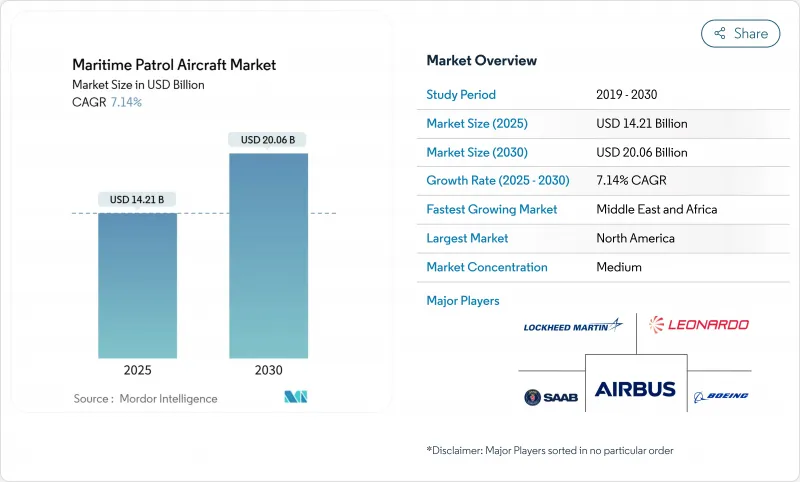

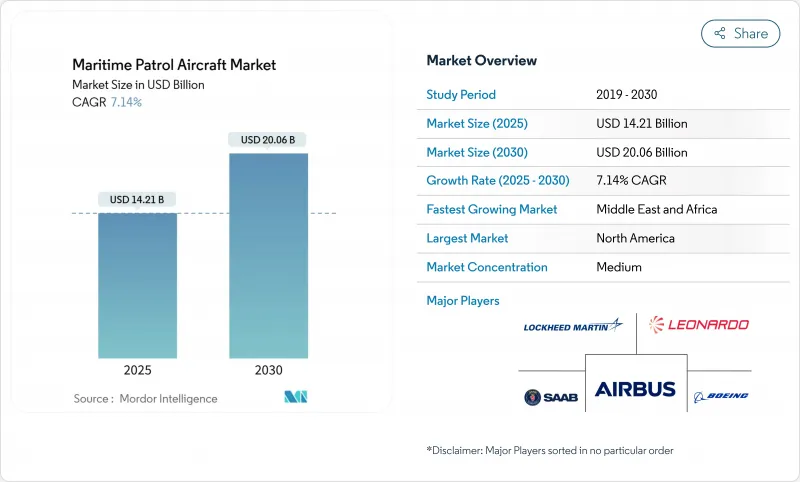

해상 초계기 시장 규모는 2025년에 142억 1,000만 달러에 달하고, CAGR 7.14%를 나타내, 2030년에는 200억 6,000만 달러에 이를 것으로 예측됩니다.

잠수함 활동의 활성화, 블루 이코노미 증가, 유인-무인 팀 편성으로의 변화가 지속적인 수요를 지지하고 있습니다. 냉전 시대 항공기의 함대 대체 사이클은 대규모로 여러 해에 걸친 조달 파이프라인을 생산하고 있으며, 비용 압력은 모듈형 센서 포드와 하이브리드 전기 추진에 대한 관심을 가속화하고 있습니다. 북미는 미국 해군의 P-8A 프로그램과 동맹국의 표준화를 배경으로 리더십을 유지하고 있습니다. 그러나 중동 및 아프리카는 해안 국가들이 새로운 해양 경비 임무에 자금을 제공하고 있기 때문에 급성장을 보여줍니다. 특수 소노부이공급망 병목 현상과 첨단 레이더의 수출 규제 제한은 10년간의 경쟁 역학을 바꿀 수 있는 구조적 제약으로 남아 있습니다.

중국과 러시아의 새로운 잠수함 증강으로 해군은 11시간 이상의 내구성, 멀티 스태틱 소나 처리, 확장 센서 퓨전을 갖춘 플랫폼을 우선시할 수밖에 없었습니다. 미국 해군은 이러한 요구 사항을 충족하기 위해 2025년 P-8A 증분 3 블록 2 업그레이드를 완료했습니다. 독일이 8기의 P-8A를 발주해 일본이 과거 최고의 7조 9,500억엔(547억 달러)의 방위 예산을 계상한 것은 연안역에서 푸른 지역으로의 ASW로의 변화를 강조하고 있습니다. 광대한 EEZ를 가진 인도 태평양 국가들은 기존 P-3 함대에서 대항할 수 없는 해중 침입을 억제하기 위해서는 지속적인 감시가 필수적이라고 생각합니다.

20개국에 이르는 600대 이상의 오리온기가 퇴역 가까이 되어 함대의 갱신은 해상 항공사상 최대의 근대화의 파도로 자리매김하고 있습니다. 한국은 2025년 P-3 추락 사고 후 P-8A로의 전환을 가속시켰습니다. 프랑스가 소형 팔콘 플랫폼이 아닌 에어버스 A321 MPA를 선택한 것은 페이로드가 풍부하고 멀티미션에 대응할 수 있는 기체를 선호하고 있음을 보여줍니다. 엄청난 방어 예산이 없는 국가들은 능력의 격차를 메우기 위해 보다 저렴한 C295 및 C-130 미션 키트를 채택하고 있습니다.

MQ-4C 등의 프로그램이 70대에서 27대로 감소했기 때문에 단가가 상승하고, 1대당 비용이 4억 달러를 넘어 상승해 고객의 예산을 압박했습니다. 효율중시의 생산시스템을 채용하고 있음에도 불구하고 보잉사는 P-8A의 생산량을 월산 1.5기로 확대하는 한편 비슷한 불경제에 직면하고 있습니다. 랜드 연구소(RAND)의 분석에 따르면 연간 생산량이 10% 증가할 때마다 비행 비용은 약 3% 절감됩니다. 센서 스위트의 복잡화는 이 가격 곡선을 확대하여 국방 지출에 제약이 있는 국가에 어려운 트레이드오프를 만들어 냅니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

2024년 해상 초계기 시장 수익의 75.54%는 유인비행대가 차지하고, P-8A 포세이돈과 일본의 P-1이 그 중심이 되었습니다. 그러나 무인 플랫폼은 CAGR 10.25%를 나타내 성장을 지속하고, AI를 활용한 자율성이 성숙함에 따라 유인의 우위성을 꾸준히 침식해 나갈 것으로 보입니다. 또한 미국 해군이 항공모함에 MQ-28을 탑재하는 데 강한 관심을 보이는 것은 혼성함대에 대한 전략적 헌신을 보여줍니다.

비용 효율성, 승무원의 한계를 넘어서는 내구성, 분쟁지대에서의 위험이 낮음은 무인 항공기의 매력을 지원합니다. 시가디언의 2024년 림팩에서의 데뷔는 소노부이의 디스펜스와 LRASM의 큐잉을 특징으로 하며 UAV가 현재 ASW와 대수면의 코어 태스크를 수행할 수 있음을 증명했습니다. 유인 MPA가 여러 자율 센티넬을 지휘하는 하이브리드 아키텍처는 2030년까지 전력 설계 논의를 지배할 것으로 보입니다.

2024년에는 제트 엔진이 매출액의 85.32%를 차지했지만 DARPA의 XRQ-73과 같은 하이브리드 전기 실증기가 첫 비행을 달성했으며 전기 시스템의 CAGR은 12.45%를 나타낼 전망입니다. 미국 육군 기금을 통한 GE 에어로스페이스 그룹 3UAV용 1-MW 하이브리드 모듈은 마이그레이션 기세를 보여줍니다.

전기 추진은 음향 시그니처를 줄이고 체공 시간을 증가시키고 방위 분야의 탄소 목표에 부합합니다. 하이브리드 전기 추진 실증기의 해상 초계기 시장 규모는 현재 겸손하지만, 민간과 군사의 이중 연구개발 경로로부터 혜택을 받고 있습니다. 터보 샤프트는 수직 상승형 초계기와의 연관성을 유지하고 있지만, 유럽과 북미의 지속적인 전기화 자금 조달은 2028년 이후 광범위한 채택을 시사합니다.

북미는 2024년 해상 초계기 시장 수익의 38.56%를 차지했으며, 미국 해군이 캐나다와 독일을 위해 34억 달러를 던져 구입한 P-8A와 현재 진행 중인 CP-140 오로라의 대체로 지원되었습니다. 캐나다 고유의 생산 능력, 확립된 서브시스템 공급업체, 지속적인 R&D 파이프라인이 이 지역의 리더십을 지키고 있습니다. 캐나다의 참여는 상호 운용성을 뒷받침하고 멕시코 조달 전망은 삼국 간 안보 통합을 반영합니다. 해안 경비대의 부대 설계 2028은 1만 5,000명의 신규 요원과 차세대 ISR 자산을 목표로 하고 있으며, 지속적인 국내 수요를 강화하고 있습니다.

유럽에서는 NATO 함대가 P-3 오리온을 단계적으로 퇴역시키는 동안 견조한 현대화 사이클이 계속되고 있습니다. 2025년 2월에 인도된 독일 최초의 P-8A는 동맹 표준화에서 매우 중요한 이정표가 되었습니다. 프랑스 에어버스 A321 MPA의 결정은 산업 정책이 조달에 미치는 영향을 강조하는 것이며, 스페인의 16대 C295 주문은 지역 작업 공유를 유지하는 것입니다. 유럽의 지속가능성 정책은 MPA의 하이브리드 전기 개념과 지속 가능한 항공 연료 시험에 대한 투자에 박차를 가하고 있습니다.

중동 및 아프리카는 걸프 국가와 아프리카 연안 국가들이 해상 안전 아키텍처를 강화함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 10.54%를 나타내 가장 빠르게 확대되는 지역입니다. UAE는 5대의 GlobalEye 프로그램을 완료하고 1억 9,000만 달러의 지원 계약을 체결했습니다. 나이지리아의 50대 항공기 조달 파이프라인에는 해적 행위와 불법 벙커 위협에 대처하는 순찰 모델이 포함되어 있습니다. 해외 에너지 인프라, 불법 어업 증가, 홍해 안보 긴장이이 지역 전체의 지출을 이끌고 있습니다.

아시아태평양은 역동적이고 다층적인 수요를 보여줍니다. 일본은 기록적인 방위 예산으로 P-1 업그레이드를 강화하고 한국은 2027년까지 P-8A 도입을 진행할 계획입니다. 인도 해군과 해안 경비대를 위한 C-295의 구매는 이중 서비스 취득 모델을 보여줍니다. 2029년까지 62억 7,000만 달러로 급증할 것으로 예상되는 호주 자본 지출은 해양 지역 인식을 우선시하고 있습니다. 광대한 EEZ, 싸움의 끊임없는 바다, 가속 잠수함의 활동은 이 지역의 강한 전망을 지원합니다.

The maritime patrol aircraft market size reached USD 14.21 billion in 2025 and is forecasted to expand at a 7.14% CAGR, achieving USD 20.06 billion by 2030.

Growing submarine activity, rising blue-economy enforcement, and the shift toward manned-unmanned teaming underpin sustained demand. Fleet-replacement cycles for Cold War-era aircraft continue to generate large, multi-year procurement pipelines, while cost pressures are accelerating interest in modular sensor pods and hybrid-electric propulsion. North America maintains leadership on the back of the US Navy's P-8A program and allied standardization. Yet, the Middle East and Africa show the fastest growth as coastal states fund new maritime-security missions. Supply-chain bottlenecks in specialized sonobuoys and export-control limits on advanced radars remain structural constraints that could alter competitive dynamics over the decade.

Renewed submarine build-ups by China and Russia compelled navies to prioritise platforms with 11-plus-hour endurance, multistatic sonar processing, and extended sensor fusion. The US Navy completed P-8A Increment 3 Block 2 upgrades in 2025 to meet these requirements. Germany's order of 8 P-8As and Japan's record JPY 7.95 trillion (USD 54.70 billion) defence budget underline the shift from coastal to blue-water ASW. Indo-Pacific nations with expansive EEZs see persistent surveillance as essential for deterring undersea incursions that legacy P-3 fleets cannot counter.

More than 600 veteran Orion aircraft across 20 countries are nearing retirement, positioning fleet renewal as the largest modernisation wave in maritime aviation history. South Korea accelerated its transition to P-8A after a 2025 P-3 crash, illustrating how safety events compress replacement timelines. France's Airbus A321 MPA choice over a smaller Falcon platform signals a preference for payload-rich, multi-mission airframes. Nations lacking large defence budgets are adopting lower-cost C295 or C-130 mission kits to bridge capability gaps.

Unit prices climbed as programs such as MQ-4C dropped from 70 to 27 aircraft, raising per-aircraft cost beyond USD 400 million and stressing customer budgets. Despite adopting an efficiency-focused production system, Boeing faces similar diseconomies while scaling P-8A output to 1.5 jets per month. RAND analysis shows that each 10% uptick in annual volume can trim about 3% from flyaway cost, underscoring the affordability challenge small-batch buyers endure. Rising complexity in sensor suites magnifies this price curve, creating difficult trade-offs for nations with constrained defence spending.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The manned fleet retained 75.54% share of maritime patrol aircraft market revenue in 2024, anchored by the P-8A Poseidon and Japan's P-1, both suited for complex, crew-intensive missions. However, unmanned platforms post a 10.25% CAGR and will steadily erode manned dominance as AI-enabled autonomy matures. Loyal-wingman trials confirm operational viability, and the US Navy's strong interest in MQ-28 insertion aboard carriers illustrates strategic commitment to mixed fleets.

Cost efficiency, endurance beyond crew limits, and lower risk in contested zones sustain the unmanned appeal. SeaGuardian's 2024 RIMPAC debut featured sonobuoy dispense and LRASM cueing, proving that UAVs can now execute core ASW and anti-surface tasks. Hybrid architectures where a manned MPA orchestrates multiple autonomous sentinels will dominate force-design discussions through 2030.

Jet engines controlled 85.32% of revenue in 2024, yet hybrid-electric demonstrators such as DARPA's XRQ-73 achieved first flight, supporting a 12.45% CAGR for electric systems. GE Aerospace's 1-MW hybrid module for Group 3 UAVs under US Army funding showcases transition momentum.

Electric propulsion reduces acoustic signature, increases loiter time, and aligns with defence-sector carbon goals. The maritime patrol aircraft market size for hybrid-electric demonstrators is modest today, but benefits from dual civilian-military R&D paths. Turboshafts retain relevance for vertical-lift patrol craft, yet sustained electrification funding in Europe and North America hints at wider adoption after 2028.

The Maritime Patrol Aircraft Market Report is Segmented by Platform (Manned and Unmanned), Propulsion System (Jet Engine, and More), Mission Type (Anti-Submarine Warfare, Intelligence, Surveillance and Reconnaissance, Search and Rescue, and More), End User (Naval Forces, Coast Guards and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America commanded 38.56% of the maritime patrol aircraft market revenue in 2024, buoyed by the US Navy's USD 3.4 billion P-8A buy for Canada and Germany and the ongoing CP-140 Aurora replacement. Indigenous production capacity, established subsystem suppliers, and continuous R&D pipelines safeguard the region's leadership. Canada's participation underpins interoperability, while Mexico's prospective procurement reflects trilateral security integration. Coast Guard Force Design 2028, targeting 15,000 new personnel and next-generation ISR assets, reinforces sustained domestic demand.

Europe continues a robust modernisation cycle as NATO fleets phase out P-3 Orions. Germany's first P-8A, delivered in February 2025, marked a pivotal milestone in alliance standardisation. France's Airbus A321 MPA decision underscores the influence of industrial policy on procurement, while Spain's 16-aircraft C295 order sustains regional workshare. European sustainability policies spur investment in hybrid-electric concepts and sustainable aviation fuel trials for MPAs.

The Middle East and Africa are the fastest expanding regions at 10.54% CAGR to 2030 as Gulf states and African littoral nations strengthen maritime-security architectures. UAE completed its 5-aircraft GlobalEye program and signed a USD 190 million support contract ensuring readiness through the decade. Nigeria's 50-aircraft procurement pipeline includes patrol models that address piracy and illegal bunkering threats. Offshore energy infrastructure, rising illegal fishing, and Red Sea security tensions drive spending across the region.

Asia-Pacific demonstrates dynamic, multi-tier demand. Japan's record defence budget funds enhanced P-1 upgrades, while South Korea advances P-8A induction by 2027. India's C-295 buy for the navy and coast-guard roles exemplifies dual-service acquisition models. Australia's capital expenditure surge to AUD 6.27 billion by 2029 prioritises maritime domain awareness. Collectively, vast EEZs, contested sea lanes, and accelerating submarine activity underpin a strong regional outlook.