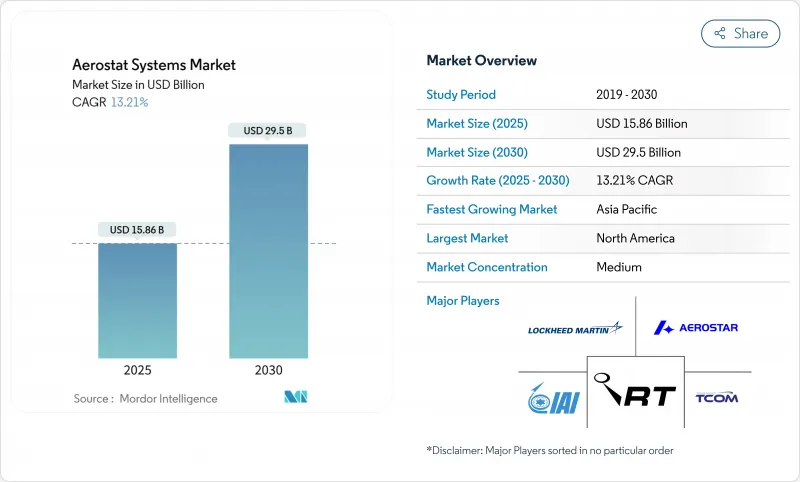

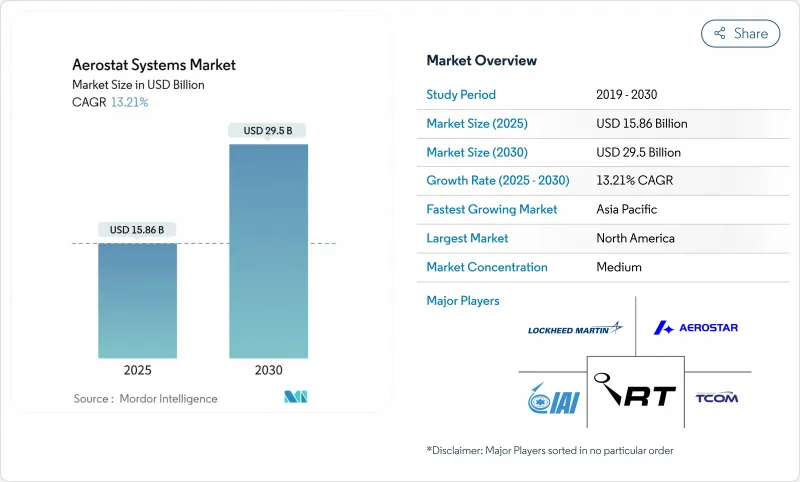

에어로스탯 시스템 시장 규모는 2025년 158억 6,000만 달러, 2030년에는 295억 달러로 확대되어 연평균 13.21%의 성장률을 보일 것으로 전망됩니다.

지속적인 감시, 국경 보안, 임시 통신 인프라 등을 위해 테더 플랫폼에 대한 의존도가 높아지는 것이 주요 성장의 촉매제가 되고 있습니다. 1억 7,000만 달러가 투입된 TARS(Tethered Aerostat Radar System)와 같은 정부 조달 프로그램은 남부 국경의 8개 지점을 대상으로 한 것으로, 이 기술의 가치 제안을 검증하고 내구성이 긴 공중 센서에 대한 예산 투입을 입증했습니다. 기존 풍선 설계는 연료를 태우지 않고도 30일간 지속할 수 있다는 점에서 여전히 우위를 점하고 있지만, 하이브리드 및 동력식 풍선은 더 무거운 페이로드와 제한적인 정점 유지 제어를 제공한다는 점에서 인기를 끌고 있습니다. 헬륨으로 채워진 풍선은 또한 재난 구호 통신의 백홀과 지방에서 5G 파일럿의 역할을 확대하여 저비용으로 신속하게 배포할 수 있는 커버리지 옵션을 원하는 이해관계자들을 끌어들이고 있습니다. 하지만 사업자는 헬륨 투입 가격 상승에 대비한 예산을 책정하고, 기상 위험에 대한 견고한 절차를 개발하고, 테더 비행을 규제하는 진화하는 항공 교통 규제를 극복해야 합니다.

2025년 QinetiQ가 수주한 남부 국경 감시 계약은 지속적인 광역 레이더 및 EO/IR 커버리지에 필수적인 에어로스탯을 확고히 했습니다. 고도 15,000피트까지 상승한 테더 풍선은 저고도에서의 침입을 감시하고 승무원 출격 없이 30일 동안 상황 데이터를 커맨드 노드에 중계했습니다. 이스라엘 항공우주산업의 하드웨어와 TCOM의 엔벨로프 전문성을 바탕으로 구축된 이스라엘의 Sky Dew 프로그램은 소형 UAV와 순항미사일에 대한 조기 경계를 가능하게 하고 또 다른 벤치마크를 제공했습니다. 국경 간 인신매매와 무인항공기의 위협이 증가함에 따라 각 기관은 지속적이면서도 예산에 맞는 센싱 계층을 찾고, 조달 파이프라인을 유지하고 있습니다.

풍선의 에어로스탯 1대가 유지보수 틈틈이 한 달간 가동함으로써 위성이나 멀티로터 UAV로 구현할 수 없는 레이더 체류시간을 동등한 총소유비용으로 실현했습니다. 테더 리프트는 헬륨 보충과 소수의 지상 작업자만 필요하기 때문에 운영자는 연료비, 승무원, 빈번한 점검 비용을 피할 수 있습니다. QinetiQ의 TARS Fleet는 예측 가능한 비용 프로파일을 기록하여 다년간의 예산 수립을 간소화합니다. 트레일러나 간이 패드에서 신속한 롤아웃을 통해 인프라 지출을 최소화할 수 있어 에어로스탯은 일시적인 이벤트, 긴급 임무 또는 타워를 건설하지 않는 탐험적인 통신 커버리지를 위한 매력적인 솔루션으로 각광받고 있습니다.

플랫폼의 한계를 넘어서는 지속적인 바람으로 인해 주기적으로 릴을 내려야 하고, 중계가 중단되고, 지상 승무원의 작업 부담이 증가했습니다. 우주 공간 근처의 바람에 대한 연구는 특정 위도에서 유효 스테이션 시간을 단축시키는 계절적 속도 피크를 보여 주었고, 운영자는 더 강력한 테더, 동적 윈치 또는 제한된 벡터링을 위해 파워 핀을 채택해야 했습니다. 결빙이나 폭우는 봉투의 무게를 증가시키고 센서의 선명도를 떨어뜨려 추가적인 위험을 추가했습니다. 따라서 운영자는 응답 주기를 단축하고 고가의 페이로드를 보호하기 위해 기상 예보 및 자동 계류 시스템에 투자했습니다.

보고서에서 분석된 기타 촉진 및 억제요인은 다음과 같습니다.

풍선 에어로스탯은 성숙한 디자인, 간편한 지상 장비, 안정적인 양력 특성으로 운영자의 지지를 받아 2024년 매출의 56.25%를 창출했습니다. 풍선 플랫폼의 에어로스탯 시스템 시장 규모는 하이브리드 아키텍처가 성장률에서 우위를 점하는 가운데, 꾸준히 상승할 것으로 예측됩니다. QinetiQ의 TARS 풍선은 EO/IR과 L-band 레이더 키트를 탑재하고 15,000피트 상공에서 헬륨과 승무원 인건비만으로 한 달간 출격할 수 있는 능력을 갖췄습니다.

풍선의 외피에 공기역학적 핀과 반강체 프레임을 결합한 하이브리드형은 테더의 내구성을 희생하지 않고 더 무거운 AESA 레이더와 멀티밴드 통신 페이로드를 탑재할 수 있기 때문에 2030년까지 18.01%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. TCOM의 해상 하이브리드는 탈착식 해상 계류 장치를 통해 해군이 부두 인프라 없이도 밤새도록 센서를 재배치할 수 있음을 보여주었습니다. 하이브리드 시스템은 특히 선박 감시, 이동식 국경 경비대 등 단계적으로 임무를 획득해 나갈 것으로 보입니다.

장거리 공중 레이더 울타리에 대한 기록적인 프로그램 지출로 인해 2024년 에어로스탯 시스템 시장 점유율의 48.52%를 군용자가 차지했습니다. 국경경비대는 인간 추적 레이더와 대 UAS 수신기에 동일한 기체를 활용하여 유지보수 풀을 확대하는 규모의 경제를 창출했습니다. 기밀성이 높은 임무에서는 소형 드론처럼 경로 밖에서 방해받지 않고, 위성처럼 강제로 소멸되지 않는 영구적인 가시선 센서가 유용하게 사용되었습니다.

2030년까지 연평균 복합 성장률(CAGR) 16.24%로 가장 빠르게 보급될 분야는 통신 중계 업무입니다. 허리케인으로 인해 지상 네트워크를 사용할 수 없는 경우, 공공 안전 부서는 이미 테더 풍선을 팝업 LTE 타워로 취급하고 있습니다. 민간 통신 사업자들은 외딴 계곡에서 실증 실험을 시작했으며, 풍선 아래에 설치된 하나의 고이득 안테나가 수십 개의 마이크로 셀을 대체하고 있습니다. 규제 당국이 주파수 대역을 확보하고 운영 규칙을 간소화함에 따라, 통신 페이로드는 이전에는 방산 계약에 묶여있던 통합업체들에게 주류 수익원이 될 수 있습니다.

이 보고서는 제품 유형(풍선, 비행선, 하이브리드), 용도(군사 ISR, 국경 및 해안 감시, 기타), 클래스(소형, 중형, 대형), 최종 사용자 산업(상업용, 군용), 추진 시스템(동력식, 비동력식), 지역(북미, 유럽, 아시아태평양, 기타)으로 구분하여 조사하였습니다. 시장 예측은 금액(USD)으로 제공됩니다.

북미는 통합 국경 보안 개념이 멕시코만에서 태평양에 이르는 다중 센서-항공관제 회랑을 촉진하여 2024년 세계 매출의 45.20%를 차지했습니다. QinetiQ가 TARS를 1억 7,000만 달러에 갱신한 것은 미국 정부의 장기적인 유지 태도를 명확히 했습니다. 캐나다는 북극권 영역 인식을 위해 보완적인 테더 풍선을 채택하고, 멕시코는 원격지 사막 경로의 감시 회랑에 중점을 두어 지상국, 테더, 헬륨 물류의 밸류체인을 확장했습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 14.25%로 가장 가파르게 상승할 것으로 예측됩니다. 해상 분쟁 지역과 광활한 배타적 경제 수역에서는 부족한 초계기 재고를 과도하게 확장하지 않고 영구적인 레이더 피켓이 필요합니다. 일본, 인도, 인도네시아의 현지 통합업체가 엔벨로프 전문가와 제휴하여 제조 현지화, 수입 관세 절감, 주권 데이터 지침 준수에 힘쓰고 있습니다. 몬순의 바람 순환과 염분을 함유한 공기를 견딜 수 있는 하이브리드 풍선은 해양 경비대와 해양 에너지 사업자들의 지지를 받으며 해양 영역에 대한 인식을 높이기 위해 노력하고 있습니다.

유럽은 국경 관리의 압력과 NATO의 준비 의무 덕분에 유력한 구매자로 남아있습니다. 폴란드의 영공 및 지상 레이더 정찰기 구매는 저고도 순항미사일 방어에 대한 동유럽 국가들의 우선순위를 보여줍니다. 서유럽 국가들은 주요 공항 주변에 설치된 에어로스탯을 활용하여 드론의 침입 감지를 개선하고, 유인 헬리콥터를 다른 임무를 위해 다른 임무에 투입할 수 있도록 멀티레이더 센서를 설치했습니다. 유럽방위기금(European Defence Fund) 산하 자금조달 컨소시엄은 고고도에서의 유사 위성 하이재킹에 대한 타당성 연구에 착수했습니다.

The aerostat systems market size reached USD 15.86 billion in 2025 and is forecasted to expand to USD 29.50 billion by 2030, registering a 13.21% CAGR.

Growing reliance on tethered platforms for persistent surveillance, border security, and temporary communications infrastructure has been the principal growth catalyst. Government procurement programs-such as the USD 170 million Tethered Aerostat Radar System (TARS) award covering eight southern-border sites-validated the technology's value proposition and demonstrated budgetary commitment to long-endurance airborne sensors. Traditional balloon designs continued to dominate because they deliver 30-day endurance without fuel burn, while hybrid and powered variants gained traction by offering heavier payloads and limited station-keeping control. Helium-filled aerostats also found expanding roles in disaster-relief telecom backhaul and rural 5G pilots, drawing in commercial stakeholders seeking low-cost, quickly deployable coverage options. Even so, operators must budget for rising helium input prices, develop robust weather-risk procedures, and navigate evolving air-traffic regulations that govern tethered flights.

Southern-border surveillance contracts awarded to QinetiQ in 2025 cemented aerostats as indispensable for continuous wide-area radar and EO/IR coverage. Elevated to altitudes near 15,000 ft, tethered balloons monitored low-altitude incursions and relayed situational data to command nodes for 30 days without a crewed sortie. Israel's Sky Dew program, built with Israel Aerospace Industries hardware and TCOM envelope expertise, provided another benchmark, enabling early warning against small UAVs and cruise missiles. Increasing cross-border trafficking and unmanned air threats, therefore, sustained procurement pipelines as agencies sought persistent but budget-friendly sensing layers.

A single balloon aerostat operating a month between maintenance cycles delivered radar dwell times that no satellite or multirotor UAV could match at a comparable total cost of ownership. Operators avoided fuel, aircrew, and frequent overhaul expenses because tethered lift required only helium top-offs and small ground crews. QinetiQ's TARS fleet documented predictable cost profiles that simplified multi-year budgeting. Rapid roll-out from trailers or modest pads minimized infrastructure outlays, making aerostats attractive for temporary events, emergency missions, or exploratory telecom coverage without tower builds.

Sustained winds above platform limits forced periodic reel-downs that interrupted coverage and raised ground-crew workload. Near-space wind studies showed seasonal velocity peaks that cut effective station time in certain latitudes, pressing operators to adopt stronger tethers, dynamic winches, or powered fins for limited vectoring. Icing and heavy rain added further risk by increasing envelope weight and degrading sensor clarity. Operators, therefore, invested in meteorological forecasting and automated mooring systems to shorten response cycles and protect expensive payloads.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Balloon aerostats generated 56.25% of 2024 revenue as operators favored their mature design, straightforward ground gear, and stable lift characteristics. The aerostat systems market size for balloon platforms is projected to climb steadily, while hybrid architectures outpace in percentage growth. Agencies ran QinetiQ's TARS balloons at 15,000 ft with EO/IR and L-band radar kits, achieving month-long sorties while incurring only helium and crew stipends.

Hybrid models, blending balloon envelopes with aerodynamic fins or semi-rigid frames, will post an 18.01% CAGR to 2030 by accommodating heavier AESA radars and multi-band telecom payloads without sacrificing tether endurance. TCOM's maritime hybrids showed how detachable sea moorings let naval forces reposition sensors overnight without pier infrastructure. The trajectory suggests hybrid systems will capture incremental mission sets-particularly shipboard overwatch and mobile border caravans-while balloons remain the default for fixed-site, low-maintenance surveillance.

Armed-forces users secured 48.52% of the aerostat systems market share in 2024, thanks to program-of-record spending on long-range airborne radar fences. Border-guard agencies leveraged the same airframes for human-tracking radars and counter-UAS receivers, producing scale economies that broadened sustainment pools. Sensitive missions valued persistent line-of-sight sensors that could not be jammed off-route like small drones or forced ablation like satellites.

Telecom-relay duties will be the fastest 16.24% CAGR niche through 2030. Public-safety departments already treat tethered balloons as pop-up LTE towers when hurricanes disable terrestrial networks. Commercial carriers began proof-of-concept deployments in remote valleys, where a single high-gain antenna under a balloon replaced dozens of microcells. As regulators clear spectrum and simplify operating rules, telecom payloads may become a mainstream revenue line for integrators formerly tied to defense contracts.

The Aerostat Systems Market Report is Segmented by Product Type (Balloon, Airships, and Hybrid), Application (Military ISR, Border and Coastal Surveillance, and More), Class (Compact-Sized, Mid-Sized, and Large-Sized), End-User Industry (Commercial and Military), Propulsion System (Powered and Unpowered) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 45.20% of global revenue in 2024 as integrated border-security concepts promoted multi-sensor aerostat corridors from the Gulf of Mexico to the Pacific. QinetiQ's USD 170 million renewal for TARS coverage underscored the US Government's long-term sustainment posture. Canada adopted complementary tethered balloons for Arctic domain awareness, while Mexico weighed surveillance corridors over remote desert routes, extending value chains for ground stations, tethers, and helium logistics.

Asia-Pacific will post the steepest 14.25% CAGR through 2030. Maritime flashpoints and sprawling Exclusive Economic Zones require enduring radar pickets that do not overextend scarce patrol aircraft inventories. Local integrators in Japan, India, and Indonesia partnered with envelope specialists to localize manufacturing, mitigate import duties, and satisfy sovereign data directives. Hybrid balloons that withstand monsoon wind cycles and salt-laden air have found traction with coast guards and offshore energy operators intent on increasing awareness of the maritime domain.

Europe remained an influential buyer thanks to border-management pressures and NATO readiness mandates. Poland's Airspace and Surface Radar Reconnaissance purchase illustrated Eastern-flank priorities for low-altitude cruise-missile defense. Western European states leveraged aerostats around major airports to host multilateration sensors that improve drone intrusion detection while freeing manned helicopters for other duties. Funding consortia under the European Defence Fund earmarked feasibility studies on high-altitude pseudo-satellite hijinks-projects likely to integrate tether innovations to limit launch-risk profiles.