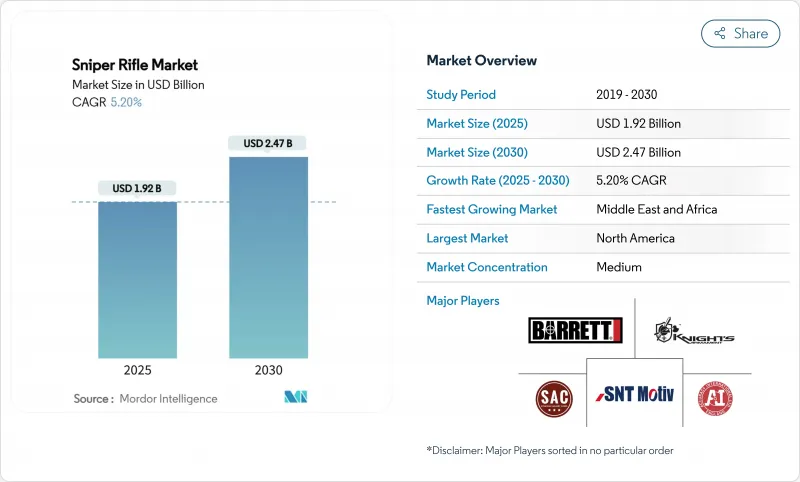

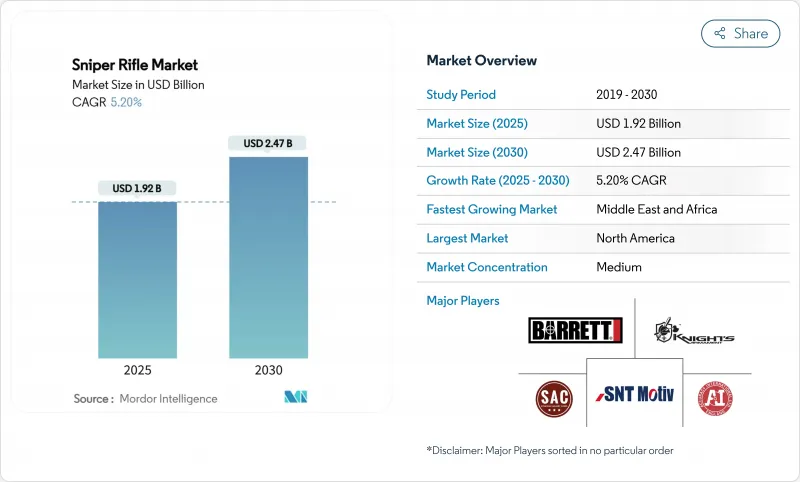

저격총 시장 규모는 2025년에 19억 2,000만 달러에 달하고, 2030년에는 24억 7,000만 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR은 5.20%를 나타낼 전망입니다

진행중인 국방 근대화 프로그램, 다구경 무기 플랫폼의 보급, 디지털 대응 광학 기기에 대한 수요가 이 꾸준한 궤도를 지원하고 있습니다. 미국, 유럽, 걸프 국가의 군사 재편 계획이 계속 조달량을 지원하는 한편 장거리 경쟁 사격과 사냥이 대규모 민간 수익 기반을 구축하고 있습니다. 광학식 화기관제의 기술 혁신 가속, 무연정밀탄약의 대두, 도시에서의 대스나이퍼 요건에 대응한 국토안전보조의 조달 증가 등이 향후 성장을 더욱 강화할 예정입니다. 동시에 수출규제 강화와 수명주기 비용 상승은 예산에 제약이 있는 최종 사용자의 채용을 억제하고 저격총 시장 전체에 신중하면서도 견고한 확대를 촉진하고 있습니다.

NATO 및 파트너 국가에서 정밀 사격 능력에 대한 배분 증가는 다년간 라이플 교환 프로그램 및 광학 장비의 업그레이드로 이어질 것입니다. 미국 육군은 2025 회계 연도에 차세대 분대 무기에 3억 6,730만 달러를 계상해, 미국 해병대는 587 유닛의 MK22 프로그램을 예정보다 빨리 완료해, 다구경으로 극단적인 사거리의 성능에 대한 제도상의 우선순위를 명확하게 했습니다. 사우디아라비아의 1,000억 달러 프레임워크 구매를 주도하는 걸프 국가의 지출은 또 다른 대규모 수요 풀을 추가하고, 노르웨이와 독일과 같은 소규모 유럽 군는 거의 동등한 위협에 대응하기 위해 새로운 장거리 소총을 표준화합니다. 이러한 동조적인 대처에 의해 초탄명중률과 간소화된 로지스틱 체인이 조합된 제조업체가 보상되고, 저격총 시장은 영속적인 대량 수주를 향한 자리 매김이 됩니다.

경쟁 사격 리그, 장거리 사냥, 레크리에이션의 정밀 매치는 활기찬 비 군사 판매 채널을 생성합니다. 스미스 앤 웨슨은 2024년 순 매출액 5억 3,580만 달러 중 1,000야드의 사격 라인용으로 조정된 정밀 롱건이 큰 비율을 차지했습니다. 민간 처리 능력의 향상으로 군용 프로그램과 제조 라인을 공유할 수 있어 단가가 낮아지고 애프터마켓의 조정 가능한 트리거, 탄소섬유 배럴, 고급 탄도 계산기의 트리클 다운이 가속화됩니다. 현재 민간 애호가가 기대하는 서브 MOA의 성능 기준은 공급업체에게 지속적인 제품 갱신 사이클을 유지하도록 압력을 가하고 정부 계약과 동일한 제조 공구를 활용하는 군사 사용자에게 간접적으로 이익을 가져오고 있습니다.

2024년 5월 미국 수출관리규칙의 개정으로 총기 및 '범죄관리' 품목 확대 그룹에 새로운 라이선스 요건이 도입되어 미국 제조업체의 리드타임과 컴플라이언스 비용이 증가했습니다. 불법 횡류를 억제하는 것이 목적이지만, 이 규칙은 일부 해외 구매자를 보다 엄격하지 않은 규정 하에서 운영되는 공급업체로 부주의하게 유도합니다. 컴플라이언스 비용에는 법적 심사, 개별 부품 번호 분류, 제 3 자 실사 비용, 소량 수출 마진 악화, 복잡한 판매 후 지원 계약 등이 포함됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

1,000m 슈퍼 라이플은 2024년 총 매출의 52.11%를 차지했으며, 이 부문은 군가 스탠드오프 거리에서 오버매치를 우선하기 때문에 CAGR 6.14%를 나타낼 전망입니다. 이러한 극단적인 사거리 시스템의 저격총 시장 규모는 2025년부터 2030년까지 2억 9,000만 달러까지 확대될 것으로 예상되지만, 이는 활동적인 전장에서 .338NM과 .50BMG 플랫폼의 조달을 반영합니다. 2km의 첫 탄명중 효율은 대포격전과 대병기의 역할을 강조하는 전술 교리의 근간을 이룹니다. 조달 계약에는 표적 캡처를 유지하면서 시그니처를 줄이기 위해 통합 억제기와 다중 센서 야간 광학 시스템이 포함되어 있습니다.

최대 1,000m 라이플총은 전망선이 제약되는 경찰 전술 부대와 시가전에서는 여전히 필수적입니다. 일반적으로 7.62NATO 또는 6.5mm 크리드 무어를 포함하는 이 무기는 훈련 비용이 낮고 서비스 소총과의 군수적 공통성으로 인해 탄약 공급이 단순해지기 때문에 안정적인 수량을 기록합니다. 저격총 시장의 수익에 차지하는 점유율은 예측 기간을 통해 약간 저하되는 것, 일관된 보충·교환 사이클이 국가 경비대나 국가 헌병대의 견고한 고객 기반을 확보하고 있습니다.

.338 라푸아 부문은 유럽, 북미, 아시아 전역에 걸친 광범위한 군용 인증과 확립된 공급망 덕분에 2024년 매출의 23.89%를 차지했습니다. 많은 군가 인정한 교전 거리를 1,500m까지 연장하고 있기 때문에 이 구경은 허용 가능한 반동으로 대인 정밀도의 기준으로 계속하고 있습니다. .338 라푸아가 차지하는 저격총 시장 점유율은 신규 참가자의 등장에 따라 약간 줄어들고 있지만 절대적인 수요는 시장 전체의 확대에 따라 성장하고 있습니다.

.300 노르마 매그넘, 8.6 블랙아웃, 신흥 9.4mm 카트리지를 포함한 '기타 구경'은 탄도계수, 총신수명, 서프레스 사격 성능의 밸런스를 취하는 노력 속에서 CAGR 최고 속도의 5.98%를 나타낼 전망입니다. 멀티 캘리버 액션은 고도, 온도 및 타겟에 맞는 카트리지 선택을 가능하게 하며, 어떠한 상품 공급망에서도 사용자를 가용성 충격으로부터 보호합니다. 레거시 7.62*51mm NATO는 기본 훈련용 총알이며, 한 발당 지출을 최소화하면서 제도적 지식을 유지합니다.

저격총 시장 보고서는 사거리(1,000M까지, 1,000M 이상), 구경(7.62 * 51mm, .300 Winchester Magnum, .338 Lapua Magnum, .50 BMG, 기타 구경), 작동 기구(볼트 액션, 세미 오토매틱), 용도(군사, 국토 안보, 민간인), 지역(북미, 유럽, 아시아태평양, 기타)으로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 2024년 매출의 38.77%를 차지했지만, 이는 미국의 국방예산이 지속적으로 계상되고 있는 것과 민간정밀사격 커뮤니티가 세계 최대이기 때문입니다. 이 지역의 저격총 시장 규모는 제조업체가 정부 및 상업시설에 고정적인 R&D 비용을 분산시킴으로써 규모 경제의 이점을 누리고 있습니다. 동시에 바이 아메리칸 조항은 연방 정부와의 계약에서 국내 조달률이 80%를 넘고 있습니다. 캐나다의 특수작전부대는 미국의 근대화 패턴을 답습하고 있으며, 이 지역 수요를 더욱 밀어 올리고 있습니다.

유럽은 상호운용성과 유효 사거리의 확대를 요구하는 NATO 회원국들 사이에서 단계적이지만 꾸준한 재자본화에 의해 큰 점유율을 유지하고 있습니다. 여기에서의 조달 방침은 통합형 서프레서, 무연 탄약에 대한 대응, 디지털 데이나이트 광학계를 중시하고, 엄격한 환경 기준과 병사의 지속가능성 기준에 따른 것이 되고 있습니다. 노르웨이, 독일, 이탈리아에 있는 고고도 훈련 시설은 극저온 배럴 야금의 장소이기도 하고, 혁신을 세계 제품 라인으로 순환시킵니다.

중동 및 아프리카는 걸프 국가의 군주국이 수십억 달러 규모의 재군비 계획을 진행하고 사하라 이남 국가들이 테러 대책과 국경 경비 능력에 투자하기 때문에 CAGR이 6.89%를 나타낼 전망입니다. 사우디아라비아와 아랍에미리트(UAE)의 대량 주문은 보다 광범위한 지역 전체의 플랫폼 표준화에 영향을 미칩니다. 아프리카 특수 부대는 NATO의 탄약 공급망과 호환되는 유럽의 볼트 액션 모델에 끌려갑니다. 이러한 계약에는 현지에서의 보수 훈련 파트너십도 수반되어 라이프 사이클의 지속성을 지원하는 토착 무기공의 스킬 세트를 구축하고 있습니다.

아시아태평양에서는 인도의 신흥 국산 제조거점과 멀티 롤 광학계를 갖춘 대 머티리얼 시스템에 대한 호주 특수 작전의 요구에 따라 채용이 증가하고 있습니다. 동남아시아의 병행 경제 성장으로 장거리 저격무기를 포함한 안보예산이 재량적으로 확보되었으나 납품은 여전히 서양 OEM의 수출규제 승인에 좌우됩니다. 남미에서는 주로 도시와 정글이 혼재하는 환경에서 국제범죄와 싸우는 전문경찰부대에 의한 중등도 수요가 보이고, 조달주기는 다국간의 공적안보자금과 밀접하게 연결되어 있습니다.

The sniper rifle market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 2.47 billion by 2030, reflecting a CAGR of 5.20% during the forecast period.

Ongoing defense-modernization programs, the proliferation of multi-caliber weapon platforms, and demand for digitally enabled optics sustain this steady trajectory. Military recapitalization programs in the United States, Europe, and the Gulf states continue to anchor procurement volumes, while long-range competitive shooting and hunting build a sizeable civilian revenue base. Accelerating innovation in optical fire-control, the emergence of lead-free precision ammunition, and rising homeland-security procurements in response to urban counter-sniper requirements further reinforce future growth. At the same time, tightened export-control regimes and higher life-cycle costs temper adoption among budget-constrained end users, fostering measured but resilient expansion across the sniper rifles market.

Escalating allocations for precision-fire capabilities in NATO and partner nations translate into multi-year rifle replacement programs and optics upgrades. The US Army earmarked USD 367.3 million for Next-Generation Squad Weapons in fiscal 2025, and the US Marine Corps completed its 587-unit MK22 program ahead of schedule, underscoring institutional priority for multi-caliber, extreme-range performance. Gulf-state outlays-headlined by Saudi Arabia's USD 100 billion framework purchase-add another sizeable demand pool, while smaller European militaries such as Norway and Germany standardize on new long-range rifles to match near-peer threats. These synchronous initiatives reward manufacturers that pair first-round hit probability with simplified logistic chains, positioning the sniper rifles market for enduring large-volume orders.

Competitive shooting leagues, long-range hunting, and recreational precision matches create a vibrant non-military sales channel. Smith & Wesson attributed a meaningful share of its USD 535.8 million FY2024 net sales to precision long guns tailored for the 1,000-yard firing line. Higher civilian throughput allows shared manufacturing lines with military programs, lowering unit costs and accelerating the trickle-down of aftermarket tunable triggers, carbon-fiber barrels, and advanced ballistic calculators. The sub-MOA performance standard now expected by civilian enthusiasts pressures suppliers to maintain continuous product refresh cycles, indirectly benefiting military users that leverage the same production tooling for government contracts.

The May 2024 amendments to the US Export Administration Regulations introduced new license requirements for an expanded group of firearms and "crime-control" items, adding lead time and compliance cost for American manufacturers. While aimed at curbing illicit diversion, the rules inadvertently steer some foreign buyers toward suppliers operating under less stringent regimes. Compliance overhead includes legal reviews, individual part number classification, third-party due diligence fees, eroding margin on small-lot exports, and complicated after-sales support agreements.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Beyond 1,000 m rifles generated 52.11% of the total 2024 revenue, and the segment is advancing at a 6.14% CAGR as militaries prioritize overmatch at standoff distances. The sniper rifle market size for these extreme-range systems is forecast to widen by USD 0.29 billion between 2025 and 2030, reflecting procurement of .338 NM and .50 BMG platforms in active theaters. First-round hit efficacy at two kilometers underpins tactical doctrines emphasizing counter-battery engagements and anti-materiel roles. Procurement contracts increasingly include integrated suppressors and multi-sensor day-night optics to reduce signature while preserving target acquisition.

Up to 1,000 m rifles remain vital for police tactical units and urban warfare where line-of-sight is constrained. These weapons, generally chambered in 7.62 NATO or 6.5 mm Creedmoor, log consistent volume because training costs are lower and logistical commonality with service rifles simplifies ammunition supply. While their share of the sniper rifles market revenue slips slightly through the forecast horizon, consistent replenishment and replacement cycles ensure a solid customer base among national guard and gendarmerie formations.

The .338 Lapua segment accounted for 23.89% of 2024 revenue thanks to widespread military qualification and established supply chains across Europe, North America, and Asia. As many armies extend qualified engagement ranges to 1,500 m, this caliber remains the benchmark for anti-personnel precision with acceptable recoil. The sniper rifle market share held by .338 Lapua erodes only marginally as new entrants arrive, but absolute demand grows in line with overall market expansion.

"Other Calibers," encompassing .300 Norma Magnum, 8.6 Blackout, and emerging 9.4 mm cartridges, register the fastest 5.98% CAGR amid efforts to balance ballistic coefficient, barrel life, and suppressed-fire performance. Multi-caliber actions allow units to select cartridges matched to altitude, temperature, and target set, insulating users from availability shocks in any commodity supply chain. Legacy 7.62*51 mm NATO is the default training round, preserving institutional knowledge while minimizing per-shot expenditure.

The Sniper Rifle Market Report is Segmented by Range (Up To 1, 000 M, and Beyond 1, 000 M), Caliber (7. 62*51 Mm, . 300 Winchester Magnum, . 338 Lapua Magnum, . 50 BMG, and Other Calibers), Operating Mechanism (Bolt-Action and Semi-Automatic), Application (Military, Homeland Security, and Civilian), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America anchored 38.77% of 2024 turnover owing to sustained US defense appropriations and the world's largest civilian precision-shooting community. The sniper rifle market size in the region benefits from economies of scale as manufacturers spread fixed R&D costs over government and commercial runs. At the same time, buy-American provisions keep domestic content above 80% in most federal contracts. Canadian special operations units follow US modernization patterns, further bolstering regional demand.

Europe maintains a significant share through gradual but steady recapitalization among NATO members seeking interoperability and extended effective ranges. Procurement agendas here emphasize integrated suppressors, lead-free ammunition compliance, and digital day-night optics, aligning with stringent environmental and soldier-sustainability standards. High-altitude training sites in Norway, Germany, and Italy also provide grounds for extreme-cold barrel metallurgy, feeding innovation that circulates back into global product lines.

The Middle East and Africa are poised for a 6.89% CAGR as Gulf monarchies advance multi-billion-dollar rearmament programs and sub-Saharan forces invest in counter-terror and border-security capabilities. Large-volume orders from Saudi Arabia and the United Arab Emirates influence platform standardization across the broader region. African special forces gravitate toward European bolt-action models compatible with NATO ammunition supply chains. Local maintenance-training partnerships often accompany these contracts, building indigenous armorer skill sets that support lifecycle sustainment.

Asia-Pacific records rising adoption propelled by India's emerging indigenous manufacturing base and Australian special operations requirements for anti-materiel systems with multi-role optics. Parallel economic growth in Southeast Asia yields discretionary security budgets that include long-range sniper assets, though deliveries remain sensitive to export-control approvals from Western OEMs. South America shows moderate demand, driven mainly by specialized police units combating transnational crime in mixed urban-jungle environments, with procurement cycles closely tied to multilateral public-security funding.