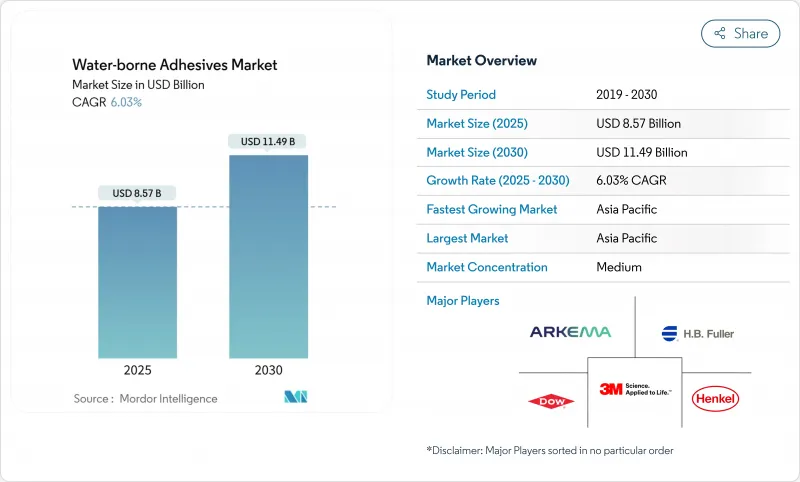

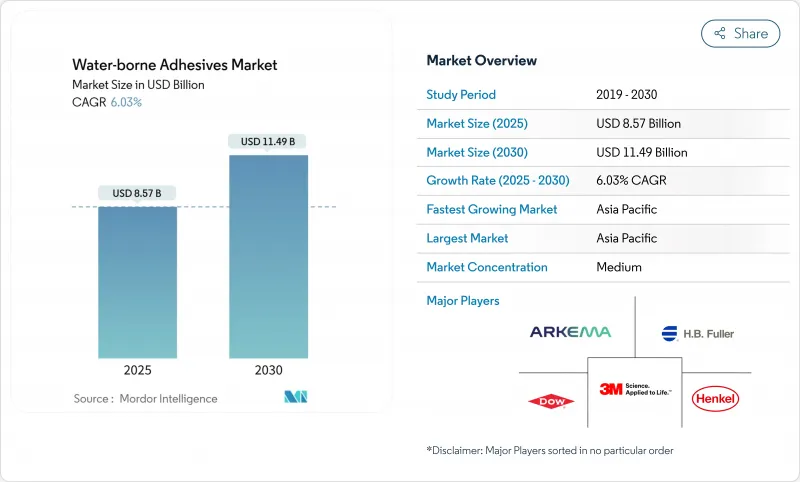

수성 접착제 시장 규모는 2025년에 85억 7,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 6.03%의 연평균 복합 성장률(CAGR)로 2030년에는 114억 9,000만 달러에 달할 것으로 예측됩니다.

수성 접착제 시장은 세계 VOC 규제 강화에 대응하고 브랜드 소유주의 지속가능성 목표를 달성하기 위해 제조업체들이 솔벤트 기반에서 수성 화학물질로의 전환을 가속화하면서 성장하고 있습니다. 이러한 성장 모멘텀은 빠르게 확대되고 있는 전자상거래 포장, 자동차 경량화, 모듈식 구조로 인해 더욱 강화되고 있으며, 각각 고성능의 저배출 접착 시스템을 요구하고 있습니다. 규제 수렴, 특히 유럽의 VOC 용제 배출 지침과 지속 가능한 제품을 위한 친환경 디자인 규제는 수성 화학물질을 사실상 영업 허가로 간주하여 다국적 기업의 포트폴리오 재구축을 촉진하는 동시에 신흥 시장으로의 기술 이전 기회를 제공합니다.

폭발적인 온라인 소매 판매로 인해 골판지 배송업체는 기존 소매업보다 1달러당 7배 더 많은 접착제를 사용하고 있습니다. 브랜드 소유자는 "자체 컨테이너 운송"에 대한 요구 사항을 엄격하게 요구하고 있으며, 컨버터는 H.B. Fuller의 Advantra 시리즈와 같은 H.B. Fuller의 Advantra 시리즈와 같은 빠른 경화 수성 등급을 채택하도록 장려하고 있으며, 커브 사이드 재활용 지침을 충족하면서 다중 노드 물류를 견딜 수 있습니다. 자동화된 케이스 씰링 라인은 고속 어플리케이터에 적합한 깨끗하고 낮은 점도의 제형에 대한 수요를 더욱 증가시키고 있습니다. 컨버터가 옴니 채널 소매 업체와의 계약을 보장하기 위해 환경 친화적 인 화학 물질을 지정함에 따라 이러한 요인은 총체적으로 수성 접착제 시장을 끌어 올립니다.

EU의 VOC 용제 배출 지침은 산업계로의 배출을 엄격히 제한하고 있기 때문에 자동차 트림, 바닥재, 파사드 패널은 수성 시스템이 표준이 되었습니다. 최근 European Coatings Show에서 바이오 PU 디스펜션의 시연을 통해 용매와 동등하거나 그 이상의 전단 강도를 보여주었습니다. Arkema는 저탄소 포장용 아크릴 수성 바인더를 출시하여 산업용 등급 수량이 5.1% 증가했다고 보고했습니다.

150℃ 이상의 연속 노출은 대부분의 수성 네트워크에 문제를 일으킵니다. 3M의 Fastbond 1000NF는 주기적인 피크에 견딜 수 있는 GREENGUARD 인증 본드를 제공한다는 점에서 진보를 보이고 있지만, 헤비 듀티 엔진, 베이킹 오븐 패널, 언더후드 라이닝은 여전히 솔벤트 기반이 주류를 이루고 있습니다. 이 열 델타를 메우기 위해서는 현재 연구 개발 초기 단계에 있는 새로운 실리콘 하이브리드 격자가 필요합니다.

보고서에서 분석된 기타 촉진 및 억제요인은 다음과 같습니다.

아크릴 에멀젼은 범용성과 저렴한 비용으로 인해 2024년 수성 접착제 시장 점유율의 38%를 차지했습니다. 폴리비닐 아세테이트는 여전히 목재 접착의 주력 제품이지만, 실내 공기 표준이 높아짐에 따라 업체들은 포름알데히드가 없는 아크릴로 전환하고 있습니다. 폴리우레탄 디스펜션은 2024년 판매량에서 차지하는 비중은 작지만 높은 박리 강도와 유연성을 겸비하고 리튬 이온 배터리 팩과 레토르트 파우치 라미네이트에서 중요한 특성을 가지고 있기 때문에 CAGR 6.55%로 발전하고 있습니다.

아크릴 블록은 프로파일렌과 아크릴산의 원료 변동으로 인한 마진 압력에 직면하고 있으며, 공급업체는 바이오 아크릴 레이트 경로와 제품별 스트림을 통합해야 할 필요성에 직면해 있습니다. 클로로프렌 분산과 틈새 하이브리드는 내유성을 포기할 수 없는 금속 가구, 신발, 광업 벨트에 사용되지만 여전히 수량에 제약이 있습니다. 전반적으로 가격 중심의 아크릴 제품군과 고가의 PU 제품군의 균형을 맞추는 배합업체는 다층적인 성장을 이룰 것으로 보입니다.

2024년 수성 접착제 시장 규모의 40%를 연포장재가 차지했으며, 이는 옴니채널 소매용 파우치, 소포장, 메일러로의 전환이 원동력이 될 것으로 보입니다. 그러나 브랜드 소유자가 PET, 산화알루미늄, 바이오 PLA 필름을 결합한 높은 장벽 설계를 요구함에 따라 다층 라미네이션은 CAGR 7.23%로 가장 빠르게 성장하고 있는 셀입니다. 수성 2액형 시스템은 현재 65N/15mm 이상의 접착 강도를 가능하게 하며, 식품 접촉 규정을 준수하면서 솔벤트 폴리우레탄의 선행 제품에 필적하는 접착 강도를 제공합니다.

테이프, 라벨, 그래픽 아트 공급망에서는 끈을 당기지 않고 자동 도포 속도에 대응하는 분산형 PSA를 채택하고 있습니다. 제본 및 종이 가공 분야에서는 새로운 비닐 아세테이트-에틸렌 공중합체가 제공하는 더 낮은 에너지의 핫 큐어 사이클에 대응하고 있습니다. 전자상거래가 가속화됨에 따라 즉시 접착력이 있으면서도 기판이 찢어지지 않는 골판지 케이스용 접착제가 각광을 받고 있으며, 대응 가능한 총 수요가 확대되고 있습니다.

수성 접착제 시장 보고서는 수지 유형(아크릴, 폴리비닐 아세테이트 에멀젼 등), 용도(연포장, 테이프 및 라벨 등), 최종 사용자 산업(건축 및 건설, 종이 및 판지 등), 기판(종이 및 판지, 금속 등), 지역(아시아태평양, 북미 등)으로 업계를 분류하고 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

아시아태평양이 2024년 40%의 매출을 주도한 것은 타의 추종을 불허하는 제조업의 두께, 탄탄한 건설 파이프라인, 가속화되는 전기자동차 생산을 반영합니다. 중국의 Tier-2 도시가 패널 접착제의 보급을 주도하고, 인도의 인프라 구축이 물량 증가를 뒷받침합니다. 이 지역의 CAGR 6.89%는 세금 감면과 녹색 조달 목록을 통해 무용제 접착제를 장려하는 일본과 한국의 규제 강화에 기인합니다.

북미는 2위를 차지했으며, 전자상거래 포장과 자동차 경량화에 힘입어 성장세를 보이고 있습니다. 미국은 소비자 제품에 대한 VOC 규제치를 지속적으로 낮추면서 수성 접착제 시장을 확대하고 있으며, 캐나다는 에너지 효율 규제로 인해 주택 개보수 단열재 채택을 촉진하고 있습니다. 멕시코의 마킬라도라(maquiladora) 회랑에서는 OEM의 수출 요건을 충족시키기 위해 수성 배합의 지정이 증가하고 있습니다.

유럽은 엄격한 지침을 통해 기술적으로 큰 영향력을 발휘하고 있습니다. 독일의 자동차 내장재, 프랑스의 유연한 식품 포장, 영국의 목조 주택 부문은 전반적으로 대륙 수요를 증가시키고 있습니다. 동유럽의 컨버터들은 EU의 결속기금의 지원을 받아 분산형 라인으로 업그레이드를 진행하여 당초 예상보다 빠르게 용매 점유율을 낮추었습니다.

남미의 전망은 브라질의 건설 경기 회복과 농업 관련 기업의 포장 수요가 헨켈의 윤디아이에 신설된 혁신 허브의 지원을 받아 완만한 수요 증가를 견인할 것으로 보입니다. 아르헨티나는 작지만 유연한 식품용 랩에 대한 수요가 꾸준히 유지되고 있습니다. 사우디아라비아의 기가 프로젝트와 남아프리카공화국의 소매 물류에서는 수입품 기준을 충족시키기 위해 수성 등급을 지정하기 시작했습니다.

The Water-borne Adhesives Market size is estimated at USD 8.57 billion in 2025, and is expected to reach USD 11.49 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

The water-borne adhesives market is growing as manufacturers accelerate the shift from solvent-based to water-based chemistries to comply with tightening global VOC rules and meet brand-owner sustainability targets. Growth momentum is reinforced by fast-expanding e-commerce packaging volumes, automotive lightweighting, and modular construction, each of which demands high-performance yet low-emission bonding systems. Regulatory convergence, especially Europe's VOC Solvents Emissions Directive and the Ecodesign for Sustainable Products Regulation, has made water-based chemistries a de facto license to operate, prompting multinationals to re-engineer portfolios while opening technology-transfer opportunities in emerging markets.

Explosive online retail sales mean corrugated shippers now use seven times more adhesive per dollar transacted than traditional retail. Brand owners have tightened "ship-in-own-container" requirements, pushing converters to adopt fast-setting water-based grades such as H.B. Fuller's Advantra series that survive multi-node logistics while meeting curbside-recyclability guidelines. Automated case-sealing lines further amplify demand for clean-running, low-viscosity formulations compatible with high-speed applicators. These factors collectively lift the water-borne adhesives market as converters specify eco-compliant chemistries to secure contracts with omnichannel retailers.

The EU VOC Solvents Emissions Directive caps industrial emissions so rigorously that water-borne systems have become standard in automotive trim, flooring and facade panels. Recent European Coatings Show demonstrations of bio-based PU dispersions highlighted equal or superior shear strength versus solvent counterparts, eroding legacy performance objections and consolidating the regulatory-driven shift. Early movers such as Arkema report a 5.1% volume lift in industrial grades after launching new acrylic water-borne binders tailored for low-carbon packaging.

Continuous exposure beyond 150 °C challenges most water-borne networks. 3M's Fastbond 1000NF illustrates progress-delivering GREENGUARD-certified bonds that tolerate cyclical peaks-but heavy-duty engines, baking-oven panels and under-hood linings remain dominated by solvent systems. Bridging this thermal delta will require novel silicone-hybrid lattices now in early R&D pipelines; until then, market penetration into these niches stays capped.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acrylic emulsions held 38% of water-borne adhesives market share in 2024 thanks to versatility and low cost. Polyvinyl acetate remains the workhorse for wood bonding, yet rising indoor-air standards are steering contractors toward formaldehyde-free acrylics. Polyurethane dispersions, although contributing a modest slice of 2024 volume, are advancing at a 6.55% CAGR because they pair high peel strength with flexibility-attributes critical in lithium-ion battery packs and retort-pouch laminates.

The acrylic bloc faces margin pressure from propylene and acrylic-acid feedstock swings, nudging suppliers to integrate bio-acrylate routes or by-product streams. Chloroprene dispersions and niche hybrids serve metal furniture, footwear and mining belts where oil-resistance is non-negotiable, but remain volume-constrained. Overall, formulators that balance price-sensitive acrylic offerings with high-value PU portfolios will capture multi-tier growth.

Flexible packaging generated 40% of water-borne adhesives market size in 2024, driven by pouch, sachet and mailer conversions for omnichannel retail. Yet multi-layer lamination is the fastest-advancing cell at 7.23% CAGR as brand owners seek high-barrier designs combining PET, aluminum oxide and bio-PLA films. Water-based two-component systems now enable more than 65 N/15 mm bond strength, matching solvent-polyurethane predecessors while ensuring food-contact compliance.

Tapes, labels and graphic arts supply chains adopt dispersion-based PSAs that meet automated application speeds without stringing. Book-binding and paper-converting segments respond to lower-energy hot-cure cycles offered by new vinyl-acetate-ethylene copolymers. As e-commerce accelerates, corrugated-case adhesives with immediate tack yet fiber-tear substrate failure gain prominence, expanding total addressable demand.

The Water-Borne Adhesives Market Report Segments the Industry by Resin Type (Acrylics, Polyvinyl Acetate Emulsion, and More), Application (Flexible Packaging, Tapes and Labels, and More), End-User Industry (Building and Construction, Paper, Board, and More), Substrate (Paper and Paperboard, Metals, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's 40% revenue leadership in 2024 reflects its unrivaled manufacturing depth, robust construction pipeline and accelerating electric-vehicle production. China's Tier-2 cities drive panel adhesive uptake, while India's infrastructure push anchors volume gains. The region's 6.89% CAGR also stems from regulatory tightening in Japan and South Korea, which incentivizes solvent-free chemistries through tax breaks and green-procurement lists.

North America ranks second, buoyed by e-commerce packaging and automotive lightweighting. The United States continues to mandate lower VOC limits in consumer products, expanding the water-borne adhesives market, whereas Canada's energy-efficiency codes spur adoption in residential retrofit insulation. Mexico's maquiladora corridors increasingly specify water-based formulations to service OEM export requirements.

Europe exerts outsized technology influence through stringent directives. Germany's auto interiors, France's flexible food packaging and the UK's timber-frame housing sectors collectively lift continental demand. Eastern European converters, supported by EU cohesion funds, upgrade to dispersion lines, eroding solvent share faster than originally forecast.

South America offers a mixed outlook: Brazil's construction recovery and agribusiness packaging needs push modest demand growth, aided by Henkel's new innovation hub in Jundiai. Argentina maintains smaller but specialized appetites in flexible food wraps. Middle East and Africa remain nascent yet promising; Saudi giga-projects and South African retail logistics are starting to specify water-based grades to meet imported-goods standards.