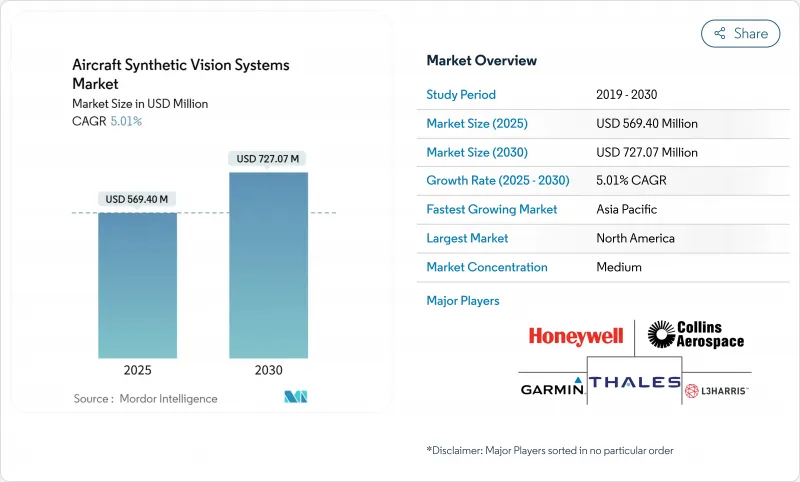

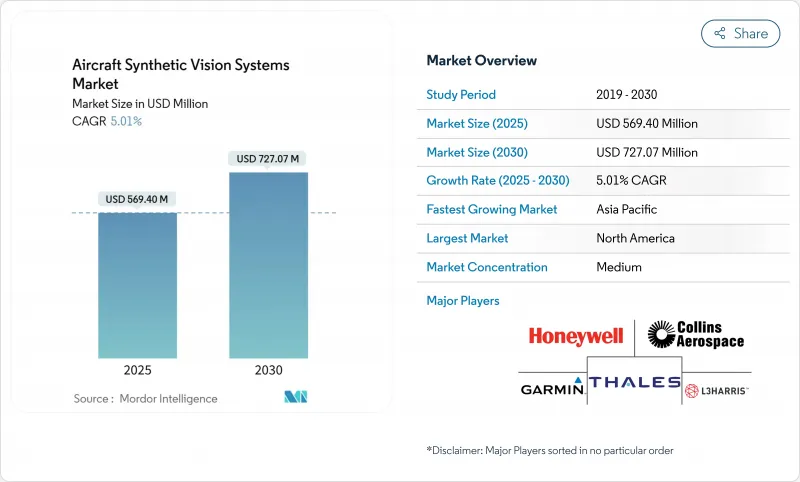

항공기용 합성 비전 시스템 시장은 2025년에 5억 6,940만 달러에 달하고, 2030년에는 7억 2,707만 달러에 이르며, CAGR 5.01%를 나타낼 것으로 예측됩니다.

미국과 유럽의 규제 당국은 낮은 시인성 운항시 높은 상황 인식을 제공하는 조종석 업그레이드를 의무화하고 있기 때문에 채용이 가속화되고 있습니다. 항공사 및 비즈니스 제트 운항사는 합성 비전이 기존 비행 데크 아키텍처에 통합될 수 있으며 다운타임을 최소화할 수 있으므로 규정 준수에 가장 비용 효율적인 방법이라고 생각합니다. 동시에 AI 구동 지형 렌더링 엔진에 초점을 맞춘 항공사와의 제휴는 파일럿 작업 부담을 줄이는 동시에 데이터 구독 서비스의 부대 수익원을 개척하고 있습니다. 또한 첨단 공기 이동성 프로그램과 합성 비전을 핵심 안전 레이어로 취급하는 6세대 전투기 프로젝트도 성장 전망을 뒷받침하고 있습니다. 이러한 요인은 OEM LINE-FIT 및 레트로 피트 채널에서 항공기용 합성 비전 시스템 시장의 견조한 전망을 지원합니다.

현재, 신형 비즈니스 제트기의 납품에는 합성 비전과 강화 시각을 단일의 디스플레이에 통합한 복합 시각 스위트를 일상적으로 포함하고 있습니다. 봄바르디아의 Global 8000과 세스나의 Citation Ascend는 이러한 기능을 기본 장비로 통합하여 고가의 애프터마켓에서 설치할 필요가 없습니다. 운영자는 조종사의 작업 부담 완화의 혜택을 누리며 제조업체는 2025년부터 2026년까지 개수가 예정된 레거시 플릿에서 정기적인 업그레이드 수익을 얻을 수 있습니다.

NGAD F-47과 같은 6세대 전투기 프로그램은 전술 데이터와 실시간 지형 이미지를 융합한 헬멧 탑재 디스플레이에 의존합니다. 콜린스 에어로스페이스의 F-35용 Gen III 헬멧은 이미 합성 비전이 암시장치를 대체하고 있음을 입증하고 있으며, 보다 폭넓은 군용 채용에 대한 길을 열고 있습니다. 그 후, 소비자용 플랫폼은 이러한 경화 기술을 계승하여 인증 사이클을 단축하고 있습니다.

머신러닝을 통한 지형 데이터베이스는 결정론적인 DO-178C 프레임워크에 잘 맞지 않으므로 승인이 길어지고 개발 비용이 증가합니다. 경우에 따라 OEM 및 바이오닉스 공급업체는 인증 위험을 줄이기 위해 SVS 기능의 복잡성을 제한합니다. 따라서 다이나믹 지형 렌더링, 도시 3D 모델링, EO/IR 피드와의 통합 등의 기능이 지연되고 있습니다. 예를 들어, 머큐리 시스템의 이미지 통합 툴은 부분적인 구제를 제공하지만 소규모 공급업체에게는 장애물인 설계 보증 레벨 C의 검증이 필요합니다. 인증 비용은 대부분의 경우 운영자에게 전가되어 SVS 업그레이드를 더 비쌉니다. 이러한 이유로 소형 터보프롭 기계 및 헬리콥터 시장에서는 SVS의 상업적 이용 가능성이 제한됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

1차 비행 디스플레이는 2024년 항공기용 합성 비전 시스템 시장 점유율의 45.51%를 차지했습니다. 헤드업 디스플레이와 헬멧 마운트 디스플레이가 CAGR 11.50%를 나타내 가장 빠른 성장을 보이고 있는데, 이는 주로 방위 관련 수주와 군사 기술의 민간으로의 트리클 다운 때문입니다. Garmin의 SVT 업그레이드 경로는 운전자가 조종석 배선을 변경하지 않고 기존 PFD에 3D 지형을 추가한다는 것을 보여줍니다. 헬멧 탑재 솔루션의 항공기용 합성 비전 시스템 시장 규모는 2030년까지 확대될 것으로 예측됩니다.

이 부문의 기세는 합성 지형에 적외선 이미지를 겹쳐서 모니터를 추가하지 않고 전천후 기능을 실현하는 통합 복합 비전 제품에도 이르고 있습니다. 유니버설 아비오닉스의 ClearVision은 민간 제트기에서의 웨어러블 HUD 채용의 선례가 되고, 콜린스 에어로 스페이스는 전투기 등급의 헬멧을 민간 회전익기에 채용하고 있습니다. 이러한 개발은 항공기의 합성 비전 시스템 시장을 개별 제품이 아닌 기술의 연속체로 강화하여 플랫폼의 횡단적인 학습과 양의 효율화를 가능하게 합니다.

디스플레이 하드웨어는 2024년에 40.12%의 매출을 획득했습니다. 그러나 소프트웨어와 지형 장애물 데이터베이스는 CAGR 9.51%로 성장하고 있으며, 비행 중에 업데이트되는 AI 리치 컨텐츠에 대한 축족을 반영하고 있습니다. 이 변화는 항공기용 합성 비전 시스템 시장 규모가 2020년대 후반에 하드웨어 전용 패키지를 따라갈 것으로 예상되는 이유를 설명합니다.

공급업체는 렌더링 엔진을 디스플레이와 별도로 라이선스를 제공하는 경우가 늘어나며 운영자는 저비용 시중 모니터로 교체할 수 있습니다. 하니웰의 MEMS 기반 KSG7200 레퍼런스 시스템은 기존 LRU에 처리 능력을 패키징한 센서 퓨전 모듈에 대한 폭넓은 동향을 돋보이게 합니다. 데이터베이스 구독은 정기적인 현금 흐름을 만들어 고객과의 관계를 강화합니다.

항공기용 합성 비전 시스템 시장 보고서는 유형별(기본 비행 디스플레이, 기타), 최종 사용자별(군사, 기타), 설치 유형별(OEM 라인 맞춤, 기타), 구성 요소별(디스플레이 시스템, 기타), 플랫폼별(고정익 항공기 등), 지역별(북미, 유럽 등)으로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 세계 매출의 35.25%를 차지했으며, FAA에 의한 강화 비행 비전에 관한 명확한 규칙과 견조한 비즈니스 제트기의 이용에 지지되고 있습니다. 운항 회사는 겨울 폭풍 활동 중에 일정을 유지하는 접근 및 크레딧을 보장하기 위해 합성 비전을 채택합니다. F-47 프로그램과 같은 국방 계약은 이 지역의 전문 지식을 깊게 하고 공급자가 민간과 군사에 걸친 R&D를 상각할 수 있게 합니다.

아시아태평양은 CAGR 8.75%를 나타내 가장 급성장하고 있는 지역이지만, 이는 중국, 인도, 인도네시아 정부가 2차 공항 정비를 진행하는 한편 ACMI 항공사에 항공기 확대를 장려하고 있기 때문입니다. 항공기용 합성 비전 시스템 시장은 한때 낮은 시인성 비행이 주요 허브 공항의 전매 특허였던 이들 국가에서 비옥한 토양을 찾을 수있었습니다. 지상 기반 ILS 배포가 지연되는 동안 위성 기반 강화와 새로운 GNSS 별자리가 더욱 널리 보급됩니다.

유럽은 SESAR 지침과 강력한 방어 계획을 배경으로 꾸준히 성장하고 있습니다. EASA의 All Weather Operations 프레임 워크는 항공사에게 CAT II/III 지상 시스템을 도입하지 않고 합성 비전을 추가하는 경제적인센티브를 제공합니다. 정확한 지형 모델에 의해 최적화된 비행 경로는 연료 소비와 CO2를 줄입니다. 이러한 요인들로 인해 대륙의 항공기용 합성 비전 시스템 시장은 균형있게 확대되고 있습니다.

The aircraft synthetic vision systems market reached USD 569.40 million in 2025 and is forecast to reach USD 727.07 million by 2030, expanding at a 5.01% CAGR.

Adoption is accelerating as US and European regulators mandate cockpit upgrades that deliver higher situational awareness during low-visibility operations. Airline and business-jet operators view synthetic vision as the most cost-effective path to compliance because the software can be embedded in existing flight-deck architectures, minimising downtime. Concurrently, air-framer partnerships focused on AI-driven terrain-rendering engines are lowering pilot workload while opening ancillary revenue streams for data-subscription services. Growth prospects are also buoyed by advanced air-mobility programs and sixth-generation fighter projects that treat synthetic vision as a core safety layer. These factors underpin a solid outlook for the Aircraft Synthetic Vision Systems market across OEM line-fit and retrofit channels.

Deliveries of new business jets now routinely include combined vision suites that merge synthetic and enhanced vision on a single display. Bombardier's Global 8000 and Cessna's Citation Ascend integrate these features as baseline equipment, eliminating costly aftermarket installations. Operators benefit from lower pilot workload, while manufacturers capture recurring upgrade revenue on legacy fleets scheduled for retrofits in 2025-2026.

Sixth-generation fighter programs like the NGAD F-47 rely on helmet-mounted displays that fuse tactical data with real-time terrain imagery. Collins Aerospace's Gen III helmet for the F-35 already demonstrates how synthetic vision replaces night-vision gear, paving the way for wider military adoption. Subsequently, civil platforms inherit these hardened technologies, shortening certification cycles.

Machine-learning terrain databases do not fit neatly into deterministic DO-178C frameworks, prolonging approvals and raising development costs. In some cases, OEMs and avionics vendors limit the complexity of SVS features to reduce certification risk. Thus, features like dynamic terrain rendering, urban 3D modeling, or integration with EO/IR feeds are delayed. For instance, Mercury Systems' image-integrity tools provide partial relief but still require Design Assurance Level C validation, a hurdle for smaller suppliers. Certification costs are passed on to operators in most cases, making SVS upgrades more expensive. This limits their commercial viability in the markets for small turboprop aircraft and helicopters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Primary flight displays held 45.51% of the aircraft synthetic vision systems market share in 2024 because pilots rely on these central screens for all critical flight cues. Heads-up and helmet-mounted displays exhibit the fastest growth at 11.50% CAGR, largely due to defence orders and the trickle-down of military technology into civil variants. Garmin's SVT upgrade path shows operators adding 3-D terrain onto existing PFDs without re-wiring the cockpit. The aircraft synthetic vision systems market size for helmet-mounted solutions is projected to increase by 2030 as advanced air-mobility platforms favour wearable displays for weight savings.

The segment's momentum extends to integrated combined-vision products that overlay infrared imagery onto synthetic terrain, delivering all-weather capability without added monitors. Universal Avionics' ClearVision set a precedent for wearable HUD adoption in commercial jets, while Collins Aerospace adapts fighter-grade helmets for civil rotorcraft. These developments reinforce the aircraft synthetic vision systems market as a technology continuum rather than a discrete product, enabling cross-platform learning and volume efficiencies.

Display hardware captured 40.12% revenue in 2024 because every installation still needs certified screens. Yet software and terrain-obstacle databases are growing at 9.51% CAGR, reflecting a pivot toward AI-rich content that refreshes during flight. This shift explains why the aircraft synthetic vision systems market size linked to software is forecast to overtake hardware-only packages in the late 2020s.

Suppliers increasingly licence rendering engines separate from displays, allowing operators to swap in lower-cost commercial-off-the-shelf monitors. Honeywell's MEMS-based KSG7200 reference system highlights a broader trend toward sensor-fusion modules that package processing power within existing LRUs. Database subscriptions create recurring cash flows and cement customer relationships, underscoring software's strategic value in the aircraft synthetic vision systems industry.

The Aircraft Synthetic Vision Systems Market Report is Segmented by Type (Primary Flight Display, and More), End User (Military, and More), Installation Type (OEM Line-Fit, and More), Component (Display System and More), Platform (Fixed-Wing Aircraft, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 35.25% of global sales in 2024, supported by the FAA's clear rules on Enhanced Flight Vision and robust business-jet utilisation. Operators embrace synthetic vision to secure approach credits that keep schedules intact during winter storm activity. Defence contracts such as the F-47 program deepen the regional expertise pool, allowing suppliers to amortise R&D across civil and military lines.

Asia-Pacific is the fastest-growing arena at 8.75% CAGR because governments in China, India, and Indonesia are upgrading secondary airports while encouraging ACMI carriers to expand fleets. The aircraft synthetic vision systems market finds fertile ground in these nations, where low-visibility procedures were once the preserve of flagship hubs. Satellite-based augmentation and new GNSS constellations further boost uptake as ground-based ILS rollouts slow.

Europe grows steadily on the back of SESAR directives and strong defence programs. EASA's All Weather Operations framework gives carriers economic incentives to add synthetic vision without installing CAT II/III ground systems. Sustainability goals add another driver: optimised flight paths enabled by accurate terrain models cut fuel burn and CO2. These factors sustain a balanced expansion of the continent's aircraft synthetic vision systems market.