솔라 컨트롤 윈도우 필름 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Solar Control Window Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1836602

리서치사:Mordor Intelligence

발행일:2025년 06월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

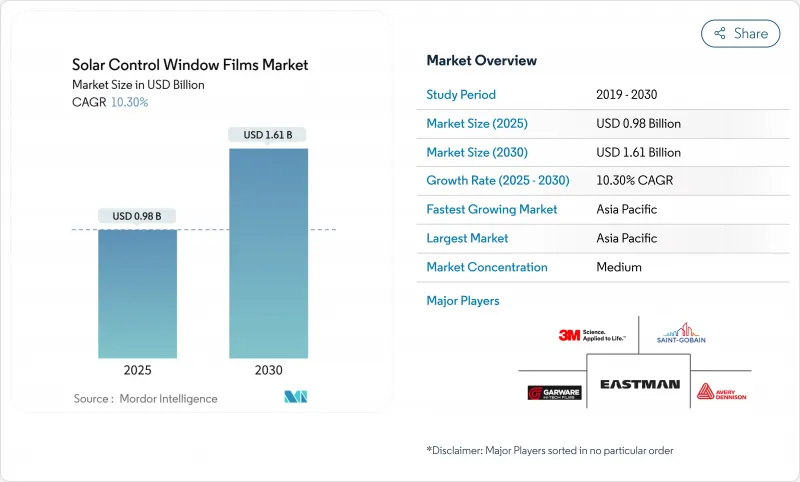

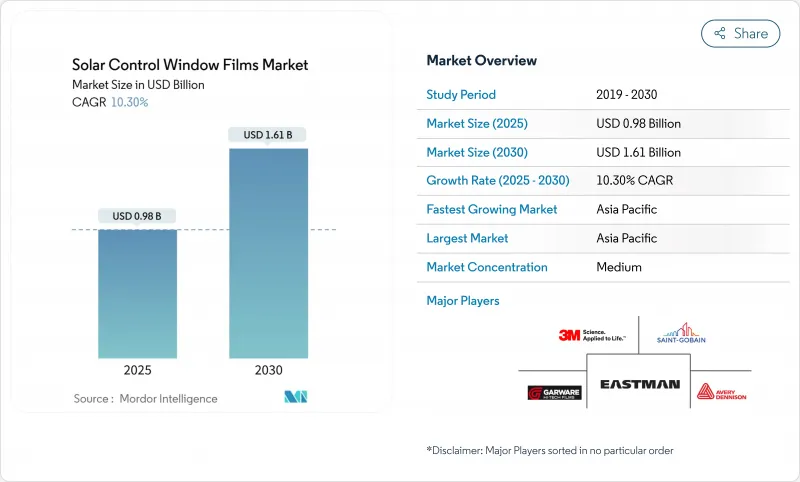

솔라 컨트롤 윈도우 필름 시장 규모는 2025년에 9억 8,000만 달러, 예측 기간 중(2025-2030년) CAGR은 10.30%를 나타내고, 2030년에는 16억 1,000만 달러에 달할 것으로 예측되고 있습니다.

진공 코팅된 반사 제품은 높은 적외선 제거 성능과 중립적인 미관을 겸비하고 있기 때문에 현재의 사양의 주류가 되고 있으며, 세라믹과 메탈릭의 하이브리드 제품은 온도 변화가 심한 기후에 있어서 성능 임계값을 높입니다. 아시아태평양의 건설 붐, EU의 넷 제로 의무화, 미국의 재정 우대 조치는 모두 원재료비가 변동해도 수량이 계속 확대되도록 수렴하고 있습니다. 이러한 힘으로 태양광 제어 창 필름 시장은 보다 광범위한 에너지 효율 가치에서 매우 중요한 지렛대로 강화되고 있습니다.

솔라 컨트롤 윈도우 필름 세계 시장 동향과 통찰

탄소발자국 삭감의 중시의 향상

기업의 기후 변화에 대한 서약은 필름이 냉방부하를 5-15% 삭감하고 과학적 근거에 근거한 배출목표에 적격이기 때문에 솔라 컨트롤 윈도우 필름 시장을 높이고 있습니다. 피크 수요 감소는 더운 지역에서 송전망의 강인화 목표에 부합합니다. 또한 부동산 투자 신탁은 글레이징 업그레이드를 이연 유지 보수가 아닌 자산 가치를 높이는 것으로 취급합니다. 신재생에너지의 보급이 가속됨에 따라 필름과 같은 수요측의 솔루션은 부하 프로파일을 안정시키는 명성을 얻고 있습니다. 이러한 위치는 설비투자의 감속기에서도 조달예산을 견고하게 하고 있습니다.

유럽의 넷제로 건축 기준이 Low-E 필름의 채택을 촉진

주요 하이라이트

EU의 개정 건축물 에너지 성능 지령은 회원국에게 공공 부문의 바닥 면적의 연간 3%를 개수하고, 2050년까지 제로 방출 기준을 충족할 것을 의무화하고 있습니다. 레트로 지향의 목표는 비싼 프레임을 교체하지 않고 열 성능을 향상시킴으로써 윈도우 필름을 향상시킵니다. 다국적 기업은 현재 아시아와 북미에서 동일한 외피 기준을 복제하고 유럽 벤치마크를 세계에 수출하고 있습니다. 라이프사이클 카본 조항은 또한 높은 엠보디 카본의 글레이징 교환보다 박막 리노베이션에 유리합니다. 그 결과 공급업체는 공공 입찰에서 더 오랫동안 주문할 수 있습니다.

프리미엄 상업 타워에서 동적 스마트 글레이징으로 대체 위험

주요 하이라이트

일렉트로크로믹과 써모크로믹 유닛은 유리를 동적으로 착색해 정적 필름으로는 대응할 수 없는 글레어의 경감을 제공합니다. 제조 비용이 낮아짐에 따라 외관 컨설턴트는 프레스티지 프로젝트의 이중 스킨과 단위화 된 커튼 월에 이러한 시스템을 지정하기 시작했습니다. 가격 프리미엄은 필름 설치의 3-5배 정도에 머물지만, 장기적인 에너지 시뮬레이션에서는 동적 제어가 유리한 경우가 많습니다. 필름 제조업체는 중급 시장을 위한 매출을 강화하고 스마트 유리 투자 회수가 12년을 넘는 개수 채널을 확대함으로써 대응하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

아시아태평양 건설 업계의 급성장

자외선 방지와 건강에 대한 우려

고온 다습 기후의 박리에 대한 보증과 관련된 배상 책임

부문 분석

진공 코팅 반사 제품은 2024년 매출의 43%를 차지했으며, 그 10.62%의 연평균 복합 성장률(CAGR)로 이 부문의 태양광 제어 윈도우 필름 시장 규모는 염색 및 클리어의 대체 제품을 크게 이끌고 있습니다. 건축가는 가시광선을 투과하면서 근적외선을 선택적으로 반사하는 초박형 금속 스택을 높이 평가합니다.

필름 제조업체는 현재 방사율 0.20 이하를 달성하는 은 인듐, 니켈 합금을 사용한 스퍼터 챔버를 배치하고 있습니다. 집합 주택의 개수에서는 염료로 염색한 폴리에스테르 필름이, 당초의 합리적인 가격에서는 아직 매력적이지만, 에너지 규제의 강화에 의해 꾸준히 반사형 구조로 양을 돌리고 있습니다.

세라믹 흡수체는 색상 안정성, 고융점, 무시할 수 있는 고주파 간섭을 반영하여 2024년 매출의 46%를 차지했습니다. 자동차 OEM이 나노 세라믹 층을 선호하는 이유는 텔레매틱스 안테나의 신호 감쇠를 피하기 위해서입니다. 그러나, 정제된 금속 나노입자 분산액이 제조 비용을 절감하고 디포거 그리드의 전도성의 이점을 회복함에 따라, 태양광 제어 윈도우 필름 시장 점유율의 이점은 감소할 수 있습니다.

메탈릭 전용 필름은 무지개색의 발생을 억제하는 스퍼터 스택의 개량에 도움이 되어, CAGR 10.56%로 성장하고 있습니다. 하이브리드 아키텍처는 현재 은 시드층 위에 알루미나와 실리카를 퇴적시켜 저반사율과 급격한 적외 저지를 겸비한 복합 광학 스택을 만들어 내고 있습니다. 이러한 진보는 역사적인 경계를 모호하게 하고, 이 카테고리를 기능 특화형 처방, 눈부심 억제, 낙서 방지, 광전지 오버레이로 밀고 진행하고 있습니다.

지역별 분석

아시아태평양은 2024년 수익의 45%를 차지했고, CAGR 10.78%로 성장하여, 태양열 컨트롤 윈도우 필름 시장의 중심이 되고 있습니다. 중국의 녹색 빌딩 평가 기준 GB/T 50378과 인도의 Eco-Niwas는 태양열 이득 계수를 의무화하고 있어 고선택성 필름의 보급을 가속화하고 있습니다.

북미에서는 리노베이션 인센티브가 정착되어 있습니다. 또한 캘리포니아 주에서는 Title 24의 개정으로 외관의 외관을 바꾸지 않고 박막 필름이 적합한 외부 차광 계수의 임계치를 높였습니다.

유럽은 성숙한 보급률을 유지하면서도 2030년 'Fit-for-55' 기후 패키지와 관련된 수요의 두 번째 물결을 누리고 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사의 성과

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

시장 개요

시장 성장 촉진요인

탄소발자국 삭감에 대한 관심 증가

유럽의 넷제로 건축 기준이 Low-E 필름의 보급을 촉진

아시아태평양 건설 업계 성장

자외선 보호와 건강에 대한 우려

아시아태평양에서의 주광 제어를 필요로 하는 전자상거래 창고 건설의 급증

시장 성장 억제요인

프리미엄 상업 타워의 다이나믹 스마트 글레이징에 의한 대체 리스크

고온 다습 기후 하에서의 박리에 대한 보증과 관련된 배상 책임

불안정한 폴리에스테르 및 나노세라믹 원료 가격

밸류체인 분석

Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

라이벌의 격렬함

가격 분석

제5장 시장 규모 및 성장 예측(금액)

필름 유형별

클리어(무반사)

염색(비반사)

진공 코팅(반사성)

고기능 필름

기타 필름 유형

흡수체 유형별

유기

무기/세라믹

금속

설치 단계별

신축

레트로 핏

최종 사용자 산업별

건설

자동차

해양

디자인

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

스페인

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

시장 집중도

전략적 동향

시장 점유율 분석

기업 프로파일

3M

Avery Dennison Corporation

Decorative Films, LLC

Eastman Chemical Company

Garware Hi-Tech Films

Johnson Window Films, Inc.

LINTEC Corporation

Madico

Polytronix, Inc.

Purlfrost

Saint-Gobain

Sharpline Converting, Inc.

SOLAR CONTROL FILMS INC

Thermolite, LLC

TintFit Window Films Ltd.

TORAY INDUSTRIES, INC.

Ziebart International

제7장 시장 기회와 전망

SHW

영문 목차

영문목차

The Solar Control Window Films Market size is estimated at USD 0.98 billion in 2025, and is expected to reach USD 1.61 billion by 2030, at a CAGR of 10.30% during the forecast period (2025-2030).International decarbonization rules, rising utility costs, and proven payback periods below three years keep demand resilient.

Vacuum-coated reflective products dominate current specifications because they combine high infrared rejection with neutral aesthetics, while ceramic-metallic hybrids push performance thresholds in climates with extreme temperature swings. Asia Pacific construction booms, EU net-zero mandates, and US fiscal incentives all converge to keep volumes expanding even when raw-material costs fluctuate. These forces collectively reinforce the solar control window films market as a pivotal lever in the wider energy-efficiency value.

Global Solar Control Window Films Market Trends and Insights

Growing Emphasis on Reducing Carbon Footprints

Corporate climate pledges elevate the solar control window films market because films shave 5-15% cooling loads and qualify for science-based emission targets. Peak-demand trimming aligns neatly with grid-resilience objectives in hot regions. Real-estate investment trusts also treat glazing upgrades as accretive to asset value rather than as deferred maintenance. As renewable penetration accelerates, demand-side solutions such as films gain prestige for stabilizing load profiles. This positioning solidifies procurement budgets even during capex slowdowns.

Net-Zero Building Codes in Europe Driving Low-E Film Adoption

Key Highlights

The EU's recast Energy Performance of Buildings Directive compels member states to renovate 3% of public-sector floor area annually and to meet zero-emission standards by 2050. Retro-orientated targets elevate window films by boosting thermal performance without costly frame replacement. Multinationals now replicate the same envelope standards in Asia and North America, exporting European benchmarks worldwide. Lifecycle-carbon clauses also favor thin-film retrofits over high-embodied-carbon glazing swaps. Consequently, suppliers see longer order visibility in public tenders.

Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers

Key Highlights

Electrochromic and thermochromic units dynamically tint glass, providing glare mitigation that static films cannot match. As manufacturing costs fall, facade consultants increasingly specify these systems for double-skin or unitized curtain walls in prestige projects. Although price premiums remain 3-5 times film installations, long-term energy simulations often favor dynamic controls. Film suppliers respond by sharpening mid-market pitches and expanding retrofit channels where smart glass paybacks extend beyond 12 years.

Other drivers and restraints analyzed in the detailed report include:

Upsurge in the Asia-Pacific Construction Industry

Awareness of UV Protection and Health Concerns

Warranty-Linked Liability for Delamination in Hot-Humid Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vacuum-coated reflective products captured 43% of 2024 revenue, and their 10.62% CAGR keeps the solar control window films market size for this segment well ahead of dyed and clear alternatives. Architects value the micro-thin metallic stack that selectively reflects near-infrared while admitting visible light.

Film manufacturers now deploy sputter chambers using silver, indium, and nickel alloys that achieve emissivity below 0.20. In mass-housing retrofits, dyed polyester films still appeal for initial affordability, yet energy-code tightening steadily redirects volume to reflective constructions.

Ceramic absorbers held 46% of 2024 revenue, reflecting their color stability, high melting point, and negligible radio-frequency interference. Automotive OEMs favor nano-ceramic layers because they avoid signal attenuation for telematics antennas. The solar control window films market share advantage may narrow, however, as refined metallic nanoparticle dispersions cut manufacturing costs and restore conductivity benefits for defogger grids.

Metallic-only films are marching at 10.56% CAGR, aided by sputter stack refinements that curb iridescence. Hybrid architectures now deposit alumina or silica atop silver seed layers, creating composite optical stacks that combine low reflectance with steep infrared rejection. Such progress blurs historic boundaries and pushes the category toward function-specific formulations, glare suppression, anti-graffiti, or photovoltaic overlay.

The Solar Control Window Films Market Report Segments the Industry by Film Type (Clear, Dyed, Vacuum Coated, and More), Absorber Type (Organic, Inorganic/Ceramic, and Metallic), Installation (New-Build and Retrofit), End-User Industry (Construction, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD)

Geography Analysis

Asia Pacific commanded 45% of 2024 revenues and is expanding at a 10.78% CAGR, ensuring it remains the gravitational center of the solar control window films market. China's Green Building Evaluation Standard GB/T 50378 and India's Eco-Niwas mandate solar-heat-gain coefficients that accelerate high-selectivity film uptake.

Retrofit incentives anchor North America. The Inflation Reduction Act's enhanced tax deduction accelerates envelope upgrades across federal and private portfolios, and California's Title 24 revisions elevate exterior-shade coefficient thresholds that thin films meet without altering facade appearance.

Europe maintains mature penetration yet enjoys a second wave of demand tied to the 2030 "Fit-for-55" climate package.

3M

Avery Dennison Corporation

Decorative Films, LLC

Eastman Chemical Company

Garware Hi-Tech Films

Johnson Window Films, Inc.

LINTEC Corporation

Madico

Polytronix, Inc.

Purlfrost

Saint-Gobain

Sharpline Converting, Inc.

SOLAR CONTROL FILMS INC

Thermolite, LLC

TintFit Window Films Ltd.

TORAY INDUSTRIES, INC.

Ziebart International

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 Introduction

1.1 Study Assumptions and Market Definition

1.2 Study Deliverables

1.3 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

4.1 Market Overview

4.2 Market Drivers

4.2.1 Growing Emphasis on Reducing Carbon Footprints

4.2.2 Net-Zero Building Codes in Europe Driving Low-E Film Adoption

4.2.3 Upsurge in the Asia-Pacific Construction Industry

4.2.4 Awareness of UV Protection and Health Concerns

4.2.5 Rapid E-Commerce Warehouse Construction Requiring Day-Lighting Control in APAC

4.3 Market Restraints

4.3.1 Substitution Risk from Dynamic Smart Glazing in Premium Commercial Towers

4.3.2 Warranty-Linked Liability for Delamination in Hot-Humid Climates

4.3.3 Volatile Polyester and Nano-Ceramic Raw Material Prices

4.4 Value Chain Analysis

4.5 Porter's Five Forces

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Power of Buyers

4.5.3 Threat of New Entrants

4.5.4 Threat of Substitutes

4.5.5 Intensity of Rivalry

4.6 Pricing Analysis

5 Market Size and Growth Forecasts (Value)

5.1 By Film Type

5.1.1 Clear (Non-reflective)

5.1.2 Dyed (Non-reflective)

5.1.3 Vacuum-Coated (Reflective)

5.1.4 High Performance Films

5.1.5 Other Film Types

5.2 By Absorber Type

5.2.1 Organic

5.2.2 Inorganic / Ceramic

5.2.3 Metallic

5.3 By Installation Stage

5.3.1 New-Build

5.3.2 Retrofit

5.4 By End-user Industry

5.4.1 Construction

5.4.2 Automotive

5.4.3 Marine

5.4.4 Design

5.4.5 Other End-user Industry

5.5 By Geography

5.5.1 Asia-Pacific

5.5.1.1 China

5.5.1.2 India

5.5.1.3 Japan

5.5.1.4 South Korea

5.5.1.5 Rest of Asia-Pacific

5.5.2 North America

5.5.2.1 United States

5.5.2.2 Canada

5.5.2.3 Mexico

5.5.3 Europe

5.5.3.1 Germany

5.5.3.2 United Kingdom

5.5.3.3 Italy

5.5.3.4 Spain

5.5.3.5 France

5.5.3.6 Rest of Europe

5.5.4 South America

5.5.4.1 Brazil

5.5.4.2 Argentina

5.5.4.3 Rest of South America

5.5.5 Middle East and Africa

5.5.5.1 Saudi Arabia

5.5.5.2 South Africa

5.5.5.3 United Arab Emirates

5.5.5.4 Rest of Middle East and Africa

6 Competitive Landscape

6.1 Market Concentration

6.2 Strategic Moves

6.3 Market Share Analysis

6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)