북미의 우주 추진 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 성장 예측

North America Space Propulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693953

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

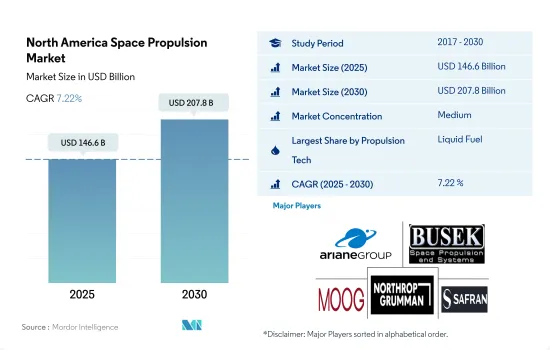

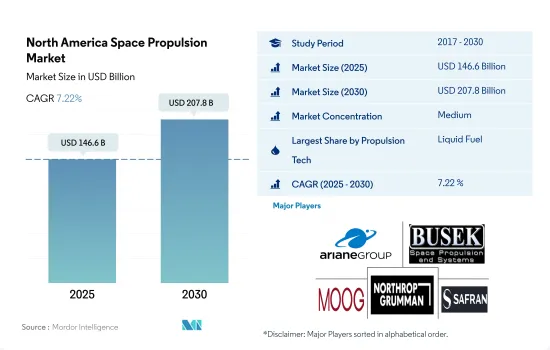

북미의 우주 추진 시장 규모는 2025년에 1,466억 달러로 추정되고, 2030년에는 2,078억 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 7.22%를 보일 것으로 예측됩니다.

거액의 우주 관련 투자에 관여하는 대기업과 우주 기관이 촉진요인

위성의 추진 시스템은 우주선을 궤도로 추진하고 그 위치를 조정하기 위해 일반적으로 사용됩니다.

가스 추진 시스템은 효율성과 신뢰성이 입증된 움직임을 가능하게 합니다. 이 시스템은 강한 추력이나 신속한 조종이 필요한 경우에 사용됩니다.

한편, 전기 추진은 상업 통신 위성의 스테이션 유지에 일반적으로 사용되고 있습니다. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, Blue Origin은 이 지역의 추진 시스템의 주요 공급기업입니다. 액체 추진 시스템은 고체 추진에 비해 비추력이 높기 때문에 위성의 효율이 높고 운영 수명이 길어집니다. NASA와 같은 주요 우주 기관 및 선도기업은 거액의 투자를 통해 연구개발에 많은 비용을 사용하므로 지속적인 기술 혁신과 보다 효율적이고 선진적 기술의 개발이 가능합니다.

추진 기술의 제품 혁신이 성장을 뒷받침할 전망

북미의 우주 추진 시장은 민간 섹터의 진입이 현저하게 증가하고 있습니다.

전기 추진 시스템 중에서도 특히 이온 추진과 홀 효과 스러스터가 산업에서 각광을 받고 있습니다.

북미는 세계적으로도 주요 시장 중 하나이며, 특히 미국에서 일어나는 강력한 우주 탐사 및 개발 활동이 그 이유입니다.

이 지역의 다양한 정부, 상업, 기타 참가 기업에 의해 위성 제조 산업 수요는 긍정적으로 성장하고 있습니다.

북미 우주 추진 시장 동향

북미 우주 추진 시장의 투자 기회

우주 프로그램에 대한 투자는 기술 혁신을 촉진하고 위성 추진 시장의 번영을 촉진하고 있으며 미션의 수명 연장에 중요한 역할을 하고 있습니다. 예를 들어, 2023년 2월, NASA는 연구 보조금으로 3억 3,300만 달러를 분배했습니다. 캐나다 우주국의 예산은 적정 수준이며 2022-2023년의 예산 지출 전망액은 3억 2,900만 달러였습니다.

NASA는 태양 전기 추진(SEP) 개발에 9,800만 달러를 지원받을 전망입니다. 2021년 3월, NASA, Maxar Technologies, 그리고 Busek Co.는 PPE에 탑재되는 6킬로와트(kW)태양전기 추진 서브 시스템의 테스트를 성공적으로 완료하였습니다.

북미 우주 추진 산업 개요

북미 우주 추진 시장은 적당히 통합되어 상위 5개사에서 52.89%를 차지하고 있습니다. 주요 기업으로는 Ariane Group, Busek Co. Inc., Moog Inc., Northrop Grumman Corporation, Safran SA(알파벳순) 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

우주 개발에의 지출

규제 프레임워크

캐나다

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

추진 기술

전기

가스

액체 연료

국가명

캐나다

미국

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Ariane Group

Blue Origin

Busek Co. Inc.

Moog Inc.

Northrop Grumman Corporation

OHB SE

Safran SA

Sierra Nevada Corporation

Space Exploration Technologies Corp.

Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The North America Space Propulsion Market size is estimated at 146.6 billion USD in 2025, and is expected to reach 207.8 billion USD by 2030, growing at a CAGR of 7.22% during the forecast period (2025-2030).

Major players and space agencies, involved in high space-related investment is the driving factor

A satellite's propulsion system is commonly used to propel a spacecraft into orbit and coordinate its position. A liquid propellant rocket or liquid rocket utilizes a rocket engine that uses liquid propellants. Gas propellants may also be used but are not expected due to their low density and difficulty in applying conventional pumping methods. Liquids are desirable as they have a reasonably high density and specific impulse.

Gas-based propulsion systems enable movements that have been proven efficient and reliable. These systems include hydrazine systems, other single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid fuels. These systems are used when strong thrust or rapid manoeuvring is required. Therefore, gas-based propulsion systems remain the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements.

On the other hand, electric propulsion is commonly used to hold stations for commercial communication satellites. It is the main propulsion of some space science missions due to its high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems in the region. Liquid propulsion systems offer higher specific impulses compared to solid propulsion, resulting in greater efficiency and longer operational life for satellites. Major players and space agencies, like NASA, are involved in high space-related investments, enabling them to spend more on R&D and allowing them to innovate continuously and develop more efficient and advanced technologies. Launching new satellites in the region is expected to accelerate the market's growth during the forecast period.

Product innovation in propulsion technology is expected to boost growth

The North American space propulsion market has witnessed a significant rise in private sector participation. Companies like SpaceX, Blue Origin, and Rocket Lab have emerged as key players, developing innovative propulsion technologies and reducing launch costs. This trend has led to increased competition and accelerated advancements in the field.

Electric propulsion systems, particularly ion propulsion and Hall-effect thrusters, have gained prominence in the industry. These systems offer higher efficiency, longer operational lifetimes, and the capability for deep space missions. They are used in commercial and government space missions, including satellites and interplanetary probes.

North America is one of the major markets globally, especially due to strong space exploration and development activity in the United States. NASA invests in start-ups to develop advanced propulsion systems for small satellites. NASA is also working on the Solar Electric Propulsion (SEP) project, which aims to extend the duration and capabilities of ambitious discoveries and science missions.

Due to various government, commercial, and other players in the region, the demand in the satellite manufacturing industry is growing positively. During 2017-2022, 4,300+ satellites were launched in the region, aiding the space propulsion market. In addition to the number of such investments and technological developments, North America is expected to lead the market globally during the forecast period.

North America Space Propulsion Market Trends

Investment opportunities in the North American space propulsion market

Investments in space programs are driving technological innovations and fostering the thriving satellite propulsion market. R&D initiatives associated with space programs lead to the creation of new propulsion systems, which offer increased efficiency and longer operational lifetime. These propulsion systems play a crucial role in spacecraft maneuvering, orbit maintenance, and mission longevity. The region's government and the private sector have dedicated funds for research and innovation in the space sector in terms of grants. In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. For instance, in February 2023, NASA distributed USD 333 million as research grants. Additionally, in 2022, the US government spent nearly USD 62 billion on its space programs, making it the world's highest spender in the space sector. Apart from the United States, the Canadian Space Agency budget is modest, and the estimated budgetary spending for 2022-23 is USD 329 million. In terms of funds allocated for NASA under the president's budget request summary for FY 2022-2027, NASA is expected to receive USD 45 million for the development of space power and nuclear propulsion.

NASA is expected to receive USD 98 million to develop solar electric propulsion (SEP). In March 2021, NASA, Maxar Technologies, and Busek Co. completed a test of the 6-kilowatt (kW) solar electric propulsion subsystem successfully destined for the PPE. The Solar Electric Propulsion project was anticipated to receive the first qualification thruster from Aerojet Rocketdyne at the beginning of the first quarter of FY 2023. The government allocated funding of USD 110 million for developing nuclear thermal propulsion systems.

North America Space Propulsion Industry Overview

The North America Space Propulsion Market is moderately consolidated, with the top five companies occupying 52.89%. The major players in this market are Ariane Group, Busek Co. Inc., Moog Inc., Northrop Grumman Corporation and Safran SA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Spending On Space Programs

4.2 Regulatory Framework

4.2.1 Canada

4.2.2 United States

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Propulsion Tech

5.1.1 Electric

5.1.2 Gas based

5.1.3 Liquid Fuel

5.2 Country

5.2.1 Canada

5.2.2 United States

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).