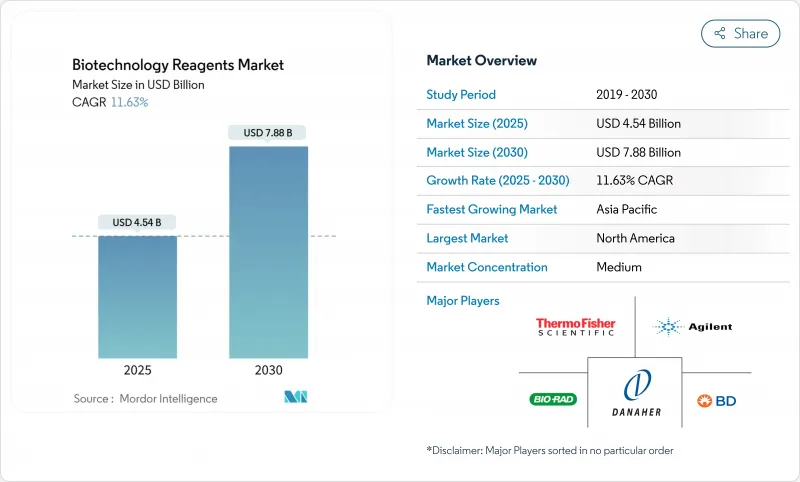

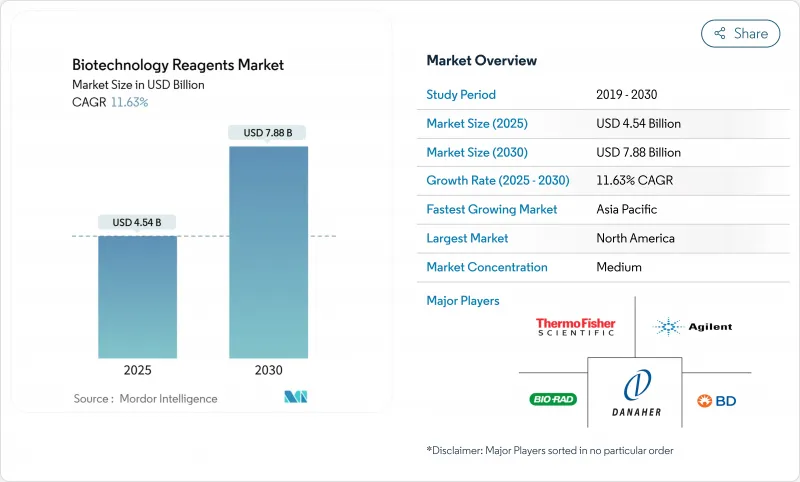

세계의 바이오테크놀러지 시약 시장 규모는 2025년 478억 4,000만 달러로 추정되며, 예측기간 중(2025-2030년) CAGR 6.95%로 확대되어, 2030년에는 669억 3,000만 달러에 달할 것으로 예측됩니다.

AI를 활용한 신약개발에 대한 투자 강화, 바이오 제조 능력 향상, 싱글 셀 분석의 급속한 보급으로 고성능 시약의 대응 가능한 수요가 확대됩니다. 소모품과 데이터 분석 플랫폼을 통합하는 다국적 기업의 합병은 엔드 투 엔드 솔루션 도입을 가속화하고 아시아에서는 정부 우대 조치가 GMP 등급 입력의 현지 생산을 지원합니다. 실험실의 디지털화가 진행됨에 따라, 특히 종양학 및 재생 의료 파이프라인에서 최적화된 자동화 대응 시약 키트 수요가 더욱 높아집니다. 한편, 세계 품질 기준의 엄격화로 제품 검증 사이클이 장기화되고 있으며, 중소 공급업체는 기존 기업과의 제휴를 촉구하고 있습니다.

정밀 발효와 합성 생물학의 신흥 기업에 대한 벤처 자금이 급증하고, 세포 및 유전자 치료 워크플로우에서 고급 시약에 의존하는 새로운 플랫폼에 20억 달러가 투입되었습니다. 각각의 생물학적 제제 후보에는 맞춤형 분석용 소모품이 필요하며, 이는 세계 바이오프로세스 기술 시장에서 지속적인 수요의 원동력이 되고 있습니다. 반면, 플랫폼 기반 탐색 모델에서 실험실은 여러 대상에 해당하는 시약 시스템을 표준화해야 합니다. 결과적으로 조달 전략은 검증된 성능 데이터를 갖춘 모듈식 AI 지원 키트를 제공하는 공급업체가 점점 더 지지를 받고 있습니다.

성체 줄기세포 프로토콜이 주류가 되어 표현형을 유지하는 분리 및 확대 시약의 기술 혁신이 촉진되고 있습니다. 아시아태평양 정부는 Aurora Biosynthetics의 2억 호주 달러(1억 2,940만 미국 달러) 공장과 같은 대규모 GMP 시설에 공동 출자하고 있으며, 준수 소모품에 대한 지역 수요를 뒷받침하고 있습니다. 개별화된 재생 절차가 보급됨에 따라 공급업체는 소량 생산으로 환자에게 맞게 처리할 수 있는 유연한 제형을 제공해야 합니다.

FDA와 EMA의 기준 검증에 대한 괴리로 인해 공급업체는 중복 테스트를 거쳐 제품 출시에 6-12개월이 소요되며 개발 비용은 최대 30% 상승합니다. 각 생산 기지에서 ISO 13485 인증을 취득하는 것은 중소기업에게 부담이 됩니다. 한편, Quality-by-Design의 문서화는 라이프사이클 전체를 커버하게 되어, 컴플라이언스 비용을 흡수할 수 있는 대규모로 수직 통합된 기업에 수요를 밀어 올리고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

생명과학 시약은 2024년 바이오테크놀러지 시약 시장 점유율의 55.62%를 차지했습니다. PCR 기반 진단과 차세대 시퀀싱에서의 강력한 이용은 이 부문의 우위를 유지하고 COVID 시대의 분자 인프라에 대한 지속적인 투자가 기준 수요를 지원합니다. 분석 시약은 규모가 작은 것으로, CAGR 9.29%로 바이오테크놀러지 시약 시장 전체의 성장을 상회하고, 깊은 특성 분석에 대한 규제의 중시와 질량 분석 주도의 단백질체학의 보급으로부터 혜택을 받습니다. 시료 전처리와 분석 시약을 통합한 새로운 하이브리드 키트는 높은 처리량 실험실에서 평가되는 워크플로의 간소화를 약속합니다.

2세대 크로마토그래피 버퍼와 단일 사용 여과 시약은 지속적인 바이오프로세스를 가능하게 하며, 전기영동 소모품은 무세포 시스템의 분리능을 최적화합니다. 공급업체는 경상 분석 수익을 얻기 위해 시약에 소프트웨어 라이선스를 번들하는 경향이 강해지고 습식 실험실과 디지털 제품 간의 수렴을 제안합니다.

북미는 확립된 바이오의약품 클러스터, 풍부한 벤처캐피탈, 지원적인 규제환경을 배경으로 2024년 매출의 39.24%를 차지했습니다. 첨단 바이오 매뉴팩처링을 추진하는 연방 정부 프로그램은 GMP 검증된 시약에 대한 수요를 견조하게 추진하고 있습니다. 유럽에서는 지속가능성에 대한 의무가 지속되고 있어 그린 케미컬 제제와 재활용 가능한 포장에 대한 관심이 높아지고 있으며 공급업체는 제품의 라이프사이클 평가를 검토할 필요가 있습니다.

2030년까지 CAGR은 9.64%가 될 것으로 예상되며, 아시아태평양이 세계적인 확대의 최상위에 설 것으로 예상됩니다. 중국의 Circular No.53은 심사 기간을 단축하고 데이터 보호 창구를 확대하고 지역 혁신과 인바운드 파트너십을 촉진했습니다. 2030년까지 바이오테크놀러지 경제를 3배로 늘리는 일본의 목표는 임상 등급 시약의 국내 수요를 뒷받침합니다. 현지 공급업체는 정부 보조금을 활용하여 능력 격차를 메우고 있지만 국제 QC 기준 준수는 여전히 장애물입니다.

중동, 아프리카, 남미 시장은 한 자리 대 중반의 성장을 기록하고 있습니다. 다국간 보건기관이 후원하는 기술이전협정은 현지 시약 충전 및 마무리 작업을 촉진하여 수입 의존도를 저하시킵니다. 그러나 제한된 콜드체인 인프라와 변동하는 통화 가치가 프리미엄 제품의 채택을 억제하고 있기 때문에 공급업체는 지역 구매력에 맞는 모듈식 비용 계층 시약 라인을 제공하는 인센티브가 되었습니다.

The Biotechnology Reagents Market size is estimated at USD 47.84 billion in 2025, and is expected to reach USD 66.93 billion by 2030, at a CAGR of 6.95% during the forecast period (2025-2030).

Intensifying investment in AI-enabled drug discovery, growing biomanufacturing capacity, and rapid adoption of single-cell analytics enlarge the addressable demand for high-performance reagents. Multinational mergers that integrate consumables with data-analysis platforms accelerate end-to-end solution uptake, while government incentives in Asia support local production of GMP-grade inputs. Ongoing digitalisation of laboratories further boosts demand for pre-optimised, automation-ready reagent kits, particularly in oncology and regenerative-medicine pipelines. Meanwhile, stricter global quality standards lengthen product-validation cycles, pressuring smaller suppliers to partner with established players.

Venture funding in precision fermentation and synthetic biology startups surged, channeling USD 2 billion into new platforms that rely on premium-grade reagents for cell-and gene-therapy workflows. Each biologic candidate requires bespoke analytical consumables, driving recurring demand in the global bioprocess technology market. Fragmented demand lets specialist suppliers command premium pricing, while platform-based discovery models push labs to standardise reagent systems compatible with multiple targets. Consequently, procurement strategies increasingly favour vendors that offer modular, AI-ready kits with validated performance data.

Adult stem-cell protocols dominate, prompting innovation in isolation and expansion reagents that preserve phenotype. APAC governments co-fund large-scale GMP facilities, such as Aurora Biosynthetics' AUD200 million (USD 129.4 million) plant, boosting regional demand for compliant consumables. As personalised regenerative procedures proliferate, suppliers must deliver flexible formulations capable of small-batch, patient-specific processing.

FDA and EMA divergence on reference-standard validation forces suppliers to duplicate studies, adding 6-12 months to product launches and raising development costs by up to 30%. Achieving ISO 13485 certification for each production site strains smaller firms, while Quality-by-Design documentation now covers entire life-cycles, pushing demand toward larger, vertically integrated players able to absorb compliance costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Life-Science Reagents captured 55.62% of biotechnology reagents market share in 2024. Strong utilisation in PCR-based diagnostics and next-generation sequencing keeps the segment ahead, while continuing investment in COVID-era molecular infrastructure supports baseline demand. Analytical Reagents, though smaller, are set to surpass overall biotechnology reagents market growth with a 9.29% CAGR, benefitting from regulatory emphasis on deep characterisation and the proliferation of mass-spectrometry-driven proteomics. Emerging hybrid kits that integrate sample prep with assay reagents promise workflow simplification valued by high-throughput labs.

Second-generation chromatography buffers and single-use filtration reagents enable continuous bioprocessing, while electrophoresis consumables optimise resolution for cell-free systems. Suppliers increasingly bundle software licences with reagents to capture recurring analytics revenue, signalling convergence between wet-lab and digital offerings.

The Biotechnology Reagents Market Report Segments the Industry Into by Reagent Type (Life-Science Reagents [PCR, and More], Analytical Reagents [Chromatography, and More]), Application (Protein Synthesis & Purification, and More), End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America anchored 39.24% of 2024 revenues on the back of entrenched biopharmaceutical clusters, deep venture capital pools, and a supportive regulatory climate. Federal programmes promoting advanced biomanufacturing generate steady requisitions for GMP-validated reagents. In Europe, continued adherence to sustainability mandates propels interest in green-chemistry formulations and recyclable packaging, prompting suppliers to revamp product life-cycle assessments.

Asia-Pacific tops global expansion, expected to post 9.64% CAGR through 2030. China's Circular No. 53 has trimmed review timelines and expanded data-protection windows, catalysing local innovation and inbound partnerships. Japan's goal of tripling its biotech economy by 2030 underwrites domestic demand for clinical-grade reagents, while Southeast Asia's CDMO rise creates fresh outlets for single-use consumables. Local suppliers leverage government subsidies to close capability gaps, although adherence to international QC standards remains a hurdle.

Markets in the Middle East, Africa, and South America record mid-single-digit growth. Technology-transfer agreements sponsored by multilateral health agencies facilitate local reagent fill-finish operations, reducing import reliance. However, limited cold-chain infrastructure and fluctuating currency valuations temper the adoption of premium products, incentivising suppliers to offer modular, cost-tiered reagent lines tailored to regional purchasing power.