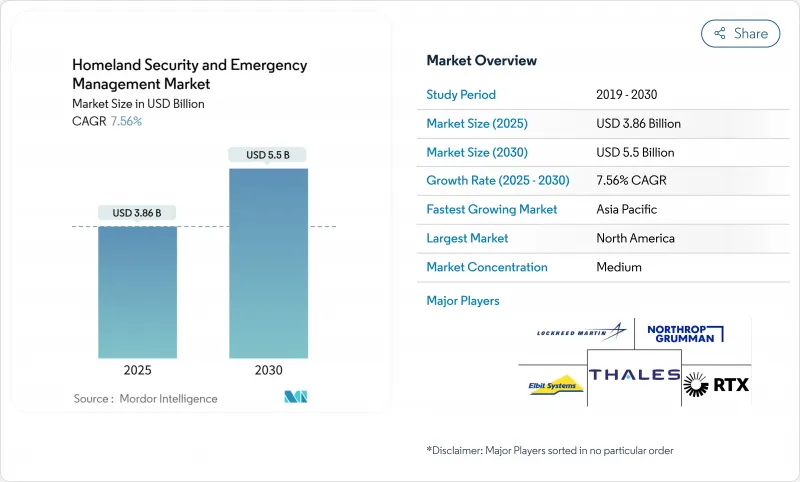

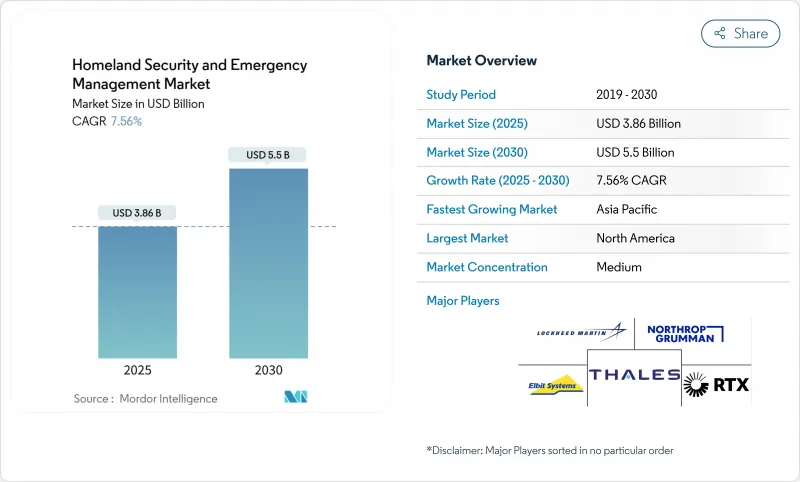

국토안보 및 긴급사태 관리 시장은 2025년 38억 2,000만 달러로 추정되고, CAGR 7.56%로 성장할 전망이며, 2030년에는 55억 달러에 이를 것으로 예측됩니다.

사이버, 물리, 환경 위협의 중복이 치열해지고 있기 때문에 정부와 민간 사업자는 경계 보호와 실시간 디지털 인텔리전스를 통합한 통합 플랫폼에 투자할 필요성에 강요하고 있습니다. 국가 주도의 사이버 공격, 지정학적 마찰 증가, 기후로 인한 재해의 빈발화에 의해 국토안보 및 긴급사태 관리 시장의 대응 가능 범위가 확대되고 있는 한편, 5G, 클라우드, AI 등의 신기술이 전국 전개에 필요한 규모를 제공합니다. 또한 5G, 클라우드, AI 등의 신기술이 전국 전개에 필요한 규모를 제공하는 한편, 방위 프라임이 클라우드나 통신 사업자와 제휴해, 중요한 인프라, 공공 안전 통신, 국경 관리를 위한 모듈식 솔루션을 제공하기 때문에 경쟁의 격렬함이 증가하고 있습니다. 동시에 구매 결정은 공급업체가 보다 신속한 사고 대응 및 측정 가능한 위험 감소를 입증해야 하는 성과 기반 계약으로 전환하고 있습니다. 조달의 틀이 성숙함에 따라 지역간 격차도 확대되고 있습니다. 북미에서는 제로 트러스트 사이버 아키텍처가 채용되고, 아시아에서는 스마트 시티의 감시 배치가 가속화되며, 유럽에서는 국경을 넘은 정보 공유와 함께 엄격한 데이터 보호가 의무화되고 있습니다.

국가 그룹은 정보 수집에서 전력망, 항만, 수도 시스템 내에 휴면 상태의 악성코드를 설치하는 것으로 이동하고 있습니다. FBI는 Volt Typhoon이 미국 운송 네트워크에 대한 비밀 액세스를 5년 이상 유지하고 분쟁 시 파괴적인 행동을 일으킬 수 있음을 밝혔습니다. 따라서 사업자는 경계 중심의 방위를 중단하고 모든 장치와 사용자를 지속적으로 검증하는 제로 트러스트 모델을 채용하게 되었습니다. 에너지 및 유틸리티 기업은 운영 기술 네트워크를 세분화하고, 공항에서는 행동 분석을 적용해 의심스러운 주변의 움직임을 발견하고 있습니다. 이러한 조치를 통해 사이버 보안에 대한 지출은 정체성 관리, 암호화된 산업 프로토콜 및 지속적인 네트워크 모니터링으로 향하고 있습니다. 랜섬웨어가 지정학적 동기에 근거한 방해 행위와 겹치면서 보험료가 상승하고 부작위의 총 비용이 상승하고 추가적인 안전 대책에 박차가 걸리고 있습니다.

미국과 유럽 연합(EU)의 규제 캘린더는 차세대 긴급 신고 라우팅, 3m 이하의 위치 정확도, 디스패처와 구급 대원 간의 멀티미디어 교환을 의무화하고 있습니다. 컴플라이언스 프로젝트에는 클라우드 기반 통화 처리, 중복 파이버 백본, NIST 및 ETSI 표준을 준수하는 사이버 보안 인증이 필요합니다. 이미 업그레이드된 카운티에서는 통화 포기율이 저하되어 여러 사상자가 발생했을 경우의 트리아지가 신속하게 실시될 수 있게 되었다고 보고하고 있습니다. IP 코어 서비스, 지리 공간 분석, 사이버 하드화된 무선 게이트웨이를 제공하는 공급업체는 직접 이익을 얻었으며 시스템 통합사업자는 유지보수 계약의 연장을 획득했습니다. 공공 경보 시스템은 민간 통신 네트워크와 인터페이스해야 하기 때문에 국경을 넘어선 표준이 강화되고 대륙을 넘어 플랫폼의 수렴이 가속화되고 있습니다.

긴급 기관은 종종 별도의 보조금 프로그램 하에서 무선, 센서 및 분석 플랫폼을 구매하고 상호부조를 방해하는 호환되지 않는 데이터 스키마를 생성합니다. 미국 정부 책임국은 중복 국토 안보 계약을 배제함으로써 수억 달러를 절약할 수 있다고 추정하고 있습니다. 유럽에서는 지자체 감시 소프트웨어가 국경 시스템과의 통합에 어려움을 겪고 있습니다. 공급업체는 고유한 형식 간의 변환을 수행하는 미들웨어를 제공해야 하지만 엔지니어링 비용이 추가되므로 롤아웃 일정이 느려지고 프로젝트의 총 가격이 상승하여 단기 성장이 억제됩니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

2024년에 가장 큰 수익을 올린 것은 중요한 인프라 보안이며, 전력, 물, 운송 자산의 탄력성에 대한 우려 증가를 뒷받침하고 있습니다. 이 부문의 국토안보 및 긴급사태 관리 시장 점유율은 21.52%로, 철도 신호나 파이프라인 모니터링 네트워크의 침해가 공개된 후에 발생했습니다. 유틸리티 사업자는 감시 제어 및 데이터 수집(SCADA) 트래픽의 부문화, 변전소 침입 감지 도입, 연방 융합 센터와의 사고 대응 플레이북 통합 등으로 대응했습니다. 이 부문의 국토 안보 및 긴급 상황 관리 시장 규모는 지속적인 보조금 할당, 사이버 사고 보고 규칙의 의무화, 예지 보전을 가능하게 하는 디지털 트윈의 통합으로 꾸준히 증가할 것으로 예측됩니다.

절대 기준으로는 작은 반면, 해상과 항만의 보안은 2030년까지 연평균 복합 성장률(CAGR) 8.46%로 확대될 것으로 예측됩니다. 이는 해상 트레이드레인의 전략적 가치, NATO의 Baltic Sentry 드론 선단, 선언된 항로에서 벗어난 선박에 플래그를 지정하는 상용 AI 시스템 등을 반영하여 해상 영역 인식에 대한 광범위한 헌신을 강조하고 있습니다. 항만에서는 지표 레이더와 수중 음향을 결합하여 광섬유 케이블 근처의 무허가 다이버를 감지합니다. 보험 인수자가 방해 파괴 행위의 리스크를 커버하기 위해 견고한 감시를 요구하는 가운데 자율형 순시선과 AI로 스코어화된 리스크 대시보드의 조달이 가속화되고 있습니다. 추가 성장 촉진요인으로는 새로운 배출 추적 센서를 필요로 하는 탈탄소화의 의무화가 있어 국토안보 및 긴급사태 관리 시장에서의 솔루션 범위가 더욱 확대되고 있습니다.

기타 솔루션 라인(CBRNE 감지, 경계 보호, 항공 보안, 위험 및 응급 서비스)은 위협 스펙트럼 전체에 중복성을 추가합니다. 이 점유율은 다양하지만 통합된 명령 및 제어 플랫폼을 통해 기관은 모든 서브시스템의 경보를 단일 창에서 시각화할 수 있어 인시던트 오케스트레이션을 간소화할 수 있습니다.

북미는 2024년에 36.81%의 점유율로 리드했습니다. 중요 인프라 방위를 위한 연방정부의 왕성한 예산과 정부기관 및 민간사업자의 광범위한 협력 관계에 의해 지원되고 있습니다. 로스앤젤레스 항구는 2024년에 7억 5,000만 회의 해킹 시도가 차단되어 공격량이 구매 우선순위를 형성하고 있음을 보여줍니다. 제로 트러스트의 채용률은 타지역을 상회하고 있으며, 인프라 투자 및 고용 촉진법(Infrastructure Investment and Jobs Act)과 같은 조성금의 틀에 의해 회복력의 업그레이드에 자금이 돌고 있습니다.

아시아태평양은 성장 엔진이며 CAGR 9.21%로 확대되고 있습니다. 급속한 도시화 및 거대 도시에 대한 투자로 인공지능을 활용한 감시, 스마트 피난 통로, 탄력 있는 통신 백본을 위한 비옥한 토양이 형성되고 있습니다. 2024년 노토반도 지진은 센서 커버 범위의 갭을 드러내고 통합 경보 플랫폼의 신속한 조달에 박차를 가했습니다. 한편 대만과 한국에서는 반도체 공장이 증가하고 엄격한 보안 경계선과 에어 갭 사이버 방위가 필요하며 지역 지출을 강화하고 있습니다.

유럽은 엄격한 규제 의무화 및 국경 관리의 공동 이니셔티브를 통해 큰 지위를 유지하고 있습니다. 베이루트 라픽 하릴리 국제공항의 생체 인식 업그레이드와 같은 프로젝트는 유럽 기준이 유럽 대륙을 넘어 수출되고 있음을 보여줍니다. EU 지역 안보 기금의 자금은 국경을 넘어서는 데이터 공유 허브를 지원합니다.

중동에서는 석유 수입을 공항, 에너지 시설, 공공 시설의 보호 시스템 중층화를 계속하고 있습니다. 아프리카와 라틴아메리카의 진전은 보다 완만하지만, 허리케인과 사이클론의 피해를 받기 쉬운 해안 도시에서는 해상 및 재해 대응 능력을 우선하고 있습니다.

The homeland security and emergency management market was valued at USD 3.82 billion in 2025 and is on track to reach USD 5.5 billion by 2030, reflecting a 7.56% CAGR.

Intensifying overlaps between cyber, physical, and environmental threats motivate governments and private operators to invest in integrated platforms that merge perimeter protection with real-time digital intelligence. State-sponsored cyberattacks, rising geopolitical frictions, and more frequent climate-driven disasters are expanding the addressable scope of the homeland security and emergency management market, while emerging technologies such as 5G, cloud, and AI deliver the scale required for nationwide rollouts. Competitive intensity is growing as defense primes partner with cloud and telecom players to field modular solutions for critical infrastructure, public safety communications, and border management. At the same time, purchasing decisions are moving toward outcome-based contracts in which vendors must demonstrate faster incident response and measurable risk reduction. As procurement frameworks mature, regional differentiation is widening: North America adopts zero-trust cyber architectures, Asia accelerates smart-city surveillance deployments, and Europe mandates strict data-protection safeguards alongside cross-border intelligence sharing.

Nation-state groups have shifted from intelligence gathering to the placement of dormant malware within electric grids, ports, and water systems. The FBI disclosed that Volt Typhoon maintained covert access to US transport networks for over five years and could launch disruptive actions during conflict events. Operators are therefore retiring perimeter-centric defenses in favor of zero-trust models that continuously validate every device and user. Energy utilities segment operational-technology networks, while airports apply behavioral analytics to spot suspicious lateral movement. These measures have pushed cybersecurity spending toward identity management, encrypted industrial protocols, and continuous network monitoring. As ransomware overlaps with geopolitically motivated sabotage, insurance premiums have risen, elevating the total cost of inaction and spurring additional safeguards.

Regulatory calendars in the United States and European Union mandate next-generation emergency call routing, location precision under three meters, and multimedia exchange between dispatchers and first responders. Compliance projects require cloud-based call handling, redundant fiber backbones, and cybersecurity certification aligned with NIST and ETSI standards. Counties already upgraded report lower call abandonment rates and faster triage of multi-casualty events. Vendors supplying IP core services, geospatial analytics, and cyber-hardened radio gateways benefit directly, while system integrators capture extended maintenance contracts. Because public warning systems must interface with private telecom networks, cross-border standards are tightening, accelerating platform convergence across continents.

Emergency agencies often buy radios, sensors, and analytics platforms under separate grant programs, creating incompatible data schemas obstructing mutual aid. The US Government Accountability Office estimates that eliminating duplicated homeland security contracts could save hundreds of millions. Parallel challenges surface in Europe, where municipal surveillance software can struggle to integrate with national border systems. Vendors must provide middleware that translates between proprietary formats, but the additional engineering cost slows rollout schedules and increases total project price, tempering near-term growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Critical infrastructure security generated the largest revenue slice in 2024, underscoring heightened concern over the resilience of electricity, water, and transportation assets. The segment's 21.52% homeland security and emergency management market share arose after publicized attempts to compromise rail signaling and pipeline monitoring networks. Utilities responded by segmenting supervisory control and data acquisition (SCADA) traffic, deploying intrusion detection at substations, and integrating incident-response playbooks with federal fusion centers. This segment's homeland security and emergency management market size is forecast to rise steadily on continued grant allocations, mandatory cyber incident reporting rules, and the incorporation of digital twins that enable predictive maintenance.

Although smaller in absolute terms, maritime and port security are projected to expand at 8.46% CAGR through 2030, reflecting the strategic value of seaborne trade lanes, NATO's Baltic Sentry drone flotilla, and commercial AI systems that flag vessels deviating from declared routes highlight a broader commitment to maritime domain awareness. Ports pair surface radars with underwater acoustics to detect unauthorized divers near fiber cables. As insurance underwriters demand robust monitoring to cover sabotage risks, procurement of autonomous patrol boats and AI-scored risk dashboards accelerates. Additional growth drivers include decarbonization mandates that require new emission-tracking sensors, further widening the solution scope within the homeland security and emergency management market.

Other solution lines-CBRNE detection, perimeter protection, aviation security, and risk and emergency services-add redundancy across the threat spectrum. While their share fluctuates, integrated command-and-control platforms allow agencies to visualize alerts from all subsystems in a single pane, simplifying incident orchestration.

The Homeland Security and Emergency Management Market Report is Segmented by Solution Type (Critical Infrastructure Security, and More), Technology (AI and Machine Learning, and More), End-Use Vertical (Military and Defense, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America led with a 36.81% share in 2024, supported by robust federal appropriations for critical-infrastructure defense and extensive collaboration between agencies and private operators. The Port of Los Angeles blocked 750 million hacking attempts in 2024, illustrating the attack volume shaping purchasing priorities. Zero-trust adoption rates outpace other regions, and grant frameworks such as the Infrastructure Investment and Jobs Act funnel funds toward resilience upgrades.

Asia-Pacific is the growth engine, expanding at 9.21% CAGR. Rapid urbanization and megacity investments create fertile ground for AI-enabled surveillance, smart evacuation corridors, and resilient telecom backbones. The 2024 Noto Peninsula earthquake exposed gaps in sensor coverage and spurred fast-track procurement of integrated warning platforms. Meanwhile, rising semiconductor fabs across Taiwan and South Korea require strict security perimeters and air-gap cyber defenses, intensifying regional spend.

Europe maintains a sizeable position through stringent regulatory mandates and joint border-management initiatives. Projects such as the biometric upgrade at Beirut-Rafic Hariri International Airport demonstrate the export of European standards beyond the continent. Funding from the EU Internal Security Fund underpins cross-border data-sharing hubs.

The Middle East continues to direct oil revenues toward layered airport, energy-facility, and public-venue protection systems. Africa and Latin America advance more slowly but prioritize maritime and disaster-response capabilities in coastal cities prone to hurricanes and cyclones.