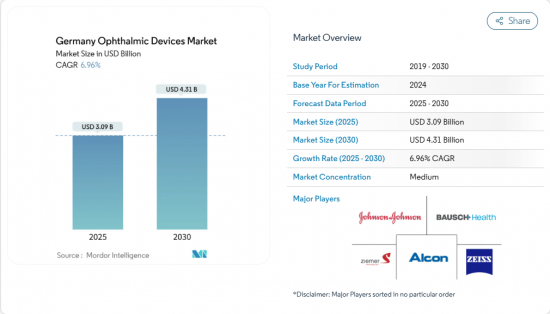

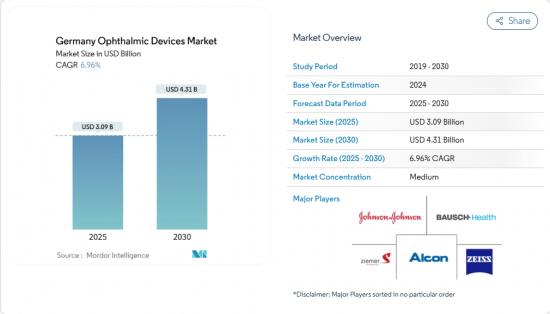

독일의 안과용 기기 시장 규모는 2025년에 30억 9,000만 달러, 2030년에는 43억 1,000만 달러에 이를 것으로 예상되며, 예측 기간의 CAGR은 6.96%를 나타낼 전망입니다.

인구의 급속한 노화, 임상의의 높은 디지털 리터러시, 백내장 수술 및 굴절 교정 수술의 외래로의 전환은 진단, 시력 관리 및 수술의 각 제품 라인에서 지속적인 수요를 지원합니다. 기기 제조업체는 진단 경로를 압축하는 데이터 대응 플랫폼과 수술실에서의 시간을 단축하는 저침습 툴에 자금을 투입하고 있으며, 거시경제가 침체한 경우에도 수주량을 확보하고 있습니다. DRG 인센티브와 기술 애드온에 대한 명확한 상환을 둘러싼 지불자의 조정으로 투자 회수 기간이 단축되어 틈새 기회를 요구하는 소규모 혁신자를 끌어들이고 있습니다. 독일의 안과용 기기 시장은 여전히 단편화되고 있지만, 소모품, 자본 설비, 소프트웨어를 번들할 수 있는 공급업체는 우수한 마진을 획득할 수 있는 입장에 있습니다.

굴절이상을 추적하는 연구에 따르면, 유병률은 초등학생으로부터 청소년기에 걸쳐 급격히 상승하고, 원시는 노인층에서 가속하고 있습니다. 소매업체는 적극적인 가격 인상 없이 반복 구매를 늘리기 위해 남녀별 프레임과 오르소 K 렌즈로 대응하고 있습니다. 스크린 타임의 보급과 야외 활동의 감소로 안경, 콘택트렌즈, 신흥 근시 억제 솔루션에 대한 수요가 증가하고 있습니다. 제품 출시와 착용 시간을 모니터링하는 모바일 앱을 결합한 Vision Care 벤더는 데이터 중심의 업셀 전략을 검증하고 브랜드 로열티를 강화하고 있습니다. 그 결과 독일의 안과용 기기 시장은 광범위하고 탄력적인 소비자 기반을 누리고 있습니다.

2024년 10월 DRG 업데이트에서는 고급 안구 렌즈의 보험 적용을 확대하는 3개의 안과 코드가 추가되었습니다. 단초점 렌즈는 계속해서 전액 보험 상환되지만, 다초점 렌즈와 토릭 렌즈는 여전히 자기 부담이 있기 때문에 곧 보급하기가 어렵습니다. 따라서 병원은 수술 후 미세 조정이 가능한 조절식 안구 렌즈를 시험적으로 도입하여 비용 효율적인 시력 결과를 실증하고 있습니다. 조기에 도입된 병원에서는 재수술률이 낮은 것으로 보고되고 있으며, 이 지표는 장래의 요금 교섭에 영향을 미칠 것으로 기대되고 있습니다. 이러한 장점을 증명하기 위해 실제 세계 증거를 사용하는 제조업체는 프리미엄 기술이 지불자의 가치 프레임 워크에 부합하는 독일 안과용 기기 시장의 시나리오를 강화하고 있습니다.

법정 질병 기금은 프리미엄 안경과 굴절 교정 안구 렌즈에 엄격한 기준 가격을 적용하여 제조 업체의 마진을 압박하고 있습니다. 2025년 이후 위험이 높은 의료기기에 공동 임상 평가를 의무화하는 EU의 의료 기술 평가 규정이 다가오고 있으며 소규모 기업 시장 진입 일정이 장기화될 수 있습니다. 견고한 실제 임상 증거를 갖춘 기업은 규제 장애물을 경쟁적 해자로 바꿀 수 있습니다. 그럼에도 불구하고 비용 상한은 여전히 ASP의 중석이 되어 독일의 안과용 기기 시장 가격의 폭을 좁히고 있습니다.

2024년 독일의 안과용 기기 시장 규모는 비전 케어 제품이 최대를 차지했지만, 이는 정착된 구매 습관과 이익률이 높은 연속 착용 렌즈의 꾸준한 도입을 반영했습니다. 현장에서의 굴절 교정 서비스를 통합한 소매 체인은 점포에의 내점자수를 늘리고, 부속 액세서리의 매출을 밀어 올려, 이 부문의 62%의 점유율을 더욱 지키고 있습니다. 모바일 앱의 컴플라이언스 트래커가 있는 근시 관리 렌즈를 배포하는 공급업체는 교체 빈도를 높이고 브랜드의 끈끈함을 향상시킵니다. 판매량이 많은 안경과 프리미엄 콘택트렌즈의 공존은 판매량의 안정과 ASP의 확대라는 이중의 기회를 강조하고 있습니다.

진단 및 모니터링 기기는 절대 베이스에서는 작은 것, 2025-2030년의 CAGR은 1자리대 후반으로 예측되어, 가장 급성장하는 카테고리가 됩니다. 병원 관리자는 OCT 및 안저 카메라 구매 촉진요인으로 예방 의료 가이드라인과 만성 질환 감시 목표를 꼽았습니다. 선도적인 렌즈 제조업체의 하이델베르크에 본사를 둔 이미지 처리 전문 기업 인수는 수직 통합이 스크리닝 하드웨어와 개별화된 렌즈 솔루션을 결합하여 스캔에서 처방까지의 원활한 데이터 흐름을 가능하게 하는 방법을 보여줍니다. 이 루프를 닫으면 공급업체는 경쟁 우위를 확보하고 독일의 안과용 기기 시장에서 점유율을 확대할 수 있습니다.

The Germany ophthalmology devices market size is valued at USD 3.09 billion in 2025 and is projected to reach USD 4.31 billion by 2030, expanding at a 6.96% CAGR over the forecast period.

A rapidly ageing population, high digital literacy among clinicians, and the migration of cataract and refractive surgery to ambulatory settings collectively underpin sustained demand across diagnostic, vision-care, and surgical product lines. Device makers are pouring capital into data-enabled platforms that compress diagnostic pathways and into minimally invasive tools that trim operating-room time, insulating order volumes even during macro-economic slow-downs. Payer alignment around DRG incentives and clearer reimbursement for technology add-ons is shortening payback horizons, which attracts small innovators seeking niche opportunities. Although the Germany ophthalmology devices market remains fragmented, suppliers that can bundle consumables, capital equipment, and software are positioned to capture superior margins.

Studies tracking refractive errors show prevalence rates rising sharply from primary-school age to young adulthood, while hyperopia accelerates in older cohorts. Retailers respond with gender-specific frames and ortho-k lenses that increase repeat purchases without aggressive price hikes. Screen-time proliferation and reduced outdoor activity amplify demand for spectacles, contact lenses, and emerging myopia-control solutions. Vision-care vendors that pair product launches with mobile apps monitoring wear-time see stronger brand loyalty, validating a data-driven upsell strategy. The Germany ophthalmology devices market consequently enjoys a broad, resilient consumer base.

The October 2024 DRG update added three ophthalmology codes that broaden coverage for advanced IOLs. While monofocal models remain fully reimbursed, multifocal and toric lenses still entail co-payments, tempering immediate uptake. Hospitals therefore pilot adjustable IOLs that can be fine-tuned post-operatively, demonstrating cost-effective visual outcomes. Early adopters report lower re-operation rates, a metric expected to influence future tariff negotiations. Manufacturers using real-world evidence to prove these benefits reinforce the Germany ophthalmology devices market narrative that premium technology aligns with payer value frameworks.

Statutory sickness funds apply tight reference pricing to premium spectacles and accommodative IOLs, compressing manufacturer margins. The looming EU Health Technology Assessment regulation, mandating joint clinical evaluations for high-risk devices from 2025, could elongate market-entry timelines for small firms. Companies equipped with robust real-world evidence may convert the regulatory hurdle into a competitive moat. Nonetheless, persistent cost caps weigh on ASPs, limiting the pricing latitude of the Germany ophthalmology devices market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Vision-care products accounted for the largest slice of Germany ophthalmology devices market size in 2024, reflecting entrenched purchasing habits and the steady introduction of higher-margin continuous-wear lenses. Retail chains integrating on-site refraction services increase store traffic and boost ancillary accessory sales, further protecting the segment's 62% share. Suppliers deploying myopia-management lenses accompanied by mobile-app compliance trackers raise replacement frequency and reinforce brand stickiness. The coexistence of high-volume spectacles and premium contact-lens materials underscores a dual-track opportunity: volume stability alongside ASP expansion.

Diagnostic and monitoring equipment, though smaller in absolute terms, is forecast to post a high single-digit CAGR from 2025-2030, making it the fastest-growing category. Hospital administrators cite preventive-care guidelines and chronic-disease surveillance targets as drivers for OCT and fundus-camera purchases. A leading lens maker's acquisition of a Heidelberg-based imaging specialist illustrates how vertical integration pairs screening hardware with personalised lens solutions, enabling seamless data flow from scan to prescription. By closing this loop, vendors sharpen competitive moats and lift wallet share within the Germany ophthalmology devices market.

The Germany Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, Ambulatory Surgery Centers (ASCs), and Other End-Users). The Market Forecasts are Provided in Terms of Value (USD).