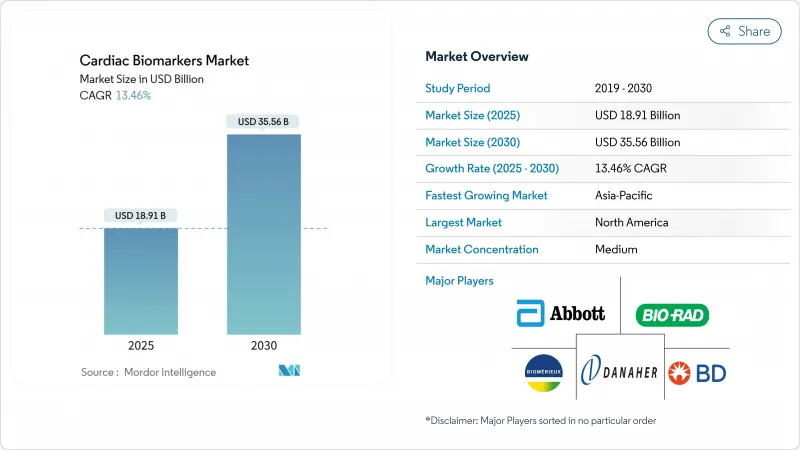

심장 바이오마커 시장 규모는 2025년에 189억 1,000만 달러, 2030년에는 355억 6,000만 달러에 이를 것으로 예측되며, CAGR은 13.46를 나타낼 전망입니다.

의료기관이 급성 관상동맥 질환의 조기 제외 전략을 추구하는 가운데, 고감도 분석, 신속한 포인트 오브 케어 플랫폼, AI 주도의 의사 결정 지원 시스템의 채택이 검사 건수를 가속화하고 있습니다. 민간인의 단백질체학 자금 제공 확대가 탐구 파이프라인을 확대하는 반면, FDA가 2024년에 승인한 최초의 포인트 오브 케어 고감도 심근 트로포닌은 구급부에서의 룰 아웃 시간을 1시간에서 17분으로 단축하고 있습니다. 심혈관 질환을 앓고 있는 미국인 성인은 1억 2,790만 명으로, 이는 인구의 48.6%에 해당합니다. 한편, 아시아태평양에서는 규제의 근대화가 진행되어, 신규 바이오마커나 분산형 검사 플랫폼에 있어서, 상환에 연동한 매력적인 성장이 전망되고 있습니다.

심혈관 질환은 여전히 세계적인 사망률의 최고이며 미국에서는 연간 4,223억 달러의 직접 의료비가 부과되고 있습니다. CMS의 2025년 진료 보상 명세서에서는 ASCVD 리스크 평가의 코딩이 의무화되어 인구통계학적 변수와 검사실에서의 심장 바이오마커를 조합한 근거에 근거한 진단이 요구되게 되어 시설에서의 도입이 가속화되고 있습니다. 밸류 베이스 케어 계약이 확대됨에 따라, 의료 제공업체는 바이오마커에 의해 유도된 개입에 의존하여 측정 가능한 결과의 개선을 문서화하고 재입원 처벌을 피할 수 있습니다.

지멘스 헬스이니어스의 고감도 트로포닌 I 테스트 Atellica IM의 FDA 승인을 통해 지표 이벤트 후 1년까지 예후 위험 계층화가 가능합니다. 실험실 품질의 마이크로플루이딕스 카트리지는 기존의 검사 방법보다 10배 낮은 농도로 트로포닌을 정량하고, 몇 분 안에 결과를 제공하고, 다시설에서의 검증 시험에서 100% 감도를 달성했습니다. 성 특이적 기준 범위는 여성 환자에서 과거의 진단 갭을 메우고 있으며, 통합형 바이오센서는 혈장 분리를 필요로 하지 않는 핑거 스틱에 의한 전혈 검사를 가능하게 합니다.

유럽의 In-Vitro 진단 규제는 현재 광범위한 임상 증거를 의무화하고 있으며 CE 마크의 타임라인을 연장하고 있습니다. 스핀칩 다이아그노스틱스는 2025년 말까지 IVDR에 근거한 신청을 실시해, 2026년에 상시할 예정이며, 장기화의 일도를 추적하고 있습니다. 미국에서는 FDA가 AI를 활용한 진단을 위한 규칙안을 책정하고 알고리즘의 투명성과 다민족 검증 코호트를 요구하고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

트로포닌은 2024년 심장 바이오마커 시장의 59.87%를 차지했으며, 이러한 골드 표준 단백질에 대한 수십 년에 걸친 임상적 신뢰가 입증되었습니다. 이 부문의 수익은 증상 발현으로부터 2시간 이내의 미세한 심근 손상을 검출하는 고감도 형태로의 이동으로부터 유도됩니다. 한편, 허혈 변형 알부민은 CAGR 14.21%로 확대되고 있습니다. 이것은 일시적인 관상 혈관 경련이 트로포닌이 놓치는 가역성 허혈을 포착하는 마커가 필요하다는 인식이 높아지고 있음을 반영합니다.

트로포닌으로 인한 심장 바이오마커 시장 규모는 2025년 113억 달러에 달했습니다. 제조업체는 마이크로 RNA와 염증성 단백질로 분석 메뉴를 늘리고 있지만 임상 도입은 규제 당국의 승인과 지침의 승인에 달려 있습니다. 크레아틴 키나아제는 고감도 트로포닌이 탁월한 특이성을 보이면서 감소하고 있으며, 미오글로빈은 주로 트로포닌이 상승하기 전에 초조기 트리아지에 사용되는 레거시 옵션으로 남아 있습니다.

심근 경색에 대한 응용은 2024년 심장 바이오마커 시장의 부문 수익의 40.23%를 차지했습니다. 병원은 진료 보상 보너스와 직접 연결되는 지표인 door-to-needle 목표를 달성하기 위해 트로포닌 알고리즘에 의존합니다. 한편, 그러나 급성 관상동맥 증후군은 저위험군 환자를 안전하게 퇴원시키고 원격 측정 병상 점유율을 낮추는 0/2시간의 배제 경로에 힘입어 CAGR 14.27%로 상승하고 있습니다.

급성 관상동맥 증후군의 심장 바이오마커 시장 규모는 불필요한 입원 회피에 보상하는 지불자의 인센티브에 의해 지원되는 것으로 추정됩니다. BNP 기반 심부전 관리는 Medicare 병원 재입원 감축 프로그램(Medicare Hospital Readmissions Reduction Program)의 재입원 패널티를 줄이고, ASCVC 코딩 요구사항은 바이오마커 패널을 연간 위험 검토에 통합합니다.

북미는 2024년 심장 바이오마커 시장의 42.21%를 차지하고 윤택한 자금을 가진 지불자, 성숙한 검사 시설 네트워크, 고감도 분석을 검증하는 가이드라인의 무결성 등에 지지되고 있습니다. CMS 코딩의 갱신은 예방적 심장병학 워크플로우에 바이오마커 요건을 추가로 정착시킵니다. 이 지역의 검사 건수는 인구의 고령화에 보조를 맞출 것입니다만, 일괄 지불 모델에 의한 가격 압력이 수익 확대를 억제할 가능성이 높습니다.

유럽은 두 번째 지역이며, 공공 의료 시스템은 신속한 제외 프로토콜을 위해 트로포닌을 채택합니다. In-Vitro Diagnostic Regulation(체외진단제 규제) 시행은 컴플라이언스 비용을 증가시키지만, 임상적으로 검증된 분석에 대한 신뢰를 높여 독일, 프랑스, 영국에서의 채택을 강화합니다. 시장의 기세는 진료 보상의 상한과 하류의 화상 이용을 줄이는 비용 효율적인 멀티플렉스 패널의 균형에 달려 있습니다.

아시아태평양은 가장 급성장하고 있으며 CAGR 14.52%를 기록할 전망입니다. 일본의 400억 달러의 의료기기 부문은 PMDA의 신속 심사 채널에 도움을 받았으며, 이미 고감도 트로포닌과 BNP 검사를 받아들입니다. 중국의 국가 의약국은 2023년에 61개의 혁신적인 진단제를 승인했으며 국내외 바이오마커 공급업체에게 보다 친절한 길을 제시합니다. 심혈관 유병률 증가와 정부 보험의 확대가 2차 병원에서의 분산형 포인트 오브 케어(POC) 솔루션 수요를 촉진하고 있습니다.

중동, 아프리카와 남미는 신흥 캐치업 시장입니다. 걸프 협력 회의 국가는 높은 처리량 분석기를 갖춘 3차 심장 센터에 투자를 추진하고 있으며, 브라질과 멕시코는 조기 심근 경색 진단을 환불하는 국민 모두 보험 제도를 도입하고 있습니다. 운임과 콜드체인의 제약이 계속되는 가운데, 저렴한 가격으로 안정된 상온 시약을 공급할 수 있는 공급자가 점유율을 확대할 것으로 보입니다.

The cardiac biomarkers market size stood at USD 18.91 billion in 2025 and is forecast to reach USD 35.56 billion by 2030, advancing at a 13.46% CAGR.

Adoption of high-sensitivity assays, rapid point-of-care platforms and AI-driven decision support systems is accelerating test volumes as health systems pursue earlier rule-out strategies for acute coronary events. Expansion of public- and private-sector proteomics funding is widening the discovery pipeline, while the FDA's first point-of-care high-sensitivity cardiac troponin approval in 2024 has shortened emergency department rule-out times from one hour to 17 minutes. Demand is further reinforced by the 127.9 million American adults living with cardiovascular disease, equivalent to 48.6% of the population. Meanwhile, Asia-Pacific regulatory modernization is creating attractive reimbursement-linked growth prospects for novel biomarkers and decentralized testing platforms.

Cardiovascular disorders remain the top global mortality driver, costing the United States USD 422.3 billion annually in direct medical expenses . Mandated ASCVD risk assessment coding under the CMS 2025 Physician Fee Schedule now requires evidence-based diagnostics that combine demographic variables with laboratory cardiac biomarkers, intensifying institutional uptake . As value-based care contracts expand, providers rely on biomarker-guided interventions to document measurable outcome gains and avoid readmission penalties.

FDA clearance of Siemens Healthineers' Atellica IM high-sensitivity troponin I test enables prognostic risk stratification for up to one year after an index event . Laboratory-quality microfluidic cartridges now quantify troponin at 10-fold lower concentrations than legacy assays and deliver results in minutes, achieving 100% sensitivity in multi-center validation studies. Sex-specific reference ranges are closing historical diagnostic gaps among female patients, while integrated biosensors allow finger-stick whole-blood testing without plasma separation.

Europe's In-Vitro Diagnostic Regulation now obliges extensive clinical evidence, stretching CE-mark timelines. SpinChip Diagnostics expects to submit under IVDR by end-2025 with launch slated for 2026, illustrating prolonged pathways. In the United States, FDA draft rules for AI-enabled diagnostics require algorithmic transparency plus multi-ethnic validation cohorts, adding compliance costs and delaying commercial roll-out.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Troponins controlled 59.87% of the cardiac biomarkers market in 2024, validating decades of clinical trust in these gold-standard proteins. Segment revenues benefit from the shift to high-sensitivity formats that detect minute myocardial injury within two hours of symptom onset. Conversely, ischemia-modified albumin is expanding at a 14.21% CAGR, reflecting growing recognition that transient coronary vasospasm events demand markers able to capture reversible ischemia that troponin misses.

The cardiac biomarkers market size attributable to troponins reached USD 11.3 billion in 2025. Manufacturers are augmenting assay menus with microRNAs and inflammatory proteins, yet clinical uptake hinges on regulatory clearance and guideline endorsement. Creatine kinase is tapering as high-sensitivity troponins deliver superior specificity, while myoglobin remains a legacy option used primarily for ultra-early triage before troponin rises.

Applications in myocardial infarction generated 40.23% of segment revenue for the cardiac biomarkers market in 2024. Hospitals rely on troponin algorithms to meet door-to-needle targets, a metric directly tied to reimbursement bonuses. Acute coronary syndrome, however, is climbing at a 14.27% CAGR, driven by 0/2-hour rule-out pathways that safely discharge low-risk patients and decrease telemetry bed occupancy.

The cardiac biomarkers market size for acute coronary syndrome is estimated to be underpinned by payer incentives that reward avoidance of unnecessary admissions. Chronic care settings are also expanding use cases; BNP-based management of heart failure reduces readmission penalties under the Medicare Hospital Readmissions Reduction Program, while ASCVD coding requirements integrate biomarker panels into annual risk reviews.

The Cardiac Biomarkers Market is Segmented by Biomarker Type (Troponins, Creatine Kinase, and More), Application (Acute Coronary Syndrome, Myocardial Infarction, and More), Location of Testing (Central Laboratory Testing, and More), End-User (Hospitals, Diagnostic Laboratories, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

North America captured 42.21% of the cardiac biomarkers market in 2024, supported by well-funded payers, mature laboratory networks and guideline alignment that validates high-sensitivity assays. CMS coding updates further entrench biomarker requirements within preventative cardiology workflows. The region's testing volumes will keep pace with population aging, yet pricing pressure from bundled payment models is likely to temper revenue expansion.

Europe follows as the second-largest region, with public healthcare systems anchoring troponin adoption for rapid rule-out protocols. Implementation of the In-Vitro Diagnostic Regulation increases compliance costs but also elevates trust in clinically validated assays, reinforcing adoption across Germany, France and the United Kingdom. Market momentum will hinge on balancing reimbursement ceilings with cost-effective multiplex panels that reduce downstream imaging utilization.

Asia-Pacific is the fastest-growing territory, poised to post a 14.52% CAGR. Japan's USD 40 billion medical device sector is already embracing high-sensitivity troponin and BNP testing, aided by PMDA expedited review channels. China's National Medical Products Administration has approved 61 innovative diagnostics in 2023, signaling a friendlier path for foreign and domestic biomarker vendors. Rising cardiovascular prevalence, coupled with government insurance expansion, drives demand for decentralized point-of-care solutions in secondary hospitals.

Middle East & Africa and South America represent emerging catch-up markets. Gulf Cooperation Council states are investing in tertiary cardiac centers equipped with high-throughput analyzers, while Brazil and Mexico roll out universal health coverage pilots that reimburse early myocardial infarction diagnostics. Suppliers able to deliver affordable, stable ambient-temperature reagents will gain share as freight and cold-chain constraints persist.