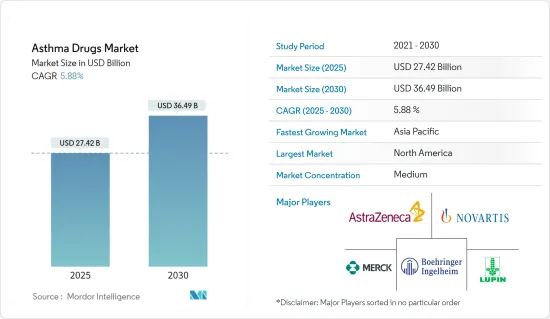

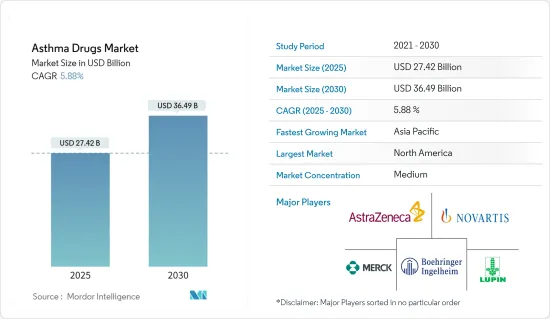

천식 치료제 시장 규모는 2025년에 274억 2,000만 달러, 2030년에는 364억 9,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025-2030년)의 CAGR은 5.88%를 나타낼 전망입니다.

천식의 이환율과 유병률 증가, 노인 증가, 기술의 진보 등의 요인이 천식 치료제 시장의 성장을 뒷받침하고 있습니다.

천식 유병률은 대기 오염, 직업 화학물질 및 분진, 소아기에 빈발하는 하기도 감염, 담배 흡연, 기타 환경 요인 등 다양한 이유로 세계적으로 증가하고 있으며, 이것이 천식 치료제 시장의 성장을 뒷받침하고 있습니다. 세계보건기구(WHO)는 천식을 비전염성 질병(NCDs) 예방 및 관리 글로벌 행동 계획에 포함했습니다. 세계 천식의 날 2023의 최신 정보에 따르면 천식의 유병률은 세계적으로 증가하고 있으며 약 3억 3,900만명이 앓고 있습니다. 이것은 세계적으로 천식 부담이 현저히 높음을 보여주며 천식 치료제 수요를 끌어 올리고 예측 기간 동안 시장 성장을 가속할 가능성이 높습니다.

세계 흡연자 증가는 사람들의 천식 위험을 증가시키고 있습니다. BMC Pulmonary Medicine이 2022년 4월에 발표한 논문에 따르면, 흡연은 다양한 비전염성 질환, 특히 폐암이나 천식 등의 만성 호흡기 질환의 중대한 위험 인자로서 널리 인식되고 있습니다. 담배 연기에 포함된 유해한 화학 물질은 염증이나 호흡기 손상을 일으켜 천식 발병 가능성을 높이거나 기존 증상을 악화시킬 가능성을 높이고 있습니다.

기술의 끊임없는 진화, 특히 바이오마커의 개발은 시장에 큰 기회를 가져올 것으로 기대되고 있습니다. AstraZeneca의 Tezspire(테제퍼맙)는 자기 투여용 프리필드 펜 사용에 대해 인체용 의약품 위원회(CHMP)로부터 긍정적인 의견을 얻었습니다.

따라서 천식 환자 증가와 기술의 진보가 천식 치료제 시장의 성장을 뒷받침하고 있습니다.

단기 작용 베타-2 작용제는 기관지 확대제이며, 기도 평활근 세포를 급속히 이완시켜 기관지 수축을 완화시켜 기류를 개선합니다. 천명, 호흡 곤란, 흉부 압박감, 운동 유발성 기관지 수축(EIB)과 같은 급성 천식 증상을 관리하는 첫 번째 선택 치료입니다. 단기 작용 베타-2 작용제는 알부테롤(살부타몰)과 테르부탈린이 있으며, 주로 정량흡입기(MDI)나 분무기를 이용하여 투여됩니다.

릴리버 요법은 돌발적인 천식 증상의 관리와 중증 천식 발작의 예방에 효과적인 약물 요법으로 중요한 역할을합니다. 단기 작용 베타-2 작용제(SABA)는 신속한 천식 증상의 완화를 위한 효과적인 선택입니다. 정량 흡입기(MDI)의 휴대성과 사용 편의성은 현장 증상 관리에 이상적인 솔루션입니다. 이 특성은 매일 흡입하는 코르티코 스테로이드(ICS)의 규칙적인 요법을 준수하는데 고생하는 환자에게 특히 매력적입니다.

2023년 10월에 World Allergy Organization Journal이 발표한 보고서에 따르면 천식 환자에서 단기 작용 베타-2 작용제의 과다배합은 즉각적인 증상 완화를 위해 이러한 약물에 상당히 의존한다는 것을 시사합니다. 이 패턴은 바람직하지 않은 임상 결과와 관련이 있으며, 환자의 26.7%가 지난 1년 동안 최소 3개의 단기 작용 베타-2 작용제를 투여받았으며, 더 심한 천식과 빈번한 악화와 관련이 있습니다.

병원, 임상 현장, 약국에서 사용되는 단기 작용 베타-2 작용제 제형의 수는 증가하고 있으며, 예측 기간 중에 크게 성장할 것으로 예측됩니다. 2024년 1월, AstraZeneca는 미국에서 AIRSUPRA(알부테롤/부데소니드)를 발매했습니다. AIRSUPRA는 2023년 1월에 천식 증상의 필요에 따라 치료 또는 예방하고 18세 이상의 갑작스러운 중증 호흡 문제(천식 발작)를 예방하는 데 도움을 주기 위해 FDA의 승인을 받았습니다. AIRSUPRA는 기도의 평활근을 이완시키는 단기 작용 베타-2 작용제와 폐의 염증을 억제하는 흡입 코르티코 스테로이드(ICS)가 포함되어 있습니다. ALA 검사에서 에어스플러는 중등증에서 중증 천식 환자에서 심각한 천식 악화 위험 감소에서 알부테롤보다 우수했습니다.

2022년 5월, Teva Pharmaceutical Industries Ltd.의 미국 계열사인 Teva Pharmaceuticals USA Inc.는 2022년 미국 흉부 학회(ATS) 2022년차 총회에서 프로에어 디지헤일러(알부테롤 황산염) 흡입 분말의 객관적인 환자 데이터에 대한 독립 전문가의 컨센서스에 의해 확립된 단기 작용 베타-2 작용제의 사용에 관한 새로운 소견을 발표했습니다. 저축 프로그램의 확대, 신약의 발매, FDA의 승인, 발표된 임상 소견은 단기 작용 베타-2 작용제의 이용 용이성과 채용의 확대에 기여해, 이 시장의 성장을 가속합니다.

단기 작용 베타-2 작용제 시장 성장은 천식 유병률 증가, 이러한 약물에 대한 과도한 의존, 비용 효과, 병용 요법 동향, 최근 제품 출시 및 승인 등의 요인에 의해 촉진되고 접근성과 시장 도입이 강화되고 있습니다.

북미의 천식 치료제 시장은 천식 유병률 증가나 임상 검사나 제품 승인 등 천식 치료제에 대한 대처 증가에 수반하는 천식 치료제의 조성금에 의해 성장이 예상되고 있습니다.

북미에서는 천식이 저소득자, 고령자, 흑인, 히스패닉계, 알래스카 원주민에게 치우쳐 퍼지고 있습니다. 이들 그룹은 천식 이환율, 사망률, 입원률이 가장 높습니다. 예를 들어 미국 천식 및 알레르기 재단이 발표 에 따르면, 미국에서는 2,700만 명 이상이 천식이었습니다. 흑인과 미국 원주민의 성인 사이에서 특히 높습니다. 2023년에 천식으로 진단된 성인 여성은 10.8%, 성인 남성은 6.5%였습니다. 수요가 증가하고 있기 때문에 예측 기간 동안 시장이 견인될 것으로 보입니다.

제품의 승인과 상시 등 시장 진출기업이 채용하는 전략은 제품의 가용성 향상에 기여하고 있어, 이 지역에서 시장의 성장을 가속할 것으로 예측됩니다. 예를 들어 Pulmatrix는 2023년 2월 알레르기성 기관지폐 아스페르길루스증(ABPA)과 천식을 대상으로 첫 환자에게 PUR1900을 투여하는 2b상 검사를 시작했습니다. 이 국제 공동 연구는 천식 환자에게 혁신적인 치료법을 제공하기 위해 Palmatrix와 Ciplar와의 제휴의 일환으로 16 주 동안 약물의 안전성, 내약성 및 효능을 평가하는 것을 목표로합니다. 이 검사의 개념 실증 데이터는 2024년 중반까지 얻을 예정입니다.

2022년 10월, AstraZeneca와 암젠은 중증 천식 성인과 12세 이상의 청소년에 대한 추가 유지 요법을 적응시키는 테즈스파이어(테제퍼맙 주사제)의 캐나다 출시를 발표했습니다. 테즈스파이어의 승인은 PATHWAY 2b상 검사와 NAVIGATOR 3상 검사를 기반으로 했으며 위약과 병용했을 때 중증 천식 환자의 주요 평가 항목과 주요 부차 평가 항목에서 표준 치료에 비해 상당한 개선이 관찰되었습니다. 중증 천식 치료제에서 테즈 스파이어의 효능이 입증됨에 따라 천식 치료제에 대한 수요가 증가하고 예측 기간 동안 시장 성장을 이끌 것으로 예측됩니다.

천식 부담과 유병률 상승, 천식 치료제 출시, 임상 검사, 투자에 주력하는 제조업체 등의 요인이 예측 기간 동안 북미 천식 치료제 시장의 성장을 뒷받침할 것으로 예측됩니다.

천식치료제 시장은 적당히 세분화되어 있습니다. 성장 기회를 위해 천식치료제 시장에는 많은 신규 진입기업이 나타나고 있습니다. 의약품 시장이 더욱 활성화될 것으로 예측됩니다. PLC, Boehringer Ingelheim GmbH, Novartis AG, Sanofi SA, Merck & Co.Inc. 등이 있습니다.

The Asthma Drugs Market size is estimated at USD 27.42 billion in 2025, and is expected to reach USD 36.49 billion by 2030, at a CAGR of 5.88% during the forecast period (2025-2030).

Factors such as an increase in the incidence and prevalence of asthma, the growing geriatric population, and technological advancements are boosting the growth of the asthma drug market.

The prevalence of asthma is increasing globally due to various reasons, such as air pollution, occupational chemicals and dust, frequent lower respiratory infections during childhood, tobacco smoking, and other environmental factors, which boost the growth of the asthma drug market. World Health Organization (WHO) included asthma in the Global Action Plan for the Prevention and Control of Noncommunicable Diseases (NCDs). As per the latest update on World Asthma Day 2023, the prevalence of asthma is increasing globally, affecting approximately 339 million people. This showed a significantly high burden of asthma globally, likely to boost the demand for asthma drugs and propel the market's growth over the forecast period.

Rising cases of smoking worldwide are increasing the risk of asthma in people. For instance, according to an article published by BMC Pulmonary Medicine in April 2022, smoking was widely recognized as a significant risk factor for various noncommunicable diseases, notably lung cancer and chronic respiratory conditions such as asthma. The harmful chemicals in tobacco smoke can cause inflammation and damage to the respiratory system, increasing the likelihood of developing asthma or exacerbating existing symptoms. Thus, the increasing number of cases of tobacco smoking is raising the demand for asthma drugs for their treatment.

The continuous evolution of technology, particularly in the development of biomarkers, is expected to create significant opportunities for the market. The inherent limitations of conventional treatments, such as delayed therapeutic effects and reduced effectiveness, drive the market toward the innovation of new targeted therapies. This shift is anticipated to fuel market growth. For instance, in January 2023, AstraZeneca's Tezspire (tezepelumab) received a positive opinion from the Committee for Medicinal Products for Human Use (CHMP) for its use in a prefilled pen for self-administration. This approval, which allows patients with severe asthma aged 12 years and older to self-administer the drug, enhances the flexibility and convenience of treatment options.

Therefore, increasing cases of asthma and technological advancements are propelling the growth of the asthma drug market. However, stringent government regulations for product approval and side effects associated with drugs are restraining the market growth.

Short-acting beta-2 agonists are bronchodilators, rapidly relaxing airway smooth muscle cells to relieve bronchoconstriction and improve airflow. They are the first-line treatments for managing acute asthma symptoms such as wheezing, shortness of breath, chest tightness, and exercise-induced bronchoconstriction (EIB). Most used short-acting beta-2 agonists include albuterol (salbutamol) and terbutaline, primarily delivered via metered-dose inhalers (MDIs) or nebulizers.

Reliever therapy plays a critical role in effective medications in managing sudden asthma symptoms and preventing severe asthma attacks. Short-acting beta-agonists (SABAs) are a prominent choice for quick relief due to their rapid onset of action. The portability and user-friendliness of metered-dose inhalers (MDIs) make them an ideal solution for on-the-spot symptom management. This characteristic is especially attractive to patients who struggle to adhere to the regular regimen of daily inhaled corticosteroids (ICS).

According to a report published by the World Allergy Organization Journal in October 2023, the overprescription of short-acting beta-2 agonists among asthma patients suggests a considerable dependency on these medications for immediate symptom relief. This pattern is linked to unfavorable clinical outcomes, with 26.7% of patients receiving at least three canisters of short-acting beta-2 agonists over the past year, correlating with more severe asthma and frequent exacerbations.

The rising number of short-acting beta-2 agonist products used in hospitals, clinical settings, and pharmacies is expected to grow significantly during the forecast period. As more hospitals and clinics adopt these products, the segment will likely experience a considerable growth surge over the coming years. For instance, in January 2024, AstraZeneca launched AIRSUPRA (albuterol/budesonide) in the United States. AIRSUPRA received FDA approval in January 2023 for the as-needed treatment or prevention of asthma symptoms and to help prevent sudden severe breathing problems (asthma attacks) in people aged 18 years and older. Airsupra contains a short-acting beta2-agonist to help relax the smooth muscles of the airways and an inhaled corticosteroid (ICS) to help decrease lung inflammation. Airsupra was approved based on the results from two Phase III trials: MANDALA and DENALI. In MANDALA, AIRSUPRA was superior to albuterol in reducing the risk of severe asthma exacerbations in patients with moderate to severe asthma. In DENALI, AIRSUPRA had a similar onset of bronchodilation compared to albuterol in patients with mild to moderate asthma.

In May 2022, Teva Pharmaceuticals USA Inc., a US affiliate of Teva Pharmaceutical Industries Ltd, published new findings at the 2022 American Thoracic Society (ATS) 2022 Annual Meeting for short-acting beta-2 agonist use established by independent expert consensus to objective patient data from ProAir Digihaler (albuterol sulfate) Inhalation Powder. Expanded savings programs, new medication launches, FDA approvals, and published clinical findings contribute to greater accessibility and adoption of short-acting beta-2 agonists, driving the growth of this market.

The growing market for short-acting beta-2 agonists is driven by factors such as increasing asthma prevalence, over-reliance on these medications, cost-effectiveness, combination therapy trends, and recent product launches and approvals, enhancing accessibility and market adoption.

The asthma drug market in North America is expected to grow due to the increasing prevalence of asthma and grants of asthma drugs with the increasing number of initiatives for them, such as clinical trials and product approvals. Robust healthcare infrastructure, better reimbursement policies, increased funding, and availability of advanced asthma drugs in the country are boosting the market's growth in North America.

In North America, asthma is spread disproportionately among people with low income, senior adults, and Black, Hispanic, and Alaska Native people. These groups have the highest asthma rates, deaths, and hospitalizations. For instance, as per the data published by the Asthma and Allergy Foundation of America in September 2023, more than 27 million people in the United States had asthma. This corresponded to 1 in 12 people, or more than 22 million people, in the United States. Adults aged 18 and older had asthma; about 4.5 million children under the age of 18 had asthma in 2022. Asthma rates are particularly high among Black and Indigenous American adults in the United States. Additionally, the condition is more prevalent among female adults than male adults; about 10.8% of female adults and 6.5% of male adults were diagnosed with asthma in 2023. The growing prevalence of asthma in the country is expected to drive the market during the forecast period, as the increasing number of individuals with asthma creates a higher demand for effective treatment and management solutions. The market is likely to respond to this trend with a greater focus on developing and delivering targeted asthma treatments to meet the needs of these high-risk groups.

The strategies employed by market players, such as product approvals and launches, are contributing to increased product availability, which is expected to drive the market's growth in the region. For instance, in February 2023, Pulmatrix initiated a Phase 2b trial, with the first patient dosed with PUR1900, targeting Allergic Bronchopulmonary Aspergillosis (ABPA) and asthma. This global trial was intended to evaluate the safety, tolerability, and efficacy of the drug over a 16-week period, forming part of Pulmatrix's partnership with Cipla to deliver innovative therapies for asthma patients. The proof-of-concept data from this study is anticipated by mid-2024.

In October 2022, AstraZeneca and Amgen announced the Canadian availability of Tezspire (tezepelumab injection), which was indicated as an add-on maintenance treatment for adults and adolescents aged 12 and older with severe asthma. The approval of Tezspire was based on the PATHWAY Phase IIb and NAVIGATOR Phase III trials, which showed significant improvements in primary and key secondary endpoints in patients with severe asthma, compared to a placebo, when used alongside standard therapy. Due to Tezspire's proven efficacy in treating severe asthma, the demand for asthma treatments is expected to increase, driving the market's growth over the forecast period.

Factors such as the rising burden and prevalence of asthma, manufacturers focusing on launches, clinical trials, and investments in asthma drugs are expected to boost the growth of the asthma drug market in North America during the forecast period.

The asthma drugs market is moderately fragmented. Due to the growth opportunities, many new players are emerging in the asthma drug market. Forthcoming patent expiries of major drugs are expected to increase competition, further driving the market, especially in the generic sector. The market is expected to grow significantly, with several generic players controlling significant market shares in the developing regions. Some of the market players include AstraZeneca PLC, Boehringer Ingelheim GmbH, Novartis AG, Sanofi SA, and Merck & Co. Inc.