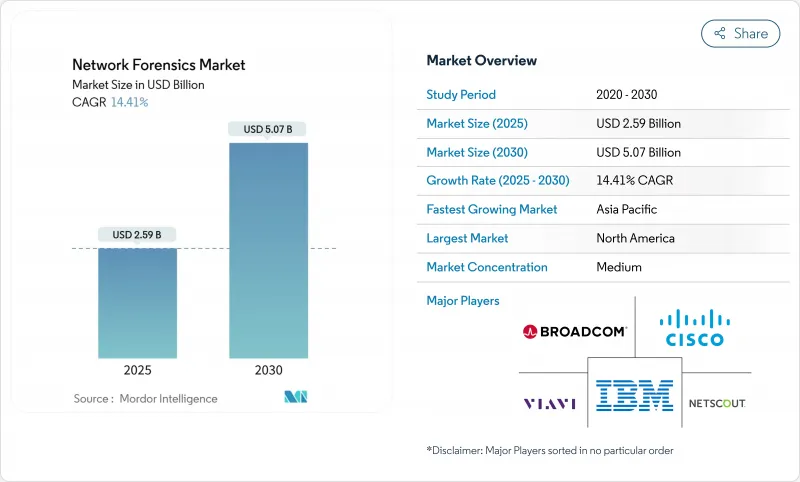

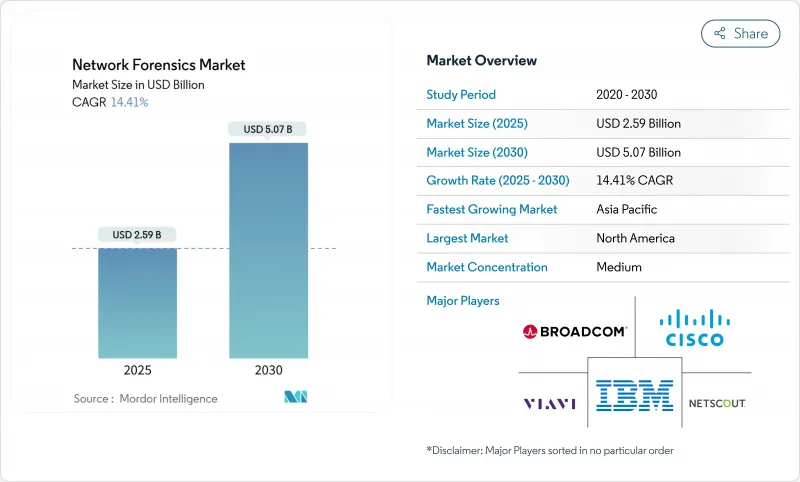

네트워크 포렌식 시장 규모는 2025년에 25억 9,000만 달러로 추정되고, 2030년에는 50억 7,000만 달러에 이를 것으로 예측되며, CAGR 14.41%로 성장할 전망입니다.

패킷 수준의 가시성이 신속한 침해 진단, 규제 당국에 대한 보고, 사이버 보험 규정 준수에 필수적이기 때문에 채용 곡선은 가파릅니다. 특히 하이브리드 클라우드 트래픽, 5G 전개, 암호화된 동서 흐름 등 기존 경계 도구가 간과했던 맹점이 드러나는 장면에서 지출의 기세가 강합니다. 따라서 공급업체는 포렌식 기능을 NDR(Network Detection and Response) 플랫폼에 통합하여 도구의 난립을 줄이고 평균 응답 시간을 단축합니다. 보험사가 보험금 청구의 검증을 위해 패킷 증거를 요구하거나, SEC 및 EU의 Digital Operational Resilience Act와 같은 규제 당국이 적시에 문서화된 인시던트의 공개를 의무화함으로써 수요도 높아지고 있습니다.

클라우드 마이그레이션이 기존 모니터링을 능가하기 때문에 기업의 73%가 기존 툴셋에서 실용적인 인사이트를 얻지 못했습니다. 찰나 워크로드 간 동서 트래픽은 레거시 컬렉터가 캡처하기 전에 사라지는 경우가 많기 때문에 여러 IaaS 및 PaaS 도메인에 걸쳐 증거 수집을 자동화하는 클라우드 네이티브 캡처 엔진에 대한 수요가 증가하고 있습니다. 새로운 제품은 패킷 캡처, 아티팩트 저장, 타임라인 재구성을 단일 워크플로우로 통합하고, 조사 효율성을 높이며, 온프레미스, 퍼블릭 클라우드, 하이브리드 환경에서 일관된 정책 구현을 지원합니다. 공급업체는 스마트 스토리지 계층화를 통합하기 시작했으며, 선형 비용 상승 없이 장기 보존을 가능하게 하고, 규제 당국이 온디맨드로 포렌식 증거를 감사할 수 있도록 하고 있습니다.

2024년 세계적 침해 비용은 488만 달러에 이르렀으며, 자격증 도난 사건은 84% 급증하였고, 비정상적인 인증 스파이크와 횡이동 비콘을 표면화하는 네트워크 분석 채택에 박차를 가하고 있습니다. 의료 기관은 여전히 포위되고 있으며, 93%가 3년 이내에 정보 유출을 만났기 때문에 체류 시간과 공격의 출처를 핀 포인트로 식별하는 지속적인 패킷 캡처의 도입을 추진하고 있습니다. 기업은 현재 엔리치된 네트워크 텔레메트리를 엔드포인트, ID, 클라우드 로그를 상호 참조하는 위협 사냥 루틴에 통합하여 적대자의 장애물을 올리고 법률, 규제, 보험 이해관계자를 위해 사건 후의 포렌식을 가속화하고 있습니다.

정보 보안 분석가 수요는 2022-2032년 32% 확대될 것으로 예상되지만, 대학 및 교육 파이프라인은 늦어지고 고용주의 54%는 패킷 분석 직무를 충족할 수 없습니다. 조직은 루틴 분석 작업을 AI 지원 플레이북으로 마이그레이션하고, 레벨 1 모니터링을 관리 서비스 파트너에게 아웃소싱하며, 툴 사용 편의성을 우선하여 전문가가 아니더라도 최소한의 시작으로 패킷 타임라인을 탐색할 수 있도록 함으로써 대응하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

이 솔루션은 2024년 네트워크 포렌식 시장 수익의 62%를 창출했으며, 고속 패킷 캡처, 행동 분석 및 암호화된 트래픽의 시각화에 대한 수요에 따라 그 지위를 확립했습니다. 공급업체의 머신러닝 알고리즘을 통합하면 기준선 트래픽 프로파일이 설정되고 몇 초 안에 편차가 표면화됩니다. 현재 서비스 분야는 소규모이지만 CAGR 18%로 확대하고 있습니다. 왜냐하면 기업은 통합, 튜닝, 지속적인 조사 지원을 필요로 하는 반면, 인재는 부족하기 때문입니다. 공급자는 평가, 사고 대응 리테이너 및 관리된 검색을 번들로 제공하여 일회성 라이선스를 정기적인 수익원으로 바꿉니다. 예측 기간 동안 하드웨어 벤더와 세계 시스템 통합사업자가 공동으로 시장 진입 프로그램을 실시함으로써, 특히 24시간 체제에서 증거 검색을 필요로 하는 규제 산업에서의 도입이 더욱 진행될 것으로 보입니다.

투자 패턴은 자동화 지원 솔루션이 자본 예산의 대부분을 차지하는 반면, 도구 가치를 극대화하는 전략적 오버레이로 자문 서비스가 성장할 것임을 시사합니다. 브렌디드 모델은 전개부터 사고의 사후 처리에 이르는 라이프사이클 관리를 지원하여 네트워크 포렌식 시장이 다양한 구매자 페르소나 사이에서 강력한 흡입력을 유지할 수 있도록 합니다.

많은 금융기관, 정부기관, 방위기관이 증거의 현지 보관을 필요로 하기 때문에 온프레미스 전개가 2024년 네트워크 포렌식 시장 규모의 53%의 점유율을 유지하고 있습니다. 하지만 트래픽이 SaaS, IaaS, 컨테이너화된 스택으로 마이그레이션됨에 따라 클라우드 네이티브 전개는 CAGR 22.5%에서 급증합니다. 클라우드 콜렉터는 지역 전반에 걸친 증거 수집을 오케스트레이션하고, 볼륨이 있는 이벤트 중에는 자동 규모를 조정하고, 스토리지를 컴퓨팅에서 분리함으로써 초기 비용을 절감합니다. 하이브리드 아키텍처가 등장하고 기밀 데이터는 현장에 머물고 버스트 워크로드와 규제가 느슨한 부문은 클라우드 컬렉터를 활용합니다.

플랫폼 제공업체는 현재 Kubernetes 클러스터 또는 사이드카로 전개할 수 있는 경량 센서를 제공하며 가상 네트워크와 물리적 스위치 범위 간의 원격 측정 패리티를 보장합니다. 컴플라이언스 팀은 클라우드 오브젝트 스토어가 가능하게 하는 불변의 감사 추적을 강조하며, 재무 팀은 계절적 트래픽 변동에 따라 지출을 조정하는 옥스 기반 소비를 평가합니다. 이러한 역학은 모두 광범위한 네트워크 포렌식 시장에서 분산 수집 토폴로지에 대한 영구적 축족을 강화합니다.

북미는 2024년에 40%의 점유율을 차지하였고, 4일 이내의 정보 유출 보고를 의무화하는 SEC 정보 공개 규칙과 보험의 적용 범위를 증거의 질에 연결시키는 선진적인 사이버 보험 생태계가 그 원동력이 되고 있습니다. 미국 기업들은 기술 부족을 극복하고 잠재적인 소송과 규제 당국의 조사에 대비하여 종합적인 로그를 유지하기 위해 AI를 활용한 분석을 도입하고 있습니다. 캐나다는 프라이버시 침해 통지의 의무화와 중요한 인프라 사업자의 집중적인 존재에 힘입어 비슷한 궤도를 따르고 있습니다.

유럽은 GDPR(EU 개인정보보호규정) 시행과 2025년 1월 DORA 개시의 혜택을 받아 2024년 네트워크 포렌식 시장 수익의 28%를 차지했습니다. 영국, 독일 및 프랑스의 은행 허브는 패킷 캡처 예산을 24시간 인시던트 알림을 제공하기 위해 두 배로 늘렸습니다. 5G 회랑에 초점을 맞춘 공공 부문의 프로젝트는 8억 6,500만 유로(9억 3,100만 달러)를 네트워크 구축에 투입하여 새로운 보안 감시 레이어를 구축하도록 촉구하고 있습니다. EU 지역 내에서 국경을 넘어서는 데이터 공유의 틀은 또한 여러 법역의 증거 허용 기준을 충족하는 표준화된 포렌식 워크플로우에 대한 수요를 자극하고 있습니다.

아시아태평양은 2025-2030년 CAGR 17.9%로 가장 급성장할 것으로 전망되는 지역입니다. 중국의 디지털 금융 확대, 인도의 5G 경매, 호주의 중요한 인프라 개혁이 지속적인 기회를 창출하고 있습니다. 한국의 디지털 포렌식 분야만으로도 2025년까지 35억 2,000만 달러의 규모에 이를 것으로 예측되고 있으며, 국가의 사이버 회복력에 대한 관민 투자를 반영하고 있습니다. 기술 부족은 여전히 심각하지만, 관리 보안 서비스는 지역 격차를 상쇄하고 중견 기업에 대한 도입을 가속화합니다. 이 지역은 국가 주도 캠페인에 노출되어 있어 고도의 다단계 침입을 재구성할 수 있는 네트워크 포렌식 시장 도구의 중요성이 더욱 높아지고 있습니다.

The network forensics market size is valued at USD 2.59 billion in 2025 and is forecast to reach USD 5.07 billion by 2030, advancing at a 14.41% CAGR.

The adoption curve is steep because packet-level visibility has become indispensable for rapid breach diagnosis, regulatory reporting and cyber-insurance compliance. Spending momentum is especially strong where hybrid-cloud traffic, 5G roll-outs and encrypted east-west flows expose blind spots that traditional perimeter tools overlook. Vendors are therefore embedding forensic functionality into Network Detection and Response (NDR) platforms, shrinking tool sprawl and lowering mean-time-to-respond. Demand is also lifted by insurers that now require packet evidence for claims validation and by regulators such as the SEC and the EU's Digital Operational Resilience Act, which mandate timely, well-documented incident disclosure.

Cloud migration has outpaced traditional monitoring, leaving 73% of enterprises unable to derive actionable insight from existing toolsets. East-west traffic among ephemeral workloads often vanishes before legacy collectors capture it, prompting demand for cloud-native capture engines that automate evidence gathering across multiple IaaS and PaaS domains. Emerging offerings integrate packet capture, artifact preservation and timeline reconstruction in a single workflow, improving investigative efficiency and supporting consistent policy enforcement across on-premises, public cloud and hybrid environments. Providers have begun to embed smart storage tiering, enabling long-term retention without linear cost escalation and ensuring regulators can audit forensic evidence on demand.

Global breach costs climbed to USD 4.88 million in 2024, while credential-theft incidents surged 84%, fueling adoption of network analytics that surface anomalous authentication spikes and lateral-movement beacons. Healthcare institutions remain under siege as 93% encountered a breach within three years, pushing them to deploy continuous packet capture that pinpoints dwell time and attack provenance. Enterprises now integrate enriched network telemetry into threat-hunting routines that cross-reference endpoint, identity and cloud logs, raising the bar for adversaries and accelerating post-incident forensics for legal, regulatory and insurance stakeholders.

Demand for information-security analysts is projected to expand 32% between 2022-2032, yet universities and training pipelines lag, leaving 54% of employers unable to fill packet-analysis roles.The deficit inflates salary baselines beyond USD 119,000 and amplifies operational risk when alerts outstrip triage capacity. Organizations respond by shifting routine parsing to AI-assisted playbooks, outsourcing level-1 monitoring to managed service partners and prioritizing tool usability so non-specialists can navigate packet timelines with minimal ramp-up.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solutions generated 62% of network forensics market revenue in 2024, a position powered by demand for high-speed packet capture, behavioural analytics and encrypted-traffic visibility. Feature velocity is brisk, with vendors embedding machine-learning algorithms that establish baseline traffic profiles and surface deviations in seconds. The services segment is smaller today yet expands at an 18% CAGR because organizations need integration, tuning and continuous investigation support while talent remains scarce. Providers bundle assessment, incident-response retainers and managed detection to convert one-time licences into recurring revenue streams. Over the forecast horizon, joint go-to-market programs between hardware vendors and global system integrators will further amplify adoption, especially in regulated industries that require 24-hour evidence retrieval.

Investment patterns suggest that automation-ready solutions will dominate capital budgets, while advisory services grow as strategic overlays that maximize tooling value. The blended model supports life-cycle management from deployment to incident post-mortems, ensuring the network forensics market retains strong pull across diverse buyer personas.

On-premise deployments maintained 53% share of network forensics market size in 2024 because many financial, government and defense entities require local custody of evidence. Nevertheless, cloud-native deployments soar at a 22.5% CAGR as traffic migrates to SaaS, IaaS and containerised stacks. Cloud collectors orchestrate evidence gathering across regions, auto-scale during volumetric events and decouple storage from compute, slashing upfront expense. Hybrid architectures emerge where sensitive data stays on site, yet burst workloads and less regulated segments leverage cloud collectors.

Platform providers now ship lightweight sensors deployable in Kubernetes clusters or as side-cars, ensuring parity of telemetry between virtual networks and physical switch spans. Compliance teams value the immutable audit trails that cloud object stores enable, while finance teams appreciate opex-based consumption that aligns spend with seasonal traffic variance. Together these dynamics reinforce an enduring pivot toward distributed collection topologies within the broader network forensics market.

Network Forensic Market is Segmented by Component (Solution and Services), by Deployment Model (On-Premise, Cloud), by Organization Size (Small and Medium Enterprises (SMEs) and Large Enterprises), by Application (Endpoint Security, Data Center Security, Network Security, and More), by End-User Industry (IT and Telecom, BFSI, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America held 40% share in 2024, driven by SEC disclosure rules that enforce four-day breach reporting and by an advanced cyber-insurance ecosystem that ties coverage to evidence quality. U.S. enterprises deploy AI-enabled analysis to overcome skills shortages and maintain comprehensive logs for potential litigation or regulatory inquiry. Canada follows a comparable trajectory, underpinned by mandatory privacy breach notifications and concentrated presence of critical infrastructure operators.

Europe captured 28% of network forensics market revenue in 2024, benefiting from GDPR enforcement and the January 2025 start of DORA. Banking hubs in the United Kingdom, Germany and France doubled packet-capture budgets to achieve 24-hour incident notification. Public-sector projects focused on 5G corridors channel EUR 865 million (USD 931 million) into network build-outs, prompting new security monitoring layers. Cross-border data-sharing frameworks inside the EU also stimulate demand for standardized forensic workflows that meet multi-jurisdictional evidence admissibility criteria.

Asia-Pacific is the fastest-growing theatre with a 17.9% 2025-2030 CAGR. China's digital-finance expansion, India's 5G auctions and Australia's critical-infrastructure reforms create sustained opportunities. South Korea's digital forensics sector alone is projected at USD 3.52 billion by 2025, reflecting public-private investment in national cyber-resilience. While skills shortages remain acute, managed security services offset local gaps and accelerate uptake among medium-sized enterprises. The region's exposure to state-sponsored campaigns further elevates the relevance of network forensics market tools that can reconstruct sophisticated, multi-stage intrusions.