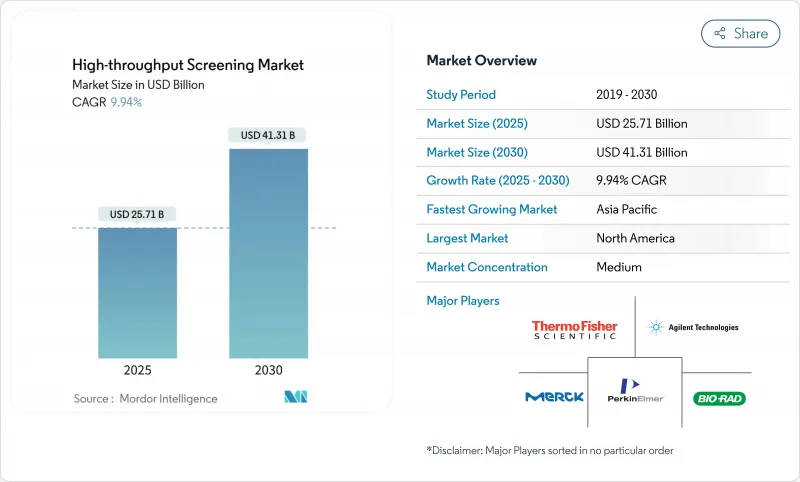

고처리량 스크리닝(HTS) 시장 규모는 2025년에 257억 1,000만 달러에 달하고, 예측 기간(2025-2030년)의 CAGR은 9.94%를 나타내, 2030년에는 413억 1,000만 달러에 달할 것으로 전망됩니다.

이 확장은 의약품의 타임라인을 단축하고 분석 당 비용을 40% 절감하는 AI를 활용한 자동화의 광범위한 도입에 뒷받침됩니다. 생리학적으로 적절한 3D 분석에 대한 수요 개발, 정밀의료에 중점을 둔 R&D 예산 증가, 개발 및 제조 위탁 기관(CDMO)으로의 전략적 아웃소싱이 상승 궤도를 강화합니다. 통합 플랫폼 제공업체 간 경쟁 격화는 신속한 기술 업데이트 사이클을 촉진하고 마이크로플루이딕스 초고처리량 스크리닝(uHTS) 플랫폼에 대한 벤처 투자는 제품 혁신을 촉진합니다. 비동물 실험과 지속가능한 실험실 실천에 대한 규제의 장려는 첨단 세포 기반 시스템에 자본을 돌리는 것으로 기세를 늘리고 있습니다.

적응형 로봇 공학의 혁신은 고처리량 스크리닝(HTS) 시장 전체의 처리량과 재현성을 향상시킵니다. 컴퓨터 비전 모듈은 현재 실시간으로 피펫팅 정확도를 안내하고 수동 워크플로우와 비교하여 실험 편차를 85% 줄였습니다. 통합된 AI 감지 알고리즘은 시간당 80개 이상의 슬라이드를 처리하여 높은 컨텐츠 이미징의 처리량 한도를 높입니다. 듀얼 인터페이스 프로그래밍을 통해 화학자는 전문가 코딩 없이 복잡한 워크플로우를 설정할 수 있어 사용자 액세스도 확대. 워크셀당 200만 달러를 넘는 설비투자도 연간 10만 화합물 이상의 생산량이라면 투자대효과 프로파일이 개선되기 때문에 정당화됩니다. 그 결과 플랫폼 업그레이드가 자체 강화 사이클이 되어, 고처리량 스크리닝(HTS) 시장을 규모, 속도, 데이터 품질의 확대를 향해 추진하고 있습니다.

정밀의료에 특화된 연구개발 예산의 확대에 의해 계산 생물학과 자동화된 실험을 통합한 스크리닝 플랫폼에 자금이 투입되고 있습니다. AI를 활용한 탐색에 의해 후보 화합물의 동정기간이 6년에서 18개월 미만으로 단축되어 AI가 발견한 2가지 암치료제를 2025년 초에 임상시험으로 진행한 리카시온 파머슈티칼스(Recursion Pharmaceuticals)와 같은 기업에 벤처기업의 자금이 유입되고 있습니다. 예산 증가와 알고리즘을 통한 효율화 시너지 효과로 인해 초기 단계 스크리닝은 위험 완화와 기간 단축을 위한 전략적 테코로 자리매김하고 있습니다. 화합물의 신속한 트리아지가 병용 요법의 탐색이나 개별화 요법을 지원하기 때문에 암 영역이나 희귀질환의 파이프라인은 특히 혜택을 받습니다.

소프트웨어, 검증, 교육 등 500만 달러에 가까운 초기 지출은 중소기업에게 재정적 마찰을 야기합니다. 연간 유지보수와 라이선싱은 영업예산을 15-20% 부풀립니다. 총 소유 비용은 대량 생산 사용자에게 유리하지만 자본 집약적이기 때문에 자금에 제약이 있는 조직에서는 도입이 지연되고 아웃소싱 서비스에 대한 수요가 유지됩니다. 장비 임대와 공유 시설 모델은이 장벽을 부분적으로 상쇄하지만 기술의 진부화 속도는 급속한 시장 침투를 막는 영원한 장애물입니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

세포 기반 분석은 복잡한 신호전달 경로를 모델링하고 인간의 효능을 생화학적 대안보다 정확하게 예측하는 능력을 반영하여 2024년 고처리량 스크리닝(HTS) 시장 점유율의 45.14%를 차지했습니다. 이 부문은 형광 리포터, 3차원 배양 스캐폴드, 미묘한 표현형의 변화를 포착하는 라벨이 없는 임피던스 기술의 지속적인 발전으로 이익을 얻고 있습니다. 실험실 칩 및 마이크로플루이딕스 플랫폼과 관련된 고처리량 스크리닝(HTS) 시장 규모는 CAGR 10.69%를 나타내 시약을 절약하고 분석 감도를 향상시킬 수 있기 때문에 빠르게 확대될 것으로 보입니다. 반면에 라벨이없는 접근법은 최소한의 분석 간섭을 찾는 안전 독성학 워크 플로우를 끌어들입니다.

고콘텐트 이미징과 AI 구동형 애널리틱스의 융합은 화면당 데이터 심도를 확대하여 예상치 못한 작용기전을 부상시키는 표현형 발견을 가능하게 합니다. 오가노이드 기반 스크리닝은 조직의 미세구조에 의해 화합물의 반응을 더욱 구별하고 종양 및 미세환경의 충실성을 필요로 하는 종양학 프로그램을 지원합니다. 이러한 기술 혁신이 결합되어 세포 기반 부문은 수익 측면에서 주도적인 지위를 굳히고 고처리량 스크리닝(HTS) 시장의 장기적인 확대를 지원하는 차세대 시스템 파이프라인의 촉매가 되고 있습니다.

1차 및 2차 스크리닝 용도는 2024년 고처리량 스크리닝(HTS) 시장 규모의 53.56%를 차지하여 히트 화합물 식별에 있어서 기본적인 역할을 명확히 했습니다. 분석 자동 소형화와 AI 트리어지는 샘플 처리량을 가속화하고 리드 화합물의 신속한 선택이라는 창약 팀의 요구에 부합합니다. 한편 독성학과 ADME의 워크플로우는 세계적인 규제 당국이 동물 이외의 안전성 데이터를 요구하고 있기 때문에 2030년까지의 CAGR이 13.82%를 나타낼 전망입니다. 이 변화는 조기 안전 조사가 후기 단계에서의 소모 비용을 최소화하는 경제적 계산을 반영한 것으로, 압축된 스케줄로 운영되는 벤처 기업 주도 프로그램에 중요한 고려사항입니다.

In vitro 독성학 플랫폼은 현재 인간 유래 세포주, 장기 온칩 장치 및 예측 AI 모델을 통합하고 있으며, 후보 화합물의 우선순위화를 돕는 360도 안전 프로파일링을 제공합니다. CRISPR을 이용한 표적 검증은 질병 유전자 연쇄 연구를 가속화하고, 멀티플렉스 바이오마커 리드아웃은 트랜스레이셔널한 관련성을 선명하게 합니다. 이러한 역학을 종합하면 레거시 대량 스크리닝과 안전성 중심 분석의 균형을 맞추어 수익 흐름을 다양화하고 프리미엄 가격을 설정하고 고처리량 스크리닝(HTS) 시장 전체의 안정성을 강화합니다.

본 보고서에서는 고처리량 스크리닝(HTS) 시장을 기술별(초고처리량 스크리닝, 셀 기반 분석 등), 용도별(표적 식별, 기타), 제품 및 서비스별(장치, 기타), 최종 사용자별(제약기업, 생명공학기업 등), 지역별(북미, 유럽, 아시아태평양 등)으로 분류하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

북미는 성숙한 제약 생태계, AI를 활용한 자동화의 높은 도입률, 벤처 캐피탈의 견조한 참여에 힘입어 2024년에 39.81%의 매출을 창출했습니다. 광범위한 화합물 라이브러리와 유리한 상환 환경이 플랫폼 업그레이드를 촉진하고 지역 전체 수요를 지원합니다. 미국의 고처리량 스크리닝(HTS) 시장 규모는 학술계 및 산업계의 트랜스레이셔널 리서치 파트너십에 인센티브를 제공하는 전략적 미국 국립보건연구소(NIH) 보조금의 혜택을 받고 있습니다.

유럽은 3차원 세포 배양의 채택을 장려하는 엄격한 품질 기준과 지지적인 규제 프레임워크를 통해 꾸준한 성장을 유지하고 있습니다. 독일, 네덜란드 및 스칸디나비아 국가의 클러스터는 지속 가능한 실험실 이니셔티브를 지원하고 대륙의 환경 목표에 부합하는 재사용 가능한 미세 유체 카트리지에 대한 투자에 박차를 가하고 있습니다. 이 지역 시장은 차세대 독성학을 향한 Horizon-Europe의 자금도 끌고 있습니다.

아시아태평양의 CAGR은 14.16%를 나타낼 전망이고, 중국의 바이오테크놀러지 섹터가 자본 유입을 재개하고 정책적 지원책이 강구됨에 따라 구미 국가를 상회할 것으로 예측됩니다. 2025년에는 생명공학주가 60% 상승하여 AI 부문의 주가지수를 웃돌아 투자자의 자신감을 창약 인프라로 향하게 했습니다. 유럽과 미국의 메이저와 아시아의 생명 공학 회사와의 라이선싱 계약은 국제 컴플라이언스 기준을 준수하면서 경쟁력있는 운영 비용을 활용하는 스크리닝 허브를 설립합니다. 장기 온칩 및 마이크로플루이딕스 기술의 급속한 도입으로 아시아는 기존 기술에서 비약적으로 진보하고 고처리량 스크리닝(HTS) 시장의 지리적 다양화가 진행되고 있습니다.

남미와 중동, 아프리카의 신흥 시장은 미개척의 가능성을 지니고 있습니다. 브라질과 아랍에미리트(UAE)은 생명공학공원 내 공용 HTS 시설에 자금을 제공하는 국가 혁신 아젠다를 선도하고 있습니다. 인프라의 한계와 규제 변동은 현재 채용률을 낮추고 있지만, 이러한 지역으로의 세계 CDMO의 진출은 기술 이전과 현지 능력 구축을 위한 무대를 마련해 세계적인 고처리량 스크리닝(HTS) 시장의 보급에 미래의 상승을 가져옵니다.

The High-throughput Screening Market size is estimated at USD 25.71 billion in 2025, and is expected to reach USD 41.31 billion by 2030, at a CAGR of 9.94% during the forecast period (2025-2030).

This expansion is anchored in widespread adoption of AI-enabled automation that compresses drug-discovery timelines and trims per-assay costs by 40%. Growing demand for physiologically relevant 3-D assays, rising R&D budgets focused on precision medicine, and strategic outsourcing to contract development and manufacturing organizations (CDMOs) reinforce the upward trajectory. Intensifying competition among integrated platform providers fosters rapid technology refresh cycles, while venture investment in microfluidic ultra-high-throughput screening (uHTS) platforms fuels product innovation. Regulatory encouragement of non-animal testing and sustainable laboratory practices adds momentum by redirecting capital toward advanced cell-based systems.

Breakthroughs in adaptive robotics are elevating throughput and reproducibility across the high throughput screening market. Computer-vision modules now guide pipetting accuracy in real time, cutting experimental variability by 85% compared with manual workflows. Integrated AI detection algorithms process more than 80 slides per hour, lifting the ceiling for high-content imaging throughput. Dual-interface programming lets chemists configure complex workflows without specialist coding, broadening user access. Capital investments exceeding USD 2 million per workcell remain justified as return-on-investment profiles improve with volumes above 100,000 compounds annually. The result is a self-reinforcing cycle of platform upgrades that propels the high throughput screening market toward greater scale, speed, and data quality.

Expanded R&D budgets dedicated to precision medicine funnel capital into screening platforms that integrate computational biology with automated experimentation. AI-powered discovery has shortened candidate identification from six years to under 18 months, attracting venture flows to companies such as Recursion Pharmaceuticals, which progressed two AI-discovered oncology drugs to clinical trials in early 2025. The multiplier effect between rising budgets and algorithmic efficiency positions early-stage screening as a strategic lever for risk mitigation and timeline compression. Oncology and rare-disease pipelines especially benefit, as rapid compound triage supports combination-therapy exploration and personalized regimens.

Initial outlays near USD 5 million, including software, validation, and training, create financial friction for smaller firms. Annual maintenance and licensing inflate operating budgets by 15-20%. Although total cost of ownership favors high-volume users, capital intensity delays adoption in cash-constrained organizations and sustains demand for outsourced services. Equipment-leasing and shared-facility models partially offset the barrier, yet the pace of technology obsolescence remains an enduring hurdle to rapid market penetration.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cell-based assays held 45.14% high throughput screening market share in 2024, reflecting their capability to model complex signaling pathways and predict human efficacy more accurately than biochemical alternatives. The segment benefits from continual advances in fluorescent reporters, 3-D culture scaffolds, and label-free impedance technologies that capture subtle phenotypic shifts. The high throughput screening market size associated with lab-on-a-chip and microfluidic platforms is set to expand rapidly as 10.69% CAGR growth unlocks reagent savings and heightens assay sensitivity. Demand for ultra-high-throughput platforms remains steady among large pharmaceutical libraries, whereas label-free approaches attract safety-toxicology workflows seeking minimal assay interference.

The fusion of high-content imaging with AI-driven analytics magnifies data depth per screen, enabling phenotypic discovery that surfaces unexpected mechanisms of action. Organoid-based screening further differentiates compound responses by tissue microarchitecture, aiding oncology programs that require tumor-microenvironment fidelity. Together, these innovations fortify the cell-based segment's leading revenue position and catalyze a pipeline of next-generation systems that sustain the high throughput screening market's long-term expansion.

Primary and secondary screening applications contributed 53.56% of the high throughput screening market size in 2024, underscoring their foundational role in hit identification. Automated assay miniaturization and AI triage have accelerated sample throughput, aligning with discovery teams' need for rapid lead selection. In contrast, toxicology and ADME workflows are poised for 13.82% CAGR through 2030 as global regulators press for non-animal safety data. The shift reflects an economic calculus wherein early safety interrogation minimizes late-stage attrition costs, a prime consideration for venture-backed programs operating on compressed timelines.

In vitro toxicology platforms now incorporate human-derived cell lines, organ-on-chip devices, and predictive AI models, offering 360-degree safety profiling that informs candidate prioritization. CRISPR-enabled target validation accelerates disease-gene linkage studies, while multiplexed biomarker readouts sharpen translational relevance. Collectively, these dynamics diversify revenue streams by balancing legacy high-volume screens with safety-centric assays that draw premium pricing, reinforcing stability across the high throughput screening market.

The High Throughput Screening Market Report Segments the Industry Into by Technology (Ultra-High-Throughput Screening, Cell-Based Assays, and More), Application (Target Identification, and More), Product and Service (Instruments, and More), End User (Pharmaceutical and Biotechnology Firms, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 39.81% revenue in 2024, sustained by mature pharmaceutical ecosystems, high adoption of AI-enabled automation, and robust venture capital participation. Expansive compound libraries and favorable reimbursement landscapes accelerate platform upgrades, anchoring region-wide demand. The high throughput screening market size in the United States benefits from strategic National Institutes of Health (NIH) grants that incentivize translational research partnerships between academia and industry.

Europe maintains steady growth through stringent quality standards and supportive regulatory frameworks that encourage 3-D cell culture adoption. Clusters in Germany, the Netherlands, and the Scandinavian countries champion sustainable laboratory initiatives, spurring investments in reusable microfluidic cartridges that dovetail with continental environmental goals. The regional market also attracts Horizon-Europe funding earmarked for next-generation toxicology.

Asia-Pacific is forecast to advance at a 14.16% CAGR, outpacing Western counterparts as China's biotech sector experiences renewed capital inflows and supportive policy measures. A 60% biotech stock rally in 2025 outperformed AI sector indices, channeling investor confidence toward drug-discovery infrastructure. Licensing deals between Western majors and Asian biotech firms establish screening hubs that leverage competitive operating costs while adhering to international compliance standards. Rapid adoption of organ-on-chip and microfluidic technologies positions Asia to leapfrog legacy modalities, expanding the high throughput screening market's geographic diversification.

Emerging markets in South America and the Middle East & Africa exhibit untapped potential. Brazil and the United Arab Emirates spearhead national innovation agendas that fund shared HTS facilities within biotechnology parks. Infrastructure limitations and regulatory variability presently temper adoption rates, yet global CDMO expansion into these regions sets the stage for technology transfer and local capacity building, offering a future lift to worldwide high throughput screening market penetration.