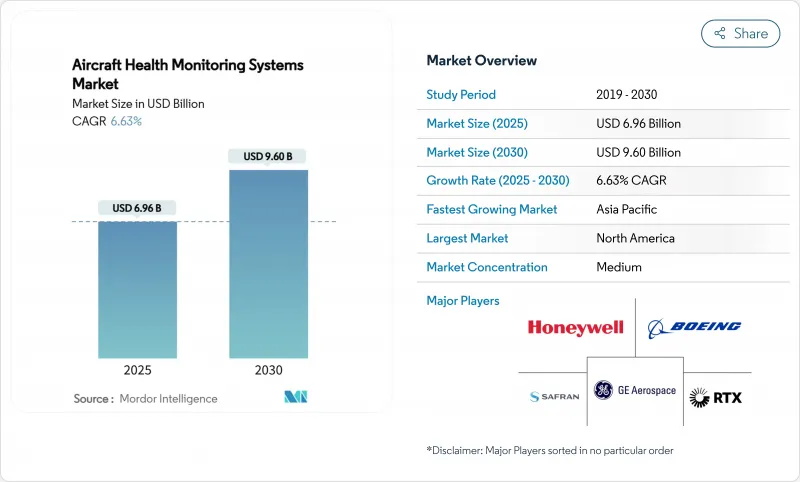

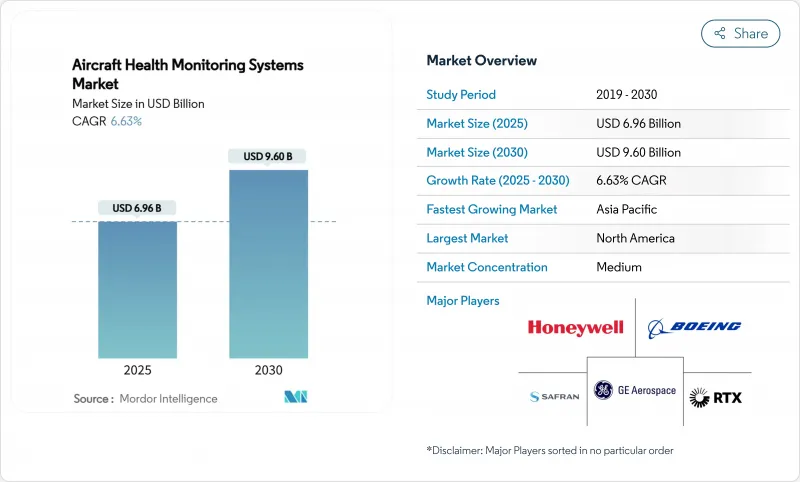

세계의 항공기 헬스 모니터링 시스템 시장 규모는 2025년 69억 6,000만 달러에 달하고, CAGR 6.63%로 추이해 2030년까지 96억 달러에 이를 것으로 예측됩니다.

항공사, MRO, OEM은 예기치 않은 지상 대기 시간을 줄이고 항공기 가동률을 향상시키는 데이터 구동 유지 보수에 투자하고 있음을 반영합니다. 규제기관은 비행 데이터 및 구조적 무결성에 대한 규칙을 강화하여 기내 분석 및 안전한 연결 시스템의 설치를 가속화하고 있습니다. Airbus Skywise와 Boeing Airplane Health Management와 같은 OEM의 디지털 플랫폼은 급속히 확대되어 혼재하는 플릿 전체에 실시간 진단을 제공하게 되었습니다. 아시아태평양 항공기의 성장과 도시형 에어 모빌리티의 프로토타입은 사이버 보안의 격차와 리노베이션 비용이 단기적인 채용을 억제하면서 용도의 범위를 더욱 넓혔습니다.

항공사는 데이터 구동형 예후 예측을 채택한 후 예정되지 않은 유지보수 이벤트가 현저하게 감소했다고 보고하고 있으며, Honeywell은 조기 부품 제거를 회피한 99%의 예측 정밀도를 나타냅니다. 인건비 상승과 엔진 수리 공장 방문률 상승은 특히 신세대 제트기가 비행 당 테라바이트 단위의 센서 데이터를 생성하기 때문에 예지보전이 예산 압박에 대한 전략적 헤지가 되었습니다. 따라서 항공기 헬스 모니터링 시스템 시장은 선택적 분석에서 핵심 운영 인프라로 이동하여 예정된 작업 시간동안 비정상적인 플래그를 지정하는 알고리즘을 통합했습니다. 또한 널리 채택됨으로써 대여주나 금융기관에 있어서 귀중한 자산 이용 지표도 개선되었습니다. 이러한 요인들이 결합되어 항공기 헬스 모니터링 시스템 시스템 시장은 여러 해 동안 강력한 투자 자극을 받고 있습니다.

FAA(미국 연방 항공국)의 개정 FOQA(운항 품질 보증) 서큘러는 미국의 운항 회사에 지속적인 데이터 감시 프로그램의 실시를 의무화했습니다. ICAO와 EASA의 규칙도 이 자세를 반영해 요구사항을 구조부품과 노후화한 항공기의 안전성까지 확대했습니다. 20,000kg MTOW를 넘는 기체에서는 대규모 데이터세트의 저장과 분석이 의무화되어 컴플라이언스는 감시 소프트웨어와 안전한 레코더의 구매자로서 보증되게 되었습니다. FOQA 조사 결과의 징벌적 악용으로부터 항공사를 지키는 보호조치가 자발적인 도입을 촉진하여 항공기 헬스 모니터링 시스템 시장을 더욱 확대했습니다.

2024년 GAO의 검토는 데이터 조작을 허용할 수 있는 패치 미적용 어비오닉스 소프트웨어와 공급망의 약점을 지적했습니다. IBM은 2020년 이후 항공 분야의 사이버 사고가 74% 급증한 것을 기록했습니다. 손상된 센서는 가짜 매개변수를 지상 승무원에게 보내고 예측 대시보드의 신뢰를 손상시키며 검증까지 항공기를 착륙시킬 수 있습니다. 규제 당국은 일관된 규칙을 만들었지만 운영자는 여전히 암호화, 네트워크 세분화 및 지속 모니터링 도구의 통합 비용에 직면하고 있습니다. 이러한 불확실성으로 인해 일부 리노베이션 프로그램이 연기되고 항공기 건전성 모니터링 시스템 및 시스템 시장의 단기 확장이 억제됩니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

항공사는 2024년에 항공기 헬스 모니터링 시스템 시장의 54.25%를 차지했는데, 이는 파견의 신뢰성과 승객의 안전에 대한 직접적인 책임을 반영하고 있습니다. 많은 플래그 캐리어는 착륙 몇 시간 전에 이상을 알리는 OEM 대시보드를 통합하여 부품의 사전 배치와 빠른 턴어라운드를 가능하게 합니다. 항공사용 항공기 헬스 모니터링 시스템 시스템 시장 규모는 디지털 퍼스트 신흥 기업이 완전히 연결된 항공기에서 서비스를 시작함에 따라 꾸준히 확대될 것으로 예측됩니다. 독립 정비, 수리, 오버홀 제공업체는 분석 대시보드를 이용해 OEM 패키지에 필적하는 부가가치 계약을 제공하여 CAGR 전망 7.54%로 활황을 보였습니다. Lufthansa Technik의 AI 기반 검사 플랫폼은 격납고의 작업 시간을 75% 줄입니다. 항공사는 자체 비행 프로파일에 대한 통찰력을 유지하기 위해 노력하고 있으며, MRO는 예측 모델을 개선하기 위해 액세스해야 하기 때문에 데이터 공유 프로토콜은 여전히 어려움을 겪고 있습니다. 그 결과, 상호 접근을 보장하는 파트너십이 항공기 헬스 모니터링 시스템 시장 전체의 조달 규범을 재구성하고 있습니다.

병행하여 임대 회사는 잔여 추적을 지원하는 표준화된 데이터 형식을 요구하고 항공사를 공통 인터페이스로 안내했습니다. 저가 항공사는 벤더 인클로저를 피하기 위해 비독점 소프트웨어를 채택하여 개방형 아키텍처 경쟁을 자극했습니다. 주요 네트워크 항공사의 규모의 이점은 센서 일괄 조달 계약을 계속 지원합니다. 그러나 지역 항공사는 구독 기반 클라우드 분석을 활용하여 항공기 헬스 모니터링 시스템 시장에 진입하는 경로가 넓어지고 있습니다.

항공 추진 시스템은 2024년 세계 매출의 42.30%를 차지했으며 비행 안전성과 비용에서 엔진 상태 모니터링의 중요성을 돋보이게 합니다. 높은 바이패스 터보 팬의 유지보수 비용은 정교한 진동과 성능 분석을 정당화하기 위해 엔진 OEM은 항공기 헬스 모니터링 시스템 및 시스템 업계의 초기 유력자가 되었습니다. 한편, 항공기 구조는 광섬유 스트레인 센서와 임베디드 브래그 격자의 경량화와 저가격화에 따라 CAGR 7.10%로 진보될 것으로 예측됩니다. 복합재 광폭동체를 운항하는 항공사는 숨겨진 갈라짐에 대한 실시간 통찰을 요구하고 있으며 구조 건전성 대시보드에 대한 수요를 높이고 있습니다.

규제 당국이 일부 수동 검사 대신 가상 검사 기록을 수락하게 되면 항공기 헬스 모니터링 시스템 시장 점유율은 구조적 응용에서 더욱 확대될 수 있습니다. 시뮬레이션된 하중 맵에 실시간 스트레인 데이터를 중첩하는 디지털 트윈 플랫폼은 엔지니어링의 변경 주기를 단축하고 OEM에 새로운 서비스 수익을 제공합니다. 한편, 항공기, 환경제어, 보조동력장치는 기체의 성능보증조항을 충족하기 위해 감시를 확대하였습니다. 다중 시스템 분석을 단일 조종석 뷰로 통합하는 시장 진출기업은 항공기 헬스 모니터링 시스템 시장에서 더 많은 점유율을 얻게 됩니다.

북미는 FAA의 의무화, 성숙한 MRO 인프라, 조기 디지털 서비스 도입이 수렴해 2024년 항공기 헬스 모니터링 시스템 시장의 40.6%를 차지하며 주요 수익의 중심이었습니다. 미국 항공사는 기존의 빠른 액세스 레코더를 새로운 안전 의무에 따라 25시간 버전으로 교체하기 시작하여 꾸준한 업그레이드 사이클을 추진했습니다. 캐나다 항공사도 마찬가지로 겨울철 신뢰성을 높이기 위해 엔진헬스키트를 채용하여 지역 수요의 회복력을 유지했습니다. 이 지역의 항공기 헬스 모니터링 시스템 시장 규모는 엄격한 사이버 컴플라이언스 요구 사항 중 한 자릿수 중반의 성장을 유지할 것으로 예측됩니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠르게 상승해 7.25%가 될 것으로 예측됩니다. 중국, 인도, 인도네시아, 태국의 국내 네트워크는 일정 회복에서 최적화로 전환하고 예측 대시보드에 따라 가동률이 높은 협폭동체를 관리합니다. A320neo와 B737-8의 새로운 장비를 도입하는 항공사는 공장 설치형 진단을 취득해 항공기 헬스 모니터링 시스템 시장을 확대했습니다. 각국 정부는 클라우드 애널리틱스를 활용하여 타사 비즈니스를 획득하고 지역 자급 자족을 강화하는 자국의 MRO 능력을 촉진했습니다.

유럽에서는 EASA가 주도한 안전관리시스템 개혁에 의해 노후화된 기체의 구조건전성 평가가 의무화되고 있는 가운데 견조한 교환 수요가 발생했습니다. Lufthansa Technik, Air France-KLM 및 다수의 저가 항공사들은 모니터링 데이터를 활용하여 부품 풀링을 개선하고 탄소 가격 압력 하에서 이익 회복력을 향상시켰습니다. 이 지역의 디지털 트윈 리서치 컨소시엄은 EU 기금을 확보하고 분석 정확도를 높이고 항공기 헬스 모니터링 시스템 시장이 보다 광범위한 항공우주 혁신 목표의 전략적 요소가 되도록 했습니다.

The aircraft health monitoring systems market size stood at USD 6.96 billion in 2025 and is projected to reach USD 9.60 billion by 2030, advancing at a 6.63% CAGR.

The upward trajectory reflects airline, MRO, and OEM investments in data-driven maintenance that cut unscheduled ground time and improve fleet availability. Regulatory bodies have tightened flight-data and structural-integrity rules, accelerating the installation of onboard analytics and secure connectivity systems. OEM digital platforms such as Airbus Skywise and Boeing Airplane Health Management scaled rapidly, providing real-time diagnostics across mixed fleets. Asia-Pacific fleet growth and urban-air-mobility prototypes further widened the application scope, while cybersecurity gaps and retrofit costs tempered near-term adoption.

Airlines reported notable cuts in unscheduled maintenance events after adopting data-driven prognostics, with Honeywell indicating 99% prediction accuracy that avoided premature part removals. Rising labor costs and higher engine shop-visit rates made predictive maintenance a strategic hedge against budget pressure, especially as new-generation jets produce terabytes of sensor data per flight. Therefore, the aircraft health monitoring systems market transitioned from optional analytics to core operational infrastructure, embedding algorithms that flag anomalies during scheduled turnarounds. Wider adoption also improved asset-utilization metrics valuable to lessors and financiers. Collectively, these factors underpin a strong, multi-year stimulus for investment across the aircraft health monitoring systems market.

The FAA's revised Flight Operational Quality Assurance circular compelled US operators to institute continuous data-monitoring programs. ICAO and EASA rules mirrored this stance, extending requirements to structural components and aging-aircraft safety. Operators above 20,000 kg MTOW must now archive and analyze large data sets, turning compliance into a guaranteed buyer pool for monitoring software and secure recorders. Protection measures that shield airlines from punitive misuse of FOQA findings fostered voluntary uptake, further enlarging the aircraft health monitoring systems market.

A 2024 GAO review pinpointed unpatched avionics software and supply-chain weaknesses that could permit data manipulation. IBM recorded a 74% jump in aviation-sector cyber incidents since 2020. A compromised sensor may feed spurious parameters to ground crews, undermining trust in predictive dashboards and potentially grounding aircraft until verification. Regulators drafted cohesive rules, yet operators still face integration costs for encryption, network segmentation, and continuous-monitoring tools. These uncertainties have postponed some retrofit programs and curbed near-term expansion of the aircraft health monitoring systems market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Airlines held 54.25% of the aircraft health monitoring systems market in 2024, reflecting their direct accountability for dispatch reliability and passenger safety. Many flag carriers embedded OEM dashboards that flag anomalies hours before landing, allowing part pre-positioning and faster turnarounds. The aircraft health monitoring systems market size for airlines is expected to progress steadily as digital-first start-ups enter service with fully connected fleets. Independent maintenance, repair, and overhaul providers posted a brisk 7.54% CAGR outlook, using analytics dashboards to deliver value-added contracts that rival OEM packages. Their growth has been propelled by deals such as Lufthansa Technik's AI-based inspection platform that cuts hangar time by 75%. Data-sharing protocols remain a sticking point because airlines aim to preserve proprietary flight-profile insights while MROs need access to refine predictive models. Consequently, partnerships that guarantee reciprocal access reshape procurement norms across the Aircraft Health Monitoring market.

In parallel, leasing companies demanded standardized data formats that support residual-value tracking, nudging airlines toward common interfaces. Low-cost carriers embraced non-proprietary software to sidestep vendor lock-in, stimulating open-architecture competition. The scale advantages of major network airlines continue to underpin bulk sensor-procurement agreements. Yet, regional players now tap cloud analytics on a subscription basis, widening entry pathways into the aircraft health monitoring systems market.

Aero-propulsion systems generated 42.30% of global revenue in 2024, underscoring the centrality of engine condition monitoring to flight safety and cost. High-bypass turbofan maintenance bills justify sophisticated vibration and performance analytics, making engine OEMs early movers in the aircraft health monitoring systems industry. Aircraft structures, however, are projected to advance at a 7.10% CAGR as fiber-optic strain sensors and embedded Bragg gratings become lighter and cheaper. Airlines that operate composite-fuselage wide-bodies seek real-time insight into hidden delamination, elevating demand for structural-health dashboards.

The aircraft health monitoring systems market share of structural applications could widen further once regulators accept virtual inspection records in lieu of some manual checks. Digital twin platforms that overlay live strain data onto simulated load maps have shortened engineering-change cycles, opening new service revenues for OEMs. Meanwhile, avionics, environmental control, and auxiliary power units expanded monitoring to satisfy airframers' performance-guarantee clauses. Market participants that blend multi-system analytics into a single cockpit view stand to capture incremental share within the aircraft health monitoring systems market.

The Aircraft Health Monitoring Systems Market Report is Segmented by End User (OEMs, Airlines, and MRO), Subsystem (Engines, and More), Component (Hardware, Software, and Services), Fit (Line-Fit and Retrofit), Transmission Mode (Onboard and Ground-Based), Aircraft Type (Fixed-Wing, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America remained the principal revenue center with 40.6% of the aircraft health monitoring systems market in 2024 as FAA mandates, mature MRO infrastructure, and early digital-service adoption converged. US carriers began replacing legacy quick-access recorders with 25-hour versions that align with new safety mandates, driving a steady upgrade cycle. Canadian operators similarly adopted engine-health kits for winter reliability, keeping regional demand resilient. The aircraft health monitoring systems market size within the region is forecast to retain mid-single-digit growth amid strict cyber-compliance requirements.

Asia-Pacific is projected to post the fastest 7.25% CAGR through 2030. Domestic networks in China, India, Indonesia, and Thailand moved from schedule recovery to optimization, relying on predictive dashboards to manage high-utilization narrow-body fleets. Airlines deploying new A320neo and B737-8 aircraft obtained factory-installed diagnostics, expanding the Aircraft Health Monitoring market. Governments promoted indigenous MRO capability, which leveraged cloud analytics to win third-party business, reinforcing regional self-sufficiency.

Europe delivered steady replacement demand amid EASA-driven safety-management-system reforms that compel structural-health assessments on aging airframes. Lufthansa Technik, Air France-KLM, and multiple low-cost carriers used monitoring data to refine parts pooling, improving profit resilience under carbon-pricing pressure. The region's digital-twin research consortia attracted EU funding, enhancing analytic sophistication and ensuring that the aircraft health monitoring systems market remains a strategic component of broader aerospace innovation goals.