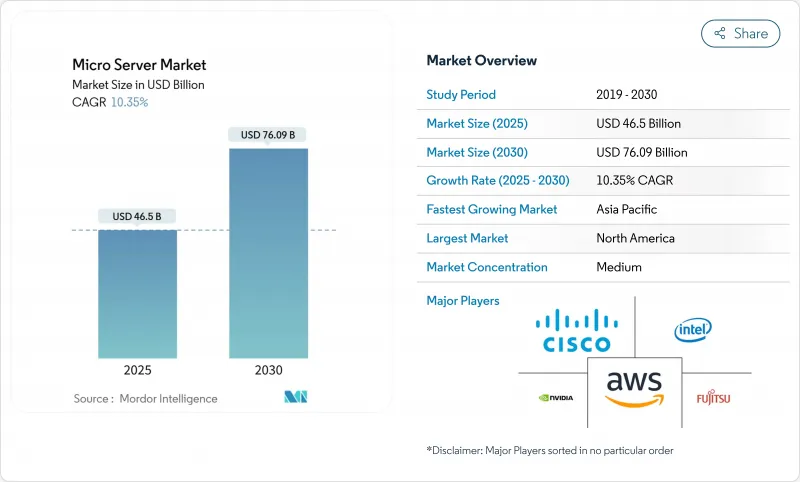

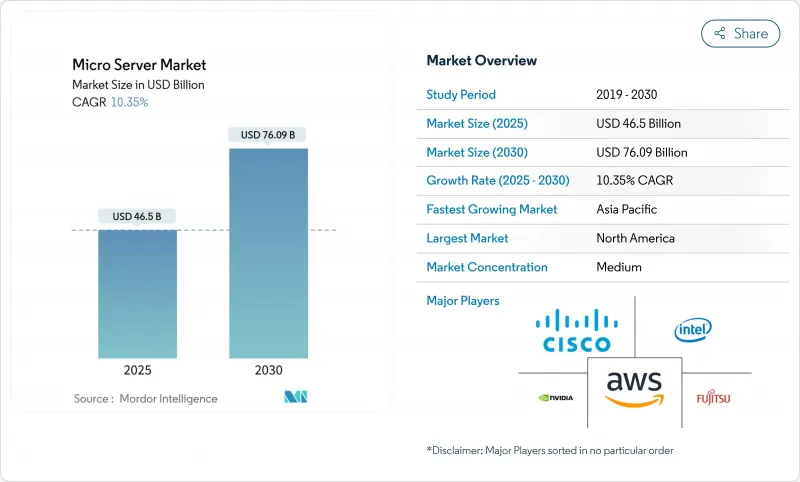

마이크로 서버 시장 규모는 2025년에 465억 달러, 2030년에는 760억 9,000만 달러에 이를 것으로 예상되며, 이 기간의 CAGR은 10.4%를 나타낼 전망입니다.

데이터센터 설치 면적의 급속한 고밀도화, AI 추론을 지원하는 저소비 전력 컴퓨트 노드 수요, 에너지 효율의 의무화가 주요 순풍이 되고 있습니다. 공급업체 간의 경쟁은 기존 x86 서버 제조업체, 맞춤형 실리콘을 설계하는 클라우드 제공업체, 와트당 성능 향상을 약속하는 ARM 기반의 신규 진출기업 등에 이르고 있습니다. 조달 예산은 계속해서 하드웨어가 대부분을 차지하지만, 기업이 이종 아키텍처에 임하는 가운데 매니지드 서비스가 급성장하고 있습니다. 지역별로는 북미가 하이퍼스케일 투자로 주도하고 있는 반면, 아시아태평양은 중소기업의 디지털화와 5G 전개로 가장 빠르게 확대되고 있습니다.

하이퍼스케일 사업자는 도입 사이클을 단축하고 와트 퍼 컴퓨트 지표를 향상시키는 공장 통합형 고밀도 스레즈를 표준화하고 있습니다. 인프라 메이슨은 몇 기가와트 규모의 캠퍼스형 '클린 에너지 파크'를 제안하고, 랜시엄은 6GW에 달할 수 있는 사이트를 계획하고 있습니다. 통신사는 메트로 에지 사이트에도 동일한 논리를 적용하고 10ms 이하의 대기 시간 목표를 달성하기 위해 5G 노드에 인접한 마이크로 데이터센터를 설치합니다. 따라서 하이퍼스케일의 경제성과 에지의 근접성의 융합으로 마이크로 서버 시장은 밀도, 비용, 전력 효율의 균형을 맞추는데 바람직한 플랫폼으로 확고한 지위를 구축하고 있습니다.

추론 지향 트래픽은 현재 많은 프로덕션 AI 스택을 지배하고 있으며 서버 설계는 원시 CPU 주파수보다 메모리 대역폭과 가속기 통합으로 향하고 있습니다. Amazon Web Services의 Graviton 4는 Arm Neoverse V2에 구축되어 96코어와 12채널 DDR5-5600을 통합하여 에너지 소비를 줄이면서 추론 대기 시간을 예산 내로 억제합니다. Dell 4U PowerEdge XE9680L은 8개의 NVIDIA Blackwell GPU를 직접 액체 냉각으로 패키징하여 표준 랙 내에서 와트당 높은 성능을 제공합니다. 이러한 청사진은 아키텍처의 축을 강조합니다. 마이크로 서버는 단순히 계산 속도를 높이는 것이 아니라 데이터를 효율적으로 이동시키고 추론 워크로드를 클러스터에 분산시키는 가속기를 통합해야 합니다.

Open Compute Project의 M-XIO와 Modular Hardware System의 사양에도 불구하고 전원 핀, PCIe 레인 및 대역 외 인터페이스에 편차가 있기 때문에 벤더 간 슬레드(sled) 교체가 복잡해지고 있습니다. 따라서 기업은 여러 예비 재고와 맞춤 주문 관리 스택을 가지고 있으며 규모의 경제를 희박하게 만듭니다. 플러그 앤 플레이의 상호 운용성의 부족은 공통 백플레인에 탑재 할 수있는 타사 가속기 모듈의 생성을 지연시킵니다. 상호 호환성을 사전에 입증하거나 종합적인 지원 계약을 번들로 제공하는 공급업체는 진정한 표준화가 나타날 때까지 유리한 위치에 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

컴포넌트별 마이크로 서버 시장 규모는 2024년 하드웨어에서 305억 5,000만 달러(공유 65.6%)에 이르렀으며, 하이퍼스케일 및 엣지 시설에서 자본 집약적인 리프레시 사이클이 확인되었습니다. 서비스는 159억 7,000만 달러로 계속되었지만, 2030년까지 연평균 복합 성장률(CAGR) 11.9%로 확대될 것으로 예상되며, 이는 아키텍처의 이질성을 조정하기 위한 관리 인프라에 대한 기업의 의존을 반영합니다. 이 지출의 대부분은 AI 랙 설계, 액체 냉각 리노베이션, 원격 플릿 오케스트레이션에 쏟아집니다.

하드웨어 수익은 Arm, x86 및 맞춤형 ASIC을 통합한 고밀도 1U 트윈 노드 슬리드와 4U GPU 트레이의 지속적인 출하에 의해 지원됩니다. Dell은 2025년 1분기에 AI에 최적화된 서버를 29억 달러 출하했는데, 이는 하드웨어 사이클의 강도를 보여주는 단일 공급업체의 신호입니다. 서비스 성장은 원격 BIOS 프로비저닝, 컨테이너 오케스트레이션 및 라이프사이클 보안 패치 적용에 대한 수요로 인해 멀티클라우드 팀이 점점 외주를 늘리고 있습니다. 컨설팅, 펌웨어 커스터마이제이션 및 24시간 지원을 마이크로 서버 플릿에 제공하는 공급업체는 끈질긴 연금 흐름을 얻고 자본 예산의 변동을 완화하고 있습니다.

1U에서 4U까지의 랙 유닛은 기존 통로 레이아웃과 표준화된 급전에 적합하기 때문에 2024년 마이크로 서버 시장 점유율의 60.1%를 차지했습니다. 그러나 견고한 에지 박스 CAGR은 11.6%를 나타내고, 통신 사업자나 산업 사업자가 제약이 많은 거점에 컴퓨팅을 도입함에 따라 레거시 섀시를 크게 웃도는 기세입니다. 많은 디자인은 전면 서비스 가능한 침지 플레이트 냉각과 -48V DC 입력을 채택하고 옥외 5G 캐비닛과 일치시킵니다.

OEM은 네트워킹, AI 가속기 및 배터리 백업을 슈박스 스케일 인클로저에 사전 통합함으로써 모듈 박스의 마이크로 서버 시장 규모를 확대합니다. Vicor가 지원하는 레퍼런스 디자인은 일반적인 랙 노드에 비해 추론 동작당 에너지 사용량이 35% 적고 그리드 용량이 부족한 곳에서는 매력적임을 보여줍니다. 한편, 멀티노드 마이크로클라우드 솔리드는 3U 프레임에 8개의 싱글 소켓 보드를 탑재하여 유지보수성을 희생하지 않고 랙 밀도를 높이는 것으로 균형을 잡고 있습니다.

북미는 2024년에 174억 4,000만 달러의 매출을 계상해 마이크로 서버 시장의 37.5%를 차지했습니다. 조지아 주 공공 서비스위원회는 현재 부하가 많은 고객에게 송전망 업그레이드 비용을 앞당겨 부담하도록 의무화하고 있으며 데이터센터 사업자를 보다 에너지 효율적인 마이크로 서버 노드로 유도하고 있습니다. AI 가속기의 연방 수출 규제는 미국에서의 조립과 테스트를 더욱 장려하고 현지에서의 가치 유지를 견고하게 만듭니다.

유럽은 에너지 효율과 사이버 내성의 엄격한 법률을 뒷받침하고 있습니다. 에너지 효율 지령의 갱신으로 IT 부하가 100kW를 넘는 데이터센터에서는 연차 보고가 의무화되고, 디지털 오퍼레이션 탄력성법에서는 금융기업에 업타임과 보안의 강화가 의무화되고 있습니다. 이러한 규칙은 킬로와트당 계산 능력이 높은 마이크로 서버에 대한 수요를 높여 사업자는 새로운 송전망을 연결하지 않고 전력 사용 효율 목표를 달성할 수 있게 합니다.

아시아태평양은 5G의 고밀도화와 중소기업의 클라우드 도입이 수렴하여 CAGR 11.2%로 예측되는 가장 급성장하고 있는 지역입니다. Compal Electronics와 Kalyani Group은 컴퓨트 밸류 체인의 현지화를 목적으로 한 'Make in India'의 인센티브를 따라 인도에서 서버를 제조하는 양해각서(MOU)를 체결했습니다. ASEAN과 남아시아 전역의 정부는 디지털 서비스의 GDP 기여를 촉진하기 위해 국내 데이터 호스팅을 추진하고 있으며, 습도가 높은 기후와 제한된 전력에 최적화된 지역별 마이크로 서버 설계에 대한 길을 열고 있습니다.

The micro server market size currently stands at USD 46.50 billion in 2025 and is forecast to climb to USD 76.09 billion by 2030, reflecting a 10.4% CAGR over the period.

Rapid densification of data-center footprints, demand for low-power compute nodes to support AI inference, and tightening energy-efficiency mandates are the primary tailwinds. Vendor competition spans established x86 server makers, cloud providers designing custom silicon, and new ARM-based entrants that promise higher performance per watt. Hardware continues to dominate procurement budgets, yet managed services grow quickly as enterprises grapple with heterogeneous architectures. Regionally, North America leads on the back of hyperscale investments, while Asia-Pacific shows the fastest expansion because of SME digitalisation and 5G roll-outs.

Hyperscale operators are standardising factory-integrated, high-density sleds that shorten deployment cycles and improve watt-per-compute metrics. Infrastructure Masons advocates campus-style "clean-energy parks" sized at multi-gigawatt scale, while Lancium plans sites that may reach 6 GW of capacity, illustrating how power availability now guides server architecture choices. Telecommunications companies extend the same logic to metro edge sites, installing micro data centres adjacent to 5G nodes to meet sub-10 millisecond latency targets; ruggedised micro servers allow rapid provisioning without full-scale facilities. Convergence of hyperscale economics with edge proximity therefore cements the micro server market as the preferred platform for balancing density, cost, and power efficiency.

Inference-oriented traffic now dominates many production AI stacks, pushing server design toward memory bandwidth and accelerator integration over raw CPU frequency. Amazon Web Services' Graviton 4, built on Arm Neoverse V2, integrates 96 cores and 12-channel DDR5-5600 to keep inference latency within budget while trimming energy draw. Dell's 4U PowerEdge XE9680L packages eight NVIDIA Blackwell GPUs with direct liquid cooling, delivering high performance per watt inside standard racks. These blueprints underscore an architectural pivot: micro servers must move data efficiently rather than simply compute faster, embedding accelerators that disperse inference workloads across clusters.

Despite the Open Compute Project's M-XIO and Modular Hardware System specifications, variance in power pins, PCIe lanes, and out-of-band interfaces complicates swapping sleds across vendors. Enterprises therefore juggle multiple spares inventories and bespoke management stacks, diluting economies of scale. Lack of plug-and-play interoperability also slows the creation of third-party accelerator modules that could otherwise ride a common backplane. Vendors that pre-certify cross-compatibility or bundle holistic support contracts are better positioned until true standardisation emerges.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The micro server market size by component reached USD 30.55 billion for hardware in 2024, equivalent to 65.6% share, confirming capital-intensive refresh cycles within hyperscale and edge facilities. Services followed at USD 15.97 billion but will expand at 11.9% CAGR through 2030, reflecting enterprise reliance on managed infrastructure to tame architectural heterogeneity. Much of the spend funneled into design-for-AI racks, liquid cooling retrofits, and remote fleet orchestration.

Hardware revenue is anchored by continued shipments of dense 1U twin-node sleds and 4U GPU trays that integrate Arm, x86, and custom ASICs. Dell shipped USD 2.9 billion in AI-optimised servers during 2025 Q1, a single-vendor signal of the hardware cycle's strength. Services growth stems from demand for remote BIOS provisioning, container orchestration, and lifecycle security patching-tasks that multicloud teams increasingly outsource. Vendors that wrap consulting, firmware customisation, and 24-hour support around micro server fleets capture sticky annuity streams, cushioning volatility in capital budgets.

Rack units between 1U and 4U captured 60.1% of micro server market share in 2024, owing to their fit with existing aisle layouts and standardised power feeds. However, rugged edge boxes are on track for an 11.6% CAGR, far outpacing legacy chassis as telecom and industrial players push compute to constrained sites. Many designs adopt front-serviceable soaked-plate cooling and -48 V DC inputs, aligning with outdoor 5G cabinets.

The micro server market size for modular boxes will rise as OEMs pre-integrate networking, AI accelerators, and battery backup into shoebox-scale enclosures. Vicor-backed reference designs show 35% lower energy use per inference operation compared with typical rack nodes, attractive where grid capacity is scarce. Meanwhile, multi-node microcloud sleds strike a balance, fitting eight single-socket boards into a 3U frame to boost rack density without sacrificing serviceability.

The Micro Server Market Report is Segmented by Component (Hardware and Services), Form Factor (Rack, Multi-Node Microcloud, and Modular Rugged Edge Box), Application (Data Centre, Cloud Computing, Media / Content Storage, and More), End-User (Large Enterprises and Small and Medium Enterprises (SMEs)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America generated USD 17.44 billion of revenue in 2024, equal to 37.5% of the micro server market, thanks to heavy hyperscale capex and government preference for defence-grade domestic supply chains. The Georgia Public Service Commission now obliges large-load customers to shoulder upfront grid-upgrade costs, nudging data-centre operators toward more energy-efficient micro server nodes. Federal export controls on AI accelerators further incentivise U.S.-based assembly and testing, solidifying local value retention.

Europe follows, propelled by stringent energy-efficiency and cyber-resilience laws. The updated Energy Efficiency Directive mandates annual reporting for data-centre sites above 100 kW IT load, while the Digital Operational Resilience Act compels financial firms to bolster uptime and security. These rules elevate demand for micro servers that deliver higher compute per kilowatt, aiding operators in meeting power-usage-effectiveness targets without new grid connections.

Asia-Pacific is the fastest-growing territory, forecast at 11.2% CAGR, as 5G densification and SME cloud adoption converge. Compal Electronics and Kalyani Group signed an MoU to manufacture servers in India, aligning with "Make in India" incentives aimed at localising the compute value chain. Governments across ASEAN and South Asia promote domestically hosted data to spur digital services GDP contributions, paving the way for region-specific micro server designs optimised for humid climates and limited utility power.