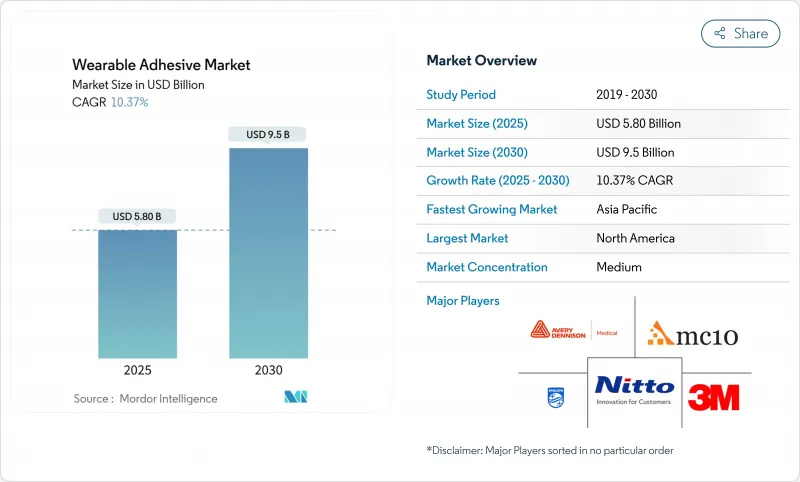

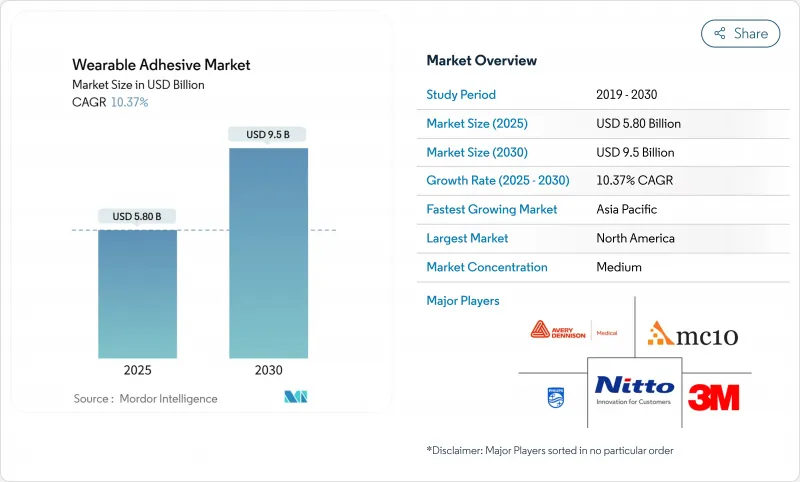

웨어러블 접착제 시장 규모는 2025년에 58억 달러, 2030년에는 95억 달러에 이르고, 예측 기간 중 CAGR은 10.4%를 나타낼 전망입니다.

성장을 지원하는 것은 세 가지 동시 이동입니다. 원격 모니터링 프로그램을 확대하는 의료의 디지털화, 산업 및 방위 바이오메트릭스의 꾸준한 성장, 장착 수명을 연장하면서 피부 반응 리스크를 저감하는 급속한 화학 혁신입니다. 2024년 매출액 점유율은 북미가 37.8%로 톱이지만, 중국의 의료기기 생산이 2025년까지 2,100억 달러의 국내 시장으로 성장함에 따라, 아시아태평양이 CAGR 10.9%로 가장 급성장하고 있는 지역이 됩니다. 이 부문의 기세는 하이드로겔 제형, 치료용 약물 전달 패치 및 재택 간호 환경에서 가장 두드러지며, 각각이 최상위 속도를 초과하는 성장을 보이고 있습니다.

2024년 3월에 FDA가 시판품 최초의 지속형 포도당 모니터인 Dexcom Stelo를 인가함으로써 2,500만 명의 미국 성인 제2형 당뇨병 환자를 대상으로 한 새로운 최종 사용자 풀을 확보하고 소매 채널 전반에 걸친 접착제 사용량 증가를 촉진했습니다. 벤처기업의 자금조달도 비슷한 기세를 보이고 있습니다. Biolinq는 2024년 4월에 5,800만 달러를 조달하여 장시간 사용 가능한 피부 접착제에 의존하는 고정밀 다분석 바이오센서를 개발했습니다. Dexcom의 G7 플랫폼은 15.5일간의 신뢰할 수 있는 접착을 달성하고 교체 빈도를 줄이고 소비자에게 널리 호소합니다. 이들 이정표는 각각 착용가능한 접착제 시장을 임상 범위를 넘어 확장하고 일상적인 건강 관리에 패치를 통합합니다.

Contact Dermatitis 잡지의 검토된 데이터에 따르면, 아크릴산 이소보르닐(IBOA)은 특정 CGM 사용자에 있어서 알레르기의 방아쇠가 되는 것으로 지적되고 있으며, 업계 전체의 처방 변경을 촉구했습니다. 다이맥스사는 IBOA 프리, TPO 프리 2000-MW 시리즈로 이에 대응했지만, 피부 접촉에 대한 ISO 10993의 요건은 충족하고 있습니다. 매사추세츠 공과 대학의 연구자들은 섬유화를 피하고 면역 거부 반응을 일으키지 않고 수개월 이식을 가능하게하는 하이드로 겔 장벽을 추가했습니다. 이러한 돌파구는 피부 유해 사건과 관련된 규제 장애물을 완화시켜 웨어러블 접착제 시장을 확대합니다.

FDA의 MAUDE 데이터베이스는 점착제 기반 웨어러블에 대한 피부염 불만이 증가하고 있음을 설명합니다. iRhythm의 Zio Monitor와 Abbott의 FreeStyle Libre 3은 모두 화학 화상이나 부정확한 측정과 관련된 경고 또는 리콜에 직면합니다. 소아 화상의 사례가 메가다인 전극의 시정을 일으키고 하나의 처방으로 모든 것에 맞는 설계는 취약한 피부 요구에 불충분하다는 것을 보여주었습니다. 이러한 사건은 웨어러블 접착제 시장 규모를 일시적으로 축소시켜 재제조 비용에 불을 붙이고 적극적인 생체 적합성 증명을 선호하는 규제 환경에 박차를 가했습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

실리콘은 2024년에 웨어러블 접착제 시장의 36.2%를 차지했는데, 이는 저자극성 프로파일, 재포지셔닝성, 입증된 ISO 10993 기록 때문입니다. NuSil과 Elkem은 롤 투 롤 코팅 라인의 점도 범위를 최적화하여 의료 분야의 계약을 획득했습니다. 하이드로겔 점착제는 현재 23%에 불과하지만 땀을 빨아들이고 장시간의 작업 시프트에서도 전기적 접촉을 유지하기 위해 CAGR 11.4%로 가속하고 있습니다. 하이드로겔 패치의 웨어러블 접착제 시장 규모는 현재의 기세가 계속되면 2030년까지 30억 달러 이상에 달할 것으로 보입니다. 하이브리드 실록산-하이드로겔 매트릭스는 특히 통기성과 전도성을 모두 필요로 하는 유연한 인쇄회로 어셈블리를 위한 중간 경로로 부상하고 있습니다.

2차 기술 혁신은 전도성과 자기 복구를 목표로 합니다. Frontiers in Chemistry '는 기계적 손상 후 결합의 무결성을 회복하고 실시간 심전도 포착을 허용하는 폴리 비닐 알콜 하이드로겔을 기록합니다. 캘리포니아 대학 버클리 학교에서 발표한 재활용 가능한 리포산 접착제는 지속 가능한 이야기를 확장하고 성능 데이터가 성숙하면 의료 폐기물을 줄일 수 있다고 생각합니다. 이러한 녹색 특성은 곧 조달 점수에 영향을 미치고 웨어러블 접착제 시장을 순환 모델로 이끌 수 있습니다.

지속 포도당 모니터, 심전도 패치, 불임 치료 추적기는 41.4%의 발판을 구축하여 웨어러블 접착제 시장에서 진단 주도권을 확립했습니다. 2025년 4월, 덱스콤의 G7 익스텐션이 15일간의 장착 기록을 달성했으며, 점착력 섹터 표준이 상승했습니다. 그러나 치료용 패치는 최초 통과 대사를 우회하는 마이크로니들형 약물전달 어레이를 원동력으로 하여 CAGR 12.0%로 질주하고 있습니다. 이 서브클래스의 웨어러블 접착제 시장 규모는 이미 8억 달러를 넘어서고, 접착 성능이 약물전달의 안전 지표를 겸하고 있기 때문에 프리미엄 가격을 즐기고 있습니다.

경피 신경 조절 및 통증 관리 장치는 이러한 경향을 더욱 강화하고, 일관된 피부 임피던스를 필요로 하기 때문에 점착제의 선택이 중요한 임상 파라미터가 됩니다. 2024년에 발행된 FDA의 지침에서는 패치제 시스템의 패치 후 72시간의 박리 테스트가 특히 요구되고 있어 신규 참가 기업에 있어서는 기술적인 장벽이 되고 있습니다. 스마트 상처 코팅은 수분 센서와 항균제 릴리스를 통합하여 두 제품의 세계를 융합시켜 차별화의 긴 경로를 제공합니다.

규제의 명확화로 북미가 37.8%의 점유율로 선두를 유지. 의료기기의 생물학적 평가에 관한 FDA의 2024년 업데이트는 이미 IBOA가 없는 화학물질을 사용하고 있는 공급업체들에게 조기 진입의 이점을 가져왔습니다. 이 지역은 또한 10일 이상의 착용에 대한 주장을 검증하는 많은 임상시험을 개최하고 있으며, 데이터와 상환의 무결성의 선순환을 포함하고 있습니다.

아시아태평양은 중국의 5개년 계획에 따라 국내 의료기기 혁신과 접착제 코팅 라인에 자금이 공급되어 CAGR이 10.9%로 가장 빨리 기록되었습니다. 2023년 후반에 발효된 인도의 새로운 등록 의무 제도는 열악한 수입품을 필터링하고 평판 좋은 공급업체를 합작 투자로 유도하여 웨어러블 접착제 시장의 발자취를 확대합니다.

유럽은 꾸준히 성장하고 있지만, 그린딜은 재활용성과 용매 삭감을 추진하고 단가를 약간 끌어올릴 수 있는 수계(water-based) 시스템 중심으로 연구개발(R&D) 방향이 전환되고 있으며, 이로 인해 단가가 다소 상승할 가능성이 있습니다.

The wearable adhesive market size stands at USD 5.80 billion in 2025 and is on course to hit USD 9.50 billion by 2030, advancing at a 10.4% CAGR during the forecast period.

Growth is underpinned by three simultaneous shifts: health-care digitalization that expands remote monitoring programs, steady gains in industrial and defense biometrics, and rapid chemistry innovation that lowers skin-reaction risk while lengthening wear life. North America leads with 37.8% revenue share in 2024, but Asia-Pacific is the fastest-expanding geography at a 10.9% CAGR as Chinese medical-device production scales toward a USD 210 billion domestic market by 2025. Segment momentum is most visible in hydrogel formulations, therapeutic drug-delivery patches, and home-care settings, each growing more than the headline pace.

The FDA's March 2024 clearance of Dexcom Stelo, the first over-the-counter continuous glucose monitor, unlocked a new end-user pool of 25 million U.S. adults with Type 2 diabetes and in turn catalyzed adhesive-volume growth across retail channels. Venture funding signals similar momentum: Biolinq raised USD 58 million in April 2024 to scale precision multi-analyte biosensors that hinge on long-wear skin adhesives. Longer sensor life is now feasible; Dexcom's G7 platform reaches 15.5 days of reliable adhesion, reducing replacement frequency and widening consumer appeal. Each of these milestones expands the wearable adhesive market beyond clinical silos and embeds patches in everyday wellness management.

Peer-reviewed data in Contact Dermatitis flagged isobornyl acrylate (IBOA) as an allergy trigger in certain CGM users, prompting industry-wide reformulations. Dymax answered with an IBOA-free and TPO-free 2000-MW series that still meets ISO 10993 requirements for skin contact. MIT researchers added a hydrogel barrier that averts fibrosis and allows months-long implantation without immune rejection. Such breakthroughs widen the wearable adhesive market by easing regulatory hurdles tied to adverse skin events.

The FDA's MAUDE database lists rising dermatitis complaints against adhesive-based wearables; iRhythm's Zio Monitor and Abbott's FreeStyle Libre 3 both faced warnings or recalls tied to chemical burns or inaccurate readings. Pediatric burn cases triggered a Megadyne electrode correction, showing that one-formula-fits-all designs fall short of vulnerable-skin needs. These events temporarily cap the wearable adhesive market size, spark reformulation costs, and fuel a regulatory climate that favors proactive biocompatibility proof.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Silicone held 36.2% of the wearable adhesive market in 2024 owing to hypoallergenic profiles, repositionability, and proven ISO 10993 records. NuSil and Elkem locked in health-care contracts by optimizing viscosity ranges for roll-to-roll coating lines. Hydrogel chemistries, although only 23% today, accelerate at an 11.4% CAGR as they wick perspiration and maintain electrical contact over long new work shifts. The wearable adhesive market size for hydrogel patches will likely surpass USD 3 billion before 2030 if current momentum persists. Hybrid siloxane-hydrogel matrices emerge as a middle path, especially for flexible printed-circuit assemblies that need both breathability and conductivity.

Second-order innovation targets conductivity and self-healing. Frontiers in Chemistry documented polyvinyl-alcohol hydrogels that restore bond integrity after mechanical damage and allow real-time ECG capture. Recyclable lipoic-acid adhesives from UC Berkeley extend sustainability narratives and could cut medical waste once performance data mature. Such green attributes may soon influence procurement scores, nudging the wearable adhesive market toward circular models.

Continuous glucose monitors, ECG patches, and fertility trackers established a 41.4% foothold, anchoring diagnostic leadership within the wearable adhesive market. The sector standard for adhesion rose in April 2025 when Dexcom's G7 extension hit a 15-day wear record. Yet therapeutic patches sprint faster at a 12.0% CAGR, powered by microneedle drug-delivery arrays that bypass first-pass metabolism. The wearable adhesive market size for this sub-class already exceeds USD 800 million and enjoys premium pricing because adhesion performance doubles as a drug-delivery safety metric.

Transdermal neuromodulation and pain-management devices reinforce the trend; their need for consistent skin impedance makes adhesive selection a critical clinical parameter. FDA guidance issued in 2024 specifically calls out 72-hour post-application peel tests for drug-in-adhesive systems, raising technical barriers for newcomers. Smart wound dressings fuse both product worlds by integrating moisture sensors with antimicrobial release, offering a long runway for differentiation.

The Wearable Adhesive Market Report is Segmented by Adhesive Chemistry (Silicone, Acrylic, Hydrogel, Hydrocolloid, and Others), Product Type (Diagnostic / Monitoring Patches, Therapeutic Patches, and More), Application (Healthcare, Sports and Fitness, Industrial and Military, and More), End-User (Hospitals, Clinics, Home-Care Settings, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Regulatory clarity keeps North America on top with 37.8% share. The FDA's 2024 update on biological evaluation of medical devices gave early-mover benefits to suppliers already using IBOA-free chemistries. The region also hosts many of the clinical trials validating 10-day plus wear claims, embedding a virtuous cycle of data and reimbursement alignment.

Asia-Pacific logs the quickest 10.9% CAGR as China's Five-Year Plan funds domestic device innovation and local adhesive coating lines. India's new mandatory registration scheme, effective late-2023, filters sub-par imports and nudges reputable suppliers into joint ventures that expand the wearable adhesive market footprint.

Europe grows steadily, but its Green Deal pushes recyclability and solvents reduction, prompting R&D pivots toward water-based systems that may modestly lift unit costs.