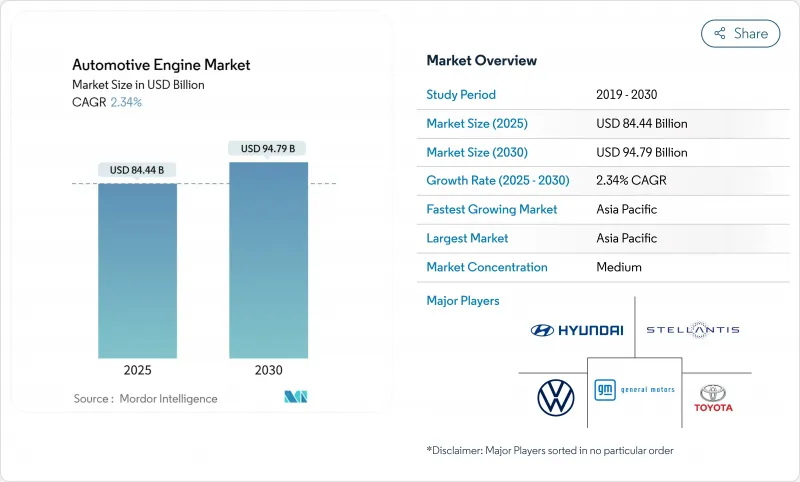

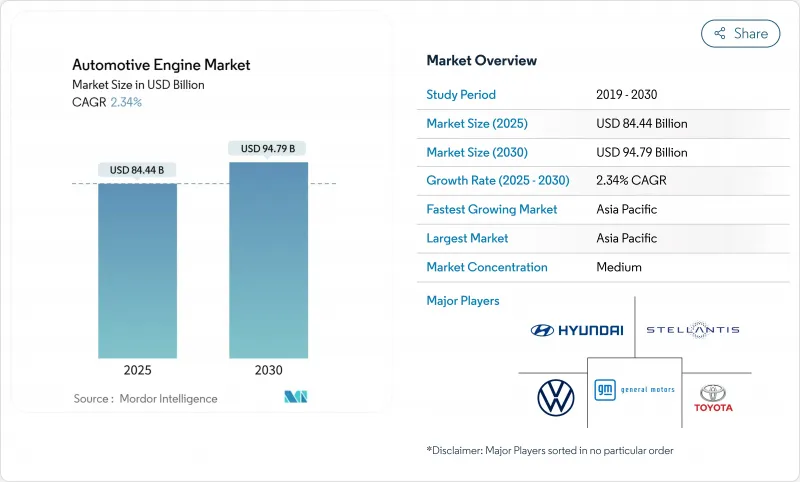

자동차 엔진 시장의 2025년 시장 규모는 844억 4,000만 달러로, 2030년에는 947억 9,000만 달러에 이르며, CAGR 2.34%를 나타낼 것으로 예측됩니다.

이 측정된 궤도는 자동차 엔진 시장이 보다 깨끗한 연소, 하이브리드 통합, 대체 연료의 선택적 도입을 통해 규모를 유지하면서 더 엄격한 배출 규제에 적응하고 있음을 보여줍니다. 아시아태평양은 수요와 생산을 선도하고 수소 내연 기관 조종사가 속도를 높이고 전기화의 불확실성을 헤지하기 위해 합성 E 연료가 상승하고 있습니다. 자동차 제조업체는 배터리 전기자동차 판매가 확대되는 동안 자동차 엔진 시장의 관련성을 확대하기 위해 아키텍처간에 위험을 분산하고 열효율을 개선하며 에너지 공급 회사와 제휴하고 있습니다. 특히 희토류와 후처리 기판공급망의 강인성은 경쟁이 격화되고 있는 것 세분화된 상황 속에서 제조업체가 이득 확보를 목표로 하는 가운데 중요한 차별화 요인이 되고 있습니다.

Euro 7 규제에서는 허용 NOx가 Euro 6에 비해 35% 삭감되고 브레이크와 타이어에 새로운 입자상 물질 규제가 도입되므로 촉매 컨버터의 대형화, 전기 가열식 후처리 장치, 가변 압축 연소 전략이 요구되고 있습니다. 북미와 아시아태평양의 주요 시장에서도 유사한 조치가 취해져 파워트레인의 세계적인 표준화가 강요되고 있습니다. 가변 밸브 타이밍, 미러 사이클 교정 및 저온 연소는 프리미엄 옵션에서 기준선 장비로 전환하고 있습니다. 그 결과 효율이 향상되고 재생 가능 연료가 혼합되면 배터리 전기 드라이브 트레인과의 탄소 갭을 줄일 수 있습니다. 이러한 규제를 종합하면 액체 연료를 포기하지 않고 컴플라이언스를 확보함으로써 자동차 엔진 시장이 강화됩니다.

2023년 4월부터 2024년 3월까지 승용차, 상용차, 삼륜차, 이륜차 및 사륜차의 총 생산량은 2,843만 4,742대에 이르렀습니다. 경쟁력 있는 인건비, 지지적인 산업 정책, 확대하는 중간층 수요가 자기강화적인 생산의 루프를 창출하고 있습니다. 이러한 기세는 성숙 경제권에서 전동화가 가속해도 지역 모델에 대한 내연기관 투자를 유지하고 자동차 엔진 시장의 성장을 지지하고 있습니다.

2024년에는 몇몇 주요 시장에서 배터리 일렉트릭의 판매량이 신차 판매량을 상회하고, 엔지니어링의 인력과 자본이 소프트웨어와 파워 일렉트로닉스에 유입되었습니다. 내연기관 프로그램의 갱신주기가 짧아지고 예산도 줄어들기 때문에 EV의 효율성이 계속 증가하고 있음에도 불구하고 기술 격차가 확대될 위험이 있습니다. 수주량 감소에 직면하는 티어원 공급업체는 전동화 부품으로의 공장 재편을 가속화할 수 있어 남은 내연 기관 생산에 비용 압력이 가해져 자동차 엔진 시장의 중하가 됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

확립된 금형과 패키징의 우위성에 의해 직렬 레이아웃은 자동차 엔진 시장에서 2024년 매출의 45.12%를 확보했고, 양판 승용차에 선호되는 아키텍처로 계속하고 있습니다. 오포즈드 피스톤 유닛은 CAGR 4.48%를 나타내며 프로토타입은 2자리 열효율 향상과 가동 부품 수의 감소를 입증하고 있습니다. 연구용 엔진은 현재 연료 사용량과 배출 가스를 줄이면서 1,000마력을 초과하고 있습니다. 상업 및 방위 분야의 관심이 높아짐에 따라 2020년대 후반에 대량 채택될 가능성이 있습니다. V형 구성은 출력 밀도가 복잡함을 상쇄하는 프리미엄 SUV나 대형 트랙에서 점유율을 유지하고 있습니다. 플랫 엔진은 낮은 무게 중심의 장점을 누릴 수있는 소량 생산 스포츠카와 오프로드 자동차에서 계속 채택되고 있습니다.

혁신적인 레이아웃에 대한 수요는 완전한 전기화 없이 효율성을 실현하는 아키텍처에 대한 업계 전반의 축족을 보여줍니다. 따라서 자동차 엔진 시장은 다양한 엔지니어링 로드맵을 지원하고 단일 기술의 위험을 줄이고 파워트레인 포트폴리오의 지역 최적화를 가능하게합니다.

가솔린은 유비쿼터스 급유 네트워크와 지속적인 연소 시스템 업그레이드를 지원하며 2024년에는 60.84%의 점유율을 유지했습니다. 수소 내연 기관은 2030년까지 연평균 복합 성장률(CAGR)이 13.42%를 나타내 가장 급성장하는 부문입니다. 현장 테스트는 익숙한 엔진의 신뢰성과 함께 CO2가 거의 0임을 입증합니다. 그린 수소 제조에 대한 국가의 보조금은 대형 트럭의 듀티 사이클 적합성과 결합하여 조기 상업 교량을 구축했습니다. 장거리화물 운송의 주류는 여전히 디젤이지만 NOx 규제 강화로 시스템 비용이 상승하고 가스와 수소 분야가 평준화됩니다.

천연 가스 엔진은 저장소에서 연료를 공급할 수 있는 함대 사용자와의 연관성을 유지하는 반면, 전자 연료 지원 엔진은 설계를 변경하지 않고 컴플라이언스에 적합한 경로를 OEM에 제공합니다. 이러한 연료의 다양화로 자동차 엔진 시장은 인프라와 정책의 급격한 변화에도 대응할 수 있는 강도를 유지하고 있습니다.

자동차 엔진 시장 보고서는 탑재 유형(직렬, V형, W형, 복서/플랫, 기타), 연료 유형(가솔린, 디젤, 천연 가스/CNG, 기타), 차량 유형(승용차, 소형 상용차, 기타), 엔진 용량(1.5L 미만, 1.5-3L, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)과 수량(단위)으로 제공됩니다.

아시아태평양은 세계 매출의 41.66%를 차지하며, CAGR은 3.06%을 나타내 다른 지역보다 높습니다. 중국은 수출을 계속 확대하고 인도는 세계 랭킹의 상위를 목표로, 동남아시아는 인도네시아와 말레이시아가 생산량을 늘리고 공급을 다양화하고 있습니다. 비용면에서의 우위성, 지지적인 정책 틀, 가구 소득의 상승이 이 지역의 ICE 생산을 강화하고 있습니다.

북미는 교체 사이클, 상용차 갱신, 다발 엔진의 제조에 의해 공장이 바빠져 CAGR 2.1%를 나타내 계속 유지될 전망입니다. 관세 리스크와 자금 조달 비용의 상승이 상승을 억제하고 있지만, ICE는 현재도 생산 대수의 90% 이상을 차지하고 있습니다. 자동차 제조업체는 향후 10년간 혼합 추진 수요에 대응할 수 있도록 유연한 라인을 계획하고 있습니다.

유럽은 가장 엄격한 규제 환경, 에너지 비용 상승 및 팬대믹 이후의 회복 지연을 반영하여 CAGR 1.8%를 나타낼 전망입니다. 하지만 이 지역에는 국내 고용을 유지하면서 컴플라이언스를 가능하게 하는 초저 배출 가스 엔진과 e연료 대응 엔진에 중점을 둔 주요 연소 연구개발센터가 존재합니다.

전반적으로 지역 세분화는 자동차 엔진 시장이 다른 속도로 진화하고 성숙 시장의 전기화와 신흥국 시장의 입증된 연소 전력에 대한 수요의 균형을 맞추고 있음을 보여줍니다.

The automotive engine market is valued at USD 84.44 billion in 2025 and is forecast to climb to USD 94.79 billion in 2030, expanding at a 2.34% CAGR.

This measured trajectory shows that the automotive engine market is adapting to stricter emission rules while retaining scale through cleaner combustion, hybrid integration, and selective deployment of alternative fuels. Asia-Pacific leads demand and production, hydrogen internal-combustion pilots are gathering pace, and synthetic e-fuels are emerging to hedge against electrification uncertainty. Automakers are spreading risk across architectures, improving thermal efficiency, and partnering with energy suppliers to extend the relevance of the automotive engine market amid growing battery-electric sales. Supply-chain resilience, especially for rare earths and after-treatment substrates, is becoming a critical differentiator as manufacturers aim to hold margins in a competitive yet fragmented landscape.

Euro 7 limits cut permissible NOx by 35% versus Euro 6 and introduce fresh particulate caps for brakes and tires, prompting bigger catalytic converters, electrically heated after-treaters, and variable-compression combustion strategies. Similar measures in North America and key Asia-Pacific markets are forcing global power-train standardization, which helps scale next-gen components. Variable valve timing, Miller-cycle calibrations, and low-temperature combustion are shifting from premium options to baseline fitments. The resulting efficiency gains narrow the carbon gap with battery-electric drivetrains when renewable fuels are blended. Altogether, these regulations reinforce the automotive engine market by ensuring compliance without abandoning liquid fuels.

From April 2023 to March 2024, the combined production of Passenger Vehicles, Commercial Vehicles, Three-Wheelers, Two-Wheelers, and Quadricycles reached 28,434,742 units. Competitive labor costs, supportive industrial policies, and expanding middle-class demand create a self-reinforcing production loop. Such momentum sustains internal-combustion investment for regional models even as electrification accelerates in mature economies, thereby underpinning growth in the automotive engine market.

Battery-electric volumes topped new-car sales in several major markets during 2024, pulling engineering talent and capital toward software and power electronics. Internal-combustion programs face shorter refresh cycles and leaner budgets, which risks widening a technology gap against ever-improving EV efficiency. Tier-one suppliers confronted with smaller order volumes may accelerate factory retooling toward electrified components, placing cost pressure on remaining ICE output and weighing on the automotive engine market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Due to established tooling and packaging advantages, the in-line layout secured 45.12% of 2024 revenue in the automotive engine market and remains the preferred architecture for mass-market passenger cars. Opposed-piston units are expanding at a 4.48% CAGR; prototypes demonstrate double-digit thermal-efficiency gains and fewer moving parts. Research engines now exceed 1,000 hp while cutting fuel use and emissions. Growing interest from commercial and defence segments suggests a viable pathway to volume adoption in the late 2020s. V-type configurations hold share in premium SUVs and heavy-duty trucks, where power density offsets complexity. Flat engines continue in low-volume sports and off-road vehicles that benefit from a low centre of gravity.

Demand for innovative layouts signals a wider industry pivot toward architectures that deliver efficiency without full electrification. The automotive engine market, therefore, supports diversified engineering roadmaps, mitigating single-technology risk and allowing regional optimisation of power-train portfolios.

Gasoline retained 60.84% share in 2024, bolstered by ubiquitous refuelling networks and continuous combustion-system upgrades. Hydrogen internal-combustion variants are the fastest-growing segment with a 13.42% CAGR through 2030; field tests demonstrate near-zero CO2 alongside familiar engine reliability. National subsidies for green-hydrogen production, combined with heavy-truck duty-cycle suitability, create an early commercial beachhead. Diesel still dominates long-haul freight, yet tightening NOx caps raise system cost, levelling the field for gas and hydrogen.

Natural-gas engines maintain relevance for fleet users with depot refuelling, whereas e-fuel-ready engines give OEMs a route to compliance without redesign. This fuel diversification keeps the automotive engine market resilient against rapid shifts in infrastructure and policy.

The Automotive Engine Market Report is Segmented by Placement Type (In-Line, V-Type, W-Type, Boxer / Flat, and More), Fuel Type (Gasoline, Diesel, Natural Gas / CNG, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Engine Capacity (Below 1. 5 L, 1. 5 To 3 L, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific holds 41.66% of global turnover and posts a 3.06% CAGR that outpaces every other region. China continues to scale exports, India aspires to top world rankings, and Southeast Asia diversifies supply with Indonesia and Malaysia stepping up output. Cost advantages, supportive policy frameworks, and rising household incomes reinforce regional ICE production.

North America sustains a 2.1% CAGR as replacement cycles, commercial-fleet renewal, and multipropulsion manufacturing keep plants busy. Tariff risks and elevated financing costs curb upside, but ICE still commands more than 90% of output today. Automakers plan flexible lines to serve mixed propulsion demand into the next decade.

Europe records a 1.8% CAGR, reflecting the toughest regulatory climate, higher energy costs, and slower post-pandemic recovery. The bloc nevertheless hosts leading combustion R&D centres focused on ultra-low emission and e-fuel-ready engines that enable compliance while retaining domestic employment.

Overall, geography segmentation shows that the automotive engine market evolves at different speeds, balancing mature-market electrification with developing-market demand for proven combustion power.