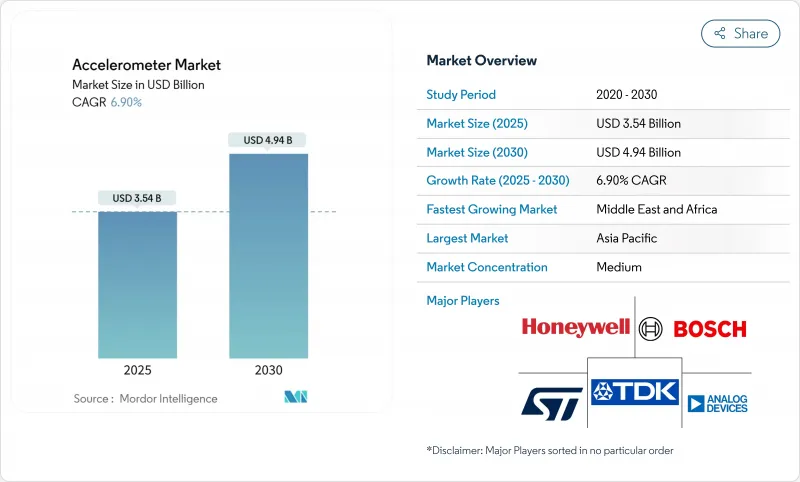

가속도계 시장은 2025년에 35억 4,000만 달러, 2030년에는 49억 4,000만 달러에 이르고, 이 기간 동안 CAGR은 6.9%를 나타낼 전망입니다.

소비자 장비, 자동차 안전 시스템 및 산업 모니터링에서 센서의 역할이 점점 더 중요해짐에 따라 수요도 커지고 있습니다. MEMS의 지속적인 소형화로 인해 시스템 비용이 절감되는 동시에 공간 제약이 있는 제품에 통합이 가능해졌으며, AI를 강화한 온칩 처리를 통해 가속도계가 엣지에서 실시간 통찰력을 제공할 수 있게 되었습니다. 또한 AI의 온칩 프로세싱을 통해 가속도 센서가 에지에서 실시간 통찰력을 제공할 수 있습니다. 자동차 산업의 Tier 1 공급업체는 ADAS 센서 융합 제품군에 높은 g 변형을 통합하고 정밀 등급 압전 장치는 항공우주 및 방위 틈새 분야에서 차별화된 가치를 유지합니다. 공급측의 리스크로는 8인치 MEMS 웨이퍼의 제약이 남아 있는 것이나 코모디티화한 소비자 부문에 있어서의 가격 압축 등이 있지만, 헬스 케어 웨어러블이나 재생에너지 인프라에 있어서의 설계의 승리가, 전체적인 성장 전망을 유지하고 있습니다.

3세대 MEMS 공정에서는 잡음 밀도를 낮추지 않고 다이 크기와 전력 소비를 줄이는 서브밀리프루프 매스 구조가 제조되었습니다. 보쉬의 소형 가속도계 2024 시리즈는 웨이퍼 레벨 칩 스케일 패키징을 통해 2g - 16g의 동적 범위를 유지하면서 재료 비용을 절감한 예를 보여줍니다. 대형 300mm MEMS 팹은 추가 규모 경제를 기대하며 OEM은 재료 비용 예산을 더 엄격한 범위에서 추가 감지 기능에 할당할 수 있습니다. ST 마이크로 일렉트로닉스의 LIS2DUXS12는 마이크로 와트 레벨에서 이벤트 분류를 가능하게 하는 머신러닝 코어를 통합하여 컴패니언 MCU의 필요성을 없애고 기판 점유 면적을 줄입니다. 주조 제조업체가 더 큰 웨이퍼로 전환함에 따라 평균 판매 가격이 떨어지고 비용에 민감한 IoT 노드의 잠재 수요가 파생되어 가속도계 시장의 성장 루프가 강화됩니다.

스마트폰, 이어폰, 피트니스 트래커는 여전히 대량 생산이 가능하지만, 2025년 설계 로드맵에서는 30μg/√Hz 이하의 노이즈 플로어와 며칠간의 배터리 수명을 위한 연속 동작을 필요로 하는 의료용 웨어러블로 전환하는 속도가 빨라지고 있습니다. 아날로그 디바이스의 ADXL380은 듀얼 신호 경로가 있는 트루 무선 이어폰을 대상으로 하며, 하나의 센서로 액티브 노이즈 제거 피드백과 헤드 제스처 인식을 모두 지원합니다. 의료기기에서 센서에 내장된 AI 추론은 클라우드 처리를 오프로드하고 병원에서 사용하기 위해 IEC 60601-1 인증을 받은 전도 감지 웨어러블을 실현합니다. 더 가치있는 임상 애플리케이션은 마진 압력을 완화하고 가속도계 시장을 최저 가격보다 품질을 중시하는 규제 의료 채널로 확장합니다.

스마트폰에서 2022년부터 2024년 사이에 관성 감지 부품 수가 30% 가까이 감소했기 때문에 공급업체는 임베디드 ML 코어와 저전력 일시 중단 모드에서 차별화를 도모해야 합니다. Kionix의 KX224 시리즈는 100만개 판매로 0.30달러 이하로 떨어지며 레거시 부품의 평균 판매 가격이 악화되고 있음을 뒷받침합니다. 공급업체는 마진을 회수하기 위해 자동 교정에 투자하고 있지만 공장의 트림 루틴은 설비 투자를 증가시키고 이익을 손상시킵니다. 이러한 불균형으로 인해 많은 경쟁사들은 손익 분기점의 PandL 위치에 머물며 가속도계 시장의 단기 수익 확대를 억제하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

MEMS 디바이스는 타의 추종을 불허하는 비용 성능의 균형으로 2024년 가속도계 시장의 72% 점유율을 획득했습니다. 200mm 웨이퍼에서의 대량 생산과 웨이퍼 레벨 패키징을 통해 MEMS는 스마트폰, 웨어러블 단말기, 자동차 ECU의 중심에 위치해 있습니다. 압전 유닛은 베이스가 작은 것, 방위 및 항공우주 사업자가 1µg 이하의 바이어스 안정성과 방사선 내성을 요구하기 때문에 연률 7.8%로 성장합니다. 압전 저항형과 정전용량형은 내충격성과 초저소비 전력이 절대적인 정밀도를 능가하는 틈새 산업용도에 대응합니다.

MEMS의 리더십은 통합의 이점에 달려 있습니다. ST 마이크로 일렉트로닉스의 센서 허브 아키텍처는 디지털 머신러닝 코어와 FIFO 버퍼를 다이에 직접 통합하여 외부 부품 수를 줄입니다. 그럼에도 불구하고, G-레인지, 극단적인 온도 또는 바이어스의 안정성이 MEMS의 한계를 초과하면 설계자는 압전 스택으로 되돌아갑니다.

완전 6자유도 측정에 대한 동향으로 3축 가속도계의 2024년 매출 점유율은 64.5%에 달할 전망입니다. OEM은 제스처 인식 및 진동 진단을 최소한의 센서 퓨전 오버헤드로 지원하기 위해 XYZ의 통합된 판독값을 선호합니다. 한편, 6축 또는 9축 기능을 내장한 콤보 IMU는 8.4%의 성장 궤도를 나타내, 드론, AR/VR 헤드셋, 로봇 공학이 견인하고 있습니다. 단축 장치는 틸트 스위치 및 자동차 에어백을 트리거하는 데 사용되지만 점유율은 꾸준히 떨어지고 있습니다.

Collins Aerospace의 SiIMU02는 손바닥 크기의 MEMS 어셈블리로 거의 광섬유 자이로의 정확성을 달성하고 다축 통합 프리미엄 엔드를 보여줍니다. 중견 소비자 제품은 가속도계, 자이로스코프 및 경우에 따라 지자기 센서를 프로그래머블 디지털 필터가 있는 단일 ASIC에 통합합니다. 이 집계는 PCB 면적과 부품 비용을 줄이고 용도의 복잡성이 증가함에 따라 가속도계 시장의 기세를 유지합니다.

아시아태평양은 중국의 소비자용 전자기기 수출 거점과 8인치 MEMS 파운드리의 밀집 지역에 의해 지원되고 있으며, 2024년 세계 매출의 46.8%를 차지합니다. 심천에 본사를 두고 있는 MEMSIC은 국내 스마트폰 OEM용 커패시터형 가속도계에 주력해 3자리 성장을 기록했습니다. 일본과 한국은 자동차 및 산업 분야에 고신뢰성 제품을 제공하고 대만 파운드리는 수탁 제조를 지원합니다. 이 지역의 가속도계 시장은 CAGR 6.4%로 안정적으로 확대되지만, 웨이퍼 용량의 제약과 인건비의 상승이 상승을 억제합니다.

중동 및 아프리카는 사우디아라비아의 비전 2030 자극책이 현지 반도체 이니셔티브에 자금을 제공하고 터빈 진동 모니터링를 필요로 하는 신재생에너지 자산의 규모를 확대하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 8.7%로 가장 빠른 성장률을 기록할 것입니다. 이집트와 모로코의 풍력 발전소는 ISO 10816의 예지 보전 벤치마크를 충족시키기 위해 3축 가속도계를 채택합니다. 유럽의 센서 제조업체와의 관민 파트너십을 통해 기술 이전이 촉진되고 현지 생산이 가속도계 시장을 견인하고 있습니다.

북미는 자동차 ADAS 지침과 고급 산업용 IoT 설치 기반으로 강력한 2위를 유지하고 있습니다. 석유 및 가스, 화학, 금속업계의 Industry 4.0 유지보수 전략의 채택은 견고하고 위험 구역에 대응한 가속도 센서 수요를 견인하고 있습니다. 유럽은 OEM이 품질과 기능 안전을 선호하기 때문에 평균 판매 가격이 높고 약간의 차이로 후진을 숭배합니다. EU의 Horizon Europe 로봇 프로젝트에 대한 자금 지원은 정밀 등급 센서의 보급을 더욱 자극하고 가속도계 시장에 대한 지역 진입을 강화하고 있습니다.

The accelerometer market is valued at USD 3.54 billion in 2025 and is forecast to reach USD 4.94 billion in 2030, representing a 6.9% CAGR over the period.

Demand scales with the sensor's increasingly critical role in consumer devices, automotive safety systems and industrial monitoring. Continuous MEMS miniaturization lowers system cost while enabling integration into space-constrained products, and AI-enhanced on-chip processing now lets accelerometers deliver real-time insights at the edge. Tier-1 automotive suppliers are embedding high-g variants in ADAS sensor-fusion suites, while precision-grade piezoelectric devices sustain differentiated value in aerospace and defense niches. Supply-side risks include lingering 8-inch MEMS wafer constraints and price compression in commoditized consumer segments, but design wins in healthcare wearables and renewable-energy infrastructure keep the overall growth outlook intact.

Third-generation MEMS processes now fabricate sub-millimeter proof-mass structures that cut die size and power draw without degrading noise density. Bosch's miniature 2024 accelerometer series exemplifies how wafer-level chip-scale packaging lowers material cost while sustaining +-2 g to +-16 g dynamic range. Larger 300 mm MEMS fabs promise further scale economies, allowing OEMs to allocate tighter bill-of-materials budgets to additional sensing functions. STMicroelectronics' LIS2DUXS12 integrates a machine-learning core enabling event classification at microwatt levels, removing the need for a companion MCU and shrinking board footprint. As foundries migrate to larger wafers, average selling prices decline and unlock latent demand in cost-sensitive IoT nodes, reinforcing the growth loop for the accelerometer market.

Smartphones, earbuds and fitness trackers remain volume engines, but 2025 design roadmaps reveal an accelerating pivot toward medical-grade wearables that require sub-30 μg/√Hz noise floors and continuous operation for multi-day battery life. Analog Devices' ADXL380 targets true-wireless earbuds with dual signal paths so a single sensor supports both active-noise-cancellation feedback and head-gesture recognition. In medical devices, AI-inference embedded in the sensor offloads cloud processing, enabling fall-detection wearables certified under IEC 60601-1 for hospital use. Higher-value clinical applications ease margin pressure and expand the accelerometer market into regulated healthcare channels that favor quality over lowest price.

In smartphones the bill-of-materials allotment for inertial sensing shrank by nearly 30% between 2022 and 2024, pushing suppliers to differentiate with embedded ML cores and lower power-suspend modes. Kionix's KX224 series sells below USD 0.30 at million-piece volumes, underscoring deteriorating average selling prices for legacy parts. Vendors invest in automated calibration to recoup margin; however, factory-trim routines raise capex and erode benefit. The imbalance confines many competitors to break-even PandL positions, tempering near-term revenue expansion for the accelerometer market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

MEMS devices captured 72% accelerometer market share in 2024 owing to unmatched cost-performance balance. Volume manufacturing on 200 mm wafers combined with wafer-level packaging positions MEMS at the heart of smartphones, wearables and automotive ECUs. Piezoelectric units, while representing a smaller base, advance at 7.8% annually as defense and aerospace operators demand sub-1 µg bias stability and radiation tolerance. Piezoresistive and capacitive variants serve niche industrial uses where shock survivability or ultra-low power trumps absolute precision.

MEMS leadership rests on integration advantages. STMicroelectronics' sensor-hub architecture merges a digital machine-learning core and FIFO buffers directly on the die, trimming external component count. Still, when g-range, temperature extremes or bias stability exceed MEMS limits, designers revert to piezoelectric stacks.

The trend toward full-six-degree-of-freedom measurement places 3-axis accelerometers at 64.5% revenue share in 2024. OEMs prefer unified X-Y-Z readings to support gesture recognition and vibration diagnostics with minimal sensor fusion overhead. Meanwhile, combo IMUs embedding 6-axis or 9-axis capability demonstrate an 8.4% growth trajectory, driven by drones, AR/VR headsets and robotics, where synchronized gyro-accelerometer data simplifies algorithm tuning. Single-axis devices persist in tilt switches and automotive airbag triggers, but share steadily erodes.

Collins Aerospace's SiIMU02 illustrates the premium end of multi-axis integration, achieving near-fiber-optic gyro accuracy in a palm-sized MEMS assembly. For mid-tier consumer products, suppliers consolidate accelerometer, gyroscope and sometimes magnetometer on a single ASIC with programmable digital filters. This convergence compresses PCB area and bill-of-materials cost, ensuring the accelerometer market maintains momentum as application complexity rises.

Accelerometer Market is Segmented by Type (MEMS Accelerometers, Piezoelectric Accelerometers, and More), Dimension (1-Axis, 2-Axis, and More), End User (Consumer Electronics, Automotive, and More), Performance Grade (Consumer Grade, Industrial Grade, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific controlled 46.8% of global revenue in 2024, anchored by China's consumer-electronics export base and a dense 8-inch MEMS foundry footprint. Shenzhen-headquartered MEMSIC recorded triple-digit growth after focusing capacitor-type accelerometers on domestic smartphone OEMs. Japan and South Korea contribute high-reliability variants for automotive and industrial sectors, while Taiwan's pure-play foundries support contract manufacturing. The region's accelerometer market will expand at a steady 6.4% CAGR, although wafer-capacity constraints and rising labor costs temper upside.

The Middle East and Africa represents the fastest 8.7% CAGR through 2030 as Saudi Arabia's Vision 2030 stimulus funds local semiconductor initiatives and scales renewable-energy assets requiring turbine vibration monitoring. Wind farms across Egypt and Morocco adopt triaxial accelerometers to meet ISO 10816 predictive-maintenance benchmarks. Regional public-private partnerships with European sensor makers expedite technology transfer, accelerating indigenous production and lifting the local accelerometer market trajectory.

North America holds a strong second position driven by automotive ADAS mandates and an advanced industrial IoT install base. Adoption of Industry-4.0 maintenance strategies across oil and gas, chemicals and metals drives demand for rugged, hazardous-area-rated accelerometers. Europe trails marginally yet enjoys higher average selling prices as OEMs prioritize quality and functional safety. EU funding for Horizon Europe robotics projects further stimulates precision-grade sensor uptake, reinforcing regional participation in the accelerometer market.