drugs, reducing costly imaging studies. Aging demographics mean larger patient pools need recurring tests, creating predictable demand that offsets slower volume growth from acute-care episodes. Payers also view CRP as a cost-effective surrogate marker that can triage patients toward or away from advanced imaging, preserving budgets without sacrificing care quality. Collectively these factors bolster long-run volumes in the C-Reactive Protein testing market.

The American Heart Association embedded hsCRP into its cardiovascular-kidney-metabolic health framework in 2025, formalizing its role alongside LDL-C and HbA1c. Medicare's Local Coverage Determination L34856 reimburses hsCRP up to three lifetime tests when used for lipid-lowering therapy optimization, creating a revenue baseline for laboratories. Guideline endorsement standardizes ordering behavior, reducing physician hesitation and expanding test penetration among intermediate-risk patients who previously lacked actionable biomarkers. Diagnostic manufacturers thus prioritize precision calibration at 0.1 mg/L increments and integrate decision-support analytics that translate hsCRP values into therapy algorithms, supporting premium pricing within the C-Reactive Protein testing market.

Despite broad evidence, many clinicians limit CRP ordering to cardiovascular contexts. Specialty societies are now publishing quick-reference algorithms clarifying when CRP outperforms ESR and procalcitonin. Until awareness improves, non-cardiology demand will lag potential, tempering growth in regions lacking continuing-medical-education resources.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Enzyme-Linked Immunosorbent Assay held 45.35% of 2024 revenues thanks to entrenched analyzers and standardized protocols across integrated delivery networks. However, lateral-flow innovation lifted this segment's 7.25% CAGR, compressing ELISA's dominance. DNA nanotechnology tripled detection sensitivity, narrowing the accuracy gap with centralized methods and unlocking pharmacy-based testing lanes. Chemiluminescence instruments preserve relevance in high-throughput core labs where 200-sample racks and auto-reagent loading reduce labor costs. Looking ahead, ELISA bench-tops will focus on bundled multi-analyte menus and connectivity hooks, while rapid cassette suppliers court decentralized buyers. The bifurcation underscores how the C-Reactive Protein testing market rewards both high-volume lab integration and ultrafast near-patient convenience, with few middle-ground options remaining.

Growing patient preference for instant answers continues to pull testing outside hospital walls. Lateral-flow suppliers now bundle digital readers that sync to electronic health records, delivering traceable quantitative values rather than subjective color bands. In rural Southeast Asia, government immunization clinics adopted disposable cassettes to guide antibiotic stewardship without waiting days for reference-lab confirmation. Meanwhile, ELISA vendors defend share by embedding reflex-testing algorithms that auto-trigger cytokine panels when CRP surpasses 3 mg/L, positioning central labs as one-stop inflammation hubs. This dual-track evolution highlights why the C-Reactive Protein testing market remains one of diagnostics' most technology-diverse arenas.

High-sensitivity reagents captured 60.53% of 2024 revenue and are pacing a 6.85% CAGR as clinicians value sub-1 mg/L precision for preventive cardiology. Regulatory bodies mandate tighter proficiency thresholds, pushing vendors to standardize calibrators traceable to IFCC reference material. Conventional range tests still anchor acute-care workflows, diagnosing pneumonia or appendicitis where CRP exceeds 50 mg/L. Yet reimbursement differentials increasingly incentivize labs to report hsCRP for borderline cardiovascular cases, reinforcing premiumization. Suppliers therefore redesign photometric optics and reagent chemistries to hold coefficient-of-variation below 3% at 0.5 mg/L, justifying higher prices.

Muted growth in conventional assays stems from antibiotic stewardship programs that limit unnecessary bacterial screens. Still, emerging markets rely on low-cost conventional kits to meet basic clinical needs. Dual-range analyzers capable of switching analytical modes offer a hedge, letting laboratories consolidate purchasing. These dynamics keep both tiers relevant, but margin expansion clusters around high-sensitivity innovations, demonstrating how detection-range segmentation shapes competitive advantage in the C-Reactive Protein testing market.

The C-Reactive Protein Testing Market Report is Segmented by Assay Type (Enzyme-Linked Immunosorbent Assay (ELISA), Chemiluminescence Immunoassay (CLIA), and More), Detection Range (High-Sensitivity CRP and Conventional CRP), Application (Diabetes, Rheumatoid Arthritis, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America's 38.82% revenue share in 2024 stems from insurer reimbursement clarity and clinician familiarity with hsCRP. Medicare's three-test lifetime cap reduces routine repeat ordering, nudging labs to focus on first-time precision and digital decision support. Consolidation among service providers-such as Quest Diagnostics' LifeLabs takeover-intensifies purchasing power, steering analyzer contracts toward end-to-end automation suites. Canadian provinces are integrating hsCRP into cardiovascular screening for individuals aged 45-75, anchoring baseline volumes across public labs.

Asia-Pacific delivers the fastest 7.21% CAGR, fueled by primary-care modernization and infectious-disease applications. China's CRP-based tuberculosis triage among HIV-positive populations achieved 72.23% sensitivity and 77.66% specificity, showcasing locally tailored use-cases. Vietnam's pharmacy pilots trimmed antibiotic misuse, bolstering government support for wider CRP rollout. Japan's healthy-aging policies subsidize hsCRP for adults in metabolic screening programs, wid¬ening the addressable base. Regional suppliers leverage domestic manufacturing incentives to lower unit costs, penetrating rural clinics previously priced out of branded assays, which expands the C-Reactive Protein testing market footprint.

Europe maintains stable demand through rigorous standardization. IFCC's laboratory medicine guideline initiatives harmonize calibrators across member states, shrinking inter-lab variability and raising clinician confidence. National Health Services in the United Kingdom added CRP to primary-care respiratory infection bundles, reimbursing tests that support antibiotic stewardship. Emerging regions in Middle East & Africa and South America collectively add single-digit share but post double-digit growth where mHealth programs piggyback CRP on multiparameter diagnostic vans servicing remote areas. Each geography thus maps distinctly onto the evolving C-Reactive Protein testing market, creating localized opportunities for agile players.